Authored by David Stockman via InternationalMan.com,

Jay Powell did it again assuring the 1% that he has their back.

Markets recovered their poise over the last 24 hours, as investors were relieved after Fed Chair Powell stuck to his recent views on the economic outlook. In his remarks yesterday, he said that recent data didn’t “materially change the overall picture” and that on inflation “it is too soon to say whether the recent readings represent more than just a bump.” In addition, he reiterated that if “the economy evolves broadly as we expect, most FOMC participants see it as likely to be appropriate to begin lowering the policy rate at some point this year.” So that all helped to validate market pricing, which still expects 71 bps of rate cuts from the Fed by the December meeting.

Needless to say, the man has no shame. And that’s to say nothing of intellectual firepower. There is not even a smidgen of a case that rate cuts in the present context will help main street, and the Fed heads and their Wall Street megaphones don’t actually even try to make that argument.

Instead, they argue for rates cuts by default. If by some tortured version of the CPI (i.e. the “supercore” index, which eliminates 61% of the CPI items by weight) they can espy the in-coming inflation trend settling into a liberally defined vicinity of 2.00%, that’s purportedly good enough to end the money-printing pause that has been in place since March 2022. Thereafter, it’s back to business as usual, flooding the canyons of Wall Street with cheap credit and a new burst of financial asset inflation.

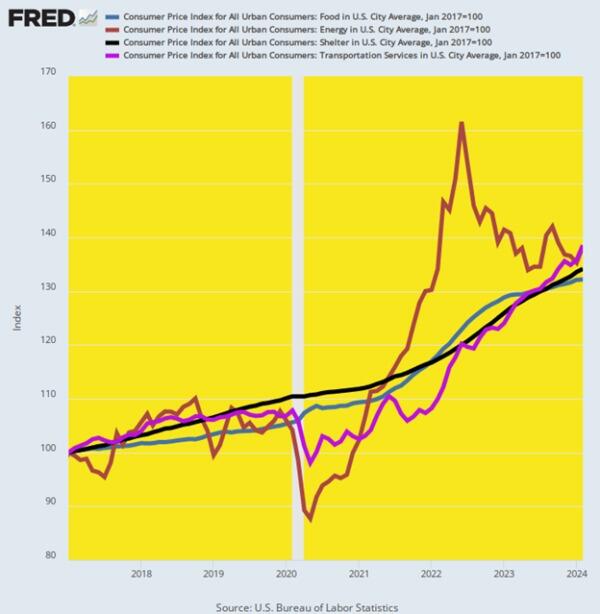

Never mind that in this particular inflation-cycle, the general price level is up by 28% since January 2017 and that tens of millions of households and businesses have been badly damaged, even as others harvested windfall gains. When it comes to inflation and all the other so-called macroeconomic metrics on their dashboards, past history–even the recent past—is dead to the Fed heads.

Instead, it’s all about the current and especially the prospective rate of change as embodied in the silly “dot-plots” they gurgle around in their brains and update four times per year.

And we do mean silly. After all, if the consensus of the 19 geniuses who participate in the dot-plot guessing game espies say a 2.27% gain in the supercore index over the next year, so what?!

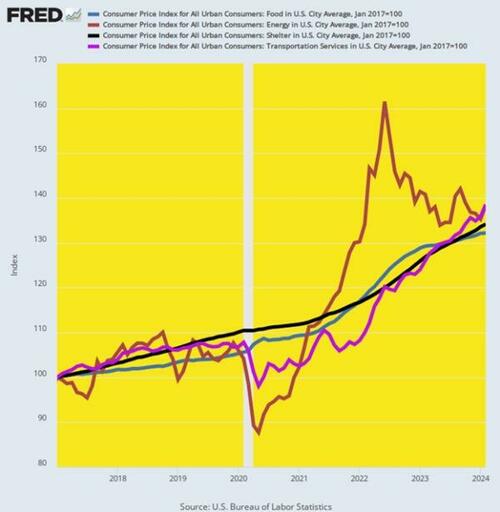

The fact is, the US economy needs a lot more relief from its recent inflationary pounding than the Fed’s guesstimated rate of slowdown in the forward year rise of the price level. After all, here is the increase in the core cost of living items since January 2017.

Change in Core Cost-of-Living Components Since January 2017:

In the case of savers, retirees, wage-earners in globally impacted industries where wages haven’t kept up with the CPI, isn’t the above enough punishment? Doesn’t it actually amount to state-directed expropriation of their living standards and modest accumulated wealth?

In any event, what the hell is so almighty urgent about rate cuts when the economy is still growing apace and the cumulative inflation of the last seven years has not been relieved in the slightest?

Increase In Major Cost-of-Living Components of the CPI Since January 2017

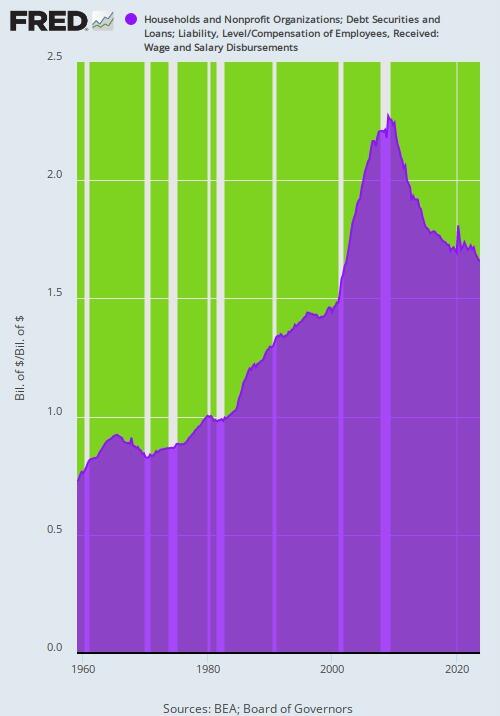

The dog-eared claim that rate cuts will enhance the growth rate of output, jobs, investment and spending on main street just doesn’t wash. Artificially low interest rates overwhelmingly fuel borrowing for speculation and financial engineering (e.g. stock buybacks) on Wall Street, not borrowing for productive investment on main street or even for enhanced “consumption” by the household sector, which is now buried in debt up to the gills after decades of easy money.

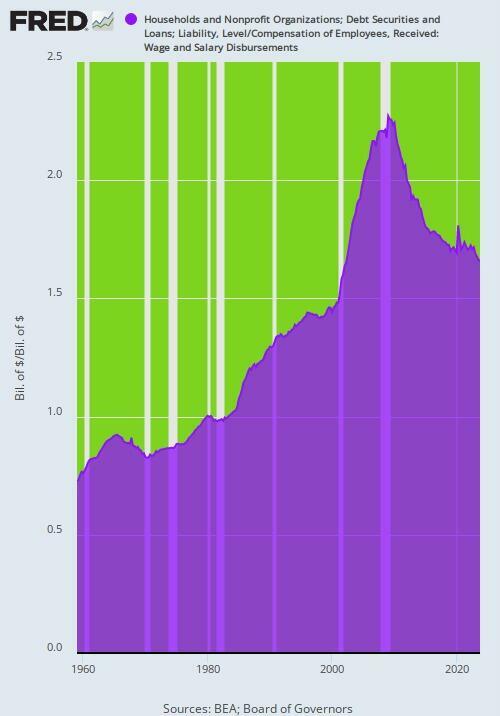

In fact, the only way that easy money causes households to spend more than the growth rate of their incomes is if they steadily increase their debt-to-income or leverage ratio. That generates incremental borrowings, which in turn can supplement spending derived from current period income.

And that’s exactly what happened in the half-century leading up to the great financial crisis. The household debt-to-income (wage and salary basis) ratio posted at 70% in 1960, but vaulted skyward thereafter, especially after Greenspan opened the spigots at the Fed after 1987. By Q1 2009 that household leverage ratio stood at 227% (purple area), and it was that massive increase in leverage which goosed household spending during this interval of time.

No more. Since Q1 2009 the household sector has been slowly but steadily deleveraging, with the ratio now down to 166% as of Q4 2023. What that means is that the Fed’s magic “stimulus” elixir simply doesn’t work any more in the household sector. It gooses organic spending not one whit.

Explosion of Household Debt Leverage During 1960 to 2009 and Deleveraging Since Then

As to the supply-side growth canard, it cannot be gainsaid that the amount of monetary stimulus has been off the charts relative to all prior history. In fact, the Fed’s balance sheet at @ $7.5 trillion is still more than 8X its pre-crisis level in Q4 2007.

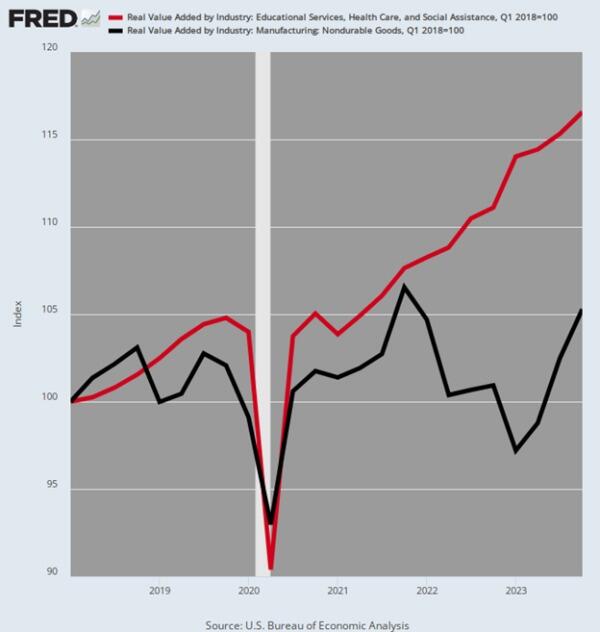

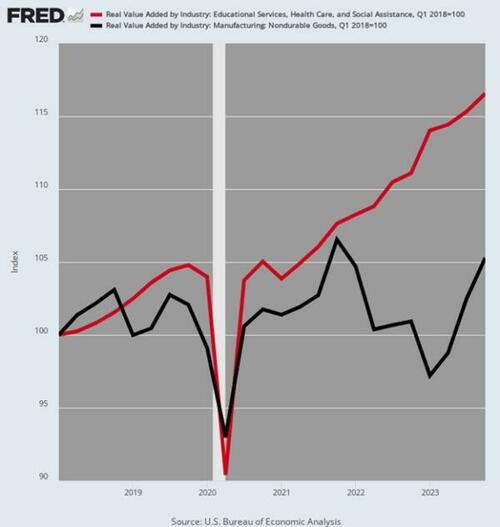

Yet when it comes to real growth of value-added production during the six year period from Q1 2018 to Q4 2023, the chart below tells you all you need to know. To wit, real value added output in the health care, education and social services sector grew at a 2.71% per annum rate, which was 3X the 0.90% real growth rate of the nondurable goods production sector.

Self-evidently, the former sector does not need easy money or ultra-low interest rates to grow. Demand in the health, education and social services sector is overwhelmingly financed by government fiscal transfers, including the massive subsidies implicit in the medical care deductions and preferences of the IRS code.

Indeed, the red line in the chart below represented the fastest growing sector of the US economy by far during that six year period, but we’d dare say none of those gains depended upon low interest rates. The sector’s munificent funding actually flows from statutory entitlements and long-standing tax code provisions, which generate essentially the same level of demand and sector output whether the Federal funds rate is 1% or 7%.

At the same time, it is highly unlikely that a return to low rates will do much for the moribund growth rates in the industrial economy, as represented here by real-value added in the nondurable goods industries. Long ago, much of US production of shoes, shirts, sheets, household supplies and the like was off-shored to lower cost venues abroad. And locking in the current inflated domestic costs levels plus another 2-3% per year going forward will not bring them back.

In sum, the Fed’s fiddling with interest rates is largely irrelevant to the supply-side path of the two industries shown below, and countless more just like them.

Real Value Added: Education, Health Care and Social Assistance Sector Versus Durable Goods, 2018 to 2023

Finally, it is tantamount to laughable to claim that the Fed needs to revert to the rate cutting modality in order to stabilize the financial markets and main street economy and to compensate for the purported inherent volatility of the free market.

Oh, puleese!

Every one of the main street recessions and financial market crises of the past six decades has been caused by the state and the machinations of its central banking branch. The very idea that there is an implicit third mandate called “financial stability” (after inflation control and full employment) is risible. It puts you in mind of the young man who killed both parents and then threw himself upon the mercy of the court on the grounds that he was an orphan!

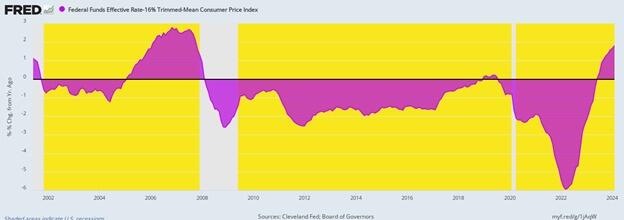

At the end of the day, sharply cutting rates any time this year or for some time to come thereafter would amount to a financial crime. After just a short stay of approximately eight months barely in positive territory (purple area) since July 2023, inflation-adjusted or real rates would be back below the zero bound, where they have destructively dwelled for much of the last several decades, as the chart makes crystal clear.

Inflation-Adjusted Federal Funds Rate, 2001 to 2024

Of course, that development would be heartily welcomed by Wall Street speculators and the Washington war-mongers and spenders alike. And that’s exactly the reason it should not be done.

* * *

The truth is, we’re on the cusp of an economic crisis that could eclipse anything we’ve seen before. And most people won’t be prepared for what’s coming. That’s exactly why bestselling author Doug Casey and his team just released a free report with all the details on how to survive an economic collapse. Click here to download the PDF now.