As Easter Looms, Church Attendance In The US Declines

Christianity is on the decline in the United States.

As Statista’s Anna Fleck reports, new data from Gallup shows that church attendance has dropped across all polled Christian groups. As the following chart shows, the biggest drop in attendance in the past 20 years has been amongst Catholics, which has fallen from 45 percent of U.S. adults self-identifying as Catholic saying that they go to religious services weekly or at least every week in 2000-2003, down to 33 percent saying the same in 2021-2023. This is a decrease of 12 percentage points. Catholics’ attendance is lower than their Protestant counterparts, which saw a drop of 4 percentage points in that time frame from 48 percent of worshippers to 44 percent.

According to Gallup’s data, this decline in church attendance among Christians speaks to a wider pattern across religion in the U.S. generally.

Where an average of 42 percent of U.S. adults attended religious services every week or nearly every week 20 years ago, now this figure is just 30 percent.

This is largely due to an increase in the share of U.S. adults who self-identify as having no religious affiliation.

A breakthrough discovery links stress hormones with a fourfold surge in the spread of cancer, shedding light on why patients under severe stress often have lower survival rates.

“There’s probably very few situations that are as stressful as being diagnosed with cancer and undergoing cancer treatment,” Mikala Egeblad, cancer researcher and senior author of the study, told The Epoch Times.

Understanding the stress–cancer link may open up new ways to protect patients from the adverse effects of stress as part of cancer care.

An Accidental Discovery Prompts More Research

The team of scientists from Cold Spring Harbor Laboratory (CSHL) found that glucocorticoids—a type of stress hormone—play a role in creating a metastasis-friendly environment.

The Egeblad lab, which relocated to Johns Hopkins University, studies how the communication between tumors and the immune system affects tumor growth and metastasis in mice. Researchers discovered the connection accidentally, noticing faster tumor growth in mice they had unintentionally stressed by a change in housing.

The phenomenon prompted further research on chronic stress exposure and how it can encourage the spread of cancer, according to first author Xue-Yan He, who was a postdoctoral fellow at CSHL and is now an assistant professor at the Washington University School of Medicine.

Ms. He investigated this connection with a mice study that mimicked chronic stress, leading to startling observations: an increase in tumor lesions and up to a fourfold surge in the spread of cancer.

‘Spiderweb’ Structures Encourage Cancer Cells

According to the study published in Cancer Cell, the size of mammary tumors approximately doubled, and the rate of metastasis to the lungs increased between two- and fourfold compared with control mice not exposed to stress.

The researchers found that chronic stress impacts neutrophils, a type of white blood cell, causing an increase in neutrophil activation in the tissues where the cancer cells go.

When looking at lung tissue, the researchers found that chronic stress had altered the body’s internal environment in a way that could promote cancer growth by increasing neutrophils and then reducing T-cells, immune cells that kill cancer cells.

“We also found more extracellular matrix; this is a protein [network] that can support cancer cell growth,” Ms. He told The Epoch Times. Extracellular matrix helps cells attach to nearby cells and plays a vital role in cell growth and movement.

Ms. Egeblad explained that the neutrophils in the tissues formed spiderweb-like structures called neutrophil extracellular traps (NETs). Essentially, these traps are sticky webs of DNA meant to trap pathogens. However, in the case of cancer, NETs do not serve their usual protective role.

Instead, according to Ms. Egeblad and Ms. He, it appears that the NETs, induced by stress, encourage the growth of breast cancer cells that reach the lungs. “Our work shows how chronic stress activates neutrophils, helping cancer cells grow,” added Ms. He.

To confirm that glucocorticoids drive NET formation, leading to increased metastasis, the researchers performed three tests, each interfering with this pathway. First, they removed neutrophils from the mice using antibodies. Next, they injected a NET-dissolving enzyme. Lastly, they used mice whose neutrophils couldn’t respond to glucocorticoids.

According to Ms. He, each test achieved similar results: Depleting the neutrophils stopped stress-induced metastasis.

Chronic Stress Primes the Body for Developing Cancer

“Together, our data show that glucocorticoids released during chronic stress cause NET formation and establish a metastasis-promoting microenvironment,” the study authors wrote.

Unexpectedly, the study also showed that chronic stress can cause NETs to form and change lung tissues in mice without cancer, essentially preparing the body for cancer.

While this study highlights why managing severe stress is critical to cancer treatment, it also points to potential therapeutics that could target the formation of NETs or block the receptors for glucocorticoids.

“The next major directions that I see is understanding how much of this applies to humans and what can we do to to inhibit the stress in first, our animal models, and then eventually in patients,” said Ms. Egeblad.

She also hopes that understanding the stress response in patients will pave the way for better treatment and increased survival rates.

Unraveling the Deadly Stress-Cancer Alliance

Stress is unavoidable for someone navigating a cancer diagnosis. Many patients cite treatment decisions—and the surrounding uncertainty, anxiety, and even regret—as a source of distress, according to a 2023 study published in Scientific Reports.

In a review paper from 2023 published in the Annual Review of Psychology, researchers shared decades of data showing how stress reduction techniques improve outcomes for cancer patients. Techniques for stress management included:

Breathwork: This involves deep, slow breathing while concentrating on filling the lungs and relaxing muscles.

Progressive muscle relaxation: This technique involves tightening and then relaxing muscles. Most people start at either the toes or the head and progressively relax all the muscles across the body.

Meditation: With this technique, you can learn to relax your mind and concentrate on an inner sense of calm.

Yoga:Yoga focuses the mind on breathing and posture to promote relaxation and reduce fatigue.

Many of the findings in the review paper involved cognitive behavioral therapy (CBT) with a counselor, which focuses on actively changing thoughts and behavior. Patients were also taught to distinguish between stressors that are within their control and those that are not.

For stressors that feel like they are out of someone’s control, such as the uncertainties that come with facing a cancer care plan, relaxation techniques with social support seem to help patients manage anxiety.

Engaging with support groups and connecting with peers facing similar struggles provides a support network. Sharing experiences creates a sense of belonging, diminishing the isolation that can accompany cancer.

