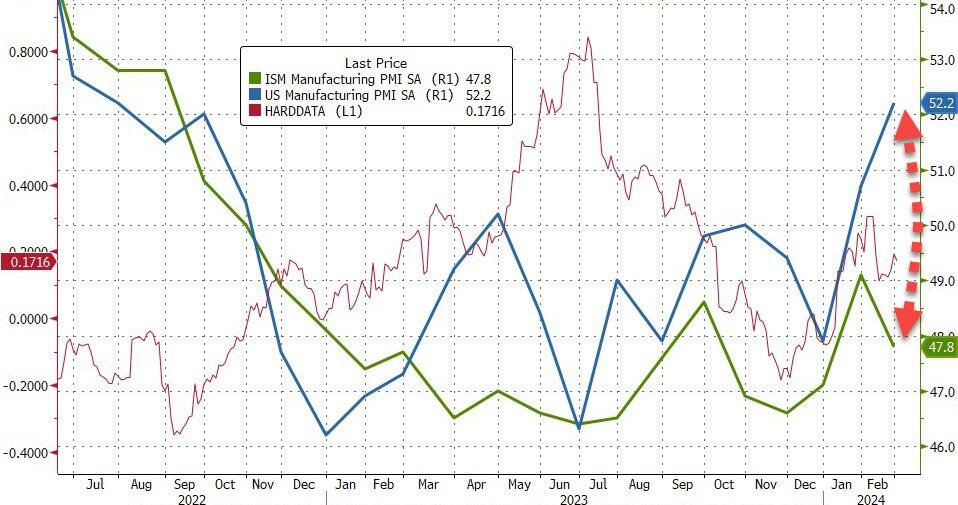

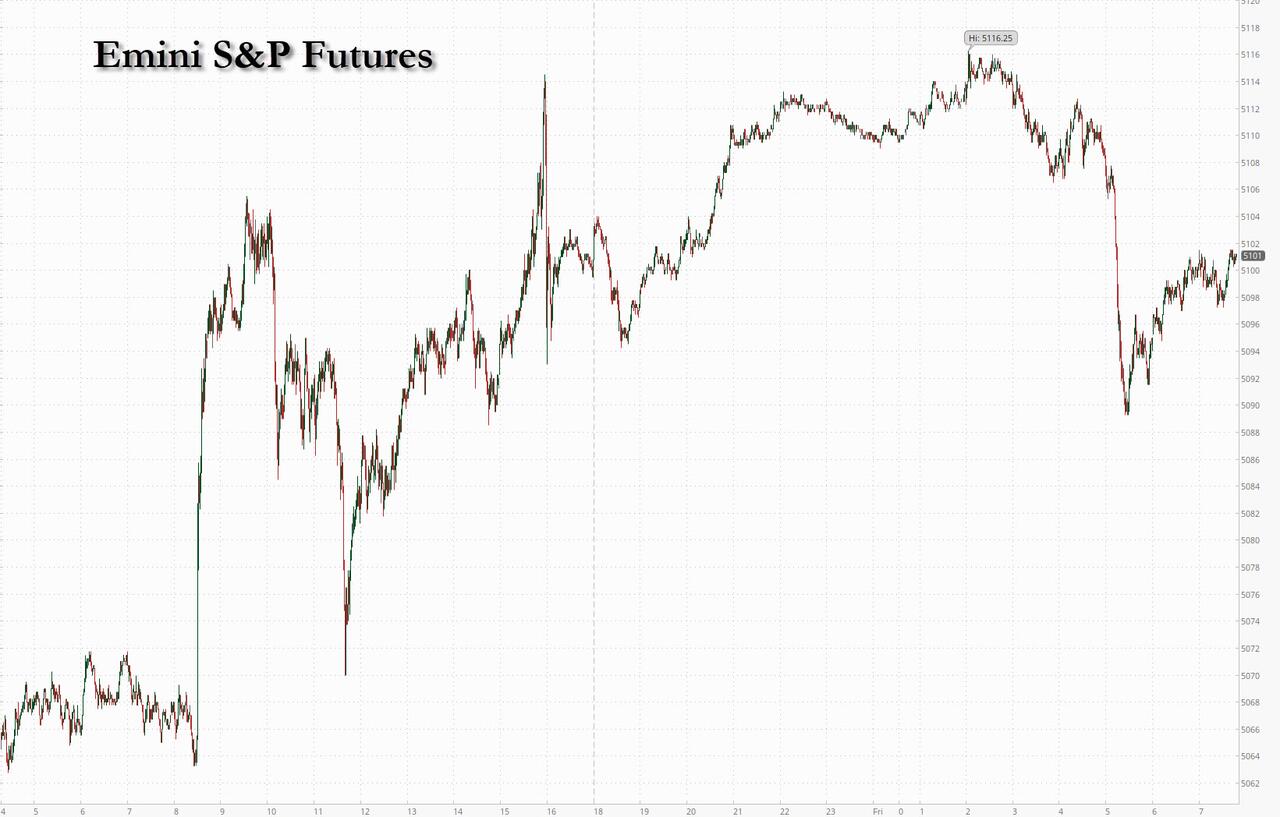

US stock futures briefly fell to a session low – then quickly recovered – as Apple slumped in premarket trading after Goldman removed the company from its conviction buy list (but retained a buy rating). As of 8:00am, S&P and Nasdaq futures traded flat and European stocks retreated from their highs as the relief rally which sent US stocks to an all time high on Thursday encouraged by an in-line reading on core PCE faded, while New York Community Bancorp plunged more than 30% in Friday’s premarket after identifying “material weaknesses” in how it tracks loan risks. Europe’s Stoxx 600 gained 0.5%, reversing an earlier dip, after Euro area inflation printed hotter than expected. Treasury yields are lower, the dollar is flat, and bitcoin is higher and back over $62,000. Today, focus will be the ISM-Mfg report at 10am ET (exp. 49.5 survey vs. 49.1 prior). Keep an eye on ISM-Mfg Prices Paid: consensus sees prices to grow again: 53.2 vs. 52.9

In premarket trading, NYCB tumbled as much as 30% after the troubled commercial real estate lender said it discovered “material weaknesses” in how it tracks loan risks, wrote down the value of companies acquired years ago and replaced its CEO to grapple with the turmoil. Dell Technologies soared 21% after its results beat expectations, boosted by the buzz around artificial intelligence. Apple fell 0.6% as Goldman removed the stock from its conviction list, while keeping a buy rating. It also removed Merck and Vertex Pharmaceuticals from its conviction list, replacing them with Amgen, Monday.com and Vulcan Materials. Here are some other notable movers:

- Caret Holdings shares jump 10% after the insurance technology company was upgraded to buy from hold at Jefferies and the broker raised its price target to a Street high.

- Eli Lilly gains 1.6% after BofA Global Research raised its price target on the weight-loss drugmaker to a Street-high of $1,000 on continued upside for its diabetes and obesity programs.

- Everbridge jumps 25% after the software firm said Thoma Bravo agreed to boost its acquisition price for the company by $6.40 per share to $35.00 per share, after it received a higher bid during the “go-shop” period.

