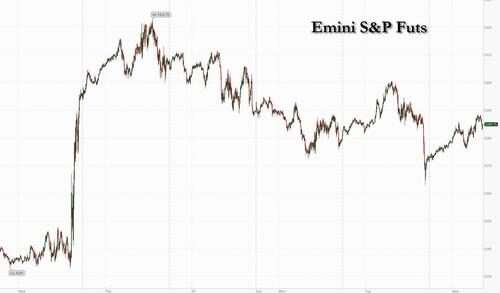

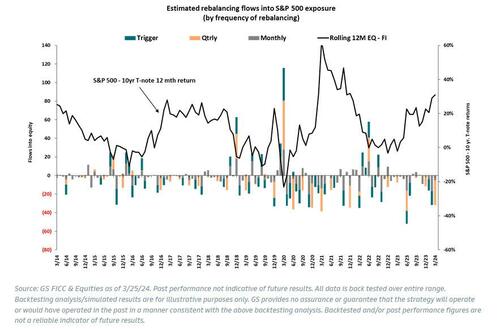

US equity futures rebounded from yesterday’s 3:30pm pension-selling inspired airpocket, and are higher along with European markets, even as Goldman anticipates continued month-end turbulence due to a sizable $32 billion in quarter-end selling, the largest since June 2023 (more details here for premium subs). As of 8:10am ET, S&P 500 futures rose 0.4% while Nasdaq 100 contracts add 0.5%, while European stocks were little changed near Tuesday’s record closing high. As JPM notes, the S&P is on a 3-day losing streak which appears to be mostly month-end/quarter-end related given the trading patterns. SPX -0.73% over those three days.Bond yields are up 1bps across the curve, but USD is flat while the yen bounced from a 34-year low on speculation that Japanese officials may be preparing to intervene to support the currency; commodities are for sale across all 3 complexes with the notable exceptions gold and natgas. Keep an eye on oil prices which could push past near-term expectations as Russia looks to cut production. The major macro events are Waller’s speech (6pm ET) and the 7Y bond auction; yesterday’s 5Y was digested well

In premarket trading, all Mag7 names are higher as are Semis and Large-cap Healthcare. Merck shares jumped 4.8% after Winrevair, a treatment for pulmonary arterial hypertension, which is a rare and dangerous form of high blood pressure, won approval from the US Food and Drug Administration. Merck also rose after its Winrevair drug won US approval. Shares in Trump Media & Technology were set to extend gains following its debut as a public company. Here are the other notable premarket movers:

- Forge Global (FRGE US) shares fall 12% after the private securities marketplace operator reported total revenue for the fourth quarter that missed the average analyst estimate.

- GameStop (GME US) shares slide 19% after reporting adjusted earnings per share and net sales for the fourth quarter that missed the average analyst estimates. The stock had gained about 18% in the two trading sessions before the earnings report.

- NCino (NCNO US) shares are up 14% after the cloud banking software company gave a forecast for adjusted earnings that was stronger than expected. Analysts were positive about the company’s results and outlook.

- Nuvation Bio (NUVB US) shares jump 13% after the biotechnology company was upgraded to buy from hold at Jefferies after the acquisition of AnHeart Therapeutics.

- One Group Hospitality (STKS US) shares are up 12% after the company said late Tuesday that it’s buying Safflower Holdings, the owner of Benihana, in a deal valued at $365m.

- Robinhood (HOOD US) shares rise 7.1%. The company, best known for offering commission-free trading, said it is rolling out a credit card to US consumers as pushes beyond trading.

- Trump Media (DJT US) shares jump 14%, putting its stock on track to extend gains after rallying 16% in its first trading day as a public company.

- Western Digital (WDC US) shares tick 1.5% higher as the computer hardware and storage company is started with an outperform rating and $80 price target at Evercore ISI, which sees strong potential.

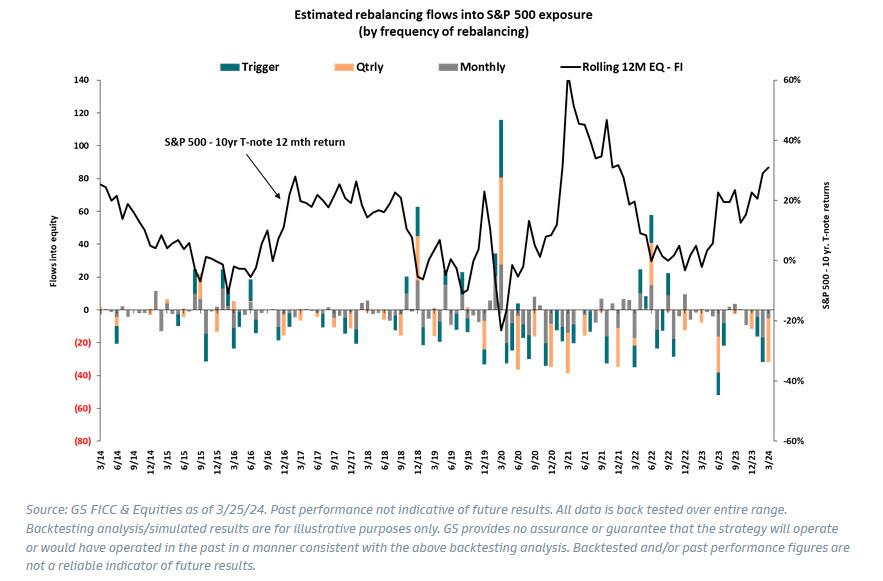

As we first reported last night, with stocks set to cap another strong quarter, pension funds are likely to sell an estimated $32 billion in equities to rebalance their positions, according to Goldman.