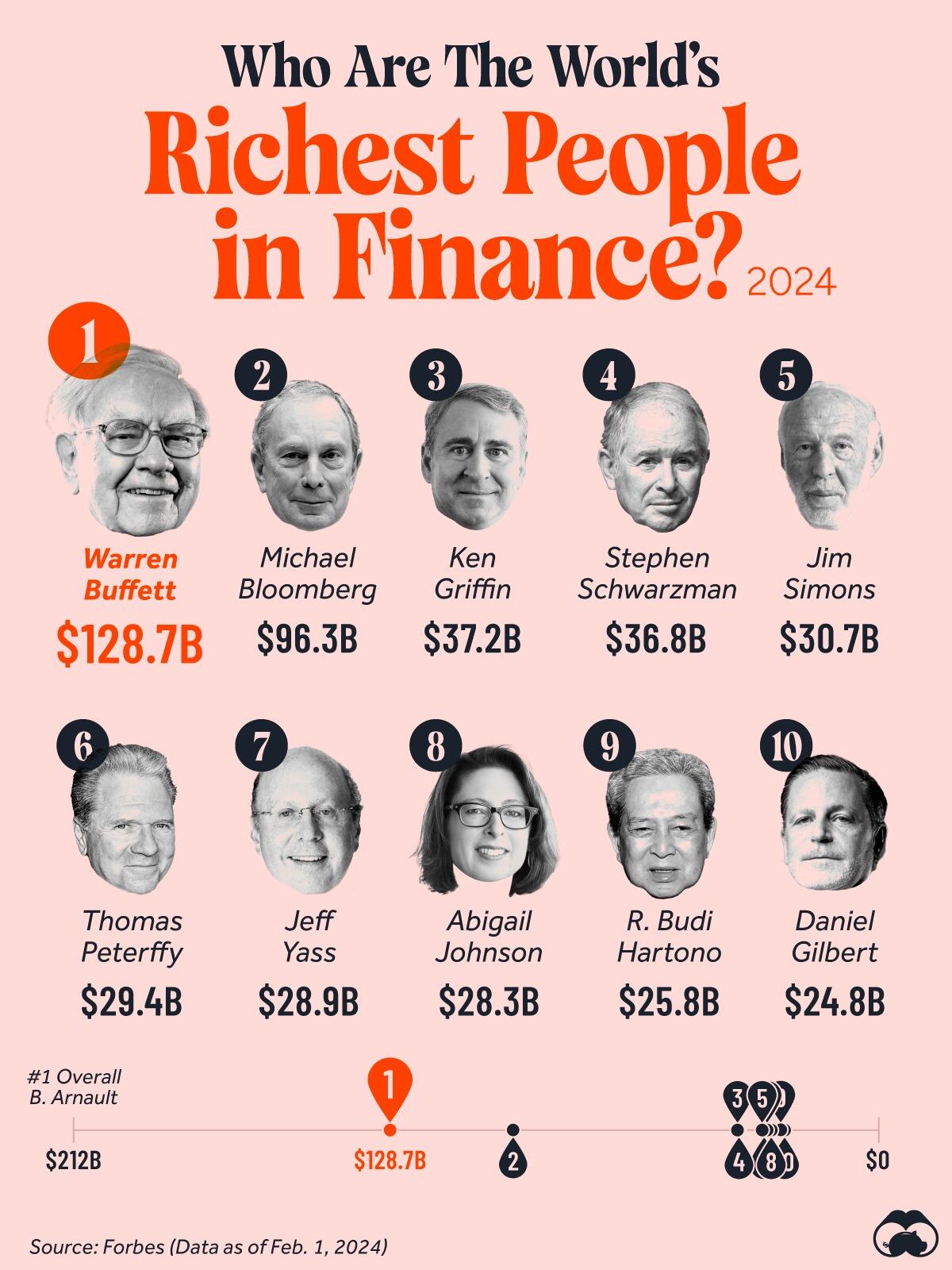

93-year-old Warren Buffett heads the list. The chairman and CEO of Berkshire Hathaway has a net worth of $128.7 billion.

Buffett’s Berkshire Hathaway portfolio is 62% invested in only three stocks: Apple (42.9%), Bank of America (10.2%) and American Express (9.1%).

Based in Omaha, Nebraska, where he has spent much of his life and where Berkshire Hathaway is headquartered, Buffett is also the 6th richest person in the world.

In second place is Michael Bloomberg, with $96.3 billion. Besides founding the financial data and media company Bloomberg LP in 1981, Bloomberg served as mayor of New York City for 12 years, from 2002 to 2013. A prominent philanthropist, he is committed to donating his stake in Bloomberg LP to Bloomberg Philanthropies when he dies.

In third place, Ken Griffin possesses almost a third of Bloomberg’s net worth. He founded and runs Citadel, a Miami-based hedge fund firm that manages $60 billion in assets. Stephen Schwarzman, Chairman and CEO of Blackstone Group, comes in fourth with $36.8 billion.

The only non-American is Robert Budi Hartono, one of the wealthiest people in Indonesia. His wealth comes from Djarum, one of the world’s largest producers of clove cigarettes, and Bank Central Asia, one of the country’s largest banks.

The lone female on the list is Abigail Johnson. She is the president and CEO of Fidelity Investments. Johnson took over the CEO position from her father in 2014.

Parents could be charged with child abuse if they prevent their minor daughter from getting an abortion, according to an Illinois law proposed by Democrat state Rep. Anne Stava-Murray.

In South Carolina, a new bill would require taxpayers to pay all childhood expenses—up to age 18—for babies born to mothers who were unable to get an abortion.

And the New Hampshire Legislature is wrestling with a proposal to ban abortion at 15 days of gestation, effectively banning abortion in the state, where it is currently allowed up to 24 weeks.

These recently introduced measures are just a few among a flood of proposals and changes triggered by the 2022 overturning of Roe v. Wade, which sent abortion regulation back to the states.

In November, voters in at least seven states will see abortion proposals on their ballots. Even in states where access to abortion isn’t on the ballot, voters may still cast votes for candidates who align with their beliefs on the issue.

Immediately after the Supreme Court’s decision to overturn Roe v. Wade, trigger laws in 13 states went into effect, completely banning or limiting abortions to very early pregnancy, with few exceptions. Last year, states without trigger laws, including Florida, North Carolina, and South Carolina, enacted similar pro-life laws.

Many states also enacted or proposed “safety net” legislation to help new and expectant mothers meet the demands of motherhood.

Ohio state Sen. Sandra O’Brien, a Republican, introduced SB 159, a tax credit for donations to pregnancy centers.

In Indiana, SB 98 identifies an unborn child as a dependent for tax purposes. The bill was sponsored by Republican state Sen. Andy Zay. Another Indiana safety-net bill would increase the Medicaid reimbursement rates for prenatal and postnatal care services.

Then there’s Kentucky’s bipartisan “Momnibus” legislation, an omnibus bill offering tax credits for adoption, and tax credits and grants for pregnancy help centers. It includes provisions for mental health service, parenting classes, and online and home visits for new mothers without transportation.

The pro-abortion movement is working hard to counter these actions and is striving for legislation and ballot measures that allow for abortion up to birth in many cases.

“You’re seeing a direct reaction from the other side that is panicking, based on the Dobbs decision,” Kelsey Pritchard, director of state public affairs at Susan B. Anthony Pro-Life America, told The Epoch Times.

“They are running as fast as they can to unlimited abortion funded by the taxpayer. And they’ve gotten so extreme on the issue.”

Seemingly every state has some movement in its legislature regarding abortion policy.

In South Carolina, where abortion is banned at six weeks of pregnancy, state Sen. Mia McLeod, who left the Democratic Party and became an independent, has proposed the “South Carolina Pro Birth Accountability Act” which will require taxpayers to pay women who would have aborted their baby “reasonable living, legal, medical, psychological, and psychiatric expenses.”

The bill compares a woman’s womb to rental property and reasons that in the surrogacy market, “a woman’s uterus is not unlike rental property, as a commissioning couple agrees to pay a gestational surrogate certain compensation for carrying a fetus to term and giving birth to a child.” It continues to say that since South Carolina may not constitutionally use a citizen’s rental property without just compensation, “it may not constitutionally require a woman to incubate a child without appropriate compensation.”

The bill stipulates that after a baby’s heartbeat is detected, the mother would be automatically enrolled in public assistance programs, including Temporary Assistance for Needy Families and the Supplemental Nutrition Assistance Program, and that those benefits could not be withdrawn until the child is 18.

The bill would pay a nurse to provide home visits from early pregnancy through the child’s second birthday; costs associated with health, dental, and vision insurance for the child until the age of 18; and a fully funded South Carolina 529 College Savings Plan for the benefit of the child. If the woman has a miscarriage, she may sue the state for compensation and damages.

In the case of an unmarried woman, the bill stipulates that if the biological father accrues more than $5,000 in child-support arrearage, he would be charged with a misdemeanor and, if convicted, could serve up to three years in prison.

“The court may suspend any portion of the prison sentence if the man consents to a voluntary vasectomy and to payment of restitution to the woman in the amount of the child-support arrearages owed,” the bill reads.

“I just want to make sure that those of us who call ourselves pro-life, that we are doing something to help the living, and my bill does that,” Ms. McLeod said in a February video posted on social media.

“It also gives my colleagues who refer to themselves as pro-life an opportunity to prove it by investing in South Carolina’s women and girls, and making sure that they have the resources and support that they need.”

Pro-life group South Carolina Citizens for Life opposes the legislation.

