Key Events This Week: Payrolls, Powell, ISM And Fed Speakers Galore

With the first quarter officially in the books, and just days until we start getting Q1 earnings (it sure does feel like we now live in one extra long earnings season), we have quite a few events this busy week starting with today’s March manufacturing ISM print – which as noted earlier printed at 50.3, up from 47.8, above the 48.3 consensus and the first print above the 50 threshold reading since September 2022 (sparking a selloff in Treasuries and pushing the USD lower). Beyond today we get lots of Fed Speak (at least 8 speakers on deck including Jerome Powell), Friday’s Payrolls, Euro Zone CPI and OPEC+ EURA.

The flood of scheduled Fed speakers will likely set the tone for the new quarter and month, including appearances from Chair Jerome Powell (who also spoke on Friday reiterating his previous non-committal comments) and the incoming St. Louis Fed President Alberto Musalem. The US jobs report due on Friday needs no introduction while the ISM surveys are also worth watching for an update on the health of the US economy.

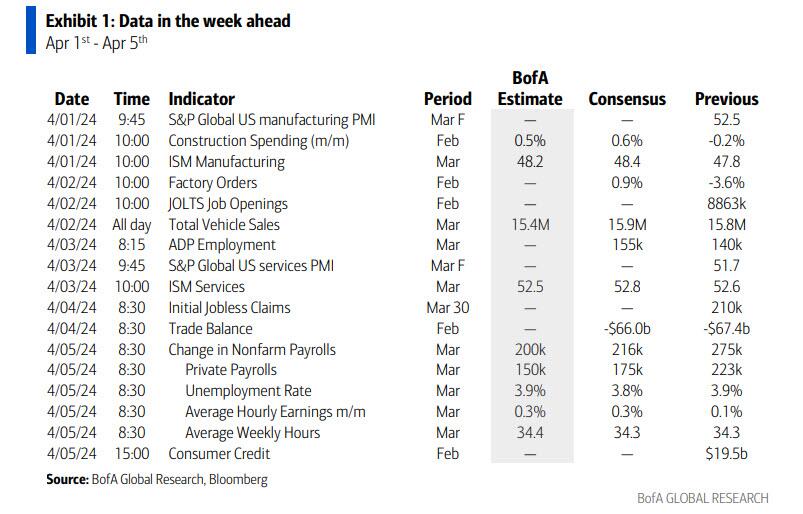

The March jobs report (Apr 5) will be the main focus in the coming week. Consensus expects nonfarm payrolls to increase by 200k (vs. 275k in February). One of the reasons BofA is calling for a slowdown in job growth is that payrolls in the month of March have shown a tendency to be weak relative to February in recent years. For a similar reason, the bank is expecting private payrolls to slow from +223k in February to a below-consensus +150k in March. Average hourly earnings (AHE), meanwhile, are likely to rise by 0.3% m/m or 4.1% y/y. The quits rate and posted wage growth from Indeed point to a moderation in y/y rates for AHE. Average weekly hours should increase by a tenth to 34.4.

On the household (HH) survey side, BofA expects the unemployment rate (u-rate) to remain at 3.9%. But the HH employment data have been much weaker than NFP in recent months. This means we could see some payback – e.g. stronger HH employment growth than NFP and a lower u-rate. But if the divergence continues, there is risk of a higher u-rate. Also, expect the labor force participation rate to recover by a tenth to 62.6%. This is because BofA expects a rebound in the 16-24 years category, which declined by 0.4ppt in February

In Europe, consumer price data from the euro area should help shape interest-rate cut expectations with traders close to fully pricing in a 25 basis point European Central Bank reduction in June. Swiss inflation will also garner some interest after the surprise rate cut by the Swiss National Bank last week.

The OPEC+ joint ministerial monitoring committee will meet on Wednesday although delegates see no need to recommend any changes to oil supply policy.

Here is a day by day analysis of key global events, courtesy of Bloomberg:

Monday, April 1

- China Caixin manufacturing PMI

- US ISM manufacturing and construction spending

- Fed’s Cook speaks

Tuesday, April 2

- RBA minutes

- German CPI

- ECB consumer expectations survey

- US factory orders and JOLTS

- Fed’s Bowman, Williams, Mester and Daly

- Chile central bank rate decision

Wednesday, April 3

- China Caixin service PMI

- Euro zone CPI and unemployment rate

- US ADP employment change and ISM services

- Fed’s Powell, Bowman, Barr, Goolsbee and Kugler

- OPEC+ JMMC meeting

Thursday, April 4

- Swiss CPI

- Euro zone PPI

- ECB minutes

- BOE decision maker panel survey

- US initial jobless claims and trade balance

- Fed’s Harker, Goolsbee, Barkin, Mester and Musalem

Friday, April 5

- German factory orders

- Euro zone retail sales

- US nonfarm payrolls, unemployment rate and average hourly earnings

- Canada employment change and unemployment rate

- Fed’s Bowman, Logan, Barkin and Kugler

* * *

Focusing just on the US, Goldman writes that the key economic data releases this week are the ISM manufacturing report on Monday, the JOLTS job openings report on Tuesday, the ISM services report on Wednesday, and the employment situation report on Friday. There are many speaking engagements from Fed officials this week, including a speech by Chair Powell on Wednesday.