- Ginkgo Bioworks shares slide 14%, after the synthetic biology firm’s forecast for the year disappointed, with Cowen saying that its guidance and quarter were “underwhelming” and noting that the company attributed the revenue decline to the biosecurity unit’s transition, and the lumpy impact of equity milestones that did not recur in 2023.

- HP Enterprise falls 5.6% after the computer hardware and storage company narrowed its adjusted earnings per share forecast for the full year. The firm cited cooling demand for networking products and a lack of availability of graphics processor units required to deliver high-powered servers.

- Humacyte falls 24%, after the biotech company offered shares to raise about $40 million at a 31% discount.

- New York Community Bancorp falls 21% after the company said it identified material weaknesses in its internal controls related to internal loan reviews. NYCB also replaced its CEO, saying that Executive Chairman Alessandro DiNello will take on the role.

- Senseonics shares drop 8.9% after the medical technology company reported fourth-quarter results. While the company beat expectations, Raymond James flagged the slower-than-expected adoption of Eversense.

- SoundHound AI falls 22%, with the voice AI software company retreating in the wake of its fourth-quarter results, as well as a massive rally in the stock price. Analysts are mixed on the report, and Cantor notes concerns about valuation.

- Sweetgreen jumps 20% after the salad chain’s first-quarter revenue forecast came ahead of expectations. Additionally, the company reported fourth-quarter same-store sales that were better than consensus. William Blair called the print a “sweet end” to the year.

Equity sentiment turned more cautious following Thursday’s core PCE data – t he Fed’s preferred inflation measure – which rose in January at the fastest pace in nearly a year, but matched economist forecasts. Traders were also comforted by jobless claims data that indicated labor-market softening. “The data came as a relief for those who were prepared for the worst,” said Ipek Ozkardeskaya, senior analyst at Swissquote Bank.