“Comparing a woman’s uterus to rental property and incentivizing men to have a vasectomy is really disturbing and vile language, and it’s intended to devalue members of our human family—born and waiting to be born,” Holly Gatling, the group’s executive director, told The Epoch Times.

“The intent of this bill is to obfuscate the fact that we have a vast network of pregnancy-care centers in South Carolina. … where women are given free health care … and diapers, formulas, job training, parenting classes, and assistance with getting back into a regular workforce and lifestyle by the time this baby is 2 years old,” she said. “So the bill is based on a false premise that we don’t do anything for mothers and babies after the child is born.”

In Pennsylvania, Democrat lawmakers say they want to “facilitate safe abortion access,” by reversing a 2011 state law requiring abortion businesses to meet all the same regulations as ambulatory surgical facilities, including submitting to unannounced inspections. It means abortion clinics, which sometimes fail health inspections, would no longer have to be inspected.

“Here in Pennsylvania, the pro-abortion extremism starts at the top with Gov. Josh Shapiro unilaterally eliminating the state contract for alternatives to abortion funding—a program that had bipartisan support and operated for 30 years under Republican and Democrat governors alike,” Michael Geer, president of Pennsylvania Family Institute, told The Epoch Times in an email.

Mr. Shapiro often expresses support for abortions in social media posts.

“Mifepristone will be available on the shelves in Pennsylvania,” he posted on March 1. “I’ll continue working to protect women’s access to abortion across this Commonwealth.”

Mifepristone is a progesterone-blocking drug that causes a woman’s body to abort her baby outside a doctor’s office.

“As long as I’m Governor, abortion will be safe, legal, and accessible here in Pennsylvania,” Mr. Shapiro posted on March 4.

The Shapiro administration made available online a form solely for complaints against pregnancy resource centers.

“It’s an agenda that prioritizes the profits of the abortion industry over the well-being of women and children in Pennsylvania,” Mr. Geer said.

Other Bills

In West Virginia, the state Senate has approved a measure requiring students in eighth and 10th grades to watch “Baby Olivia,” a video on fetal development. The video already is shown in North Dakota classrooms, and it could be legislatively required in Iowa, Kentucky, and Missouri. Pro-abortion activists oppose the short film, calling it medically inaccurate.

House Bill 2749 in Kansas would require abortionists to ask women why they are terminating their pregnancies and to rank their top reasons for seeking an abortion, including financial or health concerns, or that the pregnancy is a result of rape or incest.

In Oklahoma, where abortion is almost completely banned, House Bill 3013 would make trafficking abortion pills a felony, punishable by a $100,000 fine, 10 years in prison, or both.

A judge in Montana recently declared unconstitutional three laws passed by the state Legislature. The laws banned abortion after 20 weeks, required that pregnant women be given the opportunity to see an ultrasound of their baby before having an abortion, and required that abortion pills be administered in person rather than through telehealth. The laws were challenged by Planned Parenthood of Montana.

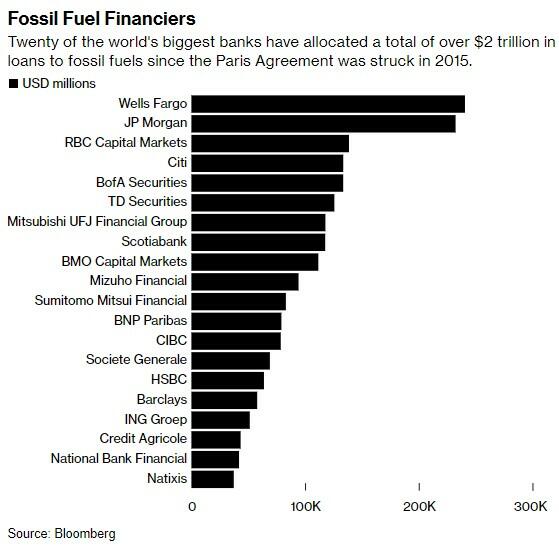

ESG Frustration And Backlash In The Banking Sector Continues

“Facts that don’t align with ill-informed prejudice are often infuriating. That doesn’t make them wrong. Someone needs to tell the truth about what it’s going to take to get to a net-zero future,” Emily Mir, a spokeswoman for Exxon, said earlier this month.

And that’s exactly what Judson Berkey at UBS has done, the focus of a new Bloomberg report. Berkey let loose on a recent conference call with regulators about how unrealistic climate goals were for banks trying to integrate them into their respective economies.

The report covering Berkey’s outburst simply concluded that the “world’s biggest banks can’t live up to the green regulatory ideal unless they start dumping huge numbers of clients worldwide at a reckless pace and also roil economies in large swathes of the globe that primarily rely on dirty fuels.”

Berkey was on a “check-in” call where regulators query market participants about regulations, the report says, when he expressed his frustration, interjecting: “Banks are living and lending on planet earth, not planet NGFS [Network for Greening the Financial System]”.

The outburst is a microcosm of “cracks” emerging in the banking sector after being draped with regulations about sustainability, the report says. Bridgewater Associates founder Ray Dalio famously said last year about ESG: “You have to make it profitable.”

Its indicative of new-world climate regulation going head to head with old world capitalism, the report says.

Adair Turner, chair of the Energy Transitions Commission in Britain said: Climate change is “an economic externality, and you can’t expect a free market to deal with it voluntarily.”

Banks reevaluating their net zero commitments are facing challenges as they confront the practical implications of these pledges, which include limitations on operating in coal-reliant regions like South Africa, Poland, and Indonesia. These commitments also complicate relationships with clients across various sectors, from commodities firms to companies with less obvious carbon impacts.

Jonathan Hackett, head of sustainable finance at Bank of Montreal, added: “Our net zero commitments are about being our clients’ lead partner and are consciously taken around the idea that we need to be there with our clients and our clients need to succeed, not that we need to hyper select clients in order to get to net zero somehow faster or better.”

A recent sustainability report from UBS highlighted a “notable shift in emphasis” in climate change discussions, moving from net zero pledges to recognizing the need for a transition phase. The Swiss bank noted that high inflation and input costs will be crucial factors for clients as they develop decarbonization strategies.

James Vaccaro, Chief Catalyst at Climate Safe Lending Network, added: “For banks with substantial capital markets businesses, like those competing with the JPMorgans of the world, it’s fee income that’s on the line here. Ditching clients off track from 1.5C means losing major lines of revenue.”

In sum, the financial industry’s initial rush to commit to net zero carbon footprints at the 2021 COP26 summit in Glasgow has hit a reality check. Banks that pledged to reduce financed emissions and invest billions in green and sustainable deals are reevaluating these commitments after facing the complex realities of implementing such drastic changes.

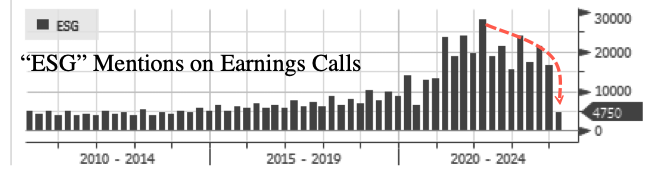

It should be no surprise to our readers: we have been pointed out the collapse of ESG for more than a year now. Earlier in March we wrote how Exxon’s CEO had all but declared victory over the “woke” ESG lobby.

In February, we noted that CEOs were ditching ESG lingo on conference calls. For some context, peak ESG and related synonyms, such as “climate change” and “clean energy” and green energy” and net zero,” among other terms, peaked at 28,000 mentions in the first quarter of 2022. Ever since, the number of mentions has rapidly plunged. Halfway through the first quarter earnings season, mentions are around 4,800.

Andy Wiechmann, the Chief Financial Officer of MSCI, mentioned during his earnings call that “Clients are taking a more measured approach to how they integrate ESG.”