While projections on pension flows vary widely on Wall Street, it could heap extra pressure on markets when trading volumes are thin around Easter. After the S&P 500 soared about 26% since late October, traders have flagged concern that positioning is stretched and stocks are more vulnerable to short-term profit taking.

Officials from Japan’s Ministry of Finance, the Bank of Japan and Financial Services Agency met to discuss markets in their first three-way meeting since late May. After the talks, Japan’s top currency official Masato Kanda pledged to take appropriate action against excessive swings, saying he sees speculative moves behind the yen’s plunge. The yen strengthened 0.3%.

“The BOJ’s finger will be on the trigger for FX intervention,” said David Forrester, Singapore-based senior FX strategist at Credit Agricole.

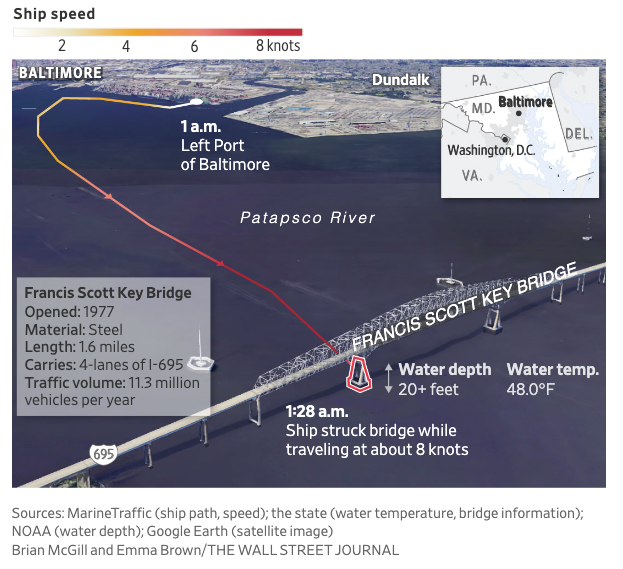

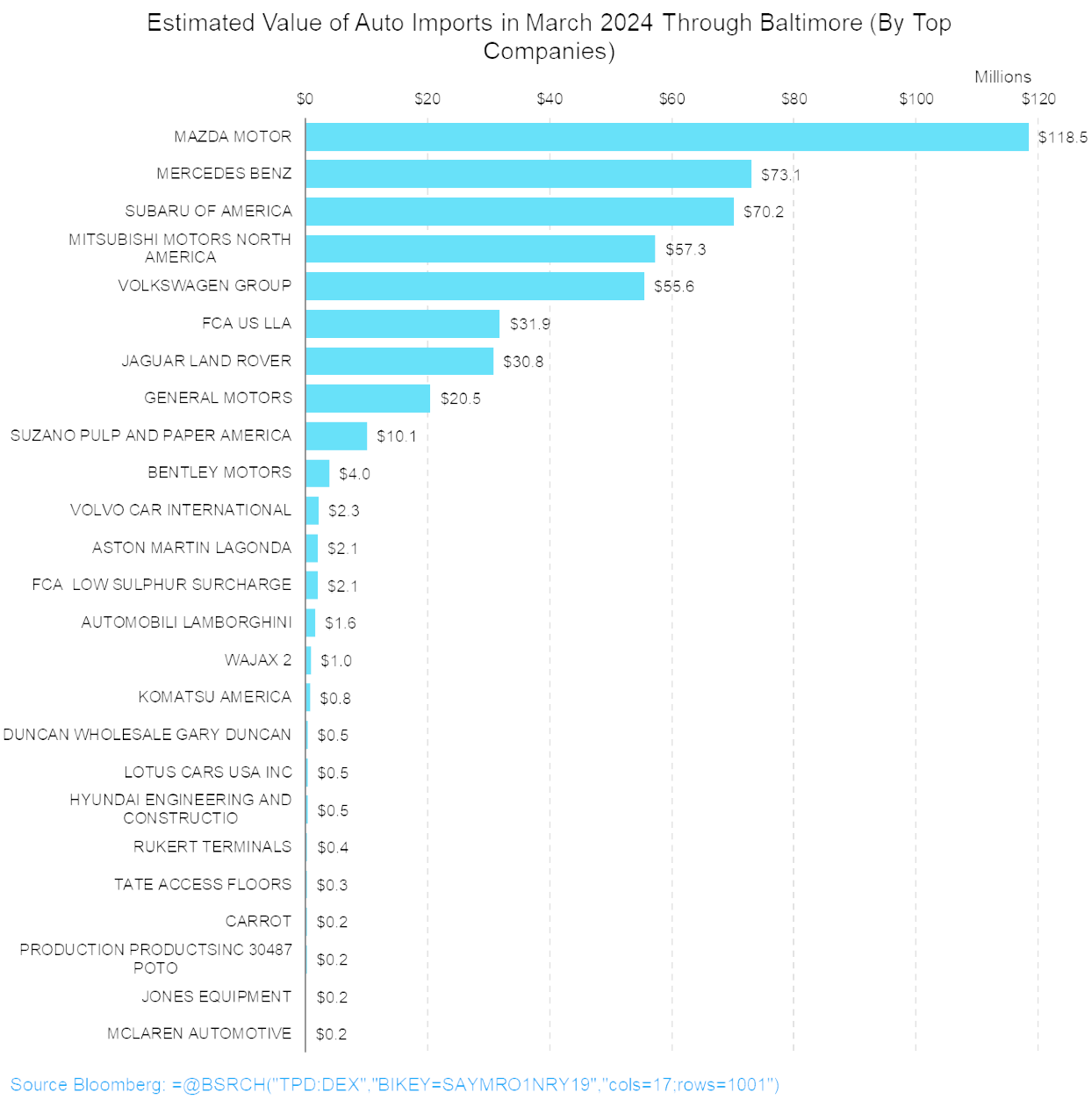

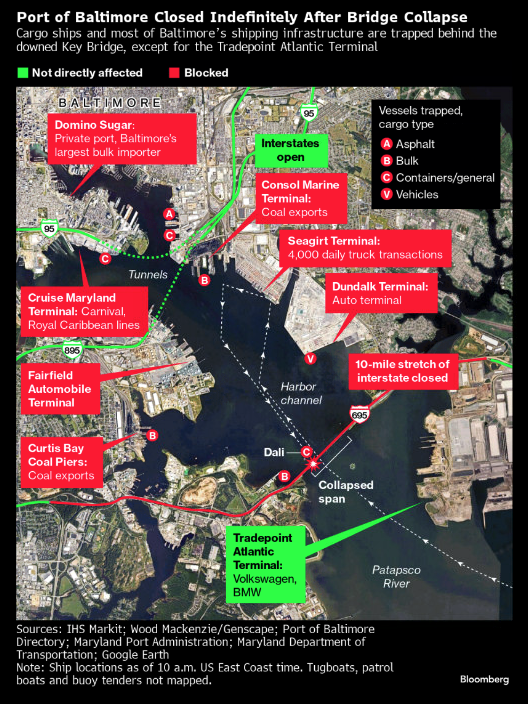

Elsewhere, Chinese President Xi Jinping met with a group of American business executives in Beijing as China seeks to restore confidence in the economy and keep relations with the US on a stable footing. Meanwhile, as much as 2.5 million tons of coal and hundreds of car shipments are threatened with disruption after the sudden collapse of the Baltimore Bridge clogged the supply chains around the port.

Stocks have had a strong start to the year, with major benchmarks scaling record levels. The S&P 500 is set for its fifth month of straight gains, while Japan’s Nikkei 225 Index of shares closed within a whisker of its all-time high. Still, moves this week have been muted ahead of Friday’s release of the Federal Reserve’s preferred inflation gauge.