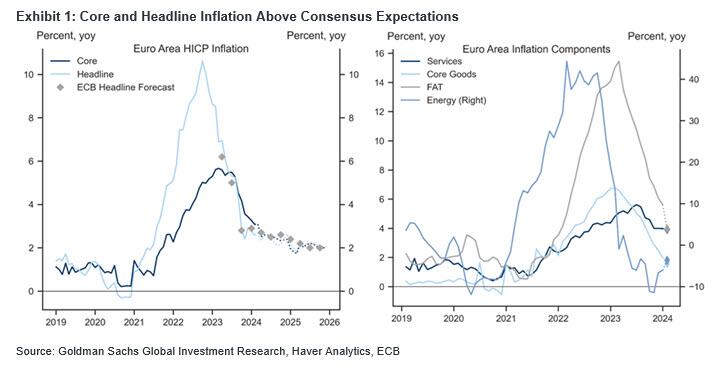

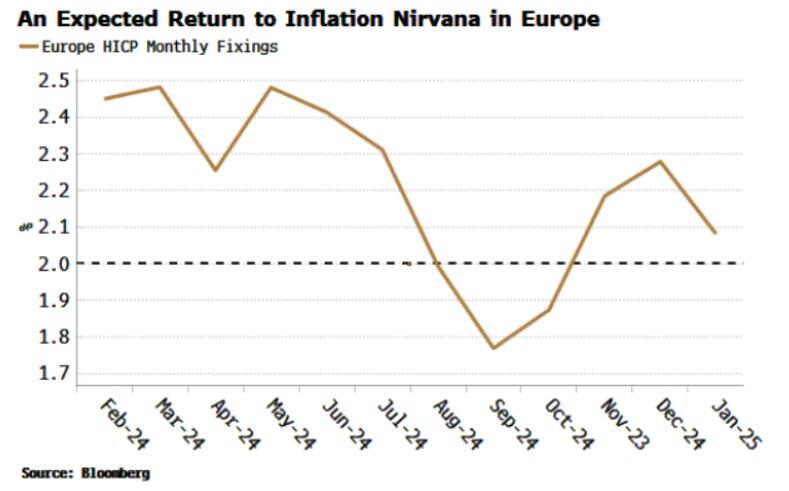

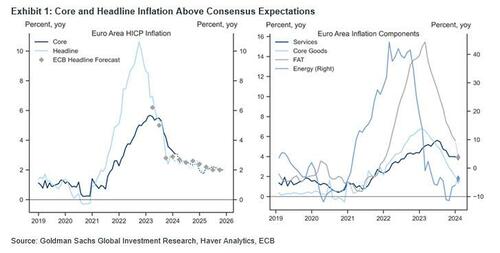

On the monetary policy front, euro-zone inflation eased less than anticipated in February — supporting European Central Bank officials who don’t want to rush into lowering rates. Meanwhile, Thursday’s US PCE report appeared not to dent the broader disinflationary trend underpinning rate-cut forecasts.

Federal Reserve Bank of San Francisco President Mary Daly said central bank officials are ready to lower interest rates as needed, but emphasized there’s no urgent need to cut given the strength of the economy. Her Atlanta counterpart Raphael Bostic said the central bank could begin cutting this summer. “For markets keenly focused on when the Fed will transition toward easing rates, this report will help restore confidence that it isn’t ‘if’ the Fed will begin to cut rates in 2024, but ‘when,’” said Quincy Krosby at LPL Financial.

Meanwhile, Bank of Americas’s Michael Hartnett said Chinese stock funds saw the largest weekly outflow since October, as the government seeks to stem a decline in the equity market. About $1.6 billion was pulled from Chinese funds in the week through Feb. 28, Hartnett wrote citing EPFR Global data. Beijing is attempting to restore market confidence after years of decline and slowing growth following the pandemic. As the turmoil deepened in recent months, the authorities have stepped up measures to help bolster sentiment, including restricting short selling and cracking down on high-speed trading.

European stocks advanced 0.5%, reversed earlier weakness after Eurozone CPI came in hotter than expected; banks and automobile shares leading gains, while construction and media stocks are the biggest laggards. Here are the biggest European movers:

- Daimler Truck shares rise as much as 15% to a record after the German truck maker posted fourth quarter results that were described “strong” by analysts, thanks to North American orders and the Mercedes-Benz trucks division

- IMCD shares rise as much as 10%, the biggest jump since August 2021, after the Dutch chemicals distributor reported margins that were better than analysts had expected

- Grifols shares jumped as much as 22%, rebounding from a 35% record decline on Thursday, after the Spanish plasma company said a key deal is coming closer to completion

- ITV shares jump as much as 16%, marking their biggest gain since April 2020, after the broadcaster sold its stake in streaming service BritBox and announced the net proceeds will be returned to shareholders through a buyback

- Bekaert gains as much as 9.1%, hitting the highest level since May 2017, with analysts planning to increase their 2024 estimates following the Belgian steel wire company’s results and outlook

- Corbion gains as much as 7.2% after the Dutch ingredients maker proposed a 9% dividend hike on the back of positive free cash flow momentum. Degroof Petercam analyst Fernand De Boer anticipates this could be followed by share buybacks

- Rightmove shares fall as much as 5.3%, the worst performance in the Stoxx 600 Real Estate Index on Friday, after the properly listings portal reported results that were in line with expectations

- IMI shares fall as much as 3.2%, extending losses into a fifth consecutive session, after the engineering firm’s EPS guidance for this year came in slightly below expectations, according to Liberum

