Futures Rise Led By Small Caps As Great Rotation Continues

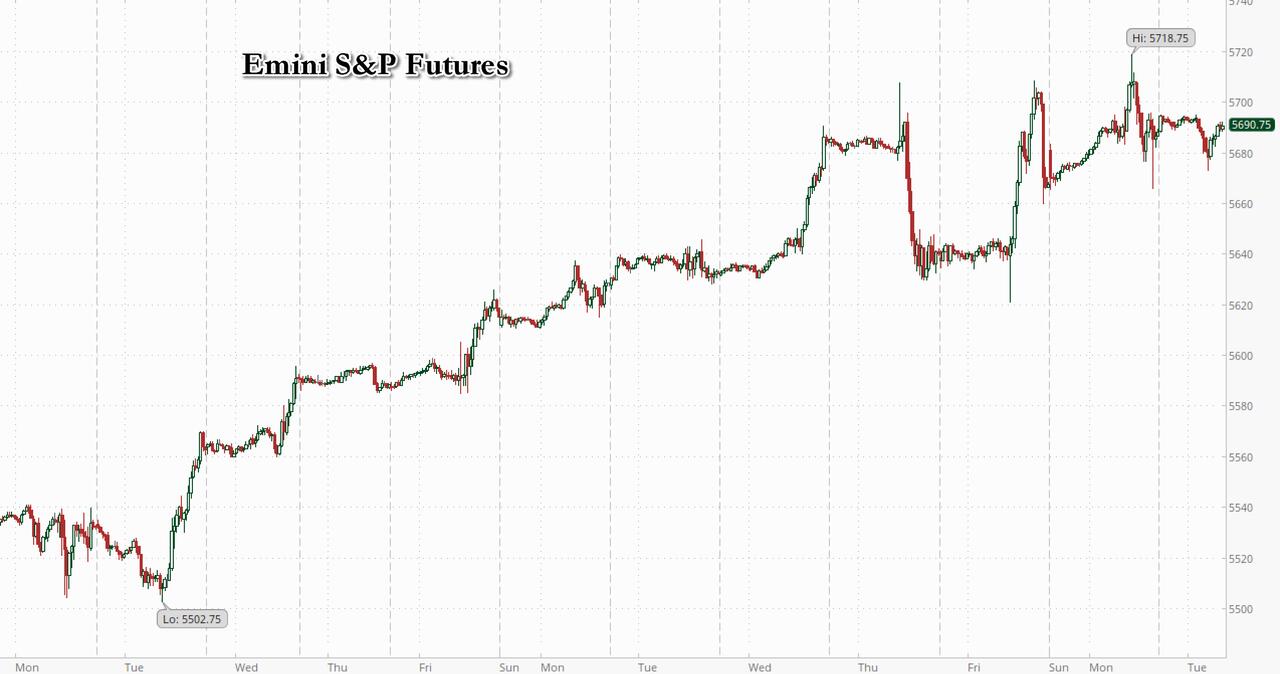

US equity futures are modestly higher, rebounding from session lows, and led by Russell futures as the rotation looks poised to continue as bond yields are lower with the curve bull flattening. As of 7:45am, S&P futures are 0.1% higher with Nasdaq futures rising 0.2%. Premarket, Mag7 is mixed with TSLA +1.7% the standout with Semis flattish. European stocks were red across the board, as China also traded lower after Trump’s selection of JD Vance – who said China represents the biggest threat to the US – as his VP, triggered further trade and geopolitical concerns in the region. FTSE -20bp/DAX -35bps/CAC -70bps/Shanghai +8bps/Hang Seng -1.6%/Nikkei +20bps/Kospi +18bps. Treasuries rose, pushing yields to their lowest since March, as expectations for a September rate cut rose: 10-year rates fell to as low as 4.17% while 2Y yields was at 4.41%. At the same time, the US Dollar is seeing some support, but the story is the BOJ and potential JPY intervention, though JPY is weaker. Commodities are weaker across all 3 complex with precious metals, natgas, and softs providing some support. Today’s macro data focus is on Retail Sales where the headline number likely is negative based upon lower gasoline prices but the Control Group is likely higher as the consumer spent on everything else.