“I’m still rather positive on equity markets, as long as nothing changes in the broader picture, one can just go with the flow,” Francois Rimeu, a strategist at La Francaise Asset Management in Paris, said. He sees a possibility the rally can broaden toward other parts of the market, such as European or mid-cap shares, given “extreme” valuation gaps among technology and US stocks.

European stocks were little changed near Tuesday’s record closing high. Retail shares are the best performers as clothing retailer Hennes & Mauritz jumped as much as 14% after its profit beat estimates thanks to cost cuts, while payments firm Adyen NV got a boost from a broker upgrade. Euro-area data showed an improvement in economic confidence, supporting expectations that the region can soon move beyond its recent weakness.

Earlier in the session, Asian stocks traded mixed after the subdued handover from Wall St heading into quarter-end and Easter. ASX 200 was underpinned by strength in the top-weighted financials and consumer-related sectors, while data also provided a tailwind after an improved leading index and softer-than-expected monthly CPI. Nikkei 225 outperformed as the yen fell to a 33-year low amid dovish-leaning BoJ comments. Hang Seng and Shanghai Comp. declined amid a slew of earnings and weakness in tech with Alibaba pressured after it withdrew its Cainiao IPO application, while the mainland failed to benefit from the PBoC’s firm liquidity operation and improved Industrial Profits.

