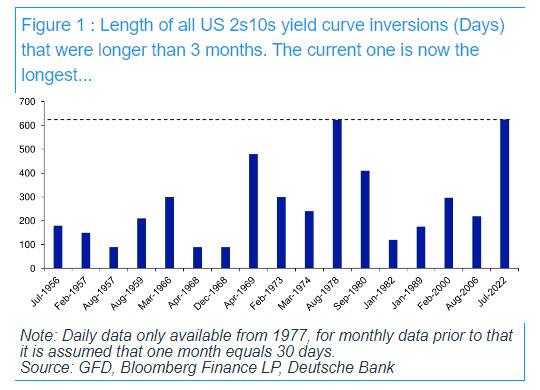

After 625 Days, The Longest Yield Curve Inversion In History

Today is a historic day, as last night – DB’s Jim Reid reminds us – we quietly passed the longest continuous US 2s10s inversion in history. After the 2s10s first inverted at the end of March 2022, it has now been continuously inverted for 625 days since July 5th 2022. That exceeds the 624 day inversion from August 1978, which previously held the record.

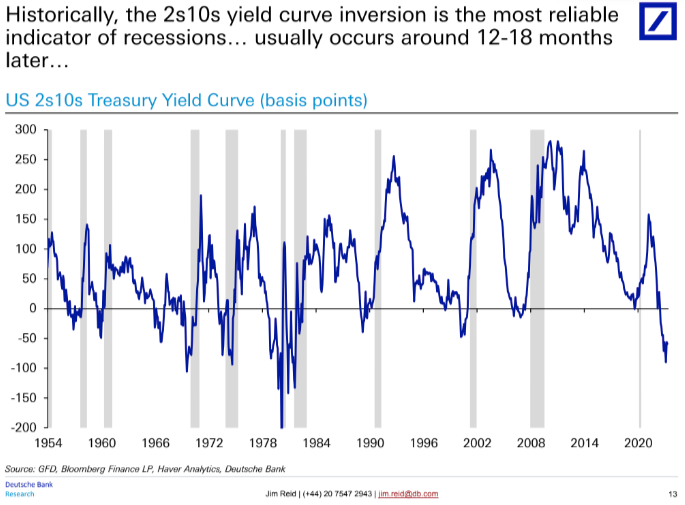

As regular readers are aware, an inverted yield curve has been the best predictor of a US downturn of any variable through history: the yield curve has always inverted before all of the last 10 US recessions, with a lag that is usually 12-18 months, but some cycles – certainly this one – take longer…. much longer.

In fact, the lack of a recession so far has prompted Red to ask – in his latest Chart of the Day note – if the inverted yield curve recession indicator has failed this cycle?

“Possibly”, the DB strategist responds, “but in many ways the yield curve has already accurately predicted many of the drivers that would normally lead to a recession. However, these variables haven’t then created recessionary conditions as they normally would have done.” He explains:

It led, as it always does, the very sharp deterioration in bank lending standards, and led the declines in bank credit and money supply that are almost unique to this cycle. It was also at the heart of why we had some of the largest bank failures on record with SVB, Signature Bank and First Republic collapsing. A significant part of their failure was a big carry trade that went wrong when the curve inverted.

However, even with the above, a recession – according to the highly political “recession authority” known as the NBER – hasn’t materialised. This is perhaps because of the following.

- When lending standards were at their tightest, the borrowing needs of the economy were low relative to previous cycles.

- Excess savings have been unusually high in this cycle (and were revised higher with the GDP revisions last September), so consumers haven’t been as exposed to tight credit as they normally are.

- The Fed unveiled a huge series of measures to ensure the regional bank crisis didn’t naturally unravel as it would have done in a free market or perhaps in many previous cycles.

- Whilst the Fed’s tightening has been reducing demand, the supply-side of the economy has bounced back strongly from the pandemic disruption, which has further supported growth and made this cycle unique.

So far so good, however, an inverted yield curve should ultimately be a significant headwind for an economy, as capitalism works best when there is a positive return for taking more risk with lending and investments further out the curve. As such, Reid notes, “the rational investor should be prepared to keep more of their money at the front end, or not lend long-term when the curve is inverted” as you are not giving up yield for being able to sleep at night.