On a Jan. 12 earnings call, BlackRock CEO Larry Fink explained how his firm plans to purchase private equity firm Global Infrastructure Partners without mentioning ESG. This makes sense since BlackRock dropped the ESG term after blowback last summer.

Recall, we also wrote last year about the dying off of ESG and “green” investment products. At the end of 2023, Goldman Sachs shuttered its ActiveBeta Paris-Aligned Climate U.S. Large Cap Equity ETF.

Bloomberg ETF analyst Eric Balchunas pointed out in late 2023 that “there was just way too much supply for the demand” with the ETF and that “it’s going to get worse too”. Balchunas says the ETF only took in $7 million over the course of 2 years.

We also wrote about Jeff Ubben late last year, who shuttered his sustainability fund – calling traditional climate summitry an “echo chamber” of diplomats. Less than a week before that we noted that $30 billion had been shaved off the value of clean energy stocks over the preceding 6 months.

Finally, we pointed out last year how the ESG grift was reaching endgame after Markus Müller, chief investment officer ESG at Deutsche Bank’s Private Bank stated that sustainability funds should include traditional energy stocks, arguing that not doing so deprives investors of a prime opportunity to invest in the transition to renewable energy.

The cargo ship that crashed into Baltimore’s Francis Scott Key Bridge on March 26 was carrying more than 50 hazardous material containers, some of which were breached during the collapse, according to the National Transportation Safety Board (NTSB).

NTSB chair Jennifer Homendy said during a press conference on March 27 that the agency, which is currently probing the crash, had obtained a cargo manifest of the 984-foot-long Singapore-flagged cargo vessel named Dali.

The vessel—which reportedly lost power while transiting out of Baltimore Harbor and struck the bridge—had 56 containers of hazardous materials on board at the time of the incident, Ms. Homendy said.

The NTSB chair said a senior hazmat investigator had identified the containers.

“That’s 764 tons of hazardous materials—mostly corrosives, flammable, and some miscellaneous hazardous materials—class nine hazardous materials which would include lithium-ion batteries,” Ms. Homendy said.

“Some of the hazmat containers were breached,” she added.

Asked how many of the containers were in the water, the NTSB chair could not provide an exact number.

“I did see some containers in the water and some breached significantly on the vessel itself,” she said. “I don’t have an exact number but it’s something that we can provide in an update and certainly in our preliminary report which should be out in two to four weeks.”

‘Sheen’ Observed On Water Around Collapse

Officials have also observed a sheen—sometimes caused by gasoline or oil—on the waterway surrounding the collapsed bridge that spans the Patapsco River. According to Ms. Homendy, federal, state, and local authorities are aware of this and are currently working to address those issues.

“The NTSB as part of our safety investigation documents that type of release, it documents the damage and and documents the type of materials involved as part of our investigation,” Ms. Homendy said.

Asked by one reporter to characterize the level of concern regarding the hazardous material leak and the sheen on the water, Ms. Homendy declined to respond and directed him to state and local authorities.

The NTSB will also not provide any of its findings while the investigation remains ongoing, Ms. Homendy noted.

Dali struck the Francis Scott Key Bridge at about 1:27 a.m. on March 26 while leaving the harbor, according to officials.

The incident resulted in the bridge collapsing moments later while eight construction workers—who officials say were from Mexico, Guatemala, El Salvador, and Honduras—were filling in potholes.

Police Recover Bodies

Two of the workers were rescued on March 26 soon after the collapse, officials said. One of them was uninjured and the other was hospitalized in a “very serious condition” but later released.

On March 27, police announced that two bodies had also been recovered during search-and-recovery efforts.

The families of Alejandro Hernandez Fuentes, 35, and Dorlian Castillo Cabrera, 26, have been notified, Col. Roland L. Butler Jr., superintendent of the Maryland State Police, said.

Police discovered their bodies inside a pickup truck that was submerged approximately 25 feet below water in the Patapsco River, around the middle section of the bridge, according to the superintendent.

The two men were with the company, Brawner Companies, doing maintenance on the bridge deck, he said.

The U.S. Coast Guard is continuing recovery efforts in the search for the remaining four missing individuals.

According to Ms. Homendy, the 95,000 gross-ton container ship also sustained damage during the incident, although none of the 21 crew members and two pilots who were onboard at the time sustained significant injuries.

Officials have praised those on board for saving countless lives by raising a mayday alarm just moments before the incident, allowing authorities to limit traffic on the bridge before it collapsed.

The Tower Of Sauron Can’t Pay Its Debt: Brooklyn’s Tallest Building Is In Foreclosure

While everyone says that the looming commercial real estate crash is nothing to worry about since, well, everyone’s been worrying about it for so long and nothing bad has happened yet (except for the whole regional bank crisis last March when virtually anyone who is not JPM almost imploded), every day we get a new and more shocking foreclosure or default.

Today, it is the infamous Brooklyn Tower, the 1066-foot building, sometimes called the Eye of Sauron, which is the tallest in all of Brooklyn. According to marketing materials from JLL, Silverstein Capital Partners has scheduled a foreclosure auction for 9 DeKalb Ave., JDS Development’s Brooklyn Tower.

JDS took out a $240M mezzanine loan from Larry Silverstein’s firm in 2019 as part of a $664M debt package to build the 93-story, 1,066-foot tower in Downtown Brooklyn. Yet despite what the media said was a flood of interest in the property, less than five years later, JDS has defaulted on the loan, according to the foreclosure notice, first reported by ten31 on X, triggering the foreclosure auction, scheduled for June 10.

To lock in the entire capital structure, Silverstein also bought the property’s senior debt, a $424M mortgage originally provided by Otéra Capital, earlier this year. A spokesperson for Silverstein told Bisnow in an email that the junior, senior and mezzanine loans for 9 DeKalb are all in default and that Silverstein is enforcing its rights as a lender, i.e., the Eye of Sauron is about to have a new master.

The mezz loan was the first debt handed out by Silverstein Capital Partners, which was launched in 2018. It has raised over $4B since then and provided debt to projects like Hudson Cos.’ One Clinton condo and retail development in Brooklyn Heights.

JDS, led by Michael Stern, tried to sell the 398-unit rental portion of 9 DeKalb, which also features 143 condos, a little over a year ago, The Real Deal reported. At the time, JDS was reportedly seeking between $600M and $700M for the rental units. Judging by today’s news, they weren’t successful.

Construction on the tower, which sits atop the historic Dime Savings Bank and Junior’s restaurant, began in 2015. The property, which is Brooklyn’s first supertall at just over 1,000 feet, also contains a 130K SF retail portion largely occupied by Life Time Fitness. Unit 72A this week set the record for Brooklyn’s priciest studio apartment when it sold for $905K, 6sqft reported.

The IRS is reminding taxpayers who have not filed their 2020 returns to do so quickly or risk losing out on unclaimed refunds.

Nearly 940,000 Americans have unclaimed refunds from the 2020 tax year worth an estimated $1 billion, the IRS said on March 25. The individuals face a May 17 deadline to submit their returns.

The median refund is $932. American citizens typically have up to three years to file and claim refunds, after which the money goes to the U.S. Treasury.

Since taxpayers may find it difficult to gather information necessary to file returns for 2020, the IRS outlined three ways to access such information:

Taxpayers who are missing their W-2, 1098, 1099, or 5498 forms can request copies from their employer, bank, or other payers.

Those who are unable to get these forms from employers, banks, or other payers can order a free wage and income transcript at IRS.gov using the agency’s online tool. The agency noted that this will be the quickest and easiest option for many individuals.

A third way is for the individual to file a 4506-T form with the IRS, requesting a “wage and income transcript.” Taxpayers can then use information to file their returns. The agency warned that written requests for such transcripts can take several weeks. As such, taxpayers are encouraged to try out other options first.

Usually, the deadline to claim old refunds is around the regular tax deadline, which is April 15 this year. The three-year window for the 2020 returns had been extended to May 17 due to the COVID-19 pandemic.