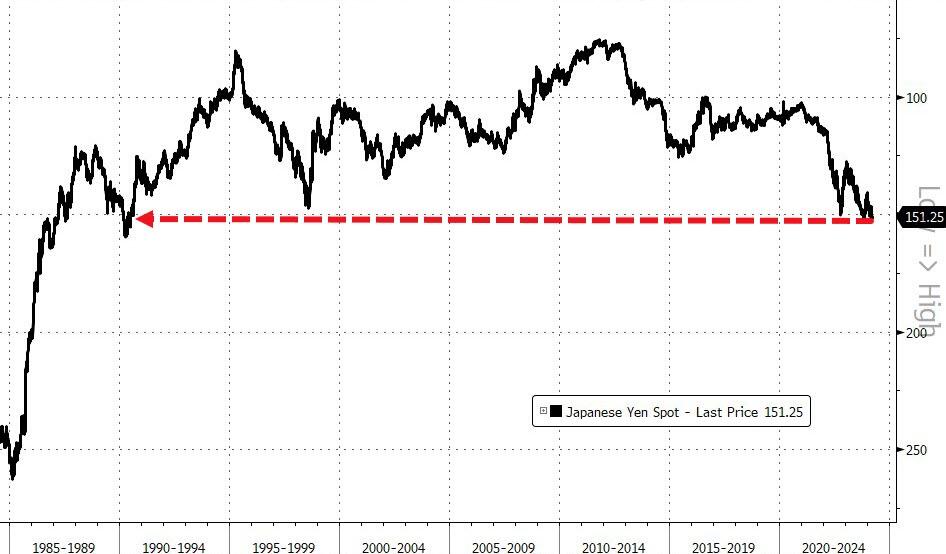

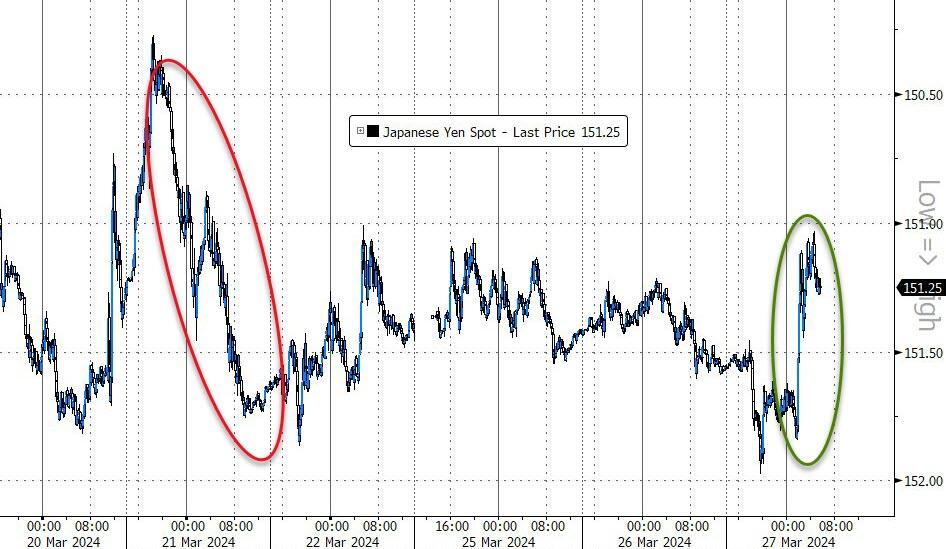

In FX, the yen rebounded after slumping to the weakest level in about 34 years, while the krona fell against the euro after the Riksbank opened the door to a rate cut as soon as May. The USDJPY fell 0.3% to ~151.10 after hitting its highest since 1990 earlier on Wednesday after Japan’s top currency official pledged to take appropriate action against excessive moves in the foreign-exchange market as the MOF stepped closer to intervention with its strongest warning yet as the yen slid to the weakest level in about 34 years against the dollar.

- USD/JPY rose as much as 0.3% to 151.97, the highest level in about 34 years, then fell 0.3% back to 151.15 as the BOJ stepped closer to potential currency intervention

- EUR/SEK rose 0.3% to 11.5111 before paring the advance to trade 0.1% higher at 11.4809, while USD/SEK steadied at 10.5964; The Riksbank signaled a potential pivot to policy easing within the next quarter

In rates, treasuries were little changed after trading in a narrow range through Asia session and European morning, leaving yields within 1bp of Tuesday’s closing levels. Treasury 10-year yields around 4.235%, slightly cheaper on the day with bunds and gilts outperforming in the sector by 3bp and 1bp; curve spreads also within 1bp of Tuesday’s close. Core European rates outperform as bunds rise after Spanish harmonized and core inflation rose less than expected in March. German 10-year yields fall 2bps to 2.33%. With no data scheduled, US session focal points are 7-year note auction and comments from Fed’s Waller after the close. The week’s auction cycle concludes with $43b 7-year note sale at 1pm New York time; Tuesday’s 5-year note stopped through by 1bp.

In commodities, oil prices pared a decline, with WTI falling as much as 1% before rebounding to trade near $81.2. Spot gold rises 0.6%.