Monday, April 1

- 09:45 AM S&P Global US manufacturing PMI, March final (Bloomberg consensus 52.5, last 52.5)

- 10:00 AM Construction spending, February (GS +1.1%, consensus +0.7%, last -0.2%)

- 10:00 AM ISM manufacturing index, March (GS 49.1, consensus 48.4, last 47.8): We estimate the ISM manufacturing index rebounded 1.3pt to 49.1 in March, reflecting the rebound in global manufacturing activity.

- 06:50 PM Fed Governor Cook speaks: Fed Governor Lisa Cook will give acceptance remarks at the Lifetime Achievement Awards Ceremony held by the Cook Center at Duke University in Washington, DC. Speech text will be made available. On March 25th, Cook said that “the risks to achieving our employment and inflation goals are moving into better balance. Nonetheless, fully restoring price stability may take a cautious approach to easing monetary policy over time.”

Tuesday, April 2

- 10:00 AM JOLTS job openings, February (GS 8,650k, consensus 8,775k, last 8,863k): We estimate that JOLTS job openings fell by 0.2mn to 8.65mn in February, reflecting the pullback in online job postings.

- 10:00 AM Factory orders, February (GS +0.7%, consensus +1.0%, last -3.6%); Durable goods orders, February final (consensus +1.4%, last +1.4%); Durable goods orders ex-transportation, February final (last +0.5%); Core capital goods orders, February final (last +0.7%); Core capital goods shipments, February final (last -0.4%)

- 10:10 AM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will speak on “Bank Mergers and Acquisitions, and De Novo Bank Formation: Implications for the Future of the Banking System” at a virtual event. Speech text will be made available. On February 27th, Bowman noted that, “should the incoming data continue to indicate that inflation is moving sustainably toward our 2 percent goal, it will eventually become appropriate to gradually lower our policy rate to prevent monetary policy from becoming overly restrictive. In my view, we are not yet at that point.”

- 12:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will moderate a discussion at the Economic Club of New York with Jeremy Siegel, professor of Finance at the Wharton School of the University of Pennsylvania. On February 28th, Williams said that “something like three [fed funds] rate cuts is a reasonable starting point” for 2024. President Williams also noted that “the risks to my forecast are two sided. Inflation may surprise to the upside, or consumer strength may fade more quickly than I anticipate.”

- 12:05 PM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester will give remarks on the economic outlook at the Cleveland Association for Business Economics and Team NEO Luncheon. A moderated Q&A is expected. On February 29th, Mester said that three rate cuts “feel about right to me if the economy evolves as I anticipate it will.”

- 01:30 PM San Francisco Fed President Daly (FOMC voter) speaks: San Francisco Fed President Mary Daly will participate in a Southern Nevada fireside chat, followed by a moderated Q&A. On February 29th, Daly said that “It would be appropriate as inflation comes down to bring the nominal rate of interest down to make sure we’re not holding on even tighter. We want to avoid holding on all the way to 2%, putting policy very tight and then cause an unnecessary downturn.”

- 05:00 PM Lightweight motor vehicle sales, March (GS 16.1mn, consensus 15.9mn, last 15.8mn)

Wednesday, April 3

- 08:15 AM ADP employment change, March (GS +120k, consensus +150k, last +140k): We estimate a 120k rise in ADP payroll employment in March, reflecting a solid underlying pace of job growth but a drag from residual seasonality: the ADP measure has slowed in March in each of the last three years and four of the last six.

- 09:45 AM S&P Global US services PMI, March final (consensus 51.7, last 51.7)

- 09:45 AM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will speak on Bank Liquidity, Regulation and the Fed’s Role as the Lender of Last Resort in Washington, DC. Speech text will be made available.

- 10:00 AM ISM services index, March (GS 53.6, consensus 52.8, last 52.6): We estimate that the ISM services index rose 1.0pt to 53.6 in March, reflecting solid growth and favorable seasonality. Our non-manufacturing survey tracker edged up 0.1pt to 52.1.

- 12:00 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will give opening remarks at the virtual event “Preventing Elder Financial Exploitation: Research, Policies and Strategies.” On March 25th, Goolsbee said that he expected three rate cuts this year and noted that “we are in this murky period where we have to strike a balance of the dual mandate.”

- 12:10 PM Fed Chair Powell speaks: Fed Chair Jerome Powell will give a speech on the economic outlook at the Stanford Business, Government, and Society Forum. Speech text and Q&A are expected. On March 29th, Powell said that that February PCE inflation data “were pretty much in-line with our expectations” and the committee is looking to see “more good inflation readings like the ones we were getting last year” to feel “confident that inflation is moving down to 2% on a sustained basis.” Powell also noted that he doesn’t think interest rates will go back down to the very low levels they were before the pandemic, but exactly where they will settle is “hard to say.”

- 01:10 PM Fed Vice Chair for Supervision Barr speaks: Fed Vice Chair for Supervision Michael Barr will speak about the Community Reinvestment Act in Washington, DC. A moderated Q&A is expected. On February 14th, Barr said that “my FOMC colleagues and I are confident we are on a path to 2% inflation, but we need to see continued good data before we can begin the process of reducing the federal funds rate.”

- 04:30 PM Fed Governor Kugler speaks: Fed Governor Adriana Kugler will speak on the “Outlook for the US Economy and Monetary Policy” in St. Louis. Speech text and Q&A are expected. On March 1st, Kugler said “I am cautiously optimistic that we will see continued progress on disinflation without significant deterioration of the labor market.”

Thursday, April 4

- 08:30 AM Trade balance, February (GS -$68.3bn, consensus -$67.0bn, last -$67.4bn)

- 08:30 AM Initial jobless claims, week ended March 30 (GS 205k, consensus 215k, last 210k): Continuing jobless claims, week ended March 23 (consensus 1,810k, last 1,819k)

- 10:00 AM Philadelphia Fed President Harker (FOMC non-voter) speaks: Philadelphia Fed President Patrick Harker will participate in a fireside chat about second chance employment. A Q&A is expected. On February 22nd, Harker said “I believe we may be in the position to see the rate decrease this year. But I would caution anyone from looking for it right now and right away. We have time to get this right, as we must.”

- 12:15 PM Richmond Fed President Barkin (FOMC voter) speaks: Richmond Fed President Thomas Barkin will deliver a speech on his economic outlook to the Home Building Association of Richmond. Speech text and Q&A are expected. On March 1st, Barkin said “I’m still hopeful inflation is going to come down and if inflation normalizes then it makes the case for why you want to normalize rates, but to me it starts with inflation.”

- 12:45 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will participate in a moderated Q&A at the Multi-Chamber Economic Outlook Luncheon and Expo.

- 02:00 PM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester will speak on the economic outlook in a virtual event. A Q&A is expected.

- 07:20 PM St. Louis Fed President Musalem (FOMC non-voter) speaks: St. Louis Fed President Alberto Musalem will give introductory remarks at the 2024 Women in Economics Symposium. This is Musalem’s first public appearance since he was named the president of the Federal Reserve Bank of St. Louis on January 4th 2024.

- 07:30 PM Fed Governor Kugler speaks: Fed Governor Adriana Kugler will speak on enriching data and analysis with real life experiences. Speech text will be made available.

Friday, April 5

- 08:30 AM Nonfarm payroll employment, March (GS +215k, consensus +200k, last +275k); Private payroll employment, March (GS +175k, consensus +165k, last +223k); Average hourly earnings (mom), March (GS +0.25%, consensus +0.3%, last +0.1%); Average hourly earnings (yoy), March (GS +4.04%, consensus +4.1%, last +4.3%); Unemployment rate, March (GS 3.8%, consensus 3.8%, last 3.9%); Labor force participation rate, March (GS 62.5%, consensus 62.5%, last 62.5%): We estimate nonfarm payrolls rose by 215k in March (mom sa), reflecting a continued boost from above-normal immigration as new entrants to the labor force are matched to open positions. Big Data measures also generally indicate a solid or strong pace of job gains, and our layoff tracker indicates that the pace of layoffs remains low. We nonetheless assume a slowdown from the February payroll gain of +275k because we believe a favorable swing in the weather boosted that report by as much as 75k. We estimate that the unemployment rate fell one tenth to 3.8%. Foreign-born unemployment increased by nearly 250k over the last three months, and we assume many of the new entrants found jobs during the March payroll month. We assume a flat-to-up labor force participation rate of 62.5%. We estimate average hourly earnings rose 0.25% (mom sa), which would lower the year-on-year rate by three tenths to 4.0%, reflecting waning wage pressures but a roughly 5bp boost from calendar effects (mom sa).

- 09:15 AM Richmond Fed President Barkin (FOMC voter) speaks: Richmond Fed President Thomas Barkin will deliver a speech on economic outlook. Speech text and Q&A are expected.

- 11:00 AM Dallas Fed President Logan (FOMC non-voter) speaks: Dallas Fed President Lorie Logan will speak at an event hosted by the Duke University Economics Department. Speech text and audience Q&A are expected. On March 1st, Logan said “slower [balance sheet] runoff is a way to approach the ample point more gradually, allowing banks to redistribute funds and the FOMC to carefully judge when we have gone far enough. This strategy will mitigate the risk of undesired liquidity stresses from QT.”

- 12:15 PM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will speak on the “Risks and Uncertainty in Monetary Policy: Current & Past Considerations” at the Shadow Open Market Committee spring meeting in New York. Speech text and Q&A are expected.

Source: BBG, Goldman

Tyler Durden

Mon, 04/01/2024 – 11:10

via ZeroHedge News https://ift.tt/iqYf5OK Tyler Durden