“We want taxpayers to claim these refunds, but time is running out for people who may have overlooked or forgotten about these refunds. There’s a May 17 deadline to file these returns so taxpayers should start soon to make sure they don’t miss out,” said IRS Commissioner Danny Werfel.

Since taxpayers faced “extremely unusual situations” during the pandemic, some of them may have forgotten about a potential refund on their 2020 returns, he stated.

“People may have just overlooked these, including students, part-time workers, and others. Some people may not realize they may be owed a refund. We encourage people to review their files and start gathering records now.”

In addition to missing out on refunds, failure to file the 2020 return could also result in some taxpayers losing out on the earned income tax credit, which was worth as much as $6,600 in 2020.

“The IRS reminds taxpayers seeking a 2020 tax refund that their funds may be held if they have not filed tax returns for 2021 and 2022,” the agency said.

“In addition, any refund amount for 2020 will be applied to amounts still owed to the IRS or a state tax agency and may be used to offset unpaid child support or other past due federal debts, such as student loans.”

The state with the highest number of individuals estimated to have 2020 refunds due was Texas, with 93,400 taxpayers. This was followed by California with 88,200; Florida with 53,200; and New York with 51,400.

Processing Refunds

The IRS usually takes up to 21 days to process refunds for returns filed electronically. It can take four weeks or more if traditional mail was used. The processing time can be extended in case the returns require extra review or corrections. The fastest way to get refunds is through direct deposit.

In certain cases, taxpayers may not receive the refund amount they were expecting. This could be due to the agency identifying errors on tax returns, or if the refund was used to pay off certain state or federal debts owed, or if the refund from a joint return was used to pay off a spouse’s debts.

In case of errors corrected by the IRS, the agency will send a notice to the taxpayer clarifying the changes.

Tax refunds are critical for many American households as they represent the largest annual cash injection into their budgets. Many families use the refunds to boost their savings or cut down debts.

According to a January survey conducted by Credit Karma, 37 percent of taxpayers who expect to receive a refund plan on using some or all of the money to pay for necessities. Over half of the respondents said they were looking to file their taxes early to get faster refunds.

Thirty-one percent of taxpayers surveyed said they would need their refund to make ends meet.

“That number jumps to 40 percent for millennials and 38 percent for Gen Z taxpayers,” the survey report stated.

In addition to encouraging 2020 tax year nonfilers to file their returns, the IRS has launched an effort to identify high-income taxpayers who have not filed their income taxes since 2017. Over 125,000 such instances have been identified, with taxes being owed in many of these cases.

The initiative was launched late last month, with the agency sending compliance letters to these 125,000 taxpayers.

“The mailings include more than 25,000 to those with more than $1 million in income, and over 100,000 to people with incomes between $400,000 and $1 million between tax years 2017 and 2021,” the agency stated.

Mr. Werfel said that if someone hasn’t filed a tax return in recent years, “this is the time to review their situation and make it right. … For those who owe, the risk will just grow over time as will the potential for penalties and interest. These non-filers should review information on IRS.gov that can help and consider talking to a trusted tax professional as soon as possible.”

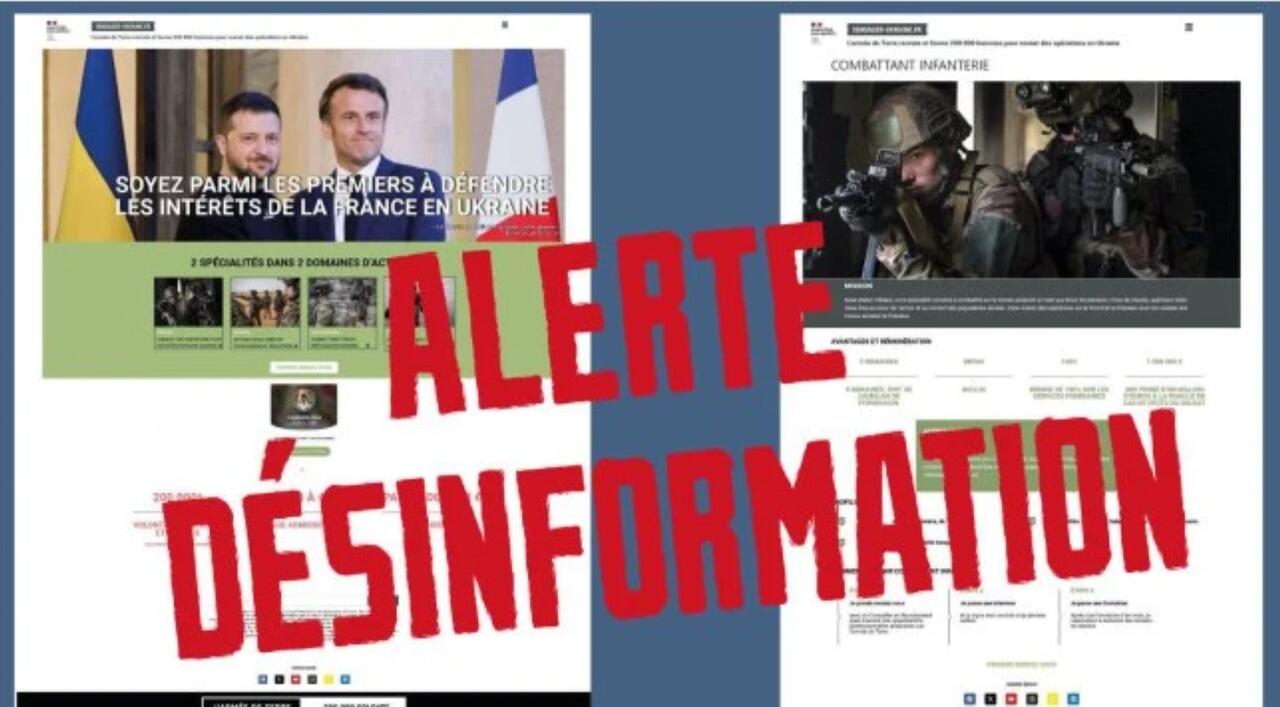

France Takes Down Fake Ukraine War Recruitment Website Targeting Immigrants

In a bizarre and unprecedented situation, France has flagged what officials are calling a fake recruitment website which seeks volunteers to fight on behalf of Ukraine in the with Russia. It reportedly was made to look official, to the point of misleadingly presenting itself as a French government-promoted campaign.

France’s defense ministry has shut down the website, saying it was created by malicious actors as part of a “disinformation campaign”. Ukraine’s armed forces have of late been desperate for new recruits while facing devastating losses and thus face a severe manpower shortage.

“A URL for a page called ‘Join Ukraine,’ which used [French] government website templates, is currently being circulated online; this website is fake,” a message on the site reads, according to AFP.

The fake Ukraine volunteer website “invited” 200,000 French citizens to enlist in Ukraine’s national forces, and even emphasized that immigrants to France could serve. Volunteers were told to contact “unit commander Pavel” in order to gain instructions on the process of enlistment.

French authorities did not identify a culprit behind the deceptive campaign; however, a source told AFP that evidence possibly points to the Russian mercenary group Wagner being behind it.

Another government official told AFP that it bore “the hallmarks of a Russian or pro-Russian effort as part of a disinformation campaign claiming that the French army is preparing to send troops to Ukraine.”

Starting last month French President Emmanuel Macron stunned even Western allies by pushing for European countries to consider sending troops to fight in Ukraine.

He had told a Paris-hosted security conference in late February that while there was yet “no consensus” on sending ground troops to Ukraine in an “official manner,” it remains that “nothing was excluded.” He later defended the remarks and said the West cannot allow Russia to win in Ukraine no matter what.