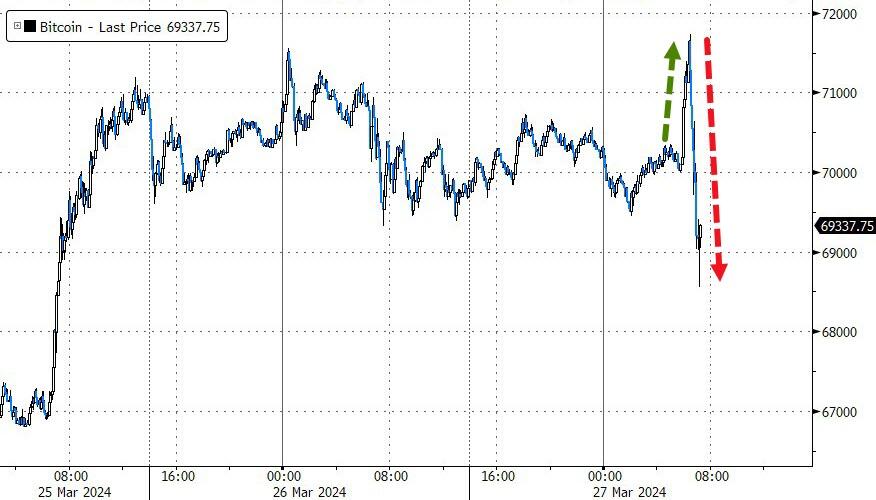

In crypto, Bitcoin has been relatively contained and holds around the $70k mark, with Ethereum also holding at key levels around $3.6k.

Looking at today’s calendar, the US economic data slate is empty for the session; Fed members scheduled to speak include Waller at 6pm.

Market Snapshot

- S&P 500 futures up 0.3% to 5,281.75

- STOXX Europe 600 little changed at 511.13

- MXAP little changed at 176.77

- MXAPJ down 0.4% to 534.12

- Nikkei up 0.9% to 40,762.73

- Topix up 0.7% to 2,799.28

- Hang Seng Index down 1.4% to 16,392.84

- Shanghai Composite down 1.3% to 2,993.14

- Sensex up 0.9% to 73,101.01

- Australia S&P/ASX 200 up 0.5% to 7,819.61

- Kospi little changed at 2,755.11

- German 10Y yield little changed at 2.34%

- Euro little changed at $1.0826

- Brent Futures down 0.8% to $85.58/bbl

- Gold spot up 0.0% to $2,179.23

- US Dollar Index little changed at 104.39

Top Overnight News

- The decadeslong push by American companies into China is stalling. American firms in China are being squeezed by escalating geopolitical tensions, tit-for-tat measures on trade and exports, and China’s drive for self-sufficiency. Meanwhile, the Chinese market is becoming less attractive. The country’s economic growth fell to its slowest rate in decades last year; consumers there are spending less, especially on foreign brands; and its once-unstoppable export machine is faltering. WSJ

- China’s President Xi Jinping met US chief executives including Chubb’s Evan Greenberg and Qualcomm’s Cristiano Amon on Wednesday as American business leaders sought to mend ties frayed by geopolitical and trade tensions between the world’s two largest economies. FT

- China’s industrial profits jumped at the start of this year, with foreign-owned and private groups reporting the largest increases. Industrial profits rose by 10.2% year on year for January-February, data from the National Bureau of Statistics showed on Wednesday. Profits at foreign-owned business surged 31.2% and climbed 12.7% at private companies. State-owned enterprises saw profits edge up just 0.5%. FT

- The yen pared gains as Japan’s top currency official said the government can’t tolerate speculative moves in the FX market and is prepared to use any option to restore calm, in line with earlier comments from the finance minister. Masato Kanda spoke after a joint meeting of the MOF, BOJ and FSA. Earlier, the yen had slid to its lowest against the dollar since 1990. BBG

- The BOE is probing how badly funding for UK businesses would be hit by the reversal of a long-running private equity boom, officials said, as they escalated warnings about leverage, transparency and valuations in private markets. FT

- Asset managers kept unwinding bullish Treasury futures bets ahead of the Fed’s recent meeting, a defensive move that sent net long positions for “real money” investors such as pension funds and insurance companies to an eight-month low. The move also signaled some may have been paring back on basis trades. BBG

- The Baltimore bridge collapse may cause months of disruptions, block the export of as much as 2.5 million tons of coal, and speed up a shift of cargo to the West Coast. Search operations were halted as six people are presumed dead. BBG

- The artificial-intelligence boom is sending Silicon Valley’s talent wars to new extremes. Tech companies are serving up million-dollar-a-year compensation packages, accelerated stock-vesting schedules and offers to poach entire engineering teams to draw people with expertise and experience in the kind of generative AI that is powering ChatGPT and other humanlike bots. They are competing against each other and against startups vying to be the next big thing to unseat the giants. WSJ

- UBS and Apollo reached a deal for the carve-out of Credit Suisse’s securitized products business after renegotiating key parts of the accord. Apollo will purchase $8 billion in senior secured financing facilities. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed after the subdued handover from Wall St heading into quarter-end and Easter. ASX 200 was underpinned by strength in the top-weighted financials and consumer-related sectors, while data also provided a tailwind after an improved leading index and softer-than-expected monthly CPI. Nikkei 225 outperformed as the yen fell to a 33-year low amid dovish-leaning BoJ comments. Hang Seng and Shanghai Comp. declined amid a slew of earnings and weakness in tech with Alibaba pressured after it withdrew its Cainiao IPO application, while the mainland failed to benefit from the PBoC’s firm liquidity operation and improved Industrial Profits.

