Yellen Pivot Is Fading: Liquidity Drains From The System As Treasury Issues Fewer Bills

By Simon White, Bloomberg Markets Live reporter and strategist

Risk assets will face a less-easy ride as Treasury bill issuance falls and coupon (notes and bonds) issuance rises, weighing on central-bank reserves.

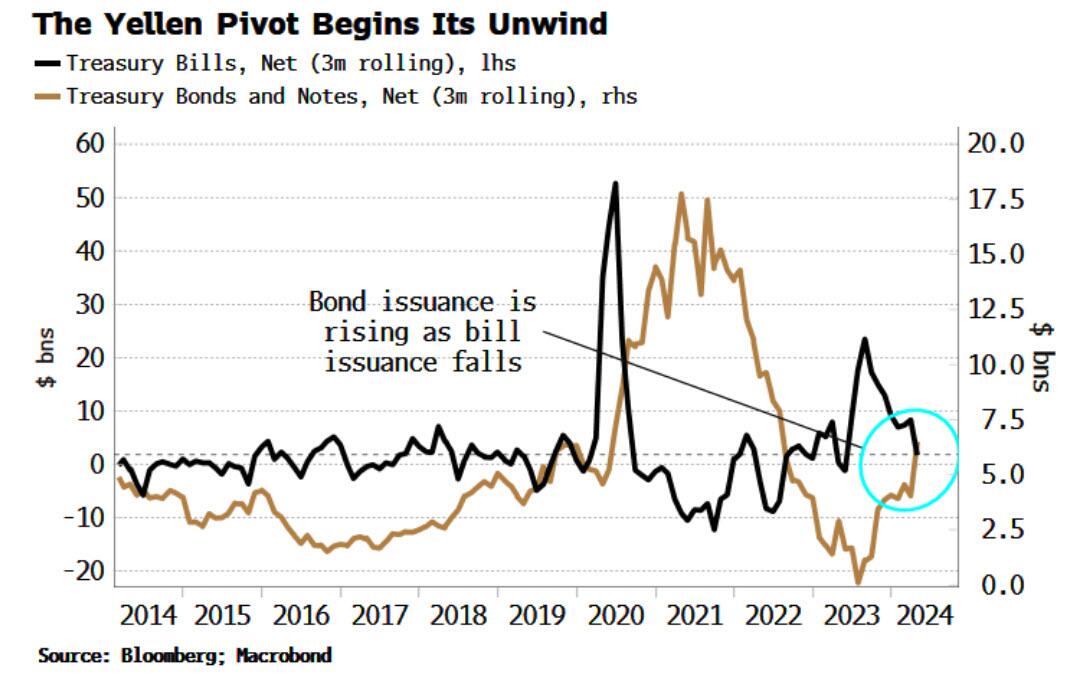

Nothing lasts forever. The Treasury tilted issuance towards bills last year – the Yellen pivot – which allowed the market to continue to rally despite the inundation of government debt. After reaching 23% in March, the bills proportion of total debt fell back to 22.2% in April, the biggest monthly drop since March 2023. The Yellen pivot is fading.

But the largest peacetime fiscal deficit still needs funding. That means good old-fashioned bond issuance is starting to take up the slack as bill issuance falls back.