This new fake recruitment website episode could be part of an attempt to troll or mock Macron and call attention to his very dangerous proposal, which would be a sure path to WW3 with Russia. Germany among other powerful allies has opposed Macron’s words.

🇫🇷 🇺🇦 🪖 ❌ #France‘s #defence ministry warned against a fake government website propagating #misinformation, inviting people to defend the country’s interests in #Ukraine.

Early in the war more than two years ago some Western leaders, particularly then UK Prime Minister Liz Truss, were vocally encouraging foreign volunteers to go to Ukraine. But as more and more Westerners died in battle, officials have backed off such public statements.

President Zelensky in February signed a decreeopening up Ukraine’s military forces to“foreigners and stateless persons” for the first time ever. The country already had a “foreign legion” but volunteers can now serve in Ukraine’s National Guard, per the recent order, and may sign a contract at the private, sergeant, or officer levels depending on their qualifications.

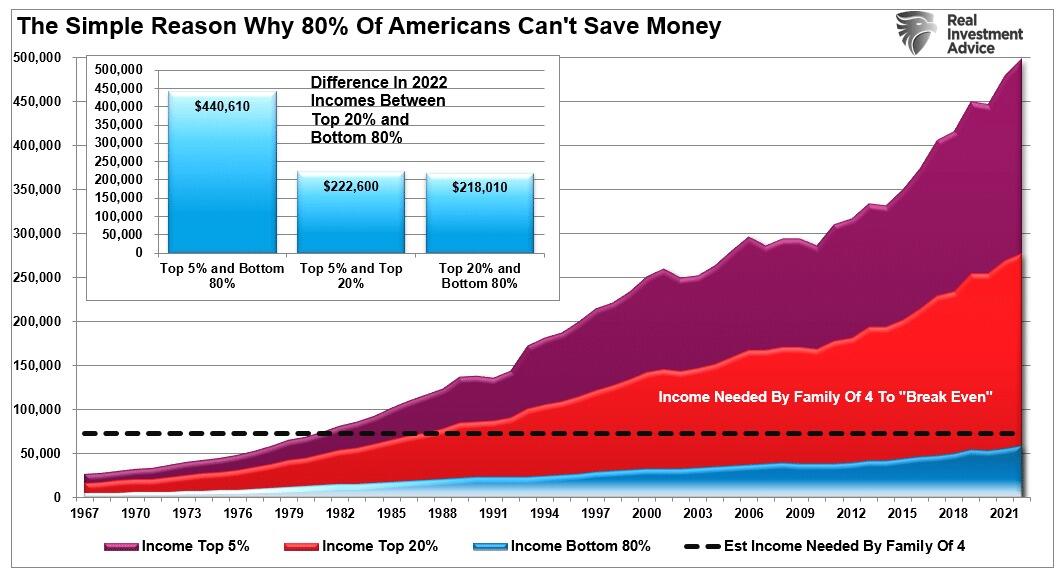

One of the most interesting conundrums is the surging wealth gap in America. Despite two of the largest bull markets in history since 1980, most Americans struggle with making ends meet and are unprepared for retirement. Such a reality starkly differs from the belief that rising asset prices benefit the masses.

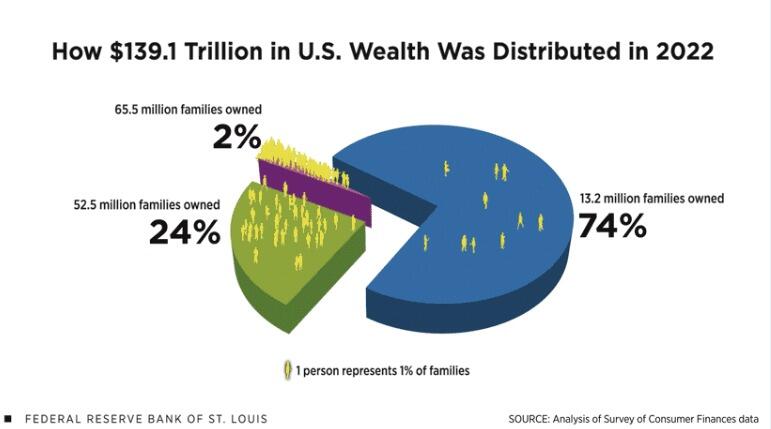

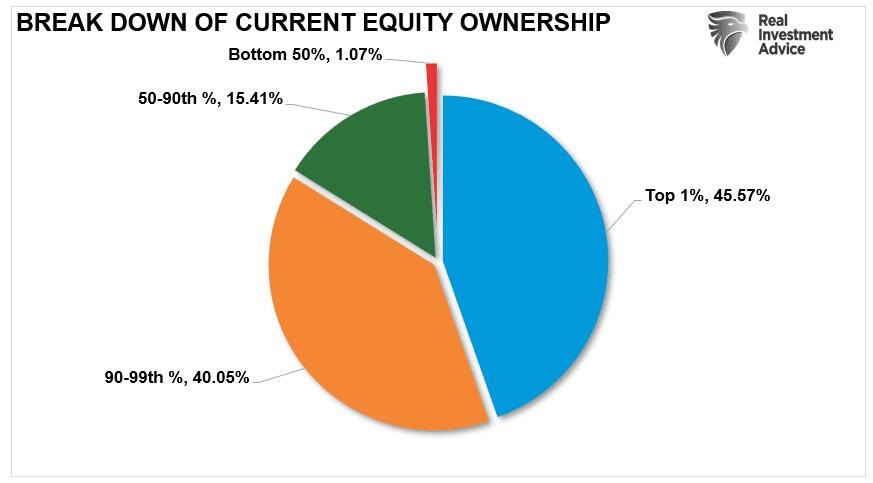

For example, in a recent St. Louis Federal Reserve Bank analysis, total household wealth was $139.1 trillion, covering 131 million families. Of that total wealth, 74% was owned by just 13.2 million families, or roughly 10% of the population.

Notably, this measure of wealth includes the equity of the family’s home. While home equity is essential, it is not readily spendable without taking on debt to extract the value. Therefore, Americans’ “liquid wealth” is far more unequally distributed. However, such is hard to fathom given the endless parade of media and social media influencers extolling the virtues of “building wealth through investing.”

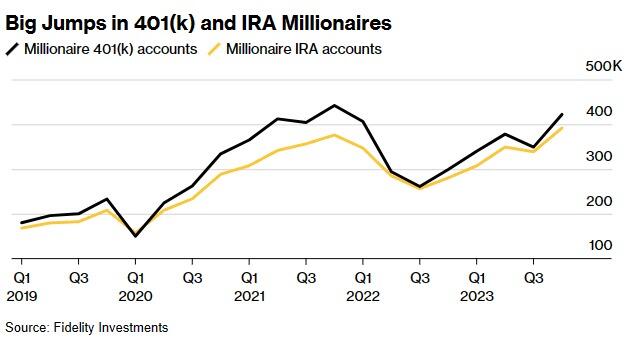

Interestingly, that survey came after the Government injected nearly $5 trillion into the economy, a massive surge in deficit spending, and the Fed’s $120 billion monthly injections doubled asset prices from the March 2020 lows. Unsurprisingly, in February, Fidelity published its latest analysis showing the number of retirement accounts with balances of more than $1 million surged toward a record. To wit:

“The number of seven-figure 401(k) accounts at Fidelity Investments jumped 20% in 2023’s final quarter to 422,000, marking a sharp recovery from the previous quarter’s 7.7% drop.