Top Asian News

- PBoC Governor Pan said bilateral currency swaps help enhance financial safety nets and that China is willing to deepen financial cooperation with other countries, according to Reuters.

- USTR office said the US mission to WTO received a consultation request from China regarding parts of the Inflation Reduction Act and the US is reviewing the request, according to Reuters.

- US President Biden’s administration is pursuing TikTok with the FTC investigating the Co. over allegedly faulty privacy and data security practices, according to POLITICO.

- Chinese Foreign Ministry Spokesperson Lin says China has been taking a hard hit as a major trade country; says China has a lot of policy space to shore up the economy; government debt level remains relatively low.

An uninspiring session thus far in Europe, Stoxx600 (+0.1%), bourses within tight ranges and sentiment mixed in relatively light newsflow. European sectors are mixed with little theme or bias; Retail is the clear outperformer after H&M’s (+12%) earnings and Energy lags amid the slide in crude oil prices. US Equity Futures (ES +0.4%, NQ +0.4%, RTY +0.1%) are trading on a firmer footing, attempting to make back the losses seen in the prior session.

Top European news

- Riksbank maintains its Rate at 4.00% as expected; “It is likely that the policy rate can be cut in May or June if inflation prospects remain favourable”.

- ECB’s Kazaks said inflation is slowing and the first rate cut is nearing, while he doesn’t object to the market view of a June rate cut and said they will lower rates cautiously step by step and must see how the economy reacts to policy easing.

- ECB’s Cipollone says uncertainty around inflation is decreasing. Increasingly confident that inflation will converge to 2% by mid-2025. The current economic environment allows for a recovery in real wages in the short term that will not fuel inflation. “The improving inflation outlook, continued strong transmission and further moderation in inflation all create scope for more confidence that we can dial back restriction”. “We are coming closer to the point when we will have the confidence to act”. Says so far from neutral rate that there is room to adjust

- Germany economic institutes expect German GDP to grow 0.1% in 2024 (prev. 1.3% in Autumn forecast). Expects German inflation at 2.3% in 2024 and 1.8% in 2025. Unemployment rate seen at 5.8% in 2024 and 5.5% in 2025.

FX

- USD is steady vs. peers with DXY in a narrow 104.21-42 range. Upside sees the 25th March high at 104.47. Downside sees yesterday’s low at 104.01; all eyes will be on Fed’s Waller at 22:00 GMT / 18:00 ET.

- EUR is flat with a lack of fresh catalysts. Currently trading in close proximity to 200 and 50DMAs at 1.0836 and 1.0838 respectively.

- JPY is now firmer vs. the USD after USD/JPY printed a fresh 33yr high overnight. JPY gained strength after news that Japan’s BoJ, MoF and FSA to hold a meeting, though subsequent comments from Japan’s Top Diplomacy Kanda echoed recent jawboning. These remarks failed to spark any real move in USD/JPY, which remains at troughs around 151.10.

- AUD hampered by softer yuan, iron ore prices and inflation data overnight. AUD/USD has been as low as 0.6512 but holding above last week’s trough at 0.6503.

- SEK is a touch softer vs. the EUR but stopping just shy of the 11.50 mark. Riksbank expectedly left rates unchanged and guidance is pointing towards a H1 cut.

- PBoC set USD/CNY mid-point at 7.0946 vs exp. 7.2250 (prev. 7.0943).

Fixed Income

- USTs are slightly softer and holds around the 110-19 mark; direction today will be guided by Fed’s Waller (Hawk), who in his February remarks foreshadowed the general tone of Powell’s speeches thereafter.

- Bund price action has been relatively contained; Spanish Flash CPI showed the core continuing to moderate, resulting in a slight move higher from 133.02 to a peak of 133.11. This move quickly faded and Bunds now reside just above 132.90 into supply.

- Gilts are unchanged with fresh catalysts sparse so far and price action generally dictated by EGBs; currently around 99.50.

- Italy sells EUR 8.25bln vs exp. EUR 7-8.25bln 3.35% 2029, 3.85% 2029, 3.85% 2034 and EUR 1.5bln vs exp. EUR 1-1.5bln 2031 CCTeu; no move in BTPs.

Commodities

- Downbeat trade across the crude complex following the large surprise build in Private Inventories; Brent May fluctuates around USD 85.50/bbl in a USD 85.28-85.87/bbl parameter.

- Uneventful trade across precious metals following Tuesday’s volatility which saw spot gold briefly test USD 2,200/oz to the upside.

- Base metals are modestly lower across the board in what is seemingly a weakness stemming from the downbeat sentiment seen across Chinese markets overnight.

- JPMorgan says without counter-measures the Russian decision to cut oil production could lift Brent to USD 90/bbl in April, mid-90s in May and near USD 100/bbl by September

Geopolitics: Middle East

- At least seven people were killed in an Israeli strike on southern Lebanon, according to two security sources cited by Reuters.