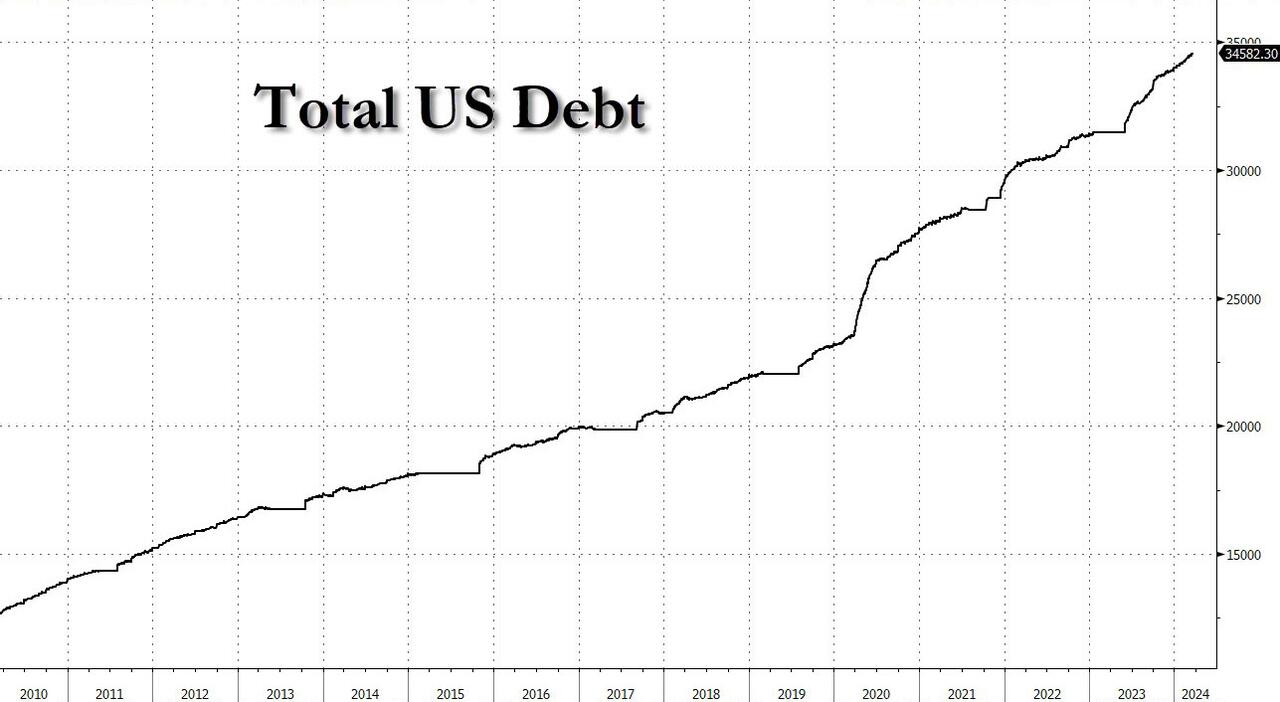

So thanks to a historic flood of fiscal stimulus and a daily orgy of new record debt as discussed earlier…

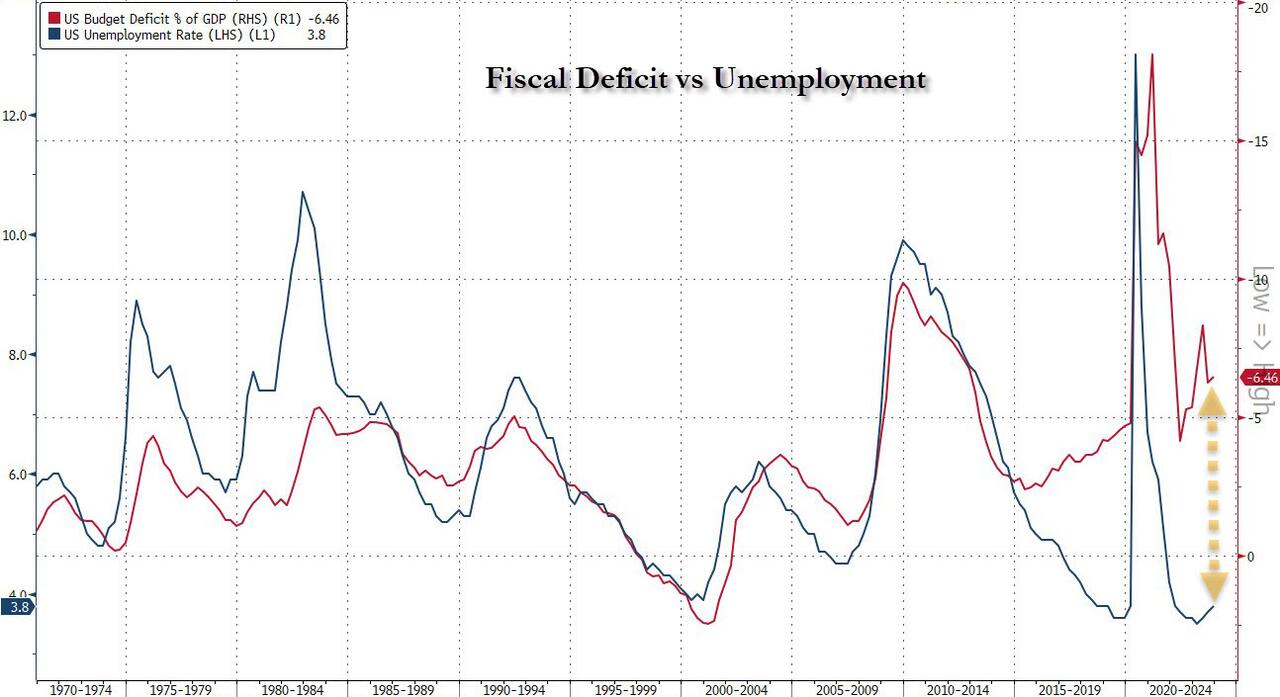

… which means that the US is now running a 6.5% deficit with unemployment near “historical lows”, an unheard of event….

… the economy has not succumbed to the inverted yield curve to date, but while it remains inverted the Fed is encouraging more defensive behavior at some point if sentiment changes. As such, the DB strategist concludes that “the quicker we get back to a normal sloping yield curve the safer the system is.”

Tyler Durden

Thu, 03/21/2024 – 22:20

via ZeroHedge News https://ift.tt/p3os2bB Tyler Durden