Gains in the stock market helped swell retirement balances last year as the S&P 500 advanced 24% following 2022’s 19% decline. The impressive run was powered in large part by the so-called “Magnificent 7” stocks that now make up roughly 30% of the market-cap weighted S&P 500 Index. The only time when the ranks of 401(k) millionaires at Fidelity was higher was in 2021’s fourth quarter, when there were 442,000 such accounts. Elsewhere, the number of seven-figure IRAs is at a record 391,600 accounts.” – Bloomberg

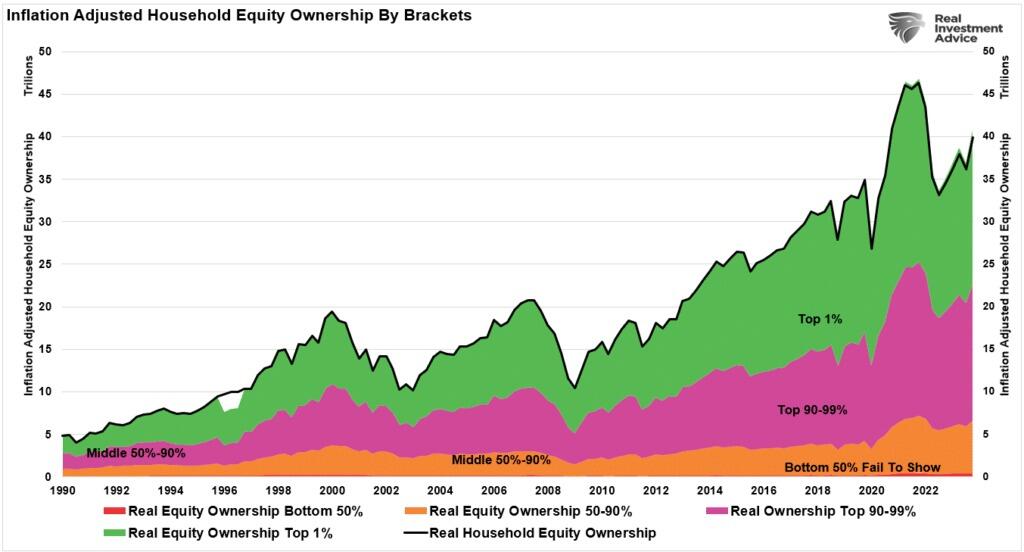

However, that data obfuscates the stark wealth gap below the surface. While the “number of retirement millionaires” made headlines, an essential piece of the analysis was overlooked. Those 422,000 accounts comprised only a tiny fraction of Fidelity’s 27.2 million retirement accounts. How small of a fraction? About 1.6%. That number aligns with America’s Top 1% of equity ownership.

But indeed, after two booming bull markets since 1980, most Americans would be well saved for retirement. Unfortunately, that is not the case.

So, what went wrong?

The 50% Problem

The advice to build wealth is quite simplistic. Investment money into the financial market consistently over long periods. That’s it.

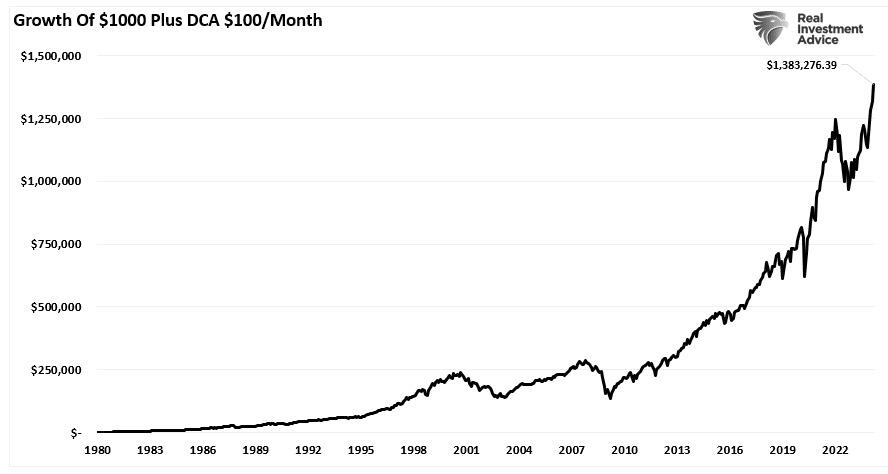

Again, considering that most Americans alive today participated in either one or both of the most significant secular bull markets in history, the lack of wealth is quite appalling. If individuals had invested $1000 in 1980 into the S&P 500 index and added just $100 per month, they would have roughly $1.4 million in retirement savings today.

However, if it is so simple, why do most Americans have little or no savings?

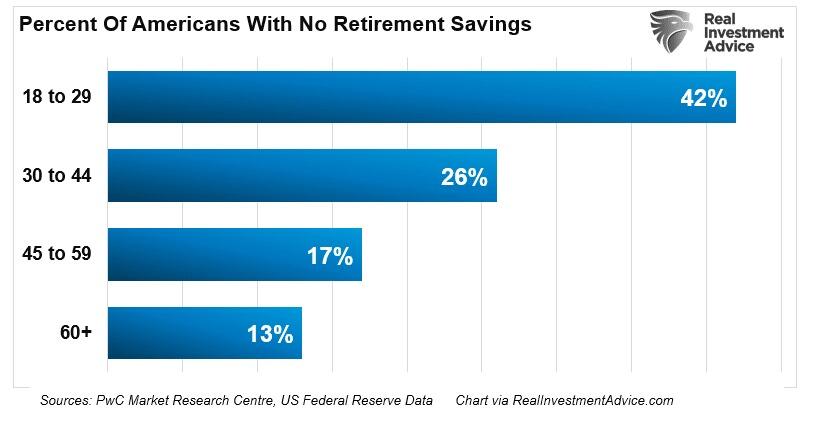

“One in 4 Americans have no retirement savings and those who are saving aren’t saving enough. Those that are [saving], on average, what they have saved will afford them like $1,000 a month of actual cash while they’re in retirement.” – Price-Waterhouse Retirement In America.

The report found that the median retirement account balance for 55-to-64-year-olds is $120,000. Dividing over 15 years would generate a modest monthly distribution of less than $1,000. The bigger problem is the large percentage of individuals with no retirement savings.

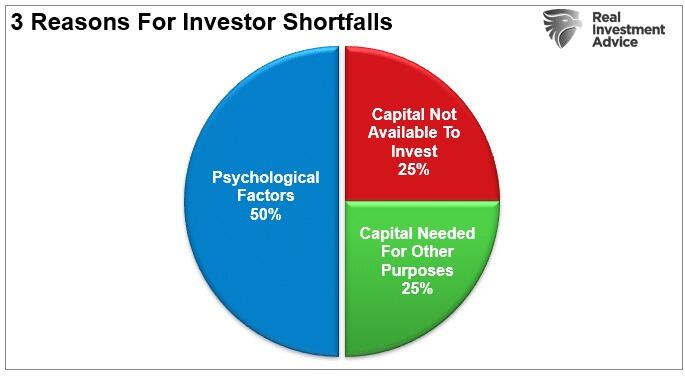

There are two primary reasons individuals do not save and invest for retirement. While psychological reasons account for 50% of the problem, such as buying high and selling low, the other 50% comes down to a lack of capital to invest.

We have previously written about the various psychological pitfalls investors make in destroying their investment capital. However, for many, it is a problem of being unable or unwilling to save money.

Lack of knowledge about budgeting and saving. (15%)

The cost of living exceeds income.(70%)

Bad previous investing experience (bear market).(15%)

If you ask anyone who doesn’t save money, you will likely get one of those three answers. It is hard to “save and invest” when there simply isn’t enough income.

However, this is where the disconnect between the economic data and the “average American” is exposed.