In premarket trading, Bank of America rose more than 2% after the lender said it sees fourth-quarter net interest income on a fully taxable-equivalent basis of about $14.5 billion, ahead of analyst estimates for $14.33 billion. Morgan Stanley initially rose after reporting Q2 earnings but then slumped after the market focused on the bank’s Wealth Management revenue miss. Here are some other notable premarket movers:

- Chegg gains 7% as Morgan Stanley raises the stock to equal-weight, with analysts saying that the educational platform provider’s shares are pricing in a “challenged” path ahead.

- Match Group jumps 9% after Starboard Value built a stake in the dating-app company.

- Trump Media falls 9.6% after the owner of Truth Social registered 38 million shares that could be sold as part of a pact with Yorkville Advisors.

- Verizon Communications ticks 0.3% higher as the carrier explores selling thousands of mobile-phone towers across the country, according to people familiar with the matter.

- Palantir dropped -1.7% after it was cut to underperform at Mizuho Securities with a PT $22

Overnight news was quiet outside of headlines from the RNC (JD Vance said Trump would negotiate with Russia & Ukraine so American can focus on the real issue, which is China) and another weak consumer print out of Europe (Hugo Boss). German Zew Survey declined for the first time in a year.

Meanwhile, the great rotation continues: The small-cap Russell index is now +1% for four straight sessions (up ~7.8% in that time window) vs NDX -30bps over same 4 days. Reminder S&P 500 has set 37 record highs this year while RTY remains ~10.5% below ATH from Nov ’21. Traders now await US retail sales data later for fresh insights on whether inflation and growth have cooled enough to satisfy policymakers who are deliberating when it’s safe to begin bringing down interest rates. Fed Chair Jerome Powell said Monday that inflation is heading toward the central bank’s 2% goal on the basis of second-quarter economic data.

“While he was not saying, ‘right we have high confidence that inflation is under control,’ which would fire the starting gun, it’s enough to support market expectations of a couple of cuts for this year and then for more of the same into next year,” said Sunil Krishnan, head of multi asset funds at Aviva Investors.

As traders start to embrace the idea of three interest-rate cuts this year, starting in September, Treasuries have wiped out their 2024 losses. Strategists at UniCredit SpA have pencilled in that many rate cuts and recommend positioning for the yield curve to steepen. Steepener trades favor buying short dated notes and selling long bonds, and are getting a boost from speculation that fiscal expansion will drive up long-dated yields.

European stocks and US equity futures pared earlier gains as disappointing earnings weighed on risk sentiment. Estoxx 50 trades lower by 0.7% on the day with consumer discretionary and energy sectors underperforming; Miners, insurance and autos were the worst performing sectors in Europe.

- Ocado shares jump as much as 20% after the online grocer reported first-half results that analysts said should provide reassurance following a rough year for the stock. The rally followed a 10% drop on Monday after a double-downgrade from Bernstein.

- SEB shares rise as much as 4.3% to a record high after reporting results that Jefferies said showed “positive trends” and included a bigger-than-expected buyback. Citi said net interest income beat estimates and consensus estimates should rise.

- Fineco shares rose as much as 3.4% in Milan after Italian newspaper Il Sole 24 Ore mentioned it among target companies managing Italians’ savings that could have been studied by investment firms such as Bain, CVC and Advent.

- Richemont shares rise as much as 2.3%, recouping an initial slide, as its first-quarter sales met expectations, contrasting with disappointing results this week from luxury peers Swatch, Burberry and Hugo Boss. The resilience of Richemont’s jewelry division impressed analysts.

- Rio Tinto shares fell as much as 2.8% after the global miner warned that full-year copper output would be at the lower end of its guidance range.

- Salzgitter falls as much as 7.2% while SSAB drops 3.9% after JPMorgan puts both stocks on negative catalyst watch ahead of their upcoming second quarter results.

- DKSH shares rise as much as 9.1% after the company, which helps others with their expansion plans, delivered earnings above expectations in the first half.

- Wise shares rise as much as 5.2% after the UK financial-software developer reported volumes for the first quarter that beat the average analyst estimate.