- Acerinox declined 7.8% in early trading in Madrid, most since July 2022, after the Spanish stainless steel producer missed estimates and gave a weaker first-quarter outlook that Morgan Stanley says suggests high-single-digit downgrades to consensus Ebitda for 2024

- AMS-Osram’s shares extend drop after Thursday’s plunge of almost 40%, declining another 8.3% after Stifel cut the recommendation on the Swiss chipmaker to hold from buy

Earlier in the session, Asian stocks rose with Japan’s Nikkei 225 climbing 1.9% to its strongest-ever close near the 40,000 mark. Asian equities kickstarted March with gains after registering their best February performance in nine years, buoyed by a climb in Japan and China. The MSCI Asia Pacific Index rose as much as 0.5% , with technology and consumer discretionary stocks among the main advancers. Shares climbed on the mainland and Hong Kong ahead of next week’s crucial National People’s Congress meeting, where traders are awaiting more policy support from Beijing. Chinese authorities will likely display “a sense of urgency to show that there is no acceleration in this deflationary environment,” Xavier Baraton, global CIO at HSBC Global Asset Management in France, told Bloomberg television. “Valuations are extremely attractive, which means limited downside for us.”

In FX, the Bloomberg Dollar Spot Index rose 0.1%. The yen was the weakest of the G-10 currencies, falling 0.3% versus the greenback after Bank of Japan Governor Ueda told reporters the price target is not already in sight, reversing hawkish comments from one of his co-workers just the day before as the BOJ confirms it has no idea what it will do next. His comment tempered speculation the bank’s first rate hike since 2007 could come as early as March.

In rates, treasuries rose while European government bonds pared an earlier decline as US equity futures fall. US 10-year yields drop 4bps to 4.22% while European bonds recovered despite euro-area inflation slowing less than expected in February.

In commodities, oil was on track for a modest weekly gain as market gauges continued to show signs of strength, with OPEC+ set to decide early this month whether to extend supply cuts into the next quarter. WTI rose 1.1% to trade near $79.10. Spot gold rose 0.5%.