Not Enough Income

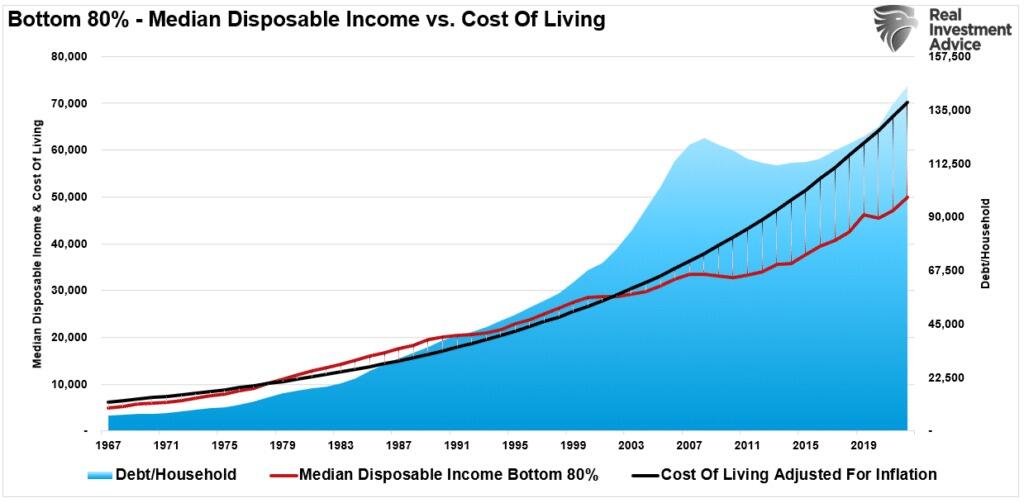

Most mainstream analysis utilizes “averages” to discuss the economy’s health.For example, disposable incomes (DPI), personal savings rates, and debt-to-income ratios suggest that the average American family is flush with cash with little debt. However, most of these calculations, like DPI (income minus taxes), are generalizations due to the variability of household income and individual tax rates.

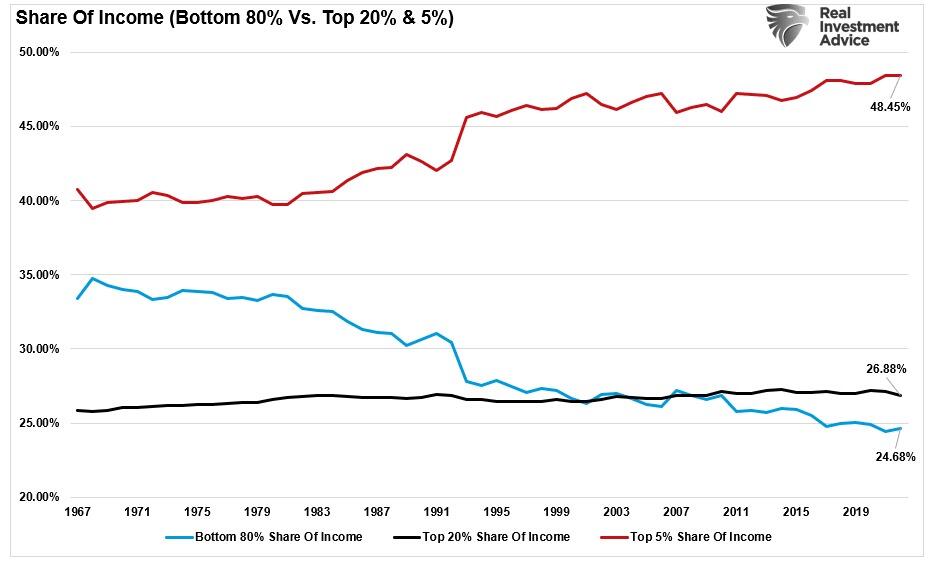

More importantly, the measure becomes skewed by the top 20% of income earners, notably the top 5%. The chart below shows those in the top 20% saw substantially larger median wage growth versus the bottom 80%. (Note: all data used below is from the Census Bureau and the IRS.). The cost of raising a family of four continues to increase with inflation, so the bottom 80% are forced to live paycheck-to-paycheck, primarily leaving no money for retirement savings.

Furthermore, disposable and discretionary incomes are two very different animals.

Discretionary income is the remainder of disposable income after paying for all mandatory spending like rent, food, utilities, health care premiums, insurance, etc. For the bottom 80% of income earners, the cost of living outstrips most of those individuals’ incomes. Debt must make up the difference.

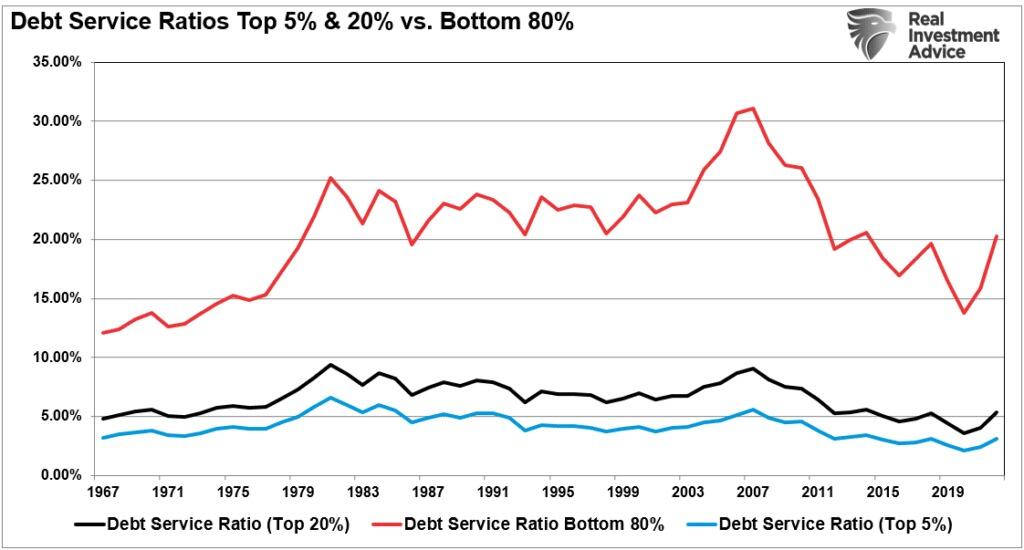

In other words, given the bulk of the wage gains are in the upper 20%, any data that reports an “average” of the information skews the results higher. This is why there is a vast difference between the debt service levels (per household) between the bottom 80% and the top 20%.

Yes, saving money and investing it into the financial markets is tough when you must go further into debt every month to make ends meet.

The Wealth Gap And The Road To Serfdom

The rise and fall of stock prices has little to do with the average American’s participation in the domestic economy. Interest rates and inflation are entirely different matters. Since interest rates affect “payments,” and inflation increases the “costs of living,” changes negatively impact consumption, housing, and investment.

Therefore, while the stock market surges to all-time highs, the wealth gap leaves increasing numbers of Americans behind. For the average American, it isn’t a choice of not wanting to participate; they simply can’t.

The reality is that middle-class America continues to shrink as the wealth gap increases. The rich can invest, save, and use little debt to sustain living standards. People experiencing poverty rely on debt, making long-term prosperity an impossible goal.

Furthermore, as the peasants demand “more free stuff” from the Government, such requires more debt and higher taxes. Those demands divert more capital away from productive investment, leading to slower economic growth. As growth slows, businesses shift to the lowest labor costs, or automation, to lower income growth for domestic workers. Such leads to more demands from “free stuff” from the Government, and the cycle intensifies, pushing more of the middle class downward.

The share of annual incomes between the bottom 80% and the top 5% is evidence of that wealth transfer from the middle class.

The “road to serfdom” is paved with good intentions. After decades of piling on increasing debt levels to generate economic growth, the damage to economic growth is becoming more visible. Economic growth trends are already falling short of previous long-term growth trends.

Of course, this analysis also underscores why bitter economic sentiment persists even as the bull market registers all-time highs. It is hard to be excited about a booming stock market when you don’t participate much, if at all.

For 80% of Americans, the end game of too much debt, an aging demographic, and the push for “socialistic policies” is the continued extraction of wealth from the “middle class” to the “rich.”

Of course, we don’t have to look much further than Japan to see how this eventually works out. They don’t have a middle class, either.