- “Israel Broadcasting Corporation: Hostage exchange negotiations continue despite Hamas’ ‘negative’ response”

Geopolitics: Other

- China State Council Taiwan Affairs Office spokesperson said some individuals in the US have ulterior motives and are continuously fabricating so-called “timelines” and hyping up the mainland’s “military threat” which is creating an atmosphere of war across the Taiwan Straits, while the spokesperson urged the US to stop fanning the flames and take concrete actions in adhering to the one-China principle, according to Global Times

US Event Calendar

- 07:00: March MBA Mortgage Applications, prior -1.6%

- 10:00: Revisions: Wholesale sales, inventories

Central Bank Speakers

- 18:00: Fed’s Waller Speaks on Economic Outlook

DB’s Jim Reid concludes the overnight wrap

As we continue to draw closer to the Easter holiday, it remained quiet in markets yesterday other than for a sizeable late sell-off in US equities which came a bit out of the blue. Markets have been a bit thin this week so that might have contributed as we await the main event at 12.30pm London time on Friday when I’ll be driving through the French countryside, and you may be having a well-deserved piece of Easter chocolate! That will, of course, be the much anticipated core PCE print.

Perhaps the most exciting thing in the last 24 hours has been the Yen hitting 34-year lows of 151.97 overnight before rallying a touch to 151.75 as I type. The move came on the back of dovish remarks by the BoJ board member Naoki Tamura that the central bank must proceed slowly and steadily towards normalising its ultra-loose policy. However, the prospect of intervention in the currency market has increased after Japanese Finance Minister Shunichi Suzuki commented that the government “will take bold action” to slow the currency’s drop if needed. The Nikkei is +1.44% as I type and bucking the trend in Asia as we’ll see below.

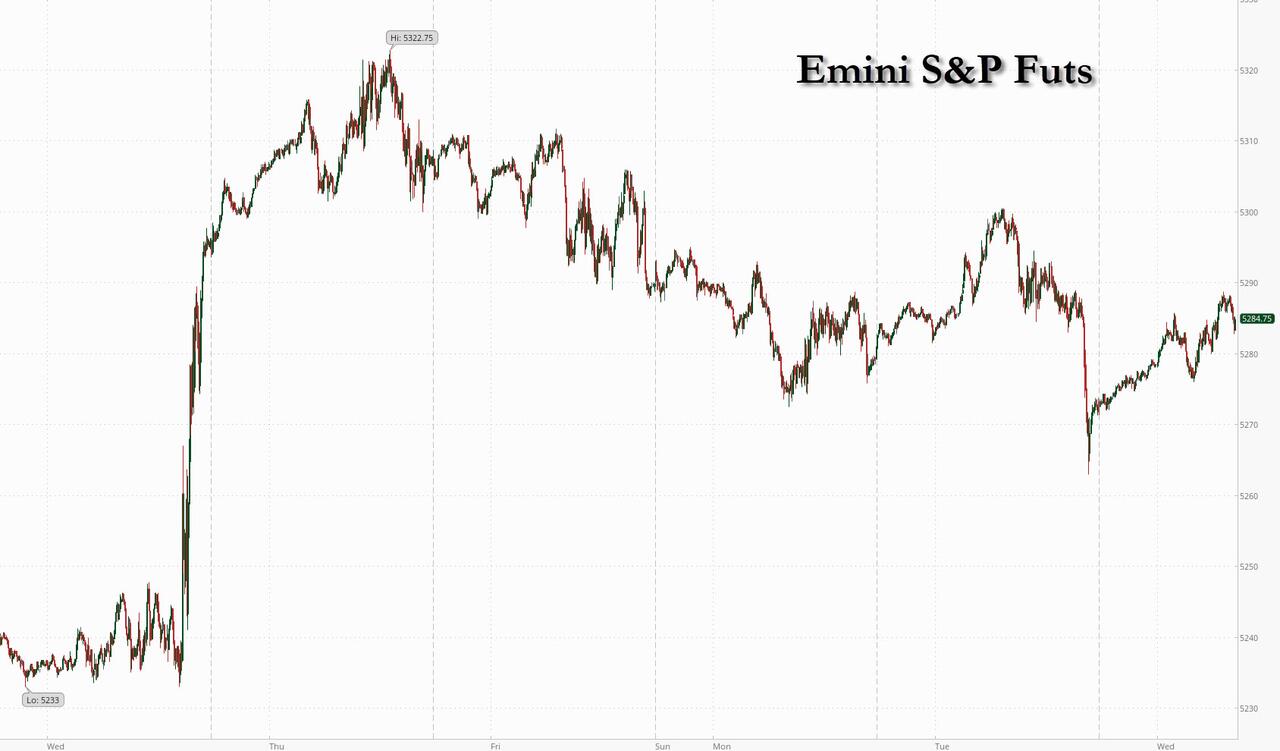

Indeed, equities closed out weak last night with the S&P 500 -0.28% lower yesterday, following in the footsteps of Monday’s -0.31% loss, with the Nasdaq (-0.42%) slightly underperforming. The S&P 500 had looked set for a very narrow but positive trading range, but then sold off by nearly half a percent in the final 30 minutes of the session, seemingly driven by quarter-end positioning.