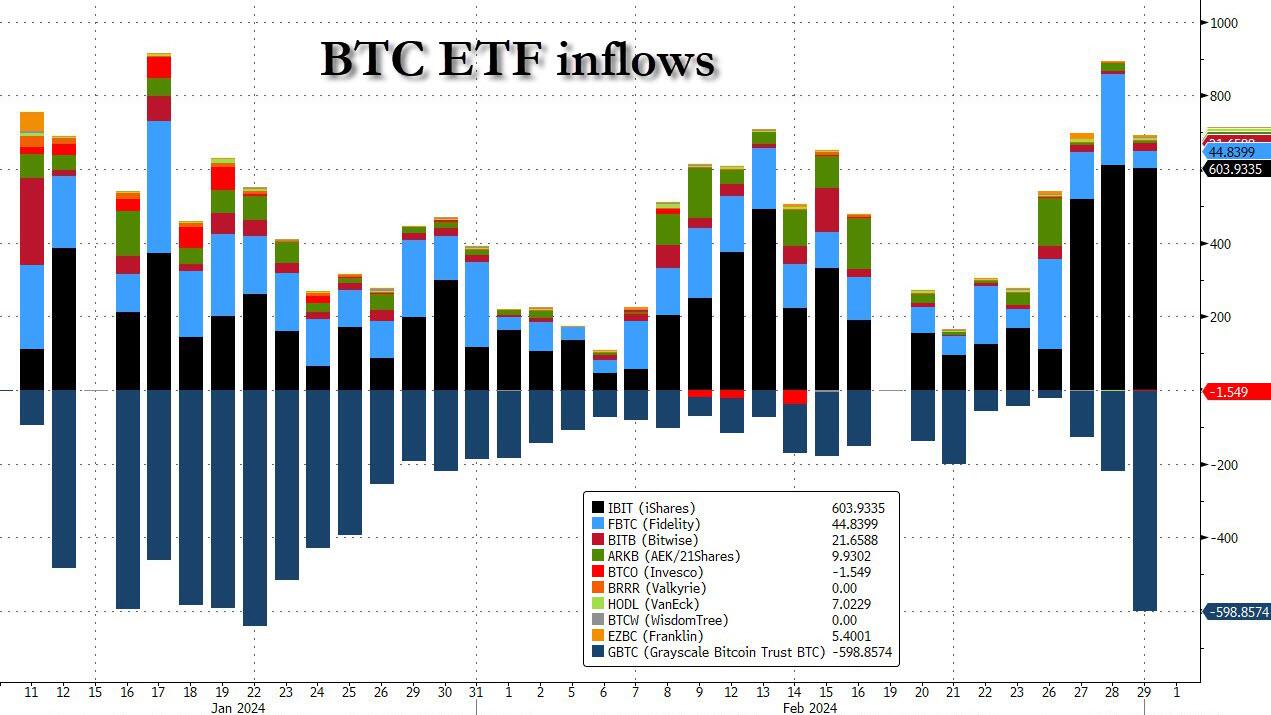

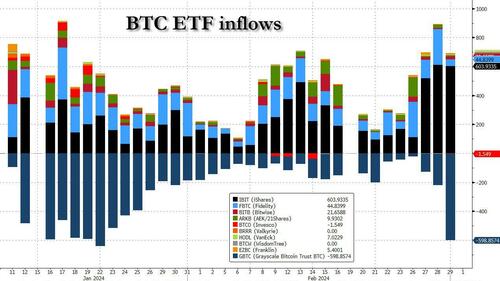

Bitcoin gained for a seventh day, trading above $62,000 as demand from exchange-traded funds continues. BlackRock Inc.’s iShares Bitcoin Trust netted a $604 million inflow on Thursday following a record $612 million on Wednesday.

Today’s US economic data calendar includes February final S&P manufacturing PMI (9:45am), January construction spending, February final University of Michigan sentiment, February ISM manufacturing (10am) and February Kansas City Fed services activity (11am). Fed speakers scheduled include Barkin (8:30am), Goolsbee (10am, 4pm), Waller, Logan (10:15am), Bostic (12:15pm), Daly (1:30pm) and Kugler (3:20pm).

Market Snapshot

- S&P 500 futures up 0.1% to 5,109.25

- STOXX Europe 600 up 0.5% to 496.98

- MXAP up 0.5% to 173.76

- MXAPJ up 0.3% to 526.58

- Nikkei up 1.9% to 39,910.82

- Topix up 1.3% to 2,709.42

- Hang Seng Index up 0.5% to 16,589.44

- Shanghai Composite up 0.4% to 3,027.02

- Sensex up 1.7% to 73,768.05

- Australia S&P/ASX 200 up 0.6% to 7,745.61

- Kospi down 0.4% to 2,642.36

- German 10Y yield little changed at 2.45%

- Euro little changed at $1.0812

- Brent Futures up 0.9% to $82.63/bbl

- Gold spot up 0.0% to $2,045.04

- US Dollar Index little changed at 104.14

Top Overnight News

- Stocks advanced Friday after a reassuring reading on US inflation calmed traders’ worst fears on the outlook for interest rates and spurred fresh record highs on Wall Street.

- Pacific Investment Management Co. is warning that US fiscal profligacy threatens to drag the Treasury market back to 1980s, a time when bond vigilantes demanded far higher compensation to own longer-dated bonds.

- Federal Reserve Bank of New York President John Williams said he doesn’t see a need for officials to tighten policy further and reiterated that he expects the central bank to cut rates later this year.

- Swiss National Bank President Thomas Jordan will step down in September after more than a decade on the job, according to a statement on Friday.

- Returns on carry trades using the world’s biggest currencies. This often profitable but potentially risky strategy involves borrowing the lowest-yielding currencies in the Group-of-10 economies and using the funds to bet on the highest-yielding ones.

- Bank of Japan Governor Kazuo Ueda is keeping his options open for the timing of a widely expected interest rate hike, a position that may fuel further market volatility as investors and economists speculate over a March or April move

Earnings

- Dell Technologies Inc (DELL) – Q4 2023 (USD): Adj. EPS 2.20 (exp. 1.73), Revenue 22.32bln (exp. 22.16bln). Shares +22.4% in pre-market trade.

- Saint Gobain (SGO FP) – FY23 (EUR): Recurring 6.39bln (prev. 6.48bln Y/Y), EBITDA 7bln (exp. 6.9bln, prev. 7.12bln Y/Y), Revenue 47.9bln (exp. 47.8bln, prev. 51.2bln Y/Y). Expects to complete previously announced 5yr 2bln buyback in 2024. Guides initial FY24 Op. margin “double digit”. Shares -4.2% in European trade

- Daimler Truck (DTG GY) – Q4 (EUR): Adj. EBIT 1.56bln (exp. 1.36bln), Revenue 15bln (exp. 14.85bln). Raises dividend to 1.9/shr (prev 1.30/shr). Guides initial FY24 Revenue 55-75bln. (Newswires) Shares +12.8% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with positive bias amid tailwinds from the US following an absence of any hawkish surprises in the PCE data, while participants also reflected on the latest Chinese PMI figures. ASX 200 printed fresh record highs and entered bull market territory after gaining over 20% from its 2022 low. Nikkei 225 extended on its best levels and advanced closer to the 40,000 level amid a weaker currency and after BoJ Governor Ueda said Japan’s economy is not yet in a situation where sustained achievement of 2% inflation can be foreseen, which is in contrast with the prior day’s hawkish rhetoric from board member Takata. Hang Seng and Shanghai Comp. lagged behind their regional peers although the Hong Kong benchmark clawed back initial losses with the help of tech strength, while the mainland was indecisive after the PBoC drained liquidity and as participants digested Chinese PMI data which was mostly encouraging although Official Manufacturing PMI remained in contraction territory for the 5th consecutive month.