- Hugo Boss shares slump as much as 11% after the German clothing producer lowered its full-year outlook, citing the impact on demand from “persistent macroeconomic and geopolitical challenges.”

- Scor drops as much as 30%, the most since 2002, after the French insurer issued a profit warning related to its life and health (L&H) insurance service result, while accelerating its annual reserving review.

- Swedbank shares slip as much as 1.9% after the Swedish lender missed expectations on the key net-interest-income (NII) metric, offsetting better-than-expected income from fees and trading, analysts say.

- Trustpilot shares drop as much as 9% after a holder sold shares in the online review platform at a discounted price of 220p.

- Shares in UK utilities fell, led by Severn Trent and United Utilities, after Ofwat’s announcement that it is opening enforcement cases into four more water and wastewater companies.

Earlier in the session, China traded lower as Trump’s selection of JD Vance as his running mate triggered further trade and geopolitical concerns in the region. New tariffs of 60% on all Chinese exports to the US would more than halve China’s annual growth rate, according to UBS Group AG, underscoring the risks for Beijing if Trump returns to the White House. Vance told Fox News that China is the biggest threat to the US.

Asian stocks declined for a third consecutive day, as Hong Kong shares extended losses amid weak economics cues and growing geopolitical worries. The MSCI Asia Pacific Index fell 0.3%, with Tencent and AIA Group among the biggest drags. Hong Kong-listed stocks slid for a second day after Chinese economic growth data came in below expectations. Prospects for a victory by Donald Trump in the US presidential election are seen having negative implications for Chinese stocks. That comes on top of the already shaky economic outlook amid a continued crisis in the Asian nation’s property market. Sectors to watch:

- Shares of South Korean construction firms including HDC Hyundai Development rise, extending their recent rally on interest rate cut bets, a recovery in Seoul real estate prices and expectations for overseas nuclear deals.

- Chinese robotaxi-linked stocks extend a rally as investors bet on brighter prospects for this sector on continuous policy support.

- Taiyo Yuden, Murata Manufacturing and TDK shares climb after Jefferies raised its price target on Japan’s electronics components makers on view they will benefit from AI-related demand.

- Shares of Apple suppliers advance in Asia as the tech giant surged to another record high after Morgan Stanley named the stock as its top pick.

- Shares of LG Energy Solution and other EV battery-related stocks extend losses in Asia after Donald Trump announced JD Vance as his running mate.

- Chinese environment equipment-related stocks rise as authorities plan to increase financial support for projects to reduce emissions at coal power plants.

In FX, Bloomberg dollar spot index was flat, erasing an earlier gain driven by speculation that Donald Trump is virtually assured to win the US presidential election. EUR and DKK were the strongest performers in G-10 FX, AUD and JPY lagged. The yen weakened against the dollar as local markets reopened, following a three-day weekend, with traders focusing on the monetary policy divergence between Japan and the US.

“The Trump trade that sees rising stocks, bond yields and dollar could continue in the short term as Trump’s chances of election win increase,” said Daisaku Ueno, chief foreign-exchange strategist at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo. “I’d expect Japan intervention to take place” when yen weakness accelerates due to Trump trade, he said. Traders added to bets the Federal Reserve will cut interest rates three times this year after Goldman Sachs Group Inc. said conditions were ripe for easing.

In rates, global bonds rallied as traders increased the odds of more cuts from the BOE and Fed by the end of 2024. Treasuries advanced with the curve flatter as Monday’s aggressive steepening move is slightly unwound. Similar gains seen across European rates as traders price in two quarter-point rate Bank of England cuts this year, following UK grocery price inflation data. US session focus includes retail sales data. Treasury yields richer on the day by up to 5bp across long-end of the curve with 2s10s spread flattening by 1bp; 10-year yields around 4.18% with bunds and gilts both lagging by around 1.5bp in the sector. Odds of three 25bps of Fed cuts by December were at 90%, while traders fully priced in the likelihood of two BOE 25bps cuts this year, swaps tied to meeting dates showed.

In commodities, WTI drifted 0.8% lower to near $81.25. Spot gold rose roughly $16 to ~$2,439/oz. Bitcoin fell to around $63,000.