Nvidia, the standout stock of the past year, led this late correction, falling from near flat on the day an hour before close to -2.57% at the close. That still leaves its shares up a more than heathy +86.9% YTD. There were also other contrasting moves within the Magnificent Seven (-0.52% overall). Apple fell early on following the news that iPhone shipments into China fell 33% year-on-year in February, but recovered during the session, ending the day as a modest underperformer (-0.67%). On the other hand, Tesla, which has so far trailed behind in 2024 (-28.5% YTD), was among the strongest performers in the S&P 500, rising +2.92% after new developments in the delivery of its self-driving assistance system. S&P (+0.37%) and Nasdaq (+0.38%) futures are back higher this morning.

Earlier on, equities had closed on the firmer side in Europe, with the STOXX 600 gaining +0.24% and the German Dax +0.67%, the latter supported by a moderate improvement in the GfK consumer confidence index from -29.0 to -27.4 (vs -28.0 expected). See Robin Winkler’s recent blog here on the green shoots we’re seeing in German data of late.

Government bonds have had a more difficult quarter but lacked a bit of direction yesterday. Yields rose a bit after decent durable goods data but fell back to broadly flat after a decent 5yr auction. $67bn was issued 1.0bps below the pre-sale yield, so it was a fairly solid auction, even as the indirect bidder share fell to 70.5%. The auctions for this week are far from over, as we have the US 2yr FRN ($28bn) and 7yr Notes ($43bn) auctions coming up later today. 10yr yields eventually fell -1.3bps on the day. 2yr Treasuries outperformed, with yields down -3.3bps. Markets slightly dialled back expectations of Fed cuts, trimming rate cut bets for 2024 by -1.4bps to 78bps.

The US data was mixed. As mentioned above, durable goods orders came in above expectations, up 1.4% (vs 1.0% expected), with core capital goods orders up +0.7% (vs. +0.1% expected). On the other hand, we saw some softer house price data, with the FHFA (-0.1% vs 0.3% expected) and the Case-Shiller 20-City (+0.14% vs +0.20% expected) house price indices for January seeing their weakest monthly prints since summer 2022 and early 2023, respectively. There were also mostly weaker signals in the survey releases. The Philadelphia Fed non-manufacturing activity index fell from -8.8 to -18 and the Richmond Fed’s manufacturing index fell to -11 (vs no change at -5 expected). The headline US Conference Board consumer confidence print for March declined to 104.7 (vs 107.0 expected). More encouragingly, the details of the print saw a rise in the jobs component, as the share of respondents saying jobs are plentiful rose to 43.1% (vs 42.8% prior), the highest level since July. This highlights a still tight labour market for now, which if maintained may weigh on the Fed’s decision to cut rates later this year.

Sticking with the US cycle, overnight Peter Sidorov published a report dissecting the recent resilience of economic activity to tight bank credit conditions. He sees a number of the tailwinds that supported this resilience last year as fading in 2024, leaving risks of a cyclical downturn in play. By contrast, he sees European growth as on track for a gradual cyclical upswing. See the note here for more.

Yesterday in Europe, we heard from the ECB’s Muller, one of the known hawks, who remarked that we are now “closer to [the] point where [the] ECB can start cutting rates.” Notably, Muller stated that “data may confirm inflation trend for ECB’s June meeting”, the first time he has explicitly commented on the June timing for the ECB’s potential next move. For more detail on the next step for the ECB, see the latest note from our European Economics team on the ECB policy path here. Off the back of this, markets increased their expectations of rate cuts, with the expected probability of a 25bps cut by the June meeting rising from 87% to 94% over the day. This sent both 2yr and 10yr bund yields down -1.1bps and -2.2bps, respectively. 10yr BTPs outperformed (-4.3bps) but OATs saw a more modest rally (-1.5bps) amid news that France’s budget deficit was larger than expected in 2023.

This morning in Asia, outside of the Japan move we discussed earlier, equity markets are mostly trading lower with the Hang Seng (-0.63%), CSI (-0.46%), Shanghai Composite (-0.52%) and the KOSPI (-0.17%) all on the weaker side.

Early-morning data showed that Australia’s inflation remained at +3.4% y/y in February for the third straight month against analyst expectations for a +3.5% gain. However, trimmed mean rose to 3.9% from 3.8% which is the first increase since last April and will be a bit uncomfortable for the RBA.

Elsewhere, China’s combined industrial profit for January and February rose sharply, advancing +10.2% y/y mainly because of a weaker base for comparison from last year.

Now to the day ahead. In terms of data releases, we have the Eurozone March services, industrial and economic confidence and the France March consumer confidence. We will hear from the Fed’s Waller and the ECB’s Cipollone. Lastly, we have the US 2yr FRN ($28bn, reopening) and 7yr Notes ($43bn) auctions.