Top Asian News

- China’s Commerce Ministry said China’s trade faces a complex, severe, and uncertain external environment, while it will help companies explore the market and expand imports to ensure domestic demand, according to Reuters.

- BoJ Governor Ueda said inflation is easing at a quick pace and wage negotiations will offer a tailwind, while he added that Japan’s economy will continue a gradual recovery and the economy is not yet in a situation where sustained achievement of 2% inflation can be foreseen. Ueda also commented that in judging whether a sustained achievement of the 2% inflation target can be foreseen, this year’s annual wage negotiation outcome is key.

- RBNZ Governor Orr said the economy is evolving as anticipated and inflation expectations have declined, while inflation is still too high but is declining and policy needs to stay restrictive for some time. Orr also said he expects to begin normalising policy next year and economic growth to begin picking up this year.

- RBNZ Deputy Governor Hawkesby said restrictive policy is needed to ensure inflation expectations anchor at 2% and policy is going to stay restrictive for some time yet, while they don’t have a lot of room to manoeuvre when it comes to future inflation shocks. Hawkesby said they are on the right path with inflation and have to hold their course, as well as noted they are not in a mindset to cut rates now and will be cutting sometime down the track.

- Fitch cuts China new home sales forecast, sees wider effects from a slower recovery. Cuts forecast for the Chinese hosing market to a 5-10% decline in 2024 new home sales

European bourses, Stoxx600 (+0.1%) began the session firmly in the green, though did succumb to some early morning pressure ahead of EZ inflation. Thereafter, European equities took another leg lower, with sentiment subdued following the hotter-than-expected print. However, the move came alongside marked uptick in EGBs, with the move seen across assets and has a risk-feel to it; though, it does appear to have been driven by the ‘relief’ in EGBs post-HICP which while hotter-than-expected continues the cooling narrative. European sectors hold a positive tilt; Autos is firmer, being propped up by post-earning gains in Daimler Truck (+12.8%). Energy has been lifted by recent strength in the crude complex; BP (+1.2%)/Shell (+1%). To the downside, Saint-Gobain weighs on Construction & Materials, after poor results. US Equity Futures (ES -0.2%, NQ -0.2%, RTY -0.4%) are entirely in the red. The RTY underperforms, largely hampered by regional banking fears after NYCB (-24% pre-market) announced it had identified weaknesses in internal controls.

Top European news

- Portuguese Finance Minister Medina called for the ECB to start lowering borrowing costs and warned that maintaining them at their current level is a “high risk”, while he noted various European countries are experiencing a strong slowdown with some already in stagnation and recession, according to Bloomberg.

- SNB Chairman Thomas Jordan to step down at end of September 2024.

- UK Chancellor Hunt has ruled out stamp duty cuts in the March budget, according to i news; due to a belief this would fuel inflation

FX

- Contained trade for the DXY and within a 104.04-21 range, respecting yesterday’s 103.65-104.20 parameters. Upcoming data/speaker slate could provide impetus and bring the weekly high of 104.24 into view.

- EUR/USD is ultimately around flat after the hotter-than-expected inflation metrics but respecting yesterday’s 1.0795-1.0856 range. Interim resistance provided by the 100DMA at 1.0824.

- JPY is the underperformer across the majors following dovishly-perceived comments from Ueda. USD/JPY is up to 150.68 at best with all eyes on the YTD peak at 150.88.

- Antipodeans are marginally firmer vs. the USD in uneventful trade with AUD continuing to pivot around the 0.65 mark after making a base for the week yesterday at 0.6486. NZD/USD unable to crack 0.61 after printing a YTD trough yesterday at 0.6077.

- PBoC set USD/CNY mid-point at 7.1059 vs exp. 7.2011 (prev. 7.1036).

Fixed Income

- USTs began the session with a bearish bias, attempting to pare back some of the PCE-induced gains. However, after the EZ CPI (which sparked a fleeting hawkish reaction), the bond complex caught a bid, taking treasuries to fresh session highs; currently around 6 ticks firmer with the curve steeper into US ISM & Fed speak.

- Bunds also began the session on a softer footing. Following the hotter-than-expected CPI there was a fleeting downward move to a test of 132.00 however this was shortlived with Bunds now bouncing and briefly surpassing the 132.54 overnight high. Perhaps driven by the view that while HICP was hotter than expected, it is still cooling overall and does not change the pre-existing narrative of a June move.

- Gilt price action is in-fitting with EGBs, and unreactive to its own PMI (the HCOB commentary brought attention to ongoing inflationary pressures); Gilts following suit, briefly moved into the green as EGBs bounced but have settled near unchanged.

