“Never Intended To Offend” – Pope Apologizes After Homophobic Slur Leak

Pope Francis has issued an apology this morning after reports surfaced that he used a homophobic slur during a private meeting.

He reportedly used the Italian term “frociaggine,” which translates to “faggotry” or “faggotness” in English.

Citing sources from inside the meeting, the Corriere della Sera and La Repubblica newspapers reported Monday that the Pope had made the comments while meeting with Italian bishops on May 20.

The remarks took place in the context of proposals from the Italian bishops to amend guidelines on candidates to seminaries.

As CNN reports, The Vatican ruled in 2005 that the church cannot allow the ordination of men who are actively gay or have “deep-seated” homosexual tendencies.

In 2016, Francis upheld this ruling.

Responding to journalists’ questions, the Director of the Holy See Press Office, Matteo Bruni, said the following:

Pope Francis is aware of the articles that came out recently about a conversation, behind closed doors, with the bishops of the CEI (Italian Episcopal Conference).

As he has said on several occasions:

“In the Church there is room for everyone, for everyone! No one is useless, no one is superfluous, there is room for everyone. Just as we are, everyone”.

“The Pope never intended to offend or express himself in homophobic terms, and he extends his apologies to those who felt offended by the use of a term, reported by others.”

We are sure all the progressives will now stop screaming and accept the Pope’s apology… and He will forgive Him.

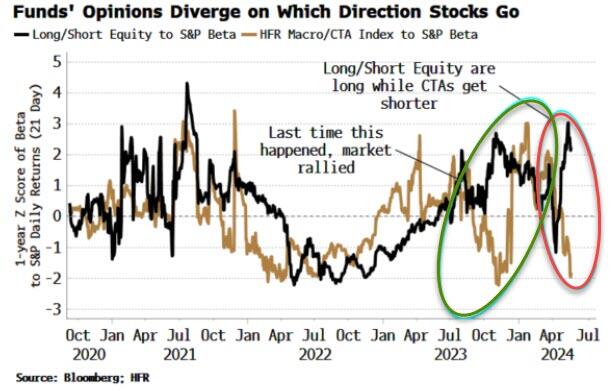

Authored by Simon White, Bloomberg macro strategist,

CTAs are getting shorter the stock market while long/short equity funds have been getting longer.

The last time this happened, in November, long/short funds were positioned correctly, with the market rallying over the next five months.

CTAs, or managed futures strategies, typically use trend-following systems to go long or short a variety of equity, bond and commodity futures. Using the S&P 500 as a proxy for overall risk, CTAs (based on, for example, HFR’s index of CTA funds or the DBi Managed Futures ETF) have become more negatively sensitive to the index.

That means they should lose money if the S&P continues to rally (if they stay similarly positioned).

Long/short equity funds buy and sell stocks they perceive as under or overvalued. Their returns have been enhanced in the higher-rates environment, given their shorts typically fund most of their longs, thus they can invest the remaining cash in T-Bills.

Long/short funds’ sensitivity to the S&P is becoming more positive. As the chart below shows, the two fund styles are generally in agreement in which direction they expect stocks to go.

The last time there was such a divergence in views was November, when the market rallied strongly – with CTAs likely boosting the rise – covering their shorts and soon becoming long.

The data indicates that long/short funds will be vindicated again.

The ingredients for a deep correction are not there at the moment.

Overall, near-term recession risk remains low, removing – again, for now – one of the biggest dangers for stocks. However, some soft data has deteriorated enough, while the hard data is still sufficiently fragile, meaning the risk of a recession could rise very quickly, i.e. more nimbleness in positioning is probably best.

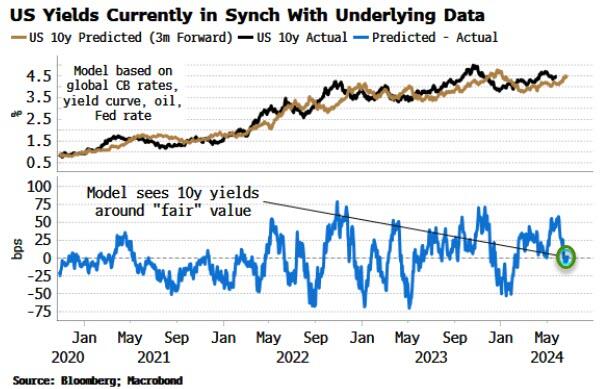

Yields look around fair value, so there are no immediate and obvious ex ante catalysts why stocks should be knocked back by a bond selloff.

Excess liquidity remains supportive for the equities.

It’s conceivable the market keeps grinding higher in the coming weeks, squeezing any CTAs who may be outright short equities (or other assets negatively correlated to the stocks).

Conference Board Consumer Confidence Rebounds In May… As Inflation Expectations Hit 2024 Highs

After dropped near the lowest level in eleven years last month, the Conference Board Consumer Confidence expectations index soared in May from 68.8 (upwardly revised from 66.4) to 74.6. The Present Situation rose from 140.6 (revised down from 142.9) to 143.1.

The best expectations print since Feb dragged the headline index up notably to 102.0 (well above the 96.0 exp)…

Source: Bloomberg

The overall trend in labor market indicators remains weaker…

Source: Bloomberg

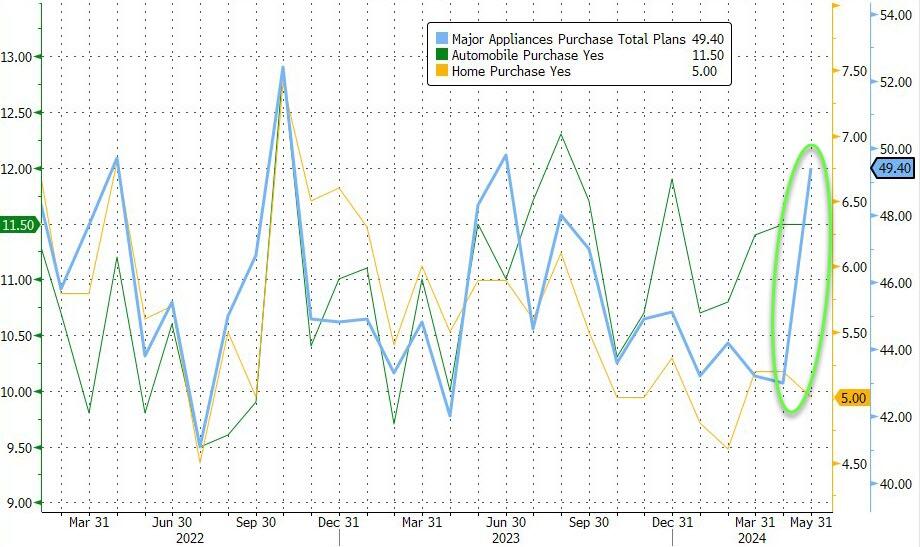

Plans to buy a home fell, plans to buy a car were flat, but plans to buy large household appliances soared…

Source: Bloomberg

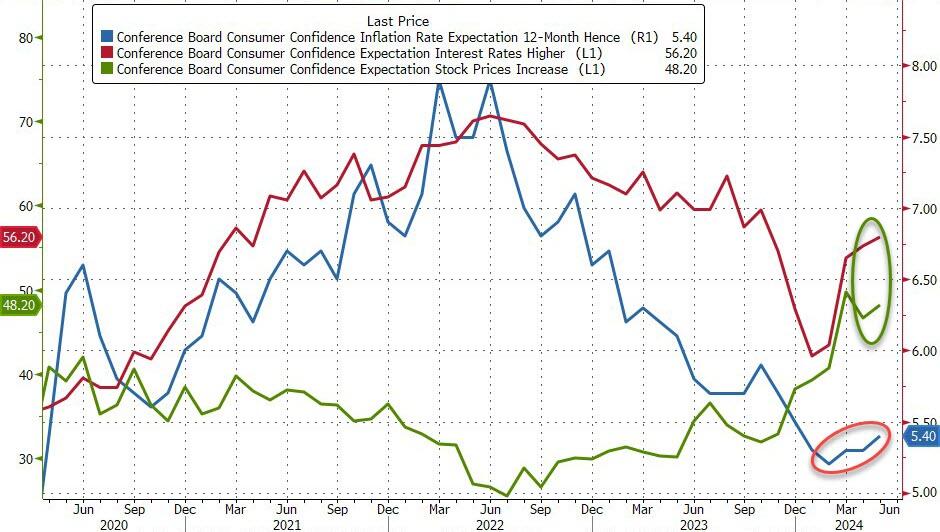

Conference Board Inflation Expectations (for one year ahead) rose to 5.4% – the highest since Dec 2023…

Source: Bloomberg

Expectations for rates to be higher and stocks to be higher both increased.

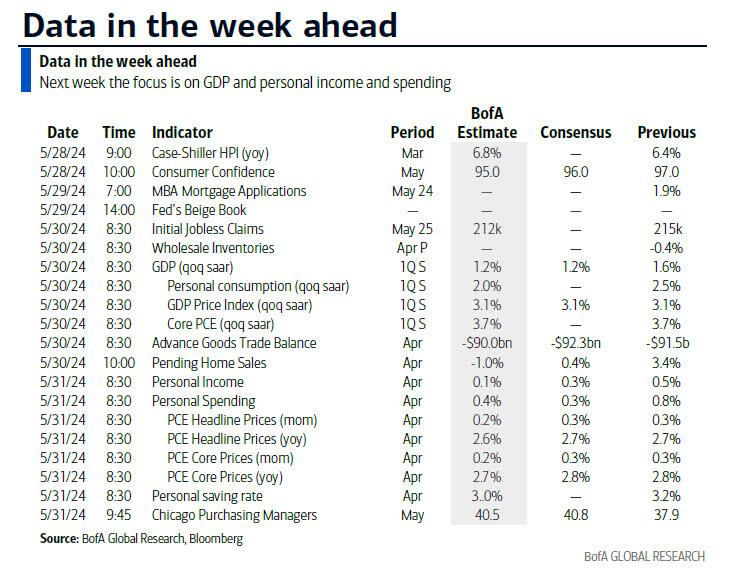

Key Events This Holiday-Shortened Week: PCE, GDP And More Fed Speakers

All roads this week point towards the April US core PCE print on Friday which in MoM terms is expected to edge down from +0.32% to +0.26%, which would be the lowest monthly increase of 2024. As DB’s Jim Reid notes, you don’t need an economist to tell you how well scrutinized this data will be and how important it is to the Fed. As part of the same release, personal income (+0.4% forecast vs. +0.5% previously) and consumption (+0.2% vs. +0.8%) will likely come in a little softer.

Back to inflation, and the preliminary May CPIs are out in Germany tomorrow, and in France, Italy and the Eurozone on Friday. DB’s European economists see this coming in at + 2.55% (+2.4% in April) for headline and +2.84% (+2.66% April) for core inflation. At the start of 2024, euro area inflation avoided the sizeable upside surprises we saw in the US, but the last print in April did see core inflation slightly stronger than expected. It would be a tall order for the data to derail the strongly signaled ECB cut next week but it could have important implications for the ECB’s signal beyond this. We will also have the latest inflation expectations from the ECB consumer expectations survey for April today. A DB survey suggests that median medium-term expectations are likely to stay stable at 2.5%. Finally on inflation, Tokyo CPI is also out on Friday.

Elsewhere, in the US we have consumer confidence today, the Fed Beige Book tomorrow, the second reading of GDP and the Trade Balance on Thursday with the Chicago PMI alongside the personal spending and income report (alongside core PCE) on Friday. In China, May’s PMIs on Friday will be the highlight. You can see the full day-by-day week ahead at the end including all the main central bank speakers highlighted too.

In what is a busy busy year for elections, this week we have the South African election tomorrow, the last leg of the Indian elections on Saturday and the Mexican equivalent on Sunday. Note it’s also less than two weeks until the European Parliamentary elections.

Courtesy of DB, here is a day-by-day calendar of events

Tuesday May 28

Data : US Q1 house price purchase index, March FHFA house price index, May Conference Board consumer confidence index, Dallas Fed manufacturing activity, Japan April PPI services, Germany April wholesale price index, Canada April industrial product price index, raw materials price index

Central banks : Fed’s Mester, Cook and Kashkari speak, ECB’s consumer expectations survey, ECB’s Knot and Schnabel speak, BoE’s Haskel speaks

Earnings : Cava

Auctions : US 2-yr Notes ($69bn), 5yr Notes ($70bn)

Wednesday May 29

Data : US May Richmond Fed manufacturing index and business conditions, Dallas Fed services activity, Japan May consumer confidence index, Germany June GfK consumer confidence, May CPI, France May consumer confidence, Italy May consumer confidence index, manufacturing confidence, economic sentiment, Eurozone April M3

Central banks : Fed’s Beige Book, Williams speaks, BoJ’s Adachi speaks, ECB’s Villeroy speaks

Earnings : Salesforce, Telecom Italia

Auctions : US 2-yr FRNs (reopening, $28bn), 7-yr Notes ($44bn)

Thursday May 30

Data : US April advance goods trade balance, wholesale inventories, retail inventories, pending home sales, initial jobless claims, Italy April unemployment rate, PPI, Eurozone May services, industrial, economic confidence, April unemployment rate, Canada Q1 current account balance, Sweden and Switzerland Q1 GDP

Central banks : Fed’s Williams, Bostic and Logan speak, BoE’s Breeden speaks

Earnings : Dell, Marvell, Dollar General, Costco

Friday May 31

Data : US April personal income and spending, PCE, May MNI Chicago PMI, China May PMIs, UK May Lloyds Business Barometer, April net consumer credit, M4, Japan April jobless rate, job-to-applicant ratio, industrial production, retail sales, housing starts, May Tokyo CPI, Germany April retail sales, import price index, France Q1 total payrolls, April consumer spending, PPI, May CPI, Italy May CPI, March industrial sales, Eurozone May CPI, Canada Q1 GDP

Central banks : Fed’s Bostic speaks, ECB’s Vujcic speaks

Finally, looking at just the US, Goldman writes that the key economic data releases this week are Q1 GDP revision on Thursday and the core PCE report on Friday. There are several speaking engagements from Fed officials this week, including remarks from Governors Bowman and Cook, and Presidents Mester, Kashkari, Williams, Bostic, and Logan.

Tuesday, May 28

12:55 AM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester will speak at an event hosted by the Bank of Japan in Tokyo about the effects of conventional and unconventional policy instruments. Speech text is expected. On May 16, Mester said “monetary policy is well positioned for risk management as we gather more evidence on how the economy is evolving” and that she “expected progress on inflation over time, but at a slower pace than we saw last year.”

12:55 AM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will speak at a closed event at the Bank of Japan. Speech text is expected. On May 17, Bowman said “at its current setting, our monetary policy stance spears to be restrictive… my baseline outlook continues to be that inflation will decline further with the policy rate held steady, but I still see a number of upside inflation risks that affect my outlook.”

09:00 AM FHFA house price index, March (consensus +0.5%, last +1.2%)

09:00 AM S&P Case-Shiller 20-city home price index, March (GS +0.5%, consensus +0.30%, last +0.61%)

09:55 AM Minneapolis Fed President Kashkari (FOMC non-voter) speaks: Minneapolis Fed President Neel Kashkari will give a speaker address followed by panel remarks at the Barclays-CEPR International Monetary Policy Forum in London. A Q&A is expected. On May 15, Kashkari said “we probably need to sit here for a while longer until we figure out where underlying inflation is headed before we jump to any conclusions.”

10:00 AM Conference Board consumer confidence, May (GS 96.4, consensus 96.0, last 97.0)

01:05 PM Fed Governor Cook speaks: Fed Governor Lisa Cook will speak on AI and the economy at the San Francisco Fed. A Q&A is expected. On March 25, Cook said “The path of disinflation, as expected, has been bumpy and uneven, but a careful approach to further policy adjustments can ensure that inflation will return sustainably to 2% while striving to maintain the strong labor market.”

Wednesday, May 29

01:45 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will join the Watertown Community Services Roundtable in Watertown, NY. On May 16, Williams said “I don’t see any indicators now telling me … there’s a reason to change the stance of monetary policy now, and I don’t expect to get that greater confidence that we need to see on the inflation progress towards a 2% goal in the very near term.”

02:00 PM Beige Book, June Meeting period: The Fed’s Beige Book is a summary of regional economic anecdotes from the 12 Federal Reserve districts. The Beige Book for the April/May FOMC meeting period noted that activity expanded slightly in early 2024 and that firms’ economic outlook for the remainder of the year was cautiously optimistic. Businesses reported weakness in discretionary spending due to heightened price sensitivity among consumers. Manufacturing activity declined slightly while residential construction increased slightly and home sales strengthened across most Districts. In this month’s Beige Book, we look for anecdotes related to possible turning points in regional labor markets and for further commentary on businesses’ inflation expectations over the next few months.

07:00 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will speak in a moderated conversation on the economic outlook and leadership. A Q&A is expected. On May 23, Bostic said that cutting rates too soon “could spur a sort of resurgence, if you will, of economic activity that might be counterproductive to what we’re trying to accomplish. I have really taken that on board… and it might be that we have to be a little more patient and be more certain that inflation is on its way” to the 2 percent target.

Thursday, May 30

08:30 AM GDP, Q1 second release (GS +1.1%, consensus +1.3%, last +1.6%); Personal consumption, Q1 second release (GS +2.0%, consensus +2.2%, last +2.5%): We estimate a 0.5pp downward revision to Q1 GDP growth to +1.1% (qoq ar), reflecting downward revisions to personal consumption (-0.5pp to +2.0%) and inventory investment, the former reflecting net negative retail sales revisions as well as softer recreation details in the quarterly census survey (QSS).

08:30 AM Initial jobless claims, week ended May 25 (GS 215k, consensus 218k, last 215k): Continuing jobless claims, week ended May 18 (consensus 1,795k, last 1,794k)

08:30 AM Advance goods trade balance, April (GS -$94.0bn, consensus -$92.0bn, last -$91.8bn)

10:00 AM Wholesale inventories, April preliminary (consensus flat, last -0.4%)

10:00 AM Pending home sales, April (GS -0.6%, consensus +0.1%, last +3.4%)

12:05 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will speak at the Economic Club of New York. Speech text and a Q&A are expected.

05:00 PM Dallas Fed President Logan (FOMC non-voter) speaks: Dallas Fed President Lorie Logan will speak at an event hosted by the Borderplex Alliance in El Paso, TX. A Q&A is expected. On April 5, Logan said “to be clear, the key risk is not that inflation might rise – though monetary policymakers must always remain on guard against that outcome – but rather that inflation will stall out and fail to follow the forecast path all the way back to 2 percent in a timely way.”

Friday, May 31

08:30 AM Personal income, April (GS +0.2%, consensus +0.3%, last +0.5%); Personal consumption, April (GS +0.25%, consensus +0.3%, last +0.8%); PCE price index, April (GS +0.27%, consensus +0.3%, last +0.3%); PCE price index (yoy), April (GS +2.68%, consensus +2.7%, last +2.7%); Core PCE price index, April (GS +0.26%, consensus +0.2%, last +0.3%); Core PCE price index (yoy), April (GS +2.77%, consensus +2.8%, last +2.8%): We estimate personal income increased 0.2% and personal spending increased 0.25% in April. We estimate that the core PCE price index rose +0.26%, corresponding to a year-over-year rate of 2.77%. Additionally, we expect that the headline PCE price index increased by 0.27% from the prior month, corresponding to a year-over-year rate of 2.68%. Our forecast is consistent with a 0.22% increase in our trimmed core PCE measure (vs. +0.24% in March and +0.24% in February).

09:45 AM Chicago PMI, May (GS 41.9, consensus 40.9, last 37.9): We estimate that the Chicago PMI rose by 4pt to 41.9 in May, reflecting the rebound in US and foreign manufacturing activity.

06:15 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will give the commencement speech to Augusta Technical College. Speech text is expected.

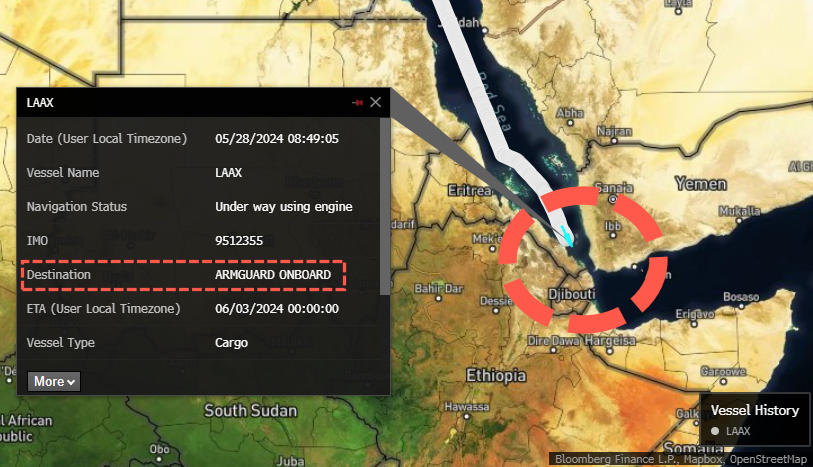

Greek-Owned Bulk Carrier Taking On Water After Missile Strike In Red Sea

According to Bloomberg, citing maritime security firm Ambrey and a US defense official, a bulk carrier flying under the Marshall Islands flag was attacked in the southern Red Sea on Tuesday. This incident occurred as Israeli forces advanced further into the south of Gazan city of Rafah. The culprits behind the maritime incident were likely Yemen’s Iran-backed Houthis.

The 750-foot-long Greek-owned vessel is currently taking on water and leaning to one side. The ship was targeted about 54 miles southwest of the Yemeni city of Hodeida, according to Ambrey. It was hit with three missiles. There were 80,000 tons of cargo on board, yet no information was given on what the ship was hauling.

Vessel-tracking data compiled by Bloomberg shows that Laax was approaching the Bab al-Mandab Strait during the attack. The ship is currently broadcasting “ARMGUARD ONBOARD” as its destination, possibly in an apparent attempt to prevent boarding.

Bloomberg noted, “Yemen’s Houthis have not been named as the attackers but the group has carried out a series of assaults on ships transiting the waterway which is crucial to international shipping over the past few months in retaliation for Israel’s war in Gaza.”

Continuing attacks in the Red Sea are not entirely unexpected, as the Houthis often retaliate against IDF offensives in Gaza. The latest fighting in Rafah will likely trigger more attacks in the Red Sea and other critical maritime chokepoints across the Middle East.

Furthermore, the ongoing attacks on critical maritime chokepoints represent a colossal failure by the Biden administration’s Operation Prosperity Guardian. The administration is weak because it’s an election year, and it doesn’t want to push Brent crude prices above $90/bbl.

Ukraine Confirms France Will Send Military Trainers To Its Soil

Ukraine’s military says it is ‘welcoming’ French trainers in Ukraine, in new remarks which strongly suggest that for the first time France is deploying its troops to Ukraine soil. This marks the beginning of major ‘boots on the ground’ escalation in a formal, public capacity by a NATO state.

“Ukraine’s top commander said on Monday he had signed paperwork allowing French military instructors to visit Ukrainian training centers soon,” Reuters reported Monday, referencing head of the armed forces Col. Gen. Oleksandr Syrskyi.

“I am pleased to welcome France’s initiative to send instructors to Ukraine to train Ukrainian servicemen,” Syrskyi said following video link talks with French defense minister Sebastien Lecornu.

“I have already signed the documents that will enable the first French instructors to visit our training centers shortly and familiarize themselves with their infrastructure and personnel,” he followed with, strongly suggesting the plan is a done deal but may not have been initiated yet.

Syrskyi suggested that France’s commitment and being out front on the “ambitious project” to train Ukrainian forces inside the country would encourage other allies to join the initiative. This follows French President Emmanuel Macron raising the idea repeatedly over the last months of placing Western boots on the ground in Ukraine. He said nothing should be ruled out.

France’s Defence Ministry said told Reuters, “As already mentioned several times, training on Ukrainian soil is one of the projects discussed since the conference on support for Ukraine convened by the President of the Republic on February 26.” This is in reference to the date on which Macron first voiced support for such a plan before a Paris security conference involving defense representatives from around the world.

“Like all the projects discussed at that time, this track continues to be the subject of work with the Ukrainians, in particular to understand their exact needs,” the ministry added.

Macron has been in Berlin this week, which marks the first time a French president has traveled to Germany for talks with the country’s Chancellor since 2000.

A focal point of the talks with German Chancellor Olaf Scholz is said to be Ukraine, and seeking to convince Scholz to join France in a more muscular Ukraine policy. However, this has remained a point of division:

Officials from both sides stressed that while there are periodic tensions on specific issues, the fundamental basis of the relationship remains sound.

But Macron’s refusal to rule out sending troops to Ukraine sparked an unusually acidic response from Scholz that Germany had no such plans. Germany also does not share Macron’s enthusiasm for a European strategic autonomy less dependent on the United States.

President Putin and his top officials have meanwhile repeatedly warned that if the West sends its troops to Ukraine, this risks sparking nuclear war. Already the Kremlin has said it has targeted groups of French mercenaries in the Kharkiv area.

Masterful takedown by Dominique de Villepin, former French Prime Minister, of Macron’s utterly irresponsible rhetoric on sending NATO ground troops to Ukraine (Villepin himself calls it irresponsible).

Starting in February Putin warned that the Western allies were “selecting targets for striking our territory” and “talking about the possibility of sending a NATO contingent to Ukraine.” With Kiev now openly welcoming French military trainers, this serious escalation is already in process.

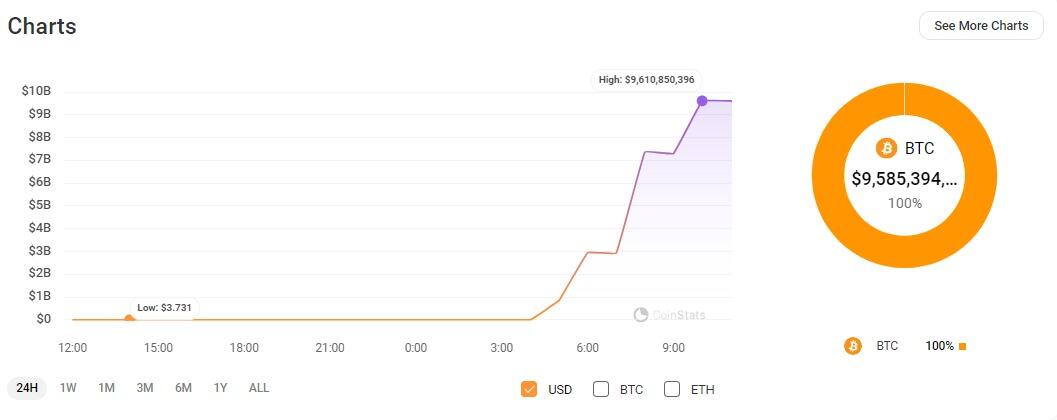

These transfers are seen as a potential indication that users who have been unable to access their funds since 2014, when Mt. Gox suspended trading and withdrawals, might finally be repaid.

The transfers represent the first on-chain movement of funds from the exchange in over five years and seem in line with Mt. Gox’s plans to repay creditors by the end of October 2024.

Mt. Gox wallet ‘”1Jbez” Source: CoinStats

The near $10 billion Bitcoin consolidation likely points to Mt. Gox’s plans to repay its users, according to Anndy Lian, intergovernmental blockchain expert and author of NFT: From Zero to Hero. Lian told Cointelegraph:

“This is the first movement of assets from Mt. Gox’s cold wallets in over five years and is likely part of the plan to distribute the assets back to creditors before the promised deadline of Oct. 31, 2024, in my humble opinion.”

Shortly after the reports, Mt. Gox rehabilitation trustee Nobuaki Kobayashi has confirmed that the consolidation is part of the exchange’s plans to start repaying creditors, without mentioning when the repayments will start to occur. Kobayashi wrote in a May 28 announcement:

“The Rehabilitation Trustee is preparing to make repayment for the portion of cryptocurrency rehabilitation claims to which cryptocurrency is allocated… As the Rehabilitation Trustee is proceeding with the preparation for the above repayments, please wait for a while until the repayments are made.

However, the current deadline could face further delays, as it was set in September 2023 — a month before Mt. Gox was initially scheduled to repay the exchange’s creditors by Oct. 31, 2023.

Over $9.4 billion worth of Bitcoin is owed to some of Mt. Gox’s 127,000 creditors who have waited to get it back for over 10 years after the exchange collapsed in 2014 after multiple unnoticed hacks.

Mt. Gox was one of the earliest cryptocurrency exchanges, once facilitating more than 70% of all trades made within the blockchain ecosystem.

Following a major hack in 2011, the site collapsed in 2014; the fallout affected about 24,000 creditors and resulted in the loss of 850,000 BTC.

Markets are pricing in a Mt. Gox repayment

Following the first batch of Mt. Gox transfers, Bitcoin price dipped 2% on May 28, to a daily low below $67,500, before recovering to just above $68,500, according to CoinMarketCap.

Source: Bloomberg

The BTC dip could be a sign of markets pricing in a potential repayment by Mt. Gox, according to Lian:

“The market has reacted to these movements with a slight bearish sentiment, as Bitcoin’s price dropped around 2.1% to as low as $67,505 after the transfer. This could be due to expectations of selling pressure from the creditors once they receive their repayments.”

Despite the slight price dip, Lian said that a potential repayment would resolve one of the most pressing, long-standing issues of the crypto industry.

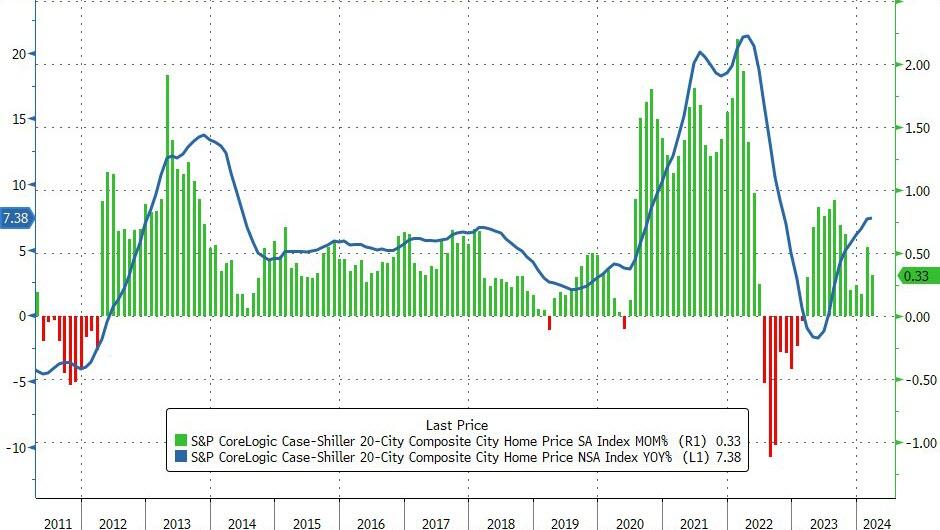

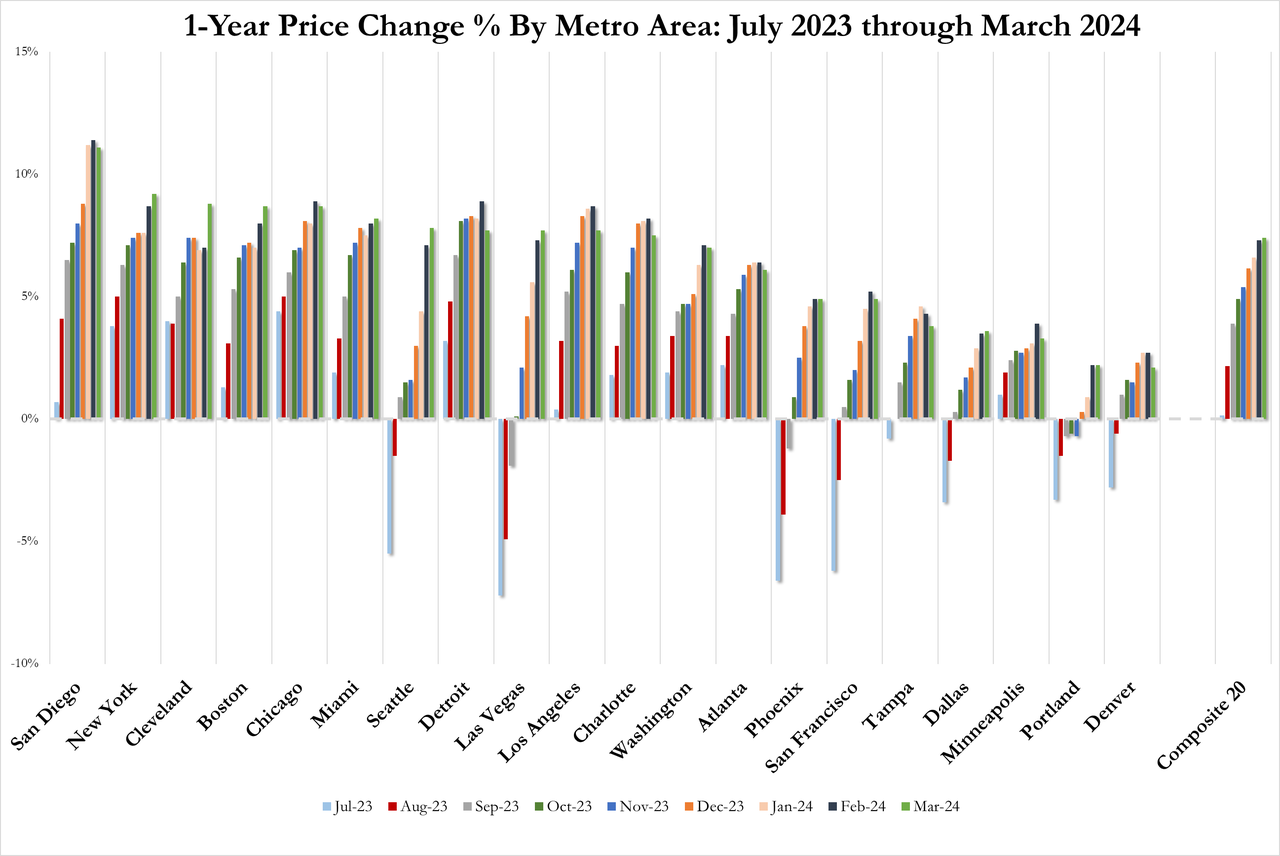

US Home Prices Reached New Record High In March, Despite Soaring Rates

Home prices in America’s 20 largest cities rose for the 13th straight month in March (according to the latest data from S&P CoreLogic – Case Shiller – data today), up 0.33% (more than the expected 0.3%) with the 0.61% MoM gain In Febriary revised down to +0.55% MoM.

Source: Bloomberg

This pushed the price up 7.38% YoY – the fastest rise since October 2022…

“We’ve witnessed records repeatedly break in both stock and housing markets over the past year. Our National Index has reached new highs in six of the last 12 months.” says Brian D. Luke, Head of Commodities, Real & Digital Assets at S&P Dow Jones Indices.

Overall, US home prices reached a new record high in March (as median new home prices began to fall)…

Source: Bloomberg

San Diego continued to report the highest year-over-year gain among the 20 cities this month with an 11.1% increase in March, followed by New York and Cleveland, with increases of 9.2% and 8.8%, respectively.

Portland, which still holds the lowest rank after reporting three consecutive months of the smallest year-over-year growth, posted the same 2.2% annual increase in March as the previous month.

Luke suggested this implies “a strong demand for urban markets.”

No city has seen a MoM decline in price in 2024.

Home prices continue to track Fed Reserves closely, but a turning point may come soon…

Source: Bloomberg

Given the smoothing and heavy lag in the Case-Shiller data, it’s hard to find a causal relationship between prices and mortgage rates…

Source: Bloomberg

…but with rates remaining above 7%, it seems hard to believe prices can continue their advance.

Everything You Need To Know As Trump Trial Heads To Verdict

As lawyers in the criminal trial of former President Donald Trump prepare to deliver their summations today, and the jury makes ready to begin deliberating as soon as the middle of the week, speculation runs high as to whether proceedings will end in an acquittal, a guilty verdict, or a hung jury.

If President Trump is convicted, evidentiary concerns and Justice Juan Merchan’s conduct are likely to raise substantive issues for the defense to pursue at the appellate level, according to one legal expert.

But other judicial experts disagree, saying it is premature to try to assess the trial’s fairness.

Manhattan District Attorney Alvin Bragg charged President Trump with 34 counts of falsifying business records in the first degree, a class E felony.

The former president was charged under the statute New York Business Law 175.10, which states that “A person is guilty of falsifying business records in the first degree when he commits the crime of falsifying business records in the second degree, and when his intent to defraud includes an intent to commit another crime or to aid or conceal the commission thereof.”

The second crime in this case was the alleged violation of New York Election Law 17-152: “Conspiracy to promote or prevent election. Any two or more persons who conspire to promote or prevent the election of any person to a public office by unlawful means and which conspiracy is acted upon by one or more of the parties thereto, shall be guilty of a misdemeanor.”

The 34 records in this case consist of 11 checks cut to Michael Cohen, a former personal attorney to President Trump, and the corresponding vouchers and invoices. Prosecutors allege these payments, categorized as legal expenses, were reimbursement for money Mr. Cohen paid to Stephanie Clifford, better known as adult actress Stormy Daniels, as part of a scheme to influence the 2016 elections.

In order to prove their case, prosecutors need to show that President Trump had the intent to defraud—more specifically, the intent to conceal the alleged conspiracy—when causing the creation of the business records.

Who Testified?

David Pecker, former head of American Media, Inc. (AMI) and publisher of the National Enquirer, was the first to take the witness stand.

Over several days, he outlined an agreement with Mr. Trump and collaboration with Mr. Cohen as AMI purchased two stories that Mr. Pecker believed would harm the 2016 Trump campaign. Neither of the two deals Mr. Pecker was involved in are related to the current charges, but prosecutors argued they provide important context and evidence toward a conspiracy.

Next, longtime Trump assistant Rhona Graff testified, affirming that she had entered contact information for key people in the case into her contact management system, offering evidence that Mr. Trump was in touch with alleged co-conspirators.

Then Gary Farro, a banker formerly with First Republic Bank, took the witness stand to affirm the creation of accounts for Mr. Cohen’s LLCs, and confirm the $131,000 wire transfer.

Robert Browning, executive director of C-SPAN’s archives, took the witness stand to allow into evidence several video clips of President Trump campaigning. Philip Thompson, a regional director at Esquire Deposition Solutions, testified to the authenticity of a deposition transcript from another Trump case.

Lawyer Keith Davidson next testified, detailing his representation of Karen McDougal and later Ms. Clifford, and his dealings with Mr. Cohen to complete a settlement contract for Ms. Clifford. Several revealing texts were entered into evidence throughout his testimony, showing exchanges between Mr. Davidson and others.

Then, two members of the district attorney’s office were called to the witness stand. Forensic analyst Doug Daus had reviewed Mr. Cohen’s cell phones, and through his testimony phone records were admitted into evidence. Paralegal Georgia Longstreet had reviewed President Trump’s social media posts and several were entered into the record, including ones depicting a change in attitude toward Mr. Cohen.

Next, Hope Hicks, former Trump campaign communications director testified and affirmed then-candidate Trump’s schedule on key dates, allowing into evidence emails exchanged within the Trump campaign.

Jeffrey McConney, former Trump Organization comptroller, testified about his oversight of the process of accepting and processing Mr. Cohen’s invoices, which Mr. McConney categorized as legal expenses, allowing into evidence email exchanges about the payments. Deb Tarasoff, a bookkeeper for The Trump Organization who worked under Mr. McConney, testified she processed these invoices, cutting the checks Mr. Trump ultimately signed.

Sally Franklin with Random House was then called to the witness stand to read into the record several excerpts from Trump books on life and business advice. Later during the trial, Tracey Menzies with Harper Collins read into the records from other Trump books.

When Ms. Clifford took the witness stand, it was to a crowded courthouse. Ms. Clifford, whom the judge described as a “difficult to control” witness, gave salacious details in her testimony that led to the defense calling for a mistrial, which the judge denied on the basis that the issues could be resolved during cross-examination.

Next, Trump Organization employee Rebecca Manochio testified that she shipped checks from Trump Tower to Washington for President Trump to sign in 2017. Former Oval Office Director of Operations Madeleine Westerhout testified that she saw President Trump signing checks, which had been sent through FedEx to bodyguard Keith Schiller and later herself.

Daniel Dixon with AT&T and Jennie Tomalin with Verizon testified to the authenticity of phone records that were then entered into evidence. Paralegal Jaden Jarmell-Schneider, with the district attorney’s office, created summary charts of records from Mr. Cohen’s phone the prosecutors believed relevant to the case.

Finally, Mr. Cohen testified as the final witness for the prosecutors, with testimony lasting a week.

The defense called few witnesses: Paralegal Danny Sitko, with defense attorney Todd Blanche’s office, had created summary charts of phone records between Mr. Cohen and attorney Robert Costello. Mr. Costello’s testimony refuted claims Mr. Cohen made that Mr. Costello was meant to keep tabs on him for Rudy Giuliani, who later became an attorney to President Trump.

Who Didn’t Testify?

Two people frequently mentioned in testimony were unavailable to the court. The first, Dylan Howard, chief content officer for AMI, initially brought the Clifford deal to the attention of Mr. Pecker and Mr. Cohen. Mr. Howard facilitated the purchase of the three stories mentioned at trial, and received and sent many texts shown in court exchanged between him and Mr. Davidson and Mr. Cohen. Mr. Howard now lives in Australia and is unable to travel due to a serious health condition.

Also unavailable was Allen Weisselberg, who is currently serving a five-month prison sentence for committing perjury in a separate civil fraud case that went to trial last fall. Mr. Weisselberg, the former CFO of The Trump Organization, came up with the idea to pay Mr. Cohen $420,000. Mr. Cohen could not testify as to why his reimbursement request for $130,000 was grossed up to $420,000, saying “I just wanted to get my money back.”

…

Will the Case Reach the Jury?

Defense attorneys made two requests for the judge to make a significant decision before turning things over to the jury: to dismiss the case or to find Mr. Cohen’s testimony not credible.

Justice Merchan is likely to issue a quick ruling on the motion, as he already instructed jurors to be present for closing arguments after the long weekend.

What Happens Next?

Justice Merchan asked jurors to prepare for a long day today.

Summations from both sides are expected to last the whole day, and the judge said his instructions to the jury would take an hour.

Prosecutors will sum up their case by reminding jurors of what they believe is the most compelling evidence. But for the defense, especially having called only two witnesses, this will be a key moment to present their own narrative.

Defense attorneys are expected to argue that nothing criminal occurred, as the nondisclosure agreements are legal, as is the payment of an attorney for legal services, and that the promotion of a person in an election through lawful means is not a crime.

On May 21, the judge held a charge conference with attorneys, who debated over what language would be used to instruct jurors on the applicable laws and their interpretation.

In some cases in which Justice Merchan rejected the attorneys’ proposed language, he said they could argue those points at summations on May 28.

The charge conference allowed both parties to present to the judge arguments about why certain language would prejudice their side, allowing the judge to put together an instruction script that avoids such prejudice.

How the judge delivers this interpretation of the law will inevitably influence the jury’s decision.

Should jurors be instructed that President Trump needed to have “willfully” concealed intent to defraud?

Should the instructions include an example explaining that a legal expense might not classify as a campaign expenditure?

Should jurors be told up front all the things prosecutors are not required to show?

Should jurors be given an example of what it means “to cause a false entry to be made”?

The jurors will work on May 29, when previously they have taken Wednesdays off, to begin deliberations while closing arguments are still fresh in their minds.

The jury’s job is to determine the facts of this case and decide whether those actions violated the law.

If the 12 jurors don’t come to a unanimous decision, the case will end in a mistrial.

There is no set time in which the jurors are required to return their verdict; a decision could be returned the same day or even take weeks.

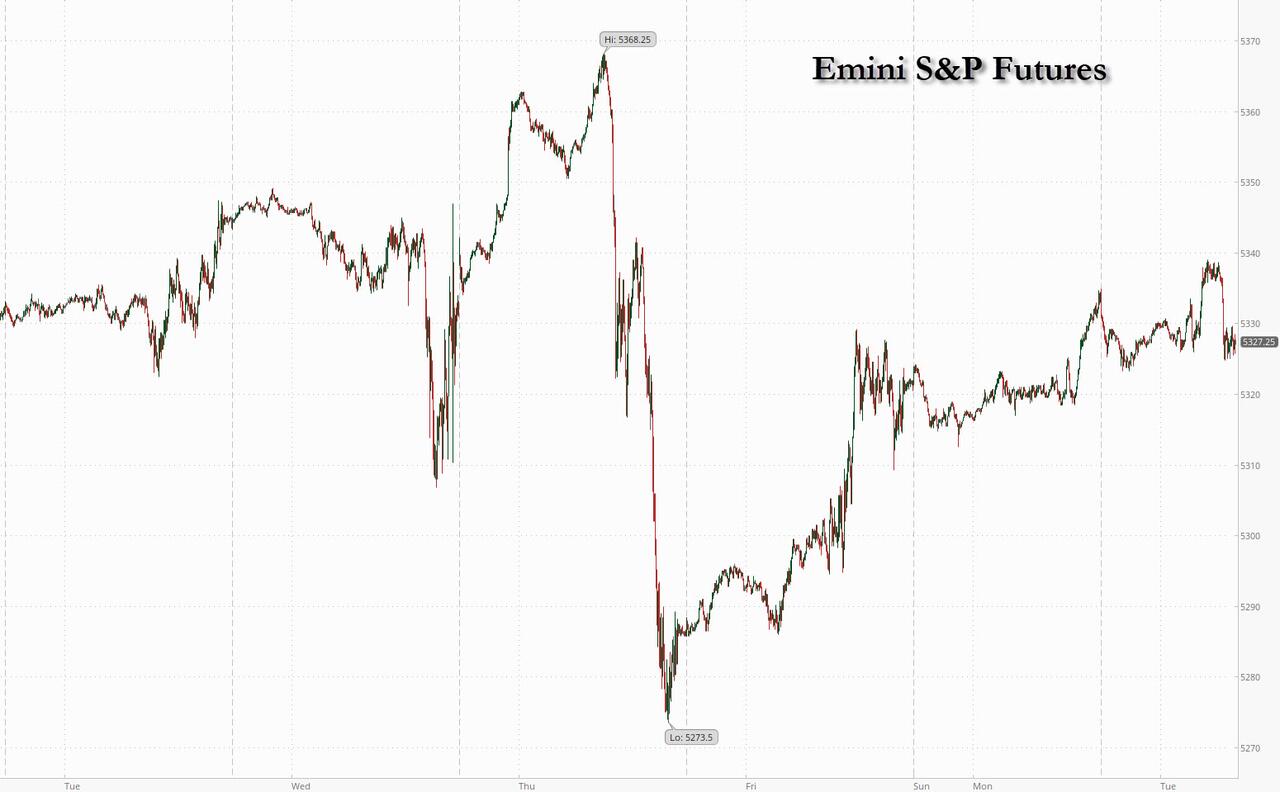

Futures Rise On Apple China Sales Rebound As Attention Turns Back To Inflation

Stocks traded in a narrow range as markets reopened in the US and Europe with investors putting (a stronger than expected) Q1 earnings season in the history books, and looking to Friday’s core PCE print prints and central bank speakers for hints on the timing of interest-rate cuts. As of 7:45am, S&P futures climbed 0.1%, while Nasdaq futs gained 0.2% helped by premarket gains for Apple which added 2.4% after China shipments rebounded. Europe’s Stoxx 600 dipped 0.2%, trimming its gain in May to 3.2%. The Bloomberg dollar index dropped while treasuries erased small gains, with 10Y yields trading at 4.46% before a slate of short-term auctions including offers of 2Y and 5Y notes on Tuesday. Brent crude rose as tensions in the Middle East ratcheted higher. On the calendar, today we get the release of house price and confidence data, before we get reports on GDP on Thursday. The centerpiece then comes on Friday, with the publication of the PCE price index, the Fed’s favorite inflation gauge. Economists expect that to show the smallest advance so far this year for the measure.

In premarket trading, the most notable movers was Apple whose shares gained 2.2% after new figures showed an iPhone sales rebound in China last month, with shipments increasing 52% amid discounts from retail partners.

Oklo rose 10%, as the Sam Altman backed provider of nuclear fission reactors extended its recent gains.

Crowdstrike gains 2.1% as Morgan Stanley boosts its price target on the stock and names it as a top pick, predicting it could become the next cybersecurity company to surpass a $100b market capitalization.

DuPont de Nemours gains 1.2% as Citi lifts its rating on the chemicals company to buy from neutral, based on upside scope from recently announced business separation plans and on recovery potential in its electronics unit.

GameStop shares jump 24% as the video-game retailer extends Friday’s postmarket gains, which were triggered by the company raising almost $1 billion in a share sale.

Nvidia shares gain 2.3%, putting the chipmaker on track to extend its post-earnings rally for a third consecutive session.

Zscaler slips 0.5%, following a downgrade to equal-weight at Wells Fargo, which says the security software firm faces pressures from increased competition.

As traders return from the long weekend they’re alert for problems connected with the switch to “T+1” rule — whereby US equities will settle in one day rather than two. There are worries about potential teething issues, including that international investors may struggle to source dollars on time, global funds will move at different speeds to their assets, and everyone will have less time to fix errors.

Meanwhile, strong earnings from tech megacaps like Nvidia helped stocks erase April’s slump, even as US data and cautious fedspeak cooled market bets on the scope for policy easing this year. And in a busy week for data, traders are concentrating on the PCE deflator, the Fed’s preferred gauge of inflation, on Friday.

“We are very much on the inflation data watch for now,” said Marija Veitmane, senior multi-asset strategist at State Street Global Markets. “Stocks and risk will continue to be supported, but I don’t see change of leadership nor a broadening of the performance. Large-cap growth stocks will be leading.”

European stocks are lower; the Stoxx 600 is down 0.2% with underperforming sectors including healthcare and industrials. European miners may be active on Tuesday as copper, along with other base metals, gained ground after China stepped up efforts to rescue its property market and a weakening US dollar boosted the demand outlook. Consumer inflation expectations in the euro zone ticked lower in April, ECB data showed, as policymakers next meet on rates on June 6. On Monday, France’s Francois Villeroy de Galhau said the ECB shouldn’t exclude cutting rates in both June and July, though hawkish policymakers including Executive Board member Isabel Schnabel recently came out in opposition to back-to-back moves.

Earlier, Asian stocks rose in thin trading, driven by advances in Hong Kong, ahead of global inflation prints set to offer monetary policy clues. The MSCI Asia Pacific Index rose as much as 0.3%, overcoming a shaky start. Gains were also notable in Indonesia and Taiwan, while Japanese benchmarks dipped. Volumes on many key gauges were 15-20% below 30-day averages after US and UK markets were closed on Monday.

“For all intents and purposes, we haven’t started the week — things will pick up tonight when the US opens,” said Kyle Rodda, a senior market analyst at Capital.Com. “I suspect the next few days, all else being equal, will be driven by end-of-month flows and then that crucial PCE Index release.”

In FX, the Bloomberg Dollar Spot index traded lower versus most of its Group-of-10 peers amid month-end flows as markets in the UK and the US reopen after holidays. The Index slipped as much as 0.2% before paring most losses. The Swedish krona tops the G-10 FX pile, rising 0.4% versus the greenback.

EUR/USD up a third day, rises 0.2% to 1.0880; the move loses traction as leveraged offers around the day’s high act as a cap for now, a Europe-based trader says

The Swedish krona was the best performing G10 currency versus the dollar, climbing 0.5% to 10.5596; EUR/SEK fell 0.4% to 11.4829, lowest since April 10. Riksbank Governor Erik Thedeen said the threshold for a rate cut in June is “very high”

In rates, treasuries were mixed with front-end outperforming, following wider gains across the gilt curve after remarks by BOE’s Broadbent, who said disinflation is “getting there,” according to the Times. US 2-year yields are richer by around 2bp on the day while yields are marginally cheaper further out the curve, steepening 2s10s spread by 1.8bp vs Friday’s close. 10-year is little changed at 4.465%, trailing gilts by 2.5bp in the sector; gilts outperform after a survey said UK shop inflation was now back to ‘normal’ levels. UK 10-year yields fall 3bps to 4.23%. The US session also features two auctions, 2-year notes at 11:30am New York time and 5-year notes at 1pm; the WI on the 2-year yield is around 4.903% ahead of $69b sale, about 0.5bp cheaper than last month’s result; $70b 5-year note sale follows

In commodities, oil prices advance, with WTI rising 1.5% to trade around $78.90 as tensions in the Middle East ratcheted higher following the death of an Egyptian soldier during a clash with Israeli troops. Spot gold falls 0.3%.

Bitcoin fell as traders monitored transfers by wallets belonging to the failed Mt. Gox exchange, whose administrators have been stepping up efforts to return a $9 billion hoard of the largest digital asset to creditors.

Looking at today’s calendar, US economic data includes 1Q house price index, March FHFA house price index and S&P CoreLogic home prices (9am), May consumer confidence (10am) and Dallas Fed manufacturing activity (10:30am); Fed officials’ scheduled speeches include Kashkari (9:55am), Cook and Daly (1:05pm).

Market Snapshot

S&P 500 futures up 0.3% to 5,336.75

STOXX Europe 600 little changed at 522.51

MXAP little changed at 181.06

MXAPJ little changed at 566.63

Nikkei down 0.1% to 38,855.37

Topix little changed at 2,768.50

Hang Seng Index little changed at 18,821.16

Shanghai Composite down 0.5% to 3,109.57

Sensex little changed at 75,344.59

Australia S&P/ASX 200 down 0.3% to 7,766.71

Kospi little changed at 2,722.85

German 10Y yield little changed at 2.54%

Euro up 0.1% to $1.0873

Brent Futures up 0.2% to $83.30/bbl

Gold spot down 0.4% to $2,341.29

US Dollar Index down 0.11% to 104.48

Top Overnight News

The US stock market is finally as fast as it was about a hundred years ago. That was the last time share trades in New York settled in a single day, as they will from Tuesday under new Securities and Exchange Commission rules.

The European Central Bank should use quantitative-easing programs primarily in times of crisis as their costs might be more pronounced than other tools in its repertoire, according to Executive Board member Isabel Schnabel.

Inflation expectations of consumers in the euro zone edged lower in April, according to the European Central Bank — reinforcing plans to start lowering interest rates next week. Prices are seen advancing 2.9% over the next 12 months, down from 3% in March, the ECB said Tuesday in its monthly poll. That’s the lowest level since September 2021, it said.

The pound is nearing its strongest level in years against two of its major counterparts as traders ratchet up bets that the Bank of England will keep interest rates on hold for longer than peers.

China’s smartphone market saw a 2% growth in sales Q1. Sales of foldable phones +48% Y/Y. Huawei rose to the top spot for the first time in quarterly global shipments, surpassing Samsung, according to Counterpoint Research. China iPhone shipments jump 52% in April.

UBS Global Research raises 2024 year-end S&P500 target to 5600 (prev. target 5400, current 5304)

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed with price action mostly rangebound in the absence of a lead from Wall St and as geopolitical uncertainty lingered following an Israeli strike on Rafah which killed dozens of Palestinians on Sunday. ASX 200 swung between gains and losses albeit in a thin range with sentiment not helped by soft retail sales. Nikkei 225 retreated after stalling beneath the 39,000 level as participants also digested the firm Services PPI data which accelerated by its fastest pace since 2015. Hang Seng and Shanghai Comp were somewhat varied as Hong Kong outperformed with Alibaba Health Information Technology front-running the gains post-earnings, while there was also notable strength in China’s major oil companies after the recent upside in underlying commodity prices. Conversely, the mainland lacks conviction with only brief support seen in property stocks following Shanghai’s latest measures to spur the flagging sector.

Top Asian News

China’s Politburo said preventing and defusing financial risks is linked to national security and people’s property security, while it added China must act to prevent and defuse financial risks, as well as promote high-quality financial development Furthermore, it stated financial risks are a major hurdle that must be overcome, according to state media.

Shanghai adjusted the minimum down payment ratio for first-home buyers to no less than 20% and for second-home buyers to no less than 30%, while it cut the lower limit for interest rates on first-home mortgages to LPR minus 45bps. Furthermore, Shanghai is to establish and improve the housing system, explore buying housing through state-owned platform companies and other entities, as well as optimise the supply of housing security.

Japanese Finance Minister Suzuki said it is important for currencies to move in a stable manner reflecting fundamentals. Suzuki added that a weak yen boosts exporters’ profits but increases the burden for consumers, while he is concerned more about the negative impact of a weak yen and is closely watching FX moves.

BoJ says its underlying inflation measure all fell below 2% in April.

Chinese President Xi has urged promoting high-quality and sufficient employment, according to state media.

China Politburo says China will promote the coordination and linkage of fiscal, monetary, investment, consumption, industrial, regional and other policies with employment policies, via state media.

European bourses, Stoxx 600 (U/C) are mixed and trade modestly on either side of the unchanged mark, continuing the tentative price action seen in APAC trade overnight. European sectors are mixed; Real Estate takes the top spot, benefitting from the relatively lower yield environment, whilst Travel & Leisure is weighed on by broader strength in crude prices. US Equity Futures (ES +0.3%, NQ +0.5%, RTY +0.5%) are indicative of a firmer open, after US markets were shut on Monday on account of Memorial Day. Apple (+1.6% pre-market) gains following reports that China iPhone shipments rose 52% in April.

Top European News

ECB Consumer Expectations Survey (Apr): 12-month inflation 2.9% (prev. 3.0%); 3-year ahead 2.4% (prev. 2.5%); growth outlook less negative and labour market seen stable

UK PM Sunak is to announce a GBP 2.4bln tax cut for pensioners in a bid to shore up the key Conservative ‘grey vote’ and stabilise the party’s chaotic start to the general election campaign, according to FT.

Statistics Norway Oil Investment Survey: Total investments in oil and gas activity in 2025, including pipeline transportation, are estimated at NOK 216 billion, +5.2% than estimated in the previous quarter.

UK Shadow Chancellor Reeves says Labour will not be matching the “Triple Lock Plus”

Central Banks

Fed’s Kashkari (non-voter) says inflation has moved sideways recently; need to wait and see and get more confidence on prices; should not rule anything out on policy path, via CNBC. Fed in good position because of strong labour market.No need to hurry to cut rates; the Fed could potentially even hike rates if inflation fails to come down further.

Fed’s Bowman (voter) would have supported either waiting to slow QT pace or more tapered slowing in balance sheet run-off, according to Reuters. ‘In my view’ bank reserves are not yet near ‘ample’ levels given the still-sizable take-up of ON-RRP. Important to keep reducing balance sheet size to reach ample reserves as soon as possible and while the economy is strong. Important to communicate any change to the run-off rate does not reflect a change in the Fed’s monetary policy stance. ‘Strongly’ supports the principle of balance sheet holdings primarily being composed of Treasuries. A longer-run balance sheet ’tilted slightly’ toward shorter maturities would allow flexibility in approach. In future, when the Fed conducts QE to restore market functioning or financial stability it should communicate that purchases will be temporary and unwound when market conditions have normalised. FOMC would have benefited from an earlier decision to taper and end QE in 2021; and would have allowed earlier rate hikes.

Fed’s Mester (voter) said would be preferable for FOMC statements to use more words to describe the current assessment of the economy and how that influences the outlook, as well as risks to that outlook, according to Reuters. Scenario analysis should also be incorporated as a standard part of Fed communications. Would like the Fed to publish an anonymised matrix of economic and policy projections so market participants can see the linkage between each participant’s outlook and their view of appropriate policy associated with that outlook. Expect the Fed will consider communications as part of its next monetary policy framework review.

BoE Deputy Governor Broadbent rejected claims that the monetary policy committee acted too slowly and hit back at critics who have accused it of failing to control inflation, according to The Times.

ECB’s Lane said keeping rates overly restrictive for too long could push inflation below target in the medium-term which would require corrective action that could even mean having to descend below neutral, while they think inflation over the coming months will bounce around at the current level and then will see another phase of disinflation bringing them back to the target later next year, according to Reuters. It was separately reported that ECB’s Lane said policymakers needed to keep rates in restrictive territory this year to ensure inflation kept easing, according to FT.

ECB’s Rehn said inflation is converging to their 2% target in a sustained way and the time is thus ripe in June to ease the monetary policy stance and start cutting rates, while he added this assumes the disinflationary trend will continue and there will be no further setbacks in the geopolitical situation and energy prices.

ECB’s Villeroy said they have significant room for rate cuts with the Deposit Facility rate at 4% and barring a surprise, a rate cut in June is a done deal, while Villeroy added that he doesn’t say they should commit already on July but they should keep their freedom on the timing and pace.

ECB’s Schnabel said QE could have weakened the transmission of monetary policy during the recent tightening cycle, according to Reuters.

RBNZ activated debt-to-income restrictions which will create limits on the amount of high-DTI lending banks can make and will include an allowance for banks to do 20% of their lending outside of our specified limits, while banks must comply with new restrictions from July 1st.

BoJ Monetary Affairs Department Director-General Masaki said changes in wages in real terms will move to positive territory on a Y/Y basis and need to keep an eye on energy prices and forex moves, according to Reuters.

FX

DXY is relatively flat/contained trade thus far with the index currently within a 104.41-56 band and as such is in close proximity to its 200 DMA at 104.37.

Modest strength in the EUR which was relatively unreactive to upticks in German Wholesale Prices and to the the ECB SCE which saw the inflation view revised lower; EUR/USD trades within a 1.0855-79 range, and off best levels.

GBP is flat vs the USD and modestly softer against the EUR. Cable sits in a 1.2764-83 parameter after briefly topping yesterday’s 1.2777 high.

JPY is slightly softer vs the USD and losing against the EUR, AUD, and GBP despite the hotter-than-expected Japanese Services PPI overnight and the currency jawboning by Finance Minister Suzuki overnight. USD/JPY currently just shy of 157.00.

Upward bias across antipodeans following the overnight rebound in commodities. The Kiwi narrowly outperforms in a continuation of last week’s hawkish hold by the RBNZ.

PBoC set USD/CNY mid-point at 7.1101 vs exp. 7.2402 (prev. 7.1091).

Fixed Income

USTs are modestly firmer but with action relatively sparse and overall rangebound into a particularly busy week highlighted by PCE on Friday; docket for today is sparse, but focus will be on US 2yr & 5yr supply. Currently trading within a tight 108-28+ to 108-22 range.

Bunds are contained after lifting to a 130.52 peak on Monday, a high driven by remarks from ECB’s Lane who in a Dublin speech/FT interview outlined that the ECB is “barring major surprises” ready to begin easing. The ECB SCE saw saw lower inflation views at both the one- & three-year ahead timeframes, an update which was enough to lift Bunds to a 130.43 peak for today vs current 130.32.

Gilts are outperforming as the UK catches up to Monday’s EGB move, with UK-specifics light except for reports via the FT which note that Sunak is to announce a GBP 2.4bln tax cut for pensioners, a development which seemingly hasn’t had any bearing on Gilts given opposition Labour is well ahead in the polls. Gilts are holding above 97.00, just off the 97.14 session high.

Italy sells EUR 4.5bln vs exp. EUR 3.75-4.5bln 3.20% 2026 & 0.00% 2024 BTP Short Term and EUR 1.5bln vs exp. 1.0-1.5bln 0.10% 2033 I/L.

Germany sells EUR 0.846bln vs exp. EUR 1bln 2.30% 2033 Green Bund and EUR 0.986bln vs exp. EUR 1bln 2.10% 2029 Green:

Commodities

WTI and Brent are both holding on to the prior day’s gains but with a discrepancy in terms of intraday price changes amid the lack of WTI settlement yesterday as US markets were closed on account of Memorial Day. The complex was lifted amid heightened geopolitical escalations, following recent Israeli strikes on Rafah. Brent August in a USD 82.76-83.11/bbl intraday parameter.

Precious metals are weaker across the board despite the softer Dollar, with no obvious reason for the weakness aside from the pullback in precious metals. XAU sits within a USD 2,340.79-2,356.44/oz parameter.

Firmer across the board with base metals rebounding; desks are citing positive sentiment underpinned by the announcement of China’s USD 47.5bln chip fund.

UBS expects OPEC+ to extend current production cuts for at least another three months; says oil remains a valid geopolitical hedge – sees Brent USD 87/bbl by year-end

Geopolitics – Middle East

Israeli tanks have reached Rafah city centre, according to Reuters witnesses

“Israeli media: Leaders of Israeli opposition parties will discuss tomorrow the formation of an alternative government and the ouster of Netanyahu”, according to Sky News Arabia.

Ambrey says it is aware of incident 54NM southwest of Yemen’s Hodeidah, according to advisory.

Israeli PM Netanyahu said something went tragically wrong regarding the Israeli air strike on Rafah and it will be investigated, while Israel’s government said initial reports are that Rafah civilians died from a fire that broke out after an Israeli strike on Hamas chiefs.

Israeli PM Netanyahu reportedly intends to dissolve the War Council so that he does not have to include Ben-Gvir and Smotrich in it, according to the Israel Broadcasting Corporation.

Israel is waiting to hear Hamas’s stance before deciding on re-joining hostage talks, according to Times of Israel.

Palestinian media reported intensive Israeli shelling in the vicinity of the Emirati hospital west of Rafah in the southern Gaza Strip, according to Al Arabiya.

Pro-Iranian militias in Iraq claimed responsibility for launching three drones at military targets in Eilat, while Israel said three drones launched from Iraq were intercepted.

White House noted devastating images following the Israeli strike in Rafah on Sunday, while it is actively engaging the IDF and partners on the ground to assess what happened. Furthermore, the White House said Israel must take every precaution possible to protect civilians.

French President Macron said he is outraged by the Israeli strikes that have killed many displaced persons in Rafah and called for these operations to stop.

EU’s Borrell said he is horrified by news out of Rafah regarding Israeli airstrikes killing dozens of displaced persons including small children and condemned this in the strongest terms, while he called for attacks to stop immediately. EU Borrell also stated that he has the green light from EU ministers to reactivate the Rafah border mission.

UN Secretary-General Guterres said they condemned Israel’s practices that led to the killing of dozens of innocent people seeking shelter from the conflict and called for the terror to stop, according to Reuters.

An Egyptian soldier was killed in a clash with Israeli troops at a crossing on Monday, according to Bloomberg.

Yemen’s Houthis said they launched attacks on three ships in the Indian Ocean and Red Sea, while Houthis also stated that they targeted two US destroyers in the Red Sea, according to Reuters.

IAEA report stated that Director General Grossi deeply regrets that Iran has not reversed its decision to bar several experienced inspectors, while it noted that outstanding safeguard issues including uranium traces at undeclared sites remain unresolved. It also stated that according to the IAEA’s definition, Iran’s stock of uranium enriched up to 20% is theoretically enough to produce a nuclear bomb if enriched further, according to Reuters.

Geopolitics – Other

Ukrainian President Zelensky will visit Belgium on Tuesday to sign the latest in a string of security accords with Western allies, according to the Belgian PM’s office cited by Reuters.

Ukrainian commander said French military instructors are to visit Ukrainian training centres, according to Reuters.

Russia’s Foreign Ministry said Russia will respond to the restriction on Russian diplomats’ movement in Poland, according to TASS.

China’s Foreign Ministry said US lawmakers paid a visit to Taiwan despite China’s strong opposition and it urged them to stop playing the Taiwan card and stop using excuses to interfere in China’s internal affairs, while it also lodged stern representations against the visit, according to Reuters.

China and the US held talks on maritime issues and exchanged views on May 24th, while they will continue negotiations to avoid a misunderstanding and agreed to manage maritime risks, according to China’s Foreign Ministry. Furthermore, China and the US agreed to maintain dialogue and China urged the US to refrain from intervening in maritime disputes between China and its neighbours, while it added the US should refrain from ganging up to ‘use the sea to control China’ and should immediately stop supporting and condoning ‘Taiwan independence’ forces.

China Maritime Safety Authority said China is to conduct military exercises in the Yellow Sea between May 28th and June 3rd and will conduct sea rocket launches in the Yellow Sea on May 28th-31st, according to Reuters.

North Korea launched a rocket carrying a spy satellite which exploded in the first stage of the launch. South Korea and Japan condemned North Korea’s launch, while the US said North Korea’s launch is a brazen violation of UN Security Council resolutions and raises tensions. Furthermore, the launch was said to have involved technologies directly involved in North Korea’s ICBM program and the US is assessing the situation but noted that the launch did not pose an immediate threat, according to Reuters.

US Event Calendar

09:00: March S&P CS Composite-20 YoY, est. 7.30%, prior 7.29%

09:00: March S&P/CS 20 City MoM SA, est. 0.30%, prior 0.61%

09:00: March FHFA House Price Index MoM, est. 0.5%, prior 1.2%

09:00: 1Q House Price Purchase Index QoQ, prior 1.5%

10:00: May Conf. Board Present Situation, prior 142.9

10:00: May Conf. Board Expectations, prior 66.4

10:00: May Conf. Board Consumer Confidenc, est. 96.0, prior 97.0

10:30: May Dallas Fed Manf. Activity, est. -12.5, prior -14.5

Central Bank Speakers

00:55: Fed’s Mester Speaks at Bank of Japan Event

00:55: Fed’s Bowman Speaks at Bank of Japan

09:55: Fed’s Kashkari Gives Panel Remarks

13:05: Fed’s Cook, Daly Speak on AI

DB’s Jim Reid concludes the overnight wrap

Good evening from a wet New York where I’ve just landed. So an early edition for you today and hopefully I’ll be asleep for part 2 of my Sunday night sleep by the time you read this. Given it was a holiday in both the US and the UK yesterday we’ll still preview the week ahead this morning and briefly review last week even if the rest of the world was trading yesterday.

In fact in the absence of the US and the UK the week has started off positively as the ECB speakers yesterday leaned dovishly with French Governing Council member de Galhau suggesting they shouldn’t rule out back to back June/July cuts. Chief Economist Lane was also slightly dovish in an interview with the FT although didn’t provide any additional hopes to the July cut narrative. Finland’s Olli Rehn also supported a cut next week in comments yesterday. Overall European bonds yields rallied 3-6bps across the curve and the number of basis points of cuts priced in for December 2024 increased from 58bps (a low for the year) on Friday to 61bps. A slightly softer than expected German IFO probably helped as well. European equities were up nearly half a percent to start the week.

Asian equity markets rallied 0.5% to 1.5% yesterday but are a little more subdued in early trading this morning with most either side of the flatline with the exception of the Hang Seng which is +0.8% in very early trading. S&P 500 (+0.12%) and NASDAQ 100 (+0.21%) futures are slightly higher after yesterday’s holiday.

Early morning data showed that Japan’s services PPI advanced +2.8% y/y in April (v/s +2.3% expected), recording its fastest rise in nine years and higher than the revised +2.4% gain in March. Elsewhere, retail sales in Australia rebounded +0.1% m/m in April but less than Bloomberg’s forecast for a +0.2% advance. This followed a -0.4% fall last month and a YoY rate just over 1% that has only really been lower during Covid in recent times. So a very soft consumption story in Australia at the moment.

In the energy space, Brent crude (+0.04%) prices have steadied this morning after rebounding more than +1.0% yesterday from more than three-month lows ahead of the online OPEC+ meeting on June 2.

Before that, all roads this week point towards the April US core PCE print on Friday which in MoM terms is expected to edge down from +0.32% to +0.26%. You don’t need me to tell you how well scrutinised this data will be and how important it is to the Fed. As part of the same release, personal income (+0.4% forecast vs. +0.5% previously) and consumption (+0.2% vs. +0.8%) will likely come in a little softer. Back to inflation, and the preliminary May CPIs are out in Germany tomorrow, and in France, Italy and the Eurozone on Friday. Our European economists see this coming in at + 2.55% (+2.4% in April) for headline and +2.84% (+2.66% April) for core inflation. See their full preview here. At the start of 2024, euro area inflation avoided the sizeable upside surprises we saw in the US, but the last print in April did see core inflation slightly stronger than expected. I t would be a tall order for the data to derail the strongly signaled ECB cut next week but it could have important implications for the ECB’s signal beyond this. We will also have the latest inflation expectations from the ECB consumer expectations survey for April today. Our economists’ own dbDIG survey (see here) suggests that median medium-term expectations are likely to stay stable at 2.5%. Finally on inflation, Tokyo CPI is also out on Friday.

Elsewhere, in the US we have consumer confidence today, the Fed Beige Book tomorrow, the second reading of GDP and the Trade Balance on Thursday with the Chicago PMI alongside the personal spending and income report (alongside core PCE) on Friday. In China, May’s PMIs on Friday will be the highlight. You can see the full day-by-day week ahead at the end including all the main central bank speakers highlighted too.

In what is a busy busy year for elections, this week we have the South African election tomorrow (DB primer here), the last leg of the Indian elections on Saturday and the Mexican equivalent on Sunday. Note it’s also less than two weeks until the European Parliamentary elections. DB has a great primer here.

It might seem like ancient history by now, but when it came to last week, markets lost some momentum after strong data cast doubt on the chance of rate cuts. In particular, the flash PMIs for May came in stronger-than-expected on both sides of the Atlantic, with the US composite PMI up to a two-year high, whilst the Euro Area number hit a one-year high. Moreover, that positive data was cemented by a fall in the US initial jobless claims, along with an upward revision in the University of Michigan’s final consumer sentiment index. That strength has been evident in other indicators, and the Atlanta Fed’s GDPNow Index is pointing to US Q2 growth at an annualised +3.5% pace.

Much as the positive data was welcome, it also led to a fresh reassessment about how rapidly central banks would be able to cut rates. For instance, the amount of cuts priced in by the Fed’s December meeting came down by -10.7bps over the week to 33bps. And for the ECB, it fell by -8.3bps to 58bps, which was the fewest so far this year. This trend was further exacerbated by the minutes from the latest Fed meeting, which leant in a hawkish direction. In fact, it said that “ Various participants mentioned a willingness to tighten policy further should risks to inflation materialize in a way that such an action became appropriate.” So that helped to crystallise concerns about more restrictive monetary policy.

This backdrop meant that sovereign bonds struggled globally. Yields on 2yr Treasuries (+12.2bps) saw their largest rise in 6 weeks (+1.1bps Friday) while 10yr yields were up +4.4bps over the week (-1.2bps Friday) to 4.47%. Similarly in Europe, yields on 10yr bunds were up +6.8bps (-1.2bps Friday), and in the UK there was an even larger selloff after the April inflation print surprised on the upside. That meant yields on 10yr gilts were up +13.4bps for the week (+0.2bps Friday) and the 2yr yield was up by +18.7bps (-0.4bps Friday). Finally in Japan, there was a significant milestone as yields on 10yr JGBs surpassed the 1% mark in trading for the first time since 2012. By the end of the week, they’d risen by +5.6bps (+0.3bps Friday). Obviously European bonds have started the week on a firmer footing which perhaps reflects the uncertainty with the back and forth on rate expectations at the moment. Albeit it’s a low volatility back and forth.

The prospect of higher rates for longer (last week at least) caused a mixed week for risk assets. The S&P 500 was essentially flat on the week (+0.03%), though a +0.70% recovery on Friday helped it just post a 5th consecutive weekly gain. There were contrasting moves within this, with a strong earnings report from Nvidia helping the Magnificent 7 (+2.91%, and +1.63% in Friday) and the NASDAQ (+1.41%, and +1.10% on Friday) up to new record highs by the close on Friday. However, most sectors outside of tech lost ground, with the Dow Jones index down -2.33% on the week (+0.01% on Friday). Meanwhile in Europe, the STOXX 600 fell -0.45% last week (-0.19% Friday).