Is Buffett’s Cash Hoard A Market Warning?

Authored by Lance Roberts via RealInvestmentAdvice.com,

Every year, investors anxiously await the release of Warren Buffett’s annual letter to see what the “Oracle of Omaha” says about the markets, the economy, and where he is placing his money.

“One of the longest-running traditions in modern finance is that every year, one Saturday morning in late February, the world’s financial class – from professionals to mere amateurs – sit down as they have for the past 65 or so years – for an hour and read the latest Berkshire annual letter written by Warren Buffett. In that letter, the man seen by many as the world’s greatest investor, wrote down his reflections, observations, aphorisms and other thoughts which are closely parsed and analyzed for insight into what he may do next, what he thinks of the current economy and market climate, or simply for insights into how to become a better investor.” – Tyler Durden

This year’s letter was no different, with various tidbits about the current market and investing environment for investors to digest. The one thing that got most of my attention was his comments about the recent surge in cash holdings. Buffett’s cash and short-term investments (read T-bills) exceed $189 billion as of Q1, 2024.

To put that into context, that $189 billion cash pile alone would make Berkshire the 58th-largest economy in the world, only slightly smaller than Hungary.

There are two critical messages regarding Buffett’s cash hoard. The first is that due to the size of Berkshire Hathaway, which is approaching a $1 Trillion market capitalization, acquisitions have to be of substantial size. As Warren previously noted:

“There remain only a handful of companies in this country capable of truly moving the needle at Berkshire, and they have been endlessly picked over by us and by others. Some we can value; some we can’t. And, if we can, they have to be attractively priced.”

Such was an essential statement. One of the most intelligent investors in history suggests that deploying Buffett’s cash hoard in meaningful size is difficult due to an inability to find reasonably priced acquisition targets. With a $189 war chest, there are plenty of companies that Berkshire could either acquire outright, use a stock/cash offering, or acquire a controlling stake in. However, given the rampant increase in stock prices and valuations over the last decade, they are not reasonably priced.

In other words:

“Price is what you pay, value is what you get.” – Warren Buffett

The Valuation Dilemma

The problem with the valuation dilemma is that historically, such has preceded market repricings.

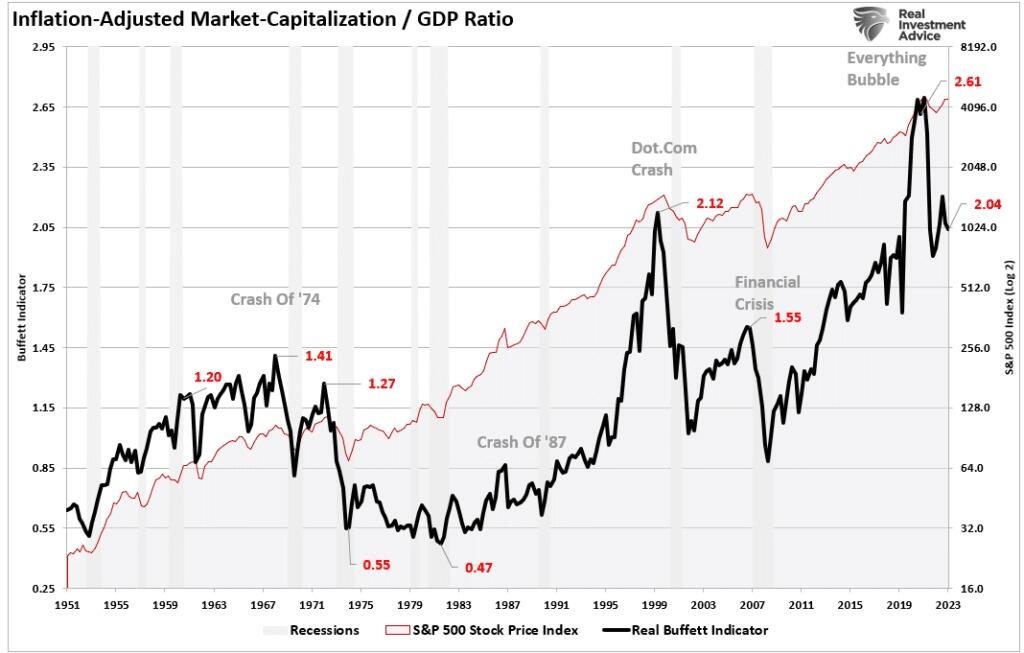

One of Warren Buffett’s favorite valuation measures is the market capitalization to GDP ratio. I have modified it slightly to use inflation-adjusted numbers. This measure is simple: stocks should not trade above the value of the economy. The reason is because economic activity provides revenues and earnings to businesses.

As discussed in “Stock Markets Are Detached From Everything,” the current environment is anything but opportunistic for a value investor like Warren Buffett. To wit:

“While stock prices can deviate from immediate activity, reversions to actual economic growth eventually occur. Such is because corporate earnings are a function of consumptive spending, corporate investments, imports, and exports. The market disconnect from underlying economic activity is due to psychology. Such is particularly the case over the last decade, as successive rounds of monetary interventions led investors to believe ‘this time is different.’”

There is a correlation between economic activity and the rise and fall of equity prices. For example, in 2000 and again in 2008, corporate earnings contracted by 54% and 88%, respectively, as economic growth declined. Such was despite calls for never-ending earnings growth before both previous contractions.

As earnings disappointed, stock prices adjusted by nearly 50% to realign valuations with weaker-than-expected current earnings and slower future earnings growth. So, while stock markets are once again detached from reality, looking at past earnings contractions suggests such deviations are not sustainable.

With the current market capitalization to GDP ratio data outside the historical range as economic growth slows, you can understand Berkshire’s dilemma of deploying cash.

The risk of overpaying for assets comes down to sustaining current profitability.

Berkshire’s issue of finding “reasonably priced” acquisitions is not just one of being overly picky about opportunities. After more than a decade of monetary infusions and zero interest rates, most companies are priced well beyond what economic dynamics can support.

The second message from Buffett’s cash hoard was more of a warning.

Buffett’s Cash Looking For A Crash?

“Occasionally, markets and/or the economy will cause stocks and bonds of some large and fundamentally sound businesses to be strikingly mispriced. Indeed, markets can – and will – unpredictably seize up or vanish as they did for four months in 1914 and a few days in 2001. If you believe American investors are now more stable than in the past, think back to September 2008. Speed of communication and the wonders of technology facilitates instant worldwide paralysis, and we have come a long way since smoke signals. Such instant panics won’t happen often – but they will happen.

Berkshire’s ability to immediately respond to market seizures with both huge sums and certainty of performance may offer us an occasional large-scale opportunity. Though the stock market is massively larger than it was in our early years, today’s active participants are neither more emotionally stable nor better taught than when I was in school. For whatever reasons, markets now exhibit far more casino-like behavior than when I was young. The casino now resides in many homes and daily tempts the occupants.

One investment rule at Berkshire has not and will not change: Never risk permanent loss of capital. Thanks to the American tailwind and the power of compound interest, the arena in which we operate has been – and will be – rewarding if you make a couple of good decisions during a lifetime and avoid serious mistakes.” – Warren Buffett

In other words, he holds such high cash levels to take advantage of market dislocations. Such is what happened in 2008 when the prestigious “white shoe” investment firm of Goldman Sachs came begging with “hat in hand” for a bailout to avoid bankruptcy. Buffett was glad to oblige by providing a massive infusion of capital at lucrative terms. During a crisis, those who “have the gold make the rules.”

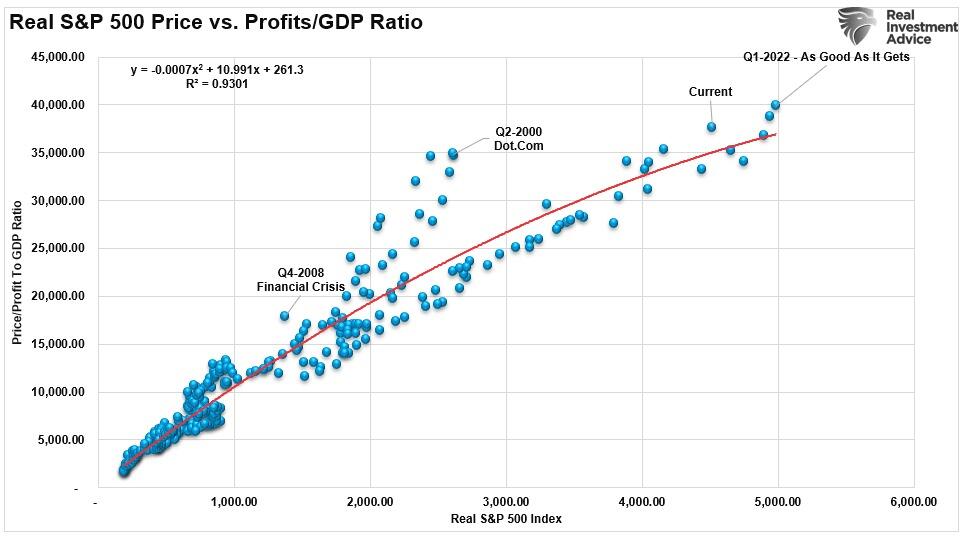

Is there such an opportunity coming in the future? The answer is most likely yes. If we examine corporate profits as they relate to economic growth, we find another measure of excess. The chart below measures the cumulative change in the S&P 500 index compared to corporate profits. Again, when investors pay more than $1 for $1 worth of profits, those excesses are eventually reversed. The current deviation of the market from underlying profitability suggests that eventual reversion will be pretty unkind to investors.

The correlation is more evident in the market versus the price-to-corporate profits ratio. Again, since corporate profits are ultimately a function of economic growth, the correlation is not unexpected. Hence, neither should the impending reversion in both series. Currently, that ratio is approaching levels that preceded more significant market reversions to realign the markets to profitability.

As noted, the high correlation is unsurprising. Investors should expect an eventual reversal with the market on the more extreme end of the valuation spectrum. However, those reversals can take much longer to occur than logic would assume.

Investors believe the deviation between fundamentals and fantasy doesn’t matter as long as the Fed supports asset prices. Such a point remains challenging to argue.

However, as is always the case, the reversion of excesses will occur. Buffett’s cash hoard suggests that he realizes that such a reversion is not unprecedented. More importantly, he wants to capitalize on it when it occurs.

Tyler Durden

Fri, 05/17/2024 – 10:20

via ZeroHedge News https://ift.tt/ctraBbJ Tyler Durden