Commodities

- Crude is firmer after a relatively contained start to the session. The complex caught a bid in the European morning, just after the release of EZ Manufacturing PMIs which were revised up but remain bleak overall; Brent holds just shy of USD 83/bbl.

- XAU is firmer, continuing to build on the prior day’s PCE-induced gains. Has climbed above USD 2050/oz, but with still some way to go thereafter before the USD 2078/oz YTD peak.

- Base metals in the red, hit by PMIs remaining in contraction (despite upward revisions) and soft Chinese performance given the region’s Manufacturing number printed below 50.0 for the fifth consecutive month. Initial USD upside is also a hindrance, though this narrative has diminished somewhat.

Geopolitics: Middle East

- Israeli PM Netanyahu said Israel won’t fold to the delusional demand of Hamas but will provide freedom of worship to Muslims during the month of Ramadan while maintaining security at the same time, according to Al Jazeera.

- French President Macron said the situation in Gaza is terrible and a ceasefire must be implemented immediately to allow humanitarian aid to be distributed, while France’s Foreign Ministry said the shooting by Israeli soldiers against civilians trying to access food is unjustifiable and they are waiting for all light to be shed on the shooting. The ministry also said it is Israel’s responsibility to comply with the rules of international law and protect the distribution of humanitarian aid to civilian populations.

- UN Secretary-General Guterres said the killing of over 100 humanitarian aid seekers in Gaza would require an effective independent investigation.

- US military said it conducted strikes against six anti-ship cruise missiles and an aerial drone that posed a threat to ships in the Red Sea, according to Reuters.

Geopolitics: Other

- US Defense Secretary Austin told the House Armed Services Committee that the Russian leadership “won’t stop there” if Ukraine is defeated and that Russia and NATO could come into conflict if Ukraine falls, according to TASS.

- Japan’s government will freeze the assets of 12 individuals and 8 organisations due to their involvement in the Ukraine conflict.

US event calendar

- 09:45: Feb. S&P Global US Manufacturing PM, est. 51.5, prior 51.5

- 10:00: Jan. Construction Spending MoM, est. 0.2%, prior 0.9%

- 10:00: Feb. ISM Manufacturing, est. 49.5, prior 49.1

- Feb. ISM New Orders, prior 52.5

- Feb. ISM Employment, prior 47.1

- Feb. ISM Prices Paid, est. 53.2, prior 52.9

- 10:00: Feb. U. of Mich. Sentiment, est. 79.6, prior 79.6

- Feb. U. of Mich. 1 Yr Inflation, est. 3.0%, prior 3.0%

- Feb. U. of Mich. 5-10 Yr Inflation, est. 2.9%, prior 2.9%

- Feb. U. of Mich. Current Conditions, prior 81.5

- Feb. U. of Mich. Expectations, prior 78.4

- 11:00: Feb. Kansas City Fed Services Activ, prior -2

DB’s Jim Reid concludes the overnight wrap

You’re not going to believe it but its March already! Since it’s the start of the month, we’ll shortly be releasing our monthly performance review, covering how different assets fared in February. In terms of the headlines, the Magnificent 7 posted its strongest performance in 9 months, which powered global equities up to all-time highs. But even as growth data remained resilient, fresh upside inflation surprises led to notable losses for bonds, and 2yr Treasury yields saw their biggest increase in 7 months since June as investors kept pushing out the timing of future rate cuts. See the full report in your inboxes shortly.

When it came to the last 24 hours, markets got a boost on a relief that the US PCE inflation report was in line with expectations, after the latest European inflation numbers fell back earlier in the day. That helped sovereign bonds rally on both sides of the Atlantic, while the S&P 500 (+0.52%) advanced to a new all-time high. The moves also leave the S&P just about on course to post another weekly advance (+0.15% so far this week). If it does hold on to this weekly gain, it would mark 16 out of 18 positive weeks for the first time since 1971, so it’s hovering around some big milestones. So no pressure today for the market!

With positive month-end sentiment dominating the end of yesterday’s session, it was not only the S&P 500 eking out yet another all-time high, but there was also a new record high for the NASDAQ (+0.90%), which moved above its previous peak from November 2021. Consistent with the narrative of the year so far, the Magnificent 7 outperformed (+1.22%), with Amazon (+2.08%) and Nvidia (+1.87%) leading the way. The equity picture had been more subdued in Europe, where the STOXX 600 ended the day unchanged, although the German DAX (+0.44%) continued to outperform yesterday. Indeed, yesterday’s advance was the 7th consecutive gain for the DAX, taking the index up to a fresh all-time high.