Today’s US economic data slate includes July New York Fed services business index and June retail sales and import/export prices (8:30am), May business inventories and July NAHB housing market index (10am). Fed members scheduled to speak include Kugler at 2:45pm

Market Snapshot

- S&P 500 futures little changed at 5,678.25

- STOXX Europe 600 down 0.5% to 516.01

- MXAP down 0.3% to 187.02

- MXAPJ down 0.4% to 582.92

- Nikkei up 0.2% to 41,275.08

- Topix up 0.3% to 2,904.50

- Hang Seng Index down 1.6% to 17,727.98

- Shanghai Composite little changed at 2,976.30

- Sensex little changed at 80,717.27

- Australia S&P/ASX 200 down 0.2% to 7,999.32

- Kospi up 0.2% to 2,866.09

- German 10Y yield -3.5bps at 2.44%

- Euro little changed at $1.0900

- Brent Futures down 0.8% to $84.16/bbl

- Gold spot up 0.6% to $2,437.84

- US Dollar Index little changed at 104.28

Top Overnight News

- Fed’s Daly (voter) said confidence is growing that they are getting nearer to a sustainable pace of getting inflation to 2%, while she sees a policy adjustment over the coming term and said some normalisation of policy is a likely outcome. Furthermore, she said the US economy is slowing and inflation is lower but they are not there yet although they are nearer to the time of achieving their goals.

- US President Biden is reportedly on the brink of failing to win a key labour endorsement as leaders of the 1.3mln member Teamsters union consider backing no candidate at all in the presidential race, according to Reuters citing sources. It was later reported that Teamsters union president O’Brien said they are not beholden to any party.

- US Special Counsel spokesperson said the dismissal of the Trump documents case deviates from the uniform conclusion of all previous courts to have considered the issue that the Attorney General is statutorily authorised to appoint a Special Counsel, while the Justice Department authorised the Special Counsel to appeal the court’s order.

- BofA Fund Manager Survey: investors remain bullish, driven by expectations of Fed cuts and a soft landing. Global growth expectations: -27% (prev. -6%), largest drop since March 2022. Soft landing expected by 68%, 18% see no landing. 67% see no recession in the next 12-months. Long ‘Magnificent 7’ the most crowded trade by a ‘country mile’. 39% believe that monetary policy is too restrictive. Geopols has replaced higher inflation as the main tail risk.

- Former President Trump is reportedly ready to hold talks with Russian President Putin on resolving the Russia-Ukraine conflict without any intermediary, according to Tass

- Federal Reserve Chair Jerome Powell said second-quarter economic data has provided policymakers greater confidence that inflation is heading down to the central bank’s 2% goal, possibly paving the way for near-term interest-rate cuts.

- Major Silicon Valley investors hailed Donald Trump’s choice of Ohio senator and former venture capitalist JD Vance as his running mate, a move that puts the technology industry closer to center stage in Washington if the former president takes the White House in November.

- For months, as copper spiked to record levels and then fell back down again, one key question has bubbled up across the metals industry: What is China’s state grid operator up to?

- China’s twin-track economy is generating doom-and-gloom headlines about domestic woes one moment and growing fears around the world about the dominance of its manufacturers the next.

- New tariffs of 60% on all Chinese exports to the US would more than halve China’s annual growth rate, according to new research from UBS Group AG, underscoring the risks for Beijing if former President Donald Trump returns to the White House.

- French President Emmanuel Macron is about to set in motion the appointment of a caretaker government until negotiations to find a new prime minister bear fruit.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed amid a quiet calendar and after the choppy but positive performance stateside following the latest comments from Fed Chair Powell. ASX 200 traded marginally lower with weakness in mining stocks following Rio Tinto’s production update. Nikkei 225 gained on return from the holiday weekend with the upside helped by a weaker currency. Hang Seng and Shanghai Comp. were subdued with underperformance in the Hong Kong benchmark after it gapped beneath the psychologically key 18,000 level, while sentiment in the mainland was clouded amid the lingering risks of higher tariffs but with downside stemmed after the PBoC upped its liquidity efforts with a CNY 676bln injection through 7-day reverse repos.

Top Asian News

- BoJ accounts point to intervention of about