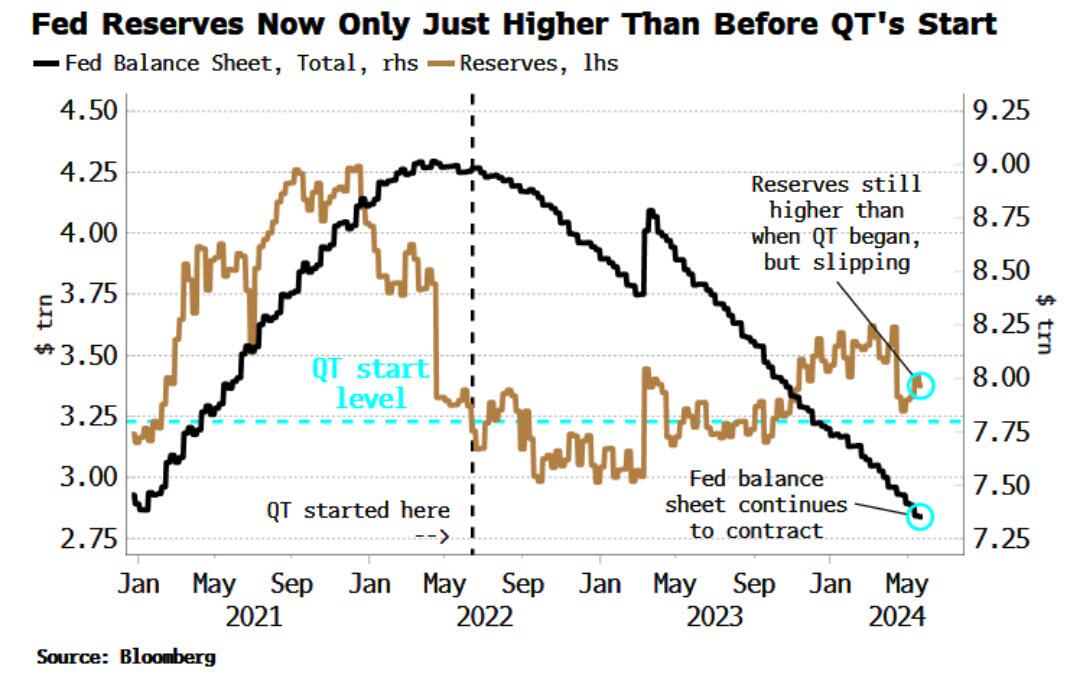

Reserves have started to decline again, draining liquidity from the system. Quantitative tightening may have been in operation for almost two years, and the Federal Reserve’s balance sheet falling since then, but reserves have spent most of the intervening period higher than they were since QT began.

This has undoubtedly given risk assets an easier time than if reserves had fallen at the same rate as the balance sheet. By issuing more bills, the Treasury enabled money market funds to fund most of the deficit using otherwise inert liquidity parked at the reverse repo facility.

But MMFs are not able to directly buy longer-term debt (i.e. notes and bonds), and unless the buyers are banks (who have been largely reducing their exposure to USTs), bank deposits and therefore reserves will be used to facilitate the purchase. On net, some of these reserves will end up being depleted through QT – although at a slower pace from June as the Fed reduces the monthly cap on the run-off rate for USTs from $60 billion to $25 billion.

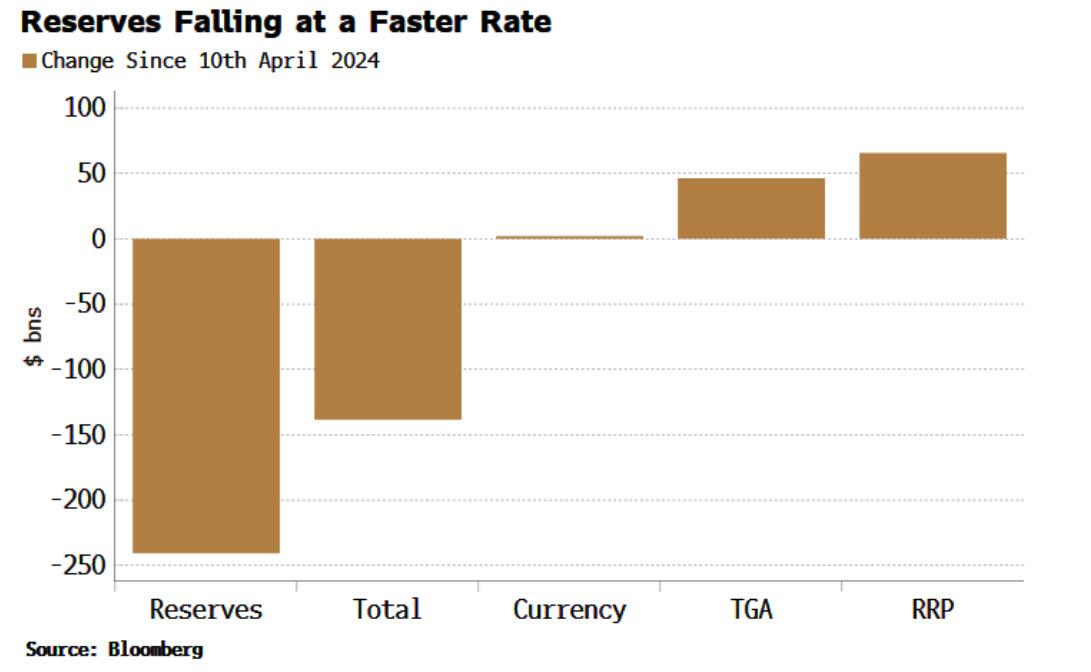

Reserves have fallen almost $250 billion since April. Almost $100 billion of that is due to a rise in RRP and the Treasury’s account at the Fed (the TGA). When neither of these two is falling, and the Fed proceeds with QT, reserves must fall.

This will be an increasing absence of a tailwind for risk assets which will eventually become a headwind. Regional banks are among those who may face a particular challenge from declining liquidity, making another bank failure a distinct possibility. It’s when those sort of choppy waters hit the Fed will probably see fit to curtail QT altogether.

Tyler Durden

Thu, 05/30/2024 – 14:05

via ZeroHedge News https://ift.tt/ra9uAv2 Tyler Durden