Looking at the main trigger of the optimism, the PCE inflation report showed headline PCE running at a monthly +0.3% as expected, which took the year-on-year measure down to 2.4%, and its lowest since February 2021. Core PCE was running above that, at a 12-month high of +0.42%, but markets weren’t too alarmed as it was in line with the +0.4% expected by the consensus. Nevertheless, the report added to signs that inflation was still lingering above target, and some of the 6-month measures (which had previously pointed to inflation being back at target) were no longer looking as favourable. For instance, core PCE had been running at +1.9% on a 6m annualised basis, but after this January report, it was up to +2.5% again. Likewise, headline PCE rose from +2.1% to +2.5% on a 6m basis. Interestingly outside the pandemic period, and the month after 9/11, the monthly core print of 0.42% was the highest since the early 1990s. However there were some odd potential one-offs in the report such as a surge in portfolio management charges. So for now the market is relaxed but inflation is proving a little sticky as we start the year. Perhaps the sanguine response is based on the fact that pretty much nobody now expects a March cut and a lot of water can flow under the bridge before June when the market expects the first one. So plenty of time to change mind on things or the data to change.

Over in the Euro Area, rates initially saw a modest sell off amid country-level flash CPI prints for February. But in the end these came largely in line with expectations, with a pattern of slowing, but still above target, inflation. German inflation was down to +2.7% on the EU-harmonised measure, whilst in France it was down to +3.1%, its lowest since September 2021. Both of these were in line with consensus, while Spain’s print was a touch above (+2.9% vs +2.8% exp.). This morning we’ll get the Euro Area-wide release, which will set the stage for the ECB’s next meeting on Thursday. With the available country prints, our economists see a marginal upside risk to the consensus expectations of +2.5% headline and +2.9% core inflation.

Against this backdrop, sovereign bonds posted a moderate rally yesterday, clawing back some of their losses over February as a whole. In the US, 10yr Treasuries yields fell -1.5bps to 4.25%, while 2yr yields retreated by -1.8bps. This was a decent turnaround, having been up by 5-6bps shortly before the US data. And over in Europe, yields on 10yr bunds (-4.8bps), OATs (-4.2bps) and BTPs (-4.1bps) all fell back by a larger amount.

Both 2yr and 10yr Treasuries had traded flat on the day around the US equity close, but saw a slight rally late on after New York Community Bancorp said it had identified “material weaknesses” in risk controls. NYCB also announced a $2.4bn goodwill impairment and replaced its CEO. Shares of the troubled regional bank fell more than 20% in extended trading, having already declined by 54% over the past month. So one to keep an eye on today.

Asian equity markets are higher this morning with the Nikkei (+1.82%) leading gains, hitting a fresh all-time high after a two-day losing streak while the Hang Seng (+0.75%), the CSI (+0.33%) and the Shanghai Composite (+0.10%) are also moving higher. South Korea is closed for a holiday. S&P 500 (+0.15%) and NASDAQ 100 (+0.21%) futures are edging higher.

Early morning data showed that China’s o fficial manufacturing PMI contracted for the fifth straight month in February but was broadly inline at 49.1 (v/s 49.0 expected) versus the 49.2 seen in January. Meanwhile, the official non-manufacturing PMI grew more than expected to 51.4 in February after a 50.7 reading in January. This saw China’s composite PMI remain steady at 50.9 in February. Elsewhere, Japan ’s labour market remained tight as the jobless rate dropped to 2.4% in January, the lowest level since early 2020 as against December’s revised level of 2.5%.

The Japanese yen (-0.27%) weakened to 150.38 after the BoJ Governor Kazuo Ueda stated that he is still not confident the nation can sustainably attain the central bank’s 2% inflation target while stressing the need to see the outcome of wage negotiations currently taking place, for confirmation of a positive wage-inflation cycle. He seems to be wanting to temper speculation that the BoJ could move as early as this month giving the BoJ some optionality. It is still likely that happens before the end of April though.

Back to yesterday, and on the inflation side, one ongoing theme is that short-term US inflation expectations have continued to move higher in recent days. In particular, the US 2yr breakeven was up +1.5bps yesterday to 2.79%, the highest since last March, and the 2yr zero-coupon inflation swap (+1.1bps) reached its highest since October at 2.445%. This comes as the recent uptick in oil prices continues to filter through to the real economy, with US gasoline prices up to a 3-month high of $3.319 per gallon on Wednesday.

Looking at yesterday’s other data, UK mortgage approvals rose to 55.2k in January (vs. 52.0k expected), which is their highest level since October 2022. Otherwise in the US, the weekly initial jobless claims rose to 215k over the week ending February 24 (vs. 210k expected), ending a run of 3 consecutive weekly declines. In the meantime, continuing claims were up to 1.905m in the week ending February 17 (vs. 1.875m expected), their highest level since November.

To the day ahead now, and data releases include the global manufacturing PMIs for February, along with the ISM manufacturing reading from the US. Over in the Euro Area, we’ll get the flash CPI inflation release for February, as well as the unemployment rate for January. Otherwise, central bank speakers include the Fed’s Barkin, Waller, Logan, Bostic, Daly and Kugler, the ECB’s Holzmann, and BoE chief economist Pill.