Futures Fade Despite Continued Tech Meltup, Japanese Yen Craters

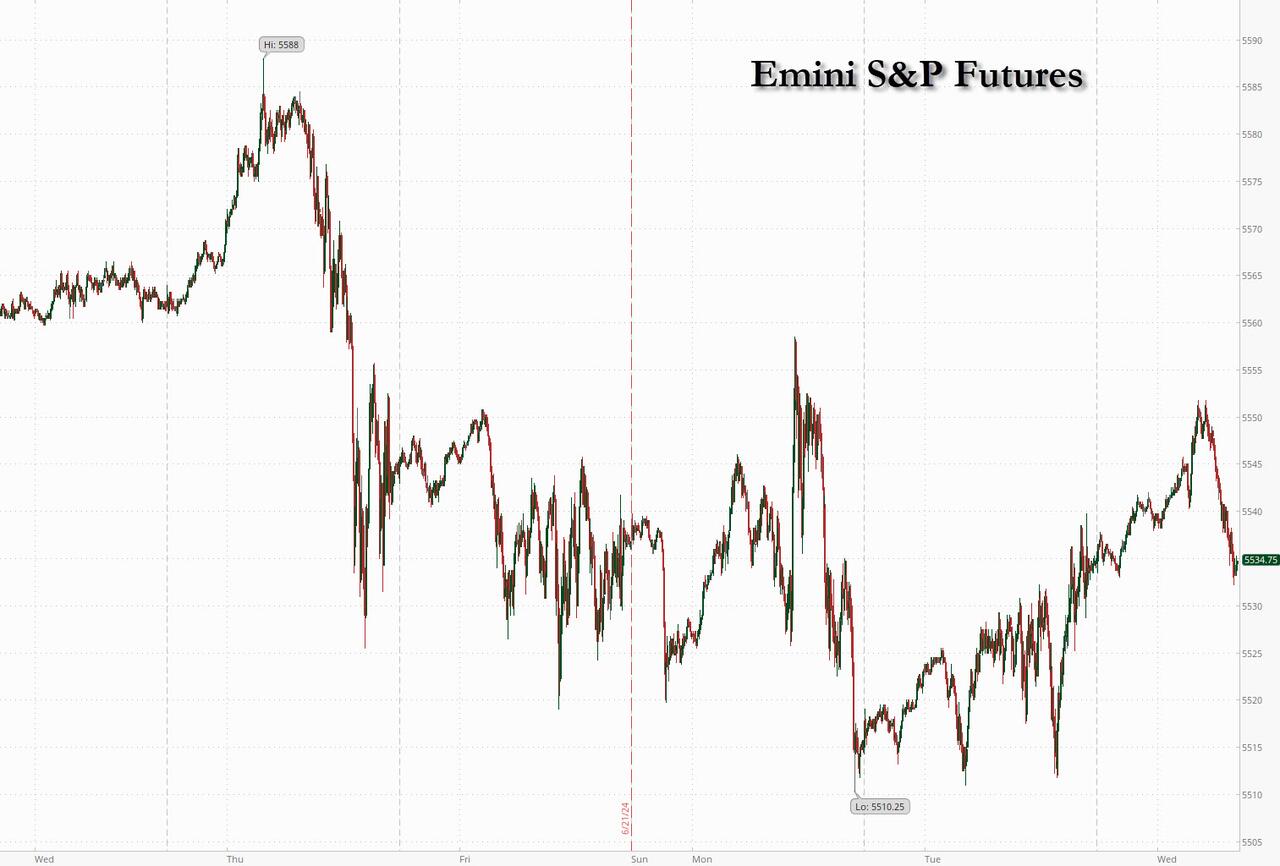

Futures are trading modestly in the red near sessions lows, erasing earlier gains of as much as 0.2% even as gigacap tech stocks continue their meltup. At 8:00am ET, S&P futures were down 0.1%, while Nasdaq futures were still green, rising 0.1% but also fading their earlier gains in another quiet start to the day (volumes this week have been tracking down 10-15% vs 10dma), with the snapback in momentum yesterday looking to continue its rally this am (NVDA +2% in premarket). Bond yields are 2-4bp higher after Fed Governor Michelle Bowman reiterated her view that borrowing costs should remain elevated for some time; USD is higher as the yen plunges below 160 vs the USD, the lowest since 1986 with another BOJ intervention now imminent. Commodities are mixed: oil and Ags are higher, while base metals are lower. Today, the key macro focus will be on MBA Mortgage Applications (up 0.8%), New Home Sales (10am, est 633k), $70bn UST 5yr note auction, Fed will release bank stress test results after the close today; Micron, Jefferies and General Mills are among companies reporting results.

Pre-mkt, Tech/Semis are continuing yesterday’s rally: Nvidia climbed more than 2% in US premarket trading, adding to Tuesday’s 7% gain. Rival Micron Technology Inc. rose more than 3% ahead of its third-quarter results later Wednesday (WTD +4.3%). Other tech names rising are QCOM +70bp, AMZN +65bp, AAPL +32bp. Here are the most notable premarket movers:

- FDX +14% pre mkt after company reported EPS upside thanks to higher op. margins and the F25 EPS outlook mid-point is slightly above plan ($21 vs. the Street $20.85). Iin addition to earnings, mgmt. outlined a plan to repurchase $2.5B in shares this FY (including $1B in FQ1) and suggested the FedEx Freight unit could be sold (the potential for a FedEx Freight sale is the key driver of the stock rally).

- Rivian Automotive shares soared 38% after Volkswagen said it plans to establish a joint venture and invest up to $5 billion until 2026 in the electric-car maker. Analysts were positive about the investment and noted that the JV is a vote of confidence for Rivian’s business. VW shares slipped.

- Aptiv shares fell 5.7% as Piper Sandler downgraded to underweight from neutral, saying that the Volkswagen-Rivian JV strikes at the core of the auto parts company’s strategy.

- Southwest Airlines shares drop as much as 10% in premarket trading after the US carrier cut its guidance for operating revenue per available seat mile for the second quarter.

- Whirlpool shares surge as much as 20% in premarket trading after Reuters reported that Robert Bosch GmbH is considering an offer for the appliance maker.

- General Mills shares fall 4.1% in premarket trading after the packaged-food company’s full-year forecast for organic net sales growth missed the average analyst estimate. The cereal maker also reported a steeper-than-expected decline in organic net sales for the fourth quarter.

- Tesla is on the verge of losing a key bragging right it’s held for the past six years: outselling all EV competitors in the US combined.

- Home Depot shares gain 0.5% in premarket trading after D.A. Davidson & Co. raised the home-improvement retailer to buy from neutral, saying a return to positive comparable sales “is in sight” with industry trends no longer getting worse.

- Grindr shares jump 5.9% in premarket trading after Dow Jones reported that the LGBTQ company raised its revenue growth forecast for the year ahead of an investor day.

- Cruise operator Carnival Corp. gained after posting a surprise quarterly profit and raising its earnings outlook.

The volatility in Nvidia shares, which account for one third of the S&P’s advance this year, has raised renewed concern about the concentration of megacap technology stocks in equity indexes.

yes, yes, another concentration chart pic.twitter.com/wr4IpiDn5z

— zerohedge (@zerohedge) June 26, 2024

“Nvidia’s volatility has weighed on market sentiment, but we think the structural investment case for artificial intelligence remains intact,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “We also hold a constructive outlook for broader equities amid solid fundamentals.”

Among other premarket movers, FedEx Corp. surged more than 13% after an upbeat profit forecast. Cruise operator Carnival Corp. gained after posting a surprise quarterly profit and raising its earnings outlook. Southwest Airlines Co. fell as much as 6.7% after cutting guidance.

Fed officials recently forecast just 25 basis points of reductions by the end of this year and a total of 125 basis points by end-2025, while market participants are pricing in about 75 basis points by the first quarter of 2025. But some are starting to hedge against deeper and more rapid easing: positioning in the rate options market shows an increase in bets that stand to benefit if the Fed reduces its key rate to as low as 2.25% over the next nine months — a whopping 3 percentage points of cuts.

The Stoxx Europe 600 index reversed an early advance and slipped 0.4% as declines for car makers and travel and leisure stocks offset gains in the tech sector. Among individual movers in Europe, Danske Bank A/S rose as much as 2.4% after lifting its full-year outlook. Just Eat Takeaway.com NV and Delivery Hero SE fell as much as 4% each after JPMorgan forecast tepid growth for the food delivery sector. Here are the most notable European movers:

- Mail delivery stocks climb on Wednesday after US firm FedEx issued a profit forecast above Wall Street’s expectations.

- Deliveroo shares rise after Reuters reported that US food delivery firm DoorDash approached the company for takeover talks. European food delivery peers waive early gains.

- Sanofi shares rise as much as 2% after Bloomberg reported that the French pharmaceutical giant has called for initial bids for its $20 billion consumer health division ahead of a potential listing.

- Danske Bank shares gain as much as 2.4% after raising its outlook for the full year, citing the strong quality of loans it has issued.

- Philips shares rise as much as 3.3% after Italy’s billionaire Agnelli family raised its holding in the Dutch medical device manufacturer, giving it a stake worth $4.19 billion.

- Future shares gain as much as 8.1% after Jefferies double upgrades to buy, removing the media company’s only negative analyst rating, on renewed confidence over a strong return of revenue growth.

- Fincantieri shares gain as much as 8% in Milan trading, rebounding from a 9.3% drop on Tuesday, after the Italian shipbuilder launched a €400m capital increase earlier this week.

- D’Amico shares advance as much as 8.1% as Pareto adds to the clean sweep of positive ratings, starting coverage with a buy rating as notes strong re-pricing potential for the stock.

- PTWP shares rise as much as 9.2% on their first day of trading on the Warsaw Stock Exchange’s main market, after the application software firm moved its listing from the NewConnect platform for smaller companies.

- Phoenix Group shares slip as much as 1% after the UK insurer said it would explore the sale of its SunLife business.

- Volex shares slump as much as 9.3%, the most since August 2022, after the producer of interconnectors and power products reported full year results.

- Alfen shares fall as much as 43%, the most on record, after the Dutch energy infrastructure firm cuts its revenue forecast and said it expects its Ebitda margin to be mid-single digit for the full year.

In the absence of major data from the euro zone on Wednesday, traders are taking their cues from policy signals. Investor expectations for the European Central Bank to loosen monetary policy twice more this year are fair, according to Governing Council member Olli Rehn, who added that officials shouldn’t overly dampen economic activity.

Earlier, in Asia equities advanced for a second day as tech shares rebounded after Nvidia drove a rally in US peers. The MSCI Asia Pacific Index rose as much as 0.4%, with TSMC and SK Hynix among the biggest boosts. A gauge of the region’s tech shares advanced after a three-day decline. Benchmarks gained in Japan, South Korea and mainland China. Australian stocks slid as a hotter-than-expected inflation data print bolstered the case for the Reserve Bank to resume raising interest rates.

Wall Street’s tech rally overnight helped lift chip-related stocks in the region, though any bullish sentiment may be contained as uncertainties remain on the Federal Reserve’s monetary policy path. Investors are watching the central bank’s preferred inflation gauge due Friday for more clues on its path to easing. China’s 10-year bond yield fell to a more than two-decade low as investors flocked to fixed-income securities amid concern about the slowing economy and expectations for further stimulus.

In FX, it was all about the continued disintegration of the yen, which breached 160 per dollar, a level that triggered a sharp reversal on April 29 due to suspected intervention, raising speculation Japanese authorities may take steps to support the currency again. As of 8:00am, the USDJPY rose to 160.36, the lowest since 1986.

In rates, treasuries are cheaper across the curve on Wednesday, holding on to losses seen during Asian trading hours amid a selloff in Australian government bonds after the country’s May inflation reading beat estimates, raising the odds that the Reserve Bank will resume raising interest rates at its next meeting. US yields are cheaper by 2.5bp to 3.5bp across the curve, with the front and belly of the curve broadly leading losses on the day. US 10-year yields trade at around 4.28%, cheaper by 3bp on the day with bunds and gilts trading broadly in line. Aussie 2-year notes climbed 18bp following CPI data. Treasury coupon issuance resumes at 1pm New York time with $70 billion in 5-year notes, which follows a 2-year sale on Tuesday which stopped on the screws. This week’s auctions conclude Thursday with $44 billion in 7-year notes. The WI 5-year yield at around 4.305% is ~25bp richer than May’s stop-out, which tailed the WI by 1.3bp

In commodities, oil rose ahead of a US government report on crude inventories and fuel demand following the release of mixed industry data. Iron ore climbed for a second day. Copper fell to the lowest in more than two months with prices facing sustained pressure from unusually weak Chinese demand. Gold was little changed. Bitcoin softer but essentially consolidating at the top-end of Tuesday’s range which itself was a consolidation of Monday’s marked Mt. Gox/technical inspired downside; at a base of USD 61.4k

The US economic data slate includes May new home sales at 10am. There are no Fed officials scheduled to speak for the session. The focus for the US session also includes a 5-year note auction, which follows solid demand for Tuesday’s 2-year sale.

Market Snapshot

- S&P 500 futures up 0.2% to 5,549.25

- STOXX Europe 600 up 0.5% to 520.12

- MXAP up 0.3% to 180.97

- MXAPJ up 0.2% to 568.06

- Nikkei up 1.3% to 39,667.07

- Topix up 0.6% to 2,802.95

- Hang Seng Index little changed at 18,089.93

- Shanghai Composite up 0.8% to 2,972.53

- Sensex up 0.7% to 78,604.07

- Australia S&P/ASX 200 down 0.7% to 7,783.01

- Kospi up 0.6% to 2,792.05

- German 10Y yield +2bps at 2.43%

- Euro down 0.2% to $1.0696

- Brent Futures up 0.1% to $85.12/bbl

- Gold spot down 0.2% to $2,315.93

- US Dollar Index up 0.18% to 105.79

Top Overnight Stories

- China’s benchmark bond yields fell to a more than two decade low, even as economists raised growth forecasts on export optimism. But adding to signs of slowing activity, vacancies are climbing at warehouses, souring global investors’ $100 billion bet. BBG

- A rare unscheduled revision to Japan’s first-quarter gross domestic product (GDP) may lead to a sharp downgrade, possibly affecting the central bank’s growth forecasts and the timing of its next interest rate hike, some analysts say. RTRS

- Rivian shares jumped 37% in premarket trading after Volkswagen agreed to invest $5 billion in a joint venture, providing a much-needed cash infusion. VW shares slipped. BBG

- Australia’s CPI came in ahead of expectations in May (+4% vs. the Street’s +3.8% forecast), which means the RBA could be forced to hike rates further in Aug. WSJ

- Switzerland dealt a surprise hit to UBS after opting to proceed with scheduling Basel III bank capital rules in January, despite wrangles over them in the US. UBS had urged the government to delay part of the rules that relate to banks’ trading books. BBG

- The ECB’s Olli Rehn said market expectations for two more cuts this year — and taking the deposit rate to as low as 2.25% in 2025 — were “reasonable,” in some of the most explicit remarks yet on the rate path from a policymaker. BBG

- US companies have been able to reprice almost $400bn of debt at lower interest rates this year due to booming investor appetite for junk loans, in an easing of financing conditions for corporate America. FT

- In New York’s 16th district, George Latimer defeated Rep. Jamaal Bowman in the most expensive congressional primary in US history. Bowman’s loss is a blow to liberals who’ve been trying to push the Democrats further left; he’s a member of the so-called “Squad” and has been critical of Israel. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks followed suit to the mixed performance stateside where the major indices reversed Monday’s price action and tech rebounded as Nvidia snapped its losing streak, while markets continue to await fresh catalysts. ASX 200 was pressured with sentiment not helped by a hot monthly CPI print which saw both Deutsche Bank and Morgan Stanley call for a 25bps hike at the next RBA meeting in August, Nikkei 225 outperforms following recent currency weakness and with tech names boosted after Nvidia’s rebound. Hang Seng and Shanghai Comp. were mixed with the former kept afloat above the 18,000 level, while the mainland was subdued despite another firm liquidity injection by the PBoC with sentiment clouded by tech and trade-related frictions as OpenAI was reportedly taking steps to block China access to its AI tools.

Top Asian News

- RBA Assistant Governor Kent said a range of measures shows that monetary policy is restrictive and policy is contributing to slower growth of demand and lower inflation, while he added that recent data reinforced the need to be vigilant to upside inflation risks and hence, they are not ruling anything in or out for interest rates.

European bourses higher across the board following the tech-led upside on Wall St.; Stoxx 600 +0.2%. Sectors mostly in the green, Tech leads while Autos lag amid pressure in Volkswagen after their investment in Rivian. Stateside, futures firmer but only modestly so, ES +0.2% & NQ +0.3% as we count down to Micron earnings after-hours; Fedex leading in the pre-market +13% post-earnings. DigiTimes reported that Nvidia (NVDA) CEO Jensen Huang was reportedly concerned about the company’s business development, with slow data centre expansion possibly impacting chip sales. Equity specifics between Volkswagen-Rivian & FedEx detailed below.

Top European News

- ECB’s Rehn said he sees bets for two more rate cuts this year as reasonable and the market’s terminal rate view of 2.25%-2.50% is also appropriate, while he sees the possibility for rate moves at any policy meeting and noted that rate cuts are contingent on additional disinflation. Rehn said he sees no disorderly market moves in France, as well as noted there is no debt crisis ahead and no need for TPI.

- ECB reportedly to begin the next strategic review once the summer break concludes, via Bloomberg; looking to present findings in H2-2025.

- Volkswagen (VOW3 GY) is to invest an initial USD 1bln in Rivian (RIVN), as part of a new, equally controlled JV to share EV architecture and software. The potential investment could rise to as much as USD 5bln by 2026 if certain milestones are achieved. The transaction could result in an unplanned cash outflow of up to EUR 2bln for Volkswagen in the current FY. Volkswagen expects FY24 net cash flow to range between EUR 2.5-4.5bln. Volkswagen will further its software-defined-vehicles plans via the JV, and transition to a pure zonal architecture. Each company will continue to separately operate their respective vehicle businesses. Rivian’s stock jumped higher by 50% in extended trading, adding around USD 6bln to its market cap. (Volkswagen).

- Switzerland is to implement Basel III trading rules as of January 1st 2025, according to Bloomberg; sees no reason to deviate from the Basel III timetable. Note, the EU has delayed it by one year to January 2026.

FX

- USD/JPY has breached 160.00 to the upside, for the first time since April 29th when it peaked at 160.20, a session which saw intervention and a large pullback in the pair; note, the breach of 160.00 this morning was accompanied by modest two-way action. Currently holding around a 160.06 session high.

- DXY continues to incrementally build on Tuesday’s advances to a current 105.86 peak but is yet to breach Monday’s 105.90 high, which essentially matches Friday’s 105.91 best.

- Action which is weighing on peers across the board; EUR/USD lost 1.07 to a 1.0686 base while Cable continues to slip from 1.27 and is approaching 12650.

- Aussie is the clear outperformer, bolstered by hot CPI which has increased the odds of a August hike to c. 33% (12% pre-release, AUD/USD to a 0.6688 peak; Kiwi softer and weighed on by the cross with NZD/USD just beneath Tuesday’s 0.6107 base.

Fixed Income

- Benchmarks in the red as the overall risk tone saps haven demand and amid a lack of fresh fundamental drivers for the complex, European docket focuses on a speech from ECB’s Lane.

- Bunds at the low-end of a 45 tick band that has seen it slip below Monday’s 132.22 base to a new WTD low, if this goes, support at 132.02 before the figure and then 131.61.

- OAT-Bund spread steady at 71bp with no fall out from an unsurprisingly fiery French election debate.

- Gilts in-fitting with only a modest uptick on the back of a robust 2038 auction, complex looks ahead to the last Sunak-Starmer debate before the election this evening.

- USTs also have a thin docket ahead with no Fed speak due and the main highlight being the 5yr auction, a tap which follows a better-than-average 2yr sale; USTs at a 110-09 fresh WTD base and holding just above last week’s 110-06+ low.

Commodities

- Initially contained trade with specifics quite light after the bearish inventory report has given way to a modest but growing bid for the crude benchmarks which are at the top-end of c. USD 1.0/bbl parameters.

- Action which comes despite a slight easing in the European risk tone (though still constructive overall) and an ongoing grind higher for the USD.

- Precious metals saw a contained start given the twin headwinds of a robust dollar and risk appetite. Yellow metal is at the low-end of a USD 2309-2323/oz band; one that sees it slip further from its 10-, 21- & 50-DMAs.

- Base metals tracking the tone but the gains capped by the dollar, overall the complex is firmer, it is yet to break the downward trend that has been in place for the likes of copper since end-May.

- US Private Inventory Data (bbls): Crude +0.9mln (exp. -2.9mln), Distillate -1.2mln (exp. -0.3mln), Gasoline +3.8mln (exp. -1.0mln), Cushing -0.4mln.

- Trading Hub Europe’s Frank remarks that German gas caverns curently show comfortable filling levels; Europe has enough LNG terminal capacities and southbound transit capacities from the north-west have been boosted.

Geopolitics: Middle East

- US Defense Secretary Austin said Hezbollah’s ‘provocations’ threaten to drag Israeli and Lebanese people into war.

- Pentagon said US Secretary of Defense Austin discussed with his Israeli counterpart efforts to de-escalate tensions on the Israeli-Lebanese border, while he warned that a war between Israel and Hezbollah would be catastrophic for Lebanon, according to Asharq News.

Geopolitics: Other

- Ukrainian President Zelensky will attend Thursday’s European Union summit in Brussels where he is expected to sign an agreement on EU security commitments for Ukraine, according to the French President’s office cited by AFP.

- Russian Defence Minister Belousov warned US Defense Secretary Austin regarding the dangers of an escalation of continued US arms supplies to Ukraine, according to the Russian Ministry.

- North Korea launched a suspected ballistic missile which was believed to have fallen outside of Japan’s EEZ shortly after with no damage reported, while Yonhap later reported that North Korea’s missile launch was believed to have failed and South Korean military said the missile used by North Korea in its failed launch was potentially a hypersonic missile.

- South Korean marines are to conduct live fire drills, according to Dong-A.

- NATO allies select Mark Rutte as the next Secretary General.

US Event Calendar

- 07:00: June MBA Mortgage Applications, prior 0.9%

- 10:00: May New Home Sales MoM, est. -0.2%, prior -4.7%

- 10:00: May New Home Sales, est. 633,000, prior 634,000

DB’s Jim Reid concludes the overnight wrap

I can safely say that this is the first time I have written the EMR from a castle. It’s in the Frankfurt countryside and quite an incredible place. This morning you need to look out at the market from the highest possible watchtower as the last 24 hours have seen a lot of differing trends from all directions.

On the plus side, tech stocks posted a decent recovery, with Nvidia (+6.76%) rebounding from its slump over recent days. But on the more negative side, several data releases were underwhelming, and multiple headlines leant on the hawkish side, i ncluding an upside surprise in both Canadian and Australian CPI. Indeed, DB have overnight changed their RBA call to a hike in August. Moreover, political events have also remained in focus, with the CAC 40 (-0.58%) and other European indices losing ground ahead of France’s election on Sunday.

We’ll start with the good news, as there was finally a bounceback for tech stocks after three consecutive declines, which helped to lift US equities more broadly. In particular, Nvidia was the second best performer in the entire S&P 500, which pushed its market cap back above the $3tn mark again. Those gains were seen amongst all the big tech stocks, with all of the Magnificent 7 (+2.40%) advancing on the day. In turn, that helped the NASDAQ (+1.26%) post a strong rebound, and it also lifted the S&P 500 up +0.39%.

But unfortunately, the good news mostly ended there, as even though the headlines pointed to a recovery for US equities, the move was dominated by the big tech stocks. In fact, over 75% of the S&P 500 actually fell yesterday, and the equal-weighted S&P 500 was down by a significant -0.72%. So as it stands with just a few days of the quarter left, the S&P 500 is up +4.09% in Q2 so far, whereas the equal-weighted index is down -2.89%. So a different story depending on which part of the market you look at, and this builds on the tech outperformance we already saw in Q1.

Matters weren’t helped by several hawkish headlines, with sovereign bonds coming under pressure after Canada’s CPI report for May. That showed headline CPI unexpectedly rising to +2.9% (vs. +2.6% expected), and the two core inflation measures followed by the Bank of Canada also rose. As it happens, the Bank of Canada did announce an initial cut at their meeting earlier this month, but after the inflation report, investors swiftly moved to dial back the chance of a follow-up move in July. Indeed, overnight index swaps had been pricing a 61% chance of a July cut on the previous day, but that was down to 16% by the close. Canadian government bonds also lost ground, with the 10yr yield up +5.0bps.

The inflation surprise has continued in Australia overnight with the latest CPI reading seeing it surge to its highest level this year. It printed at +4.0% y/y in May, above market expectations for a +3.8% gain and up from +3.6% in April. Our Aussie economist now believes the RBA will hike 25bps in August. See his report justifying the call here. Following the CPI data, the Australian dollar has risen +0.44% to trade at 0.6676 versus the dolla r while yields on the policy sensitive 3yr government bonds are currently +16.8bps higher at 4.09%, its biggest one-day gain since April, while yields on the 10yr are +11.7bps, standing at 4.32% as I type.

US Treasuries are also edging up around +1.5bps across the board after the Aussie CPI print after rising yesterday on the Canadian CPI beat. By last night’s close, 2yr Treasury yields were up +1.7bps to 4.74%, and the 10yr yield was up +1.6bps to 4.25%. Treasury yields did come slightly off their intra-day high seen around the European close following a solid 2yr auction which saw the highest bid-to-cover ratio since September. There was also some hawkish Fedspeak though, with Governor Bowman warning that “we are still not yet at the point where it is appropriate to lower the policy rate.” In addition, she said that cutting rates “ too soon or too quickly could result in a rebound of inflation, requiring further future policy rate increases to return inflation to 2 percent over the longer run.” Meanwhile, Fed Governor Cook maintained patience on rate cut prospects, saying these will be appropriate “at some point”.

Back in Europe, risk assets struggled, with the STOXX 600 (-0.23%), the CAC 40 (-0.58%) and the DAX (-0.81%) all posting losses. However, the Franco-German 10yr spread did tighten a bit, coming down by -1.1bps to 76bps, and yields came down across the continent, including on 10yr bunds (-1.1bps). With regards to politics, last night saw the debate between three potential French PM candidates though there are no immediate signs that this will materially alter the election race. Polls continue to put Marine Le Pen’s National Rally party in the lead, and yesterday’s Ifop poll had the National Rally on 36%, the left-wing alliance on 28.5%, and President Macron’s centrist group on 21%.

Asian equity markets are again mixed this morning with the Nikkei (+1.41%) sharply higher and with the KOSPI (+0.23%) edging higher. On the other hand, the S&P/ASX 200 (-0.80%) is the worst performer following the CPI data discussed above. Elsewhere Chinese stocks are also losing ground with the Hang Seng (-0.16%), the CSI (-0.39%) and the Shanghai Composite (-0.36%) all lower in morning trade. S&P 500 (+0.05%) and NASDAQ 100 (+0.08%) futures are slightly higher.

Finally on the data yesterday, the Conference Board’s consumer confidence measure for the US fell back to 100.4 (vs. 100.0 expected). The FHFA’s house price index was also up by +0.2% in April (vs. +0.3% expected).

To the day ahead now, and data releases include US new home sales for May. From central banks, we’ll hear from the ECB’s Rehn, Panetta, Lane and Kazaks.

Tyler Durden

Wed, 06/26/2024 – 08:20

via ZeroHedge News https://ift.tt/MAtFfs5 Tyler Durden