What Could Go Wrong? ‘Basel III Endgame’ Stress Sparks Rebirth Of “Synthetic Credit Risk Sharing”

Ironically, on a day when Fed Chair Powell spent a large portion of his time discussing the new regulatory threats from Basel Endgame rules – that force banks to hold more capital, less risk – BlackRock has published a report that is forecasting rapid growth for transactions that allow banks to shed risk in their loan portfolios.

The freshly re-branded Synthetic Risk Transfer (SRT) deals, are simply credit-linked notes (which have been relatively uncommon since the great financial crisis) offering high (mid-double-digit) yields for borrowers willing to accept the implied credit default swap (that effectively transfers the credit risk tied to a pool of loans – such as CREs).

Specifically, in SRT transactions, a bank earmarks a pool of assets on its balance sheet and buys credit default protection on the first 5% to 15% of the losses of that pool, so if losses materialize, the holders of the SRTs absorb the hit, according to BlackRock.

The renaissance of these vehicles is driven by a combination of higher rates (which are among the main factors that have crushed CRE loan values) and forthcoming Basel III regulations that will force banks to hold more capital to cover potential losses.

“With volatile interest rates and origination volumes, combined with increasing regulatory requirements, synthetic transactions are making more sense and are expected to pick up meaningfully in the near future,” said Chris Hentemann, chief investment officer and founder of hedge fund 400 Capital Management.

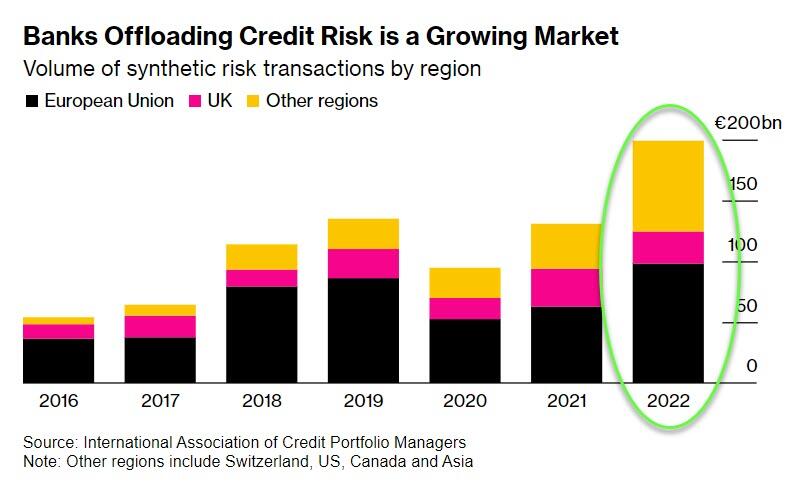

Bloomberg reports that last year banks around the world sold $25 billion of SRTs partially offloading the risk of $300 billion of loans, according to an estimate by Pemberton Asset Management.

While European banks have been the biggest users of such transactions in previous years, the big rise in SRT volumes will come from large Wall Street banks under pressure to boost their regulatory capital requirements, according to William Im, a director in BlackRock’s global opportunistic credit team.

“Given greater acceptance of this as a tool and ongoing Basel III endgame regulatory pressures, there is a real world in which this market has a potential to grow at 30-to-40% each year for the next two years,” Im said.

The growth trajectory Im envisions “sounds like a stark number, but if you compare investor demand as well as bank demand that well may be the case,” he said.

In its paper, BlackRock cited the collapse of the Silicon Valley Bank and other regional banks as a factor driving growth in the market for regulatory capital securities.

Rising rates and increased risk weightings mean “it’s not easy to be a bank CEO right now,” Joel Holsinger, co-head of alternative credit at Ares, said.

“It is a truly transformational moment.”

However, it is notably that Chair Powell’s comments today on the Basel III endgame likely signal there’s little chance a rule is finalized this year. Bloomberg Intelligence senior government analyst Nathan Dean notes that with the elections coming closer and closer, it’s more likely the Fed hits the brakes on the proposal or re-proposes the rule. We currently ascertain a 60% chance of a re-proposal.

But, given the wave of marketing for SRTs, we suspect, the inevitability of higher capital requirements will do nothing to slow the growth of this trade.

We have seen this movie before though: of course, the quants have their models, perfectly calibrated to ‘synthetically transfer’ that risk at a premium that pays big bonuses, but after scraping away the copulas and the codependencies, this is nothing more than a game of hot-potato (who can hold the potato long enough to earn a decent yield before it permanently scars your ‘hand’).

Of course, there is always the embedded option of The Fed Put. Should the fecal matter truly strike the rotating object, let history be a lesson, Federal-Reserve-Backed SPVs will come to the rescue to re-collateralize the new TBTF market participants.

Tyler Durden

Wed, 03/06/2024 – 20:00

via ZeroHedge News https://ift.tt/iHXR5tT Tyler Durden