Beige Book Reveals Economy In Far Worse Shape Than White House Claims

There was something odd about the latest Beige book (which was prepared based on information collected on or before April 8, 2024, so before the latest CPI print): if accurate, it would suggest that the rosy economic picture painted by the White House is woefully incorrect, whether on purpose or not (spoiler alert: it is on purpose).

Reading the Beige Book, we find that contrary to the official GDP print which claims the economy is cruising at a brisk 3%, ten out of twelve Districts experienced “either slight or modest” economic growth, while the other two reported no changes in activity.

What is more concerning for the economy where spending amounts for 70% of all economic growth, the Beige Book found that consumer spending “barely increased” overall, but reports were quite mixed across Districts and spending categories:

- Several reports mentioned weakness in discretionary spending, as consumers’ price sensitivity remained elevated.

- Auto spending was buoyed notably in some Districts by improved inventories and dealer incentives, but sales remained sluggish in other Districts.

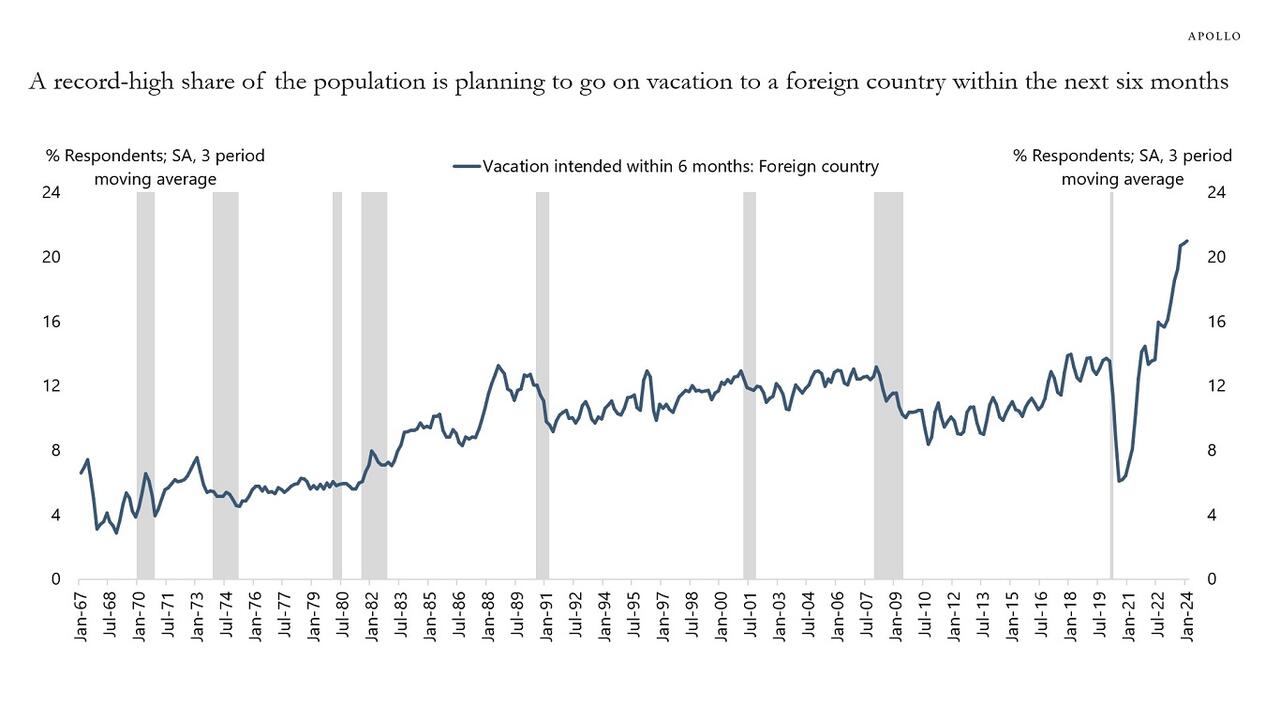

- Tourism activity increased modestly, on average, which is odd considering the recent Conference Board survey found a record number of people planned on traveling abroad. Almost as if they lied…

- Manufacturing activity declined slightly, as only three Districts reported growth in that sector.

- Contacts reported slight increases in nonfinancial services activity, on average, and bank lending was roughly flat overall.

- Residential construction increased a little, on average, and home sales strengthened in most Districts. In contrast, nonresidential construction was flat, and commercial real estate leasing fell slightly.

- The economic outlook among contacts was cautiously optimistic, on balance.

Next, we turn to employment, where contrary to the BLS claims that jobs are soaring month after month (even if they are all part-time workers, mostly going to illegal aliens), the Beige Book found that employment rose at a slight pace overall, with nine Districts reporting very slow to modest increases, and the remaining three Districts reporting no changes in employment.

Not surprisingly, most Districts noted increases in labor supply – which makes sense in a country where 10 million Biden voters illegals have entered in the past year. Yet despite the improvements in “labor supply”, many Districts described persistent shortages of qualified applicants for certain positions, including machinists, trades workers, and hospitality workers. Guess you can only have so many gardeners and construction workers. Several Districts reported improved retention of employees, and others pointed to staff reductions at some firms.

There’s more: contrary to the surging wages of the post-covid era, the Beige Book found that Multiple Districts said that annual wage growth rates had recently returned to their historical averages. On balance, contacts expected that labor demand and supply would remain relatively stable, with modest further job gains and continued moderation of wage growth back to pre-pandemic levels.

Last but not least, the Beige Book commented on inflation and found that price increases were modest, on average, running at about the same pace as in the last report, as disruptions in the Red Sea and the collapse of Baltimore’s Key Bridge caused some shipping delays but so far did not lead to widespread price increases. Movements in raw materials prices were mixed, but six Districts noted moderate increases in energy prices. Another widely known fact: several Districts reported sharp increases in insurance rates, for both businesses and homeowners.

Most ominously, another frequent comment was that firms’ ability to pass cost increases on to consumers had weakened considerably in recent months, resulting in smaller profit margins. That’s hardly the stuff soft- or no-landings are made of.

Inflation also caused strain at nonprofit entities, resulting in service reductions in some cases.

On balance, contacts expected that inflation would hold steady at a slow pace moving forward. At the same time, contacts in a few Districts—mostly manufacturers—perceived upside risks to near-term inflation in both input prices and output prices.

Turning to the specific regional Feds, we found these summaries notable:

- Boston: Business activity expanded at a modest pace in recent weeks, and prices rose slightly. Employment was flat overall, but one retailer reported significant layoffs. Convention and tourism activity grew at a robust pace. Home sales increased on a year-over-year basis, marking a turnaround. The outlook ranged from cautiously optimistic to bullish.

- New York: On balance, regional economic activity remained flat. Labor market conditions were solid and continued to normalize as labor supply and labor demand came into better balance. Consumer spending was unchanged after a weak first quarter. Housing markets strengthened, with the spring selling season picking up beyond the seasonal norm. The pace of selling price increases remained modest.

- Philadelphia: On balance, business activity was flat in the current Beige Book period—after declining slightly last period. Employment edged up, despite staffing and recruitment efforts slowing to a crawl. Wage and price inflation continue to moderate; however, housing affordability continues to be a concern. Overall, the outlook is positive, as firms remained optimistic about expectations for future growth.

- Cleveland: District business activity increased modestly, as did employment. Firms anticipated greater ease filling open positions, including those that have been particularly challenging, because of increased labor availability. Wage pressures continued to normalize, and some contacts reduced starting wages for new roles. Cost and price pressures changed little.

- Richmond: The regional economy grew at slight pace since our previous report. Consumer spending on retail goods was mixed but spending on travel and tourism was up slightly. Fifth District port activity slowed and was impacted by the collapse of the Francis Scott Key Bridge. Employment growth slowed from a moderate to a modest rate in recent weeks, but wages continued to grow moderately. Price growth also remained moderate.

- Atlanta: The Sixth District economy grew modestly. Labor markets continued to stabilize; wage pressures eased. Many nonlabor costs moderated. Retail sales were steady, but consumers remained price conscious. Tourism remained robust. Commercial real estate conditions slowed. Transportation activity was mixed. Manufacturing grew slightly. Loan demand was flat. Energy activity improved.

- Chicago: Economic activity increased slightly. Employment increased modestly; business and consumer spending rose slightly; nonbusiness contacts saw no change in activity; and manufacturing and construction and real estate activity were flat. Prices and wages rose moderately, while financial conditions were stable. Prospects for 2024 farm income were unchanged.

- St. Louis: Economic activity has continued to increase slightly since our previous report. Prices have increased modestly, as contacts are broadly feeling the pressures of increases in both labor and non-labor costs. The outlook was neutral to slightly optimistic, which is generally unchanged from our previous report, but better than one year ago.

- Minneapolis: District economic activity grew slightly. Employment grew some, but labor demand was softer. Wage pressures were present but continued to ease, while price pressures ticked up. Consumer spending was mostly flat, and manufacturing slowed modestly. Commercial and residential construction improved slightly. Agricultural conditions were steady at low levels.

- Kansas City: The District economy expanded modestly. Demand for auto loans and residential mortgages rose as borrowing rates declined. Demand for HELOC also increased as a means to consolidate or refinance household debt. Job gains were modest even as worker availability improved slightly.

- Dallas: The Eleventh District economy expanded modestly. While activity in services and housing grew, manufacturing output, retail sales, and loan demand declined slightly. Employment growth slowed as wages, input costs, and selling prices grew at a moderate pace. Overall, Texas firms noted an uptick in uncertainty.

- San Francisco: Economic activity continued to grow at a slight pace, employment levels were little changed, and prices and wages rose slightly. Retail sales were unchanged, and demand for services grew modestly. Demand for manufactured products changed little, and conditions in agriculture were mixed. Real estate activity was slightly down. Financial sector conditions were largely unchanged.

More in the full beige book

Tyler Durden

Wed, 04/17/2024 – 15:20

via ZeroHedge News https://ift.tt/IWbDtzi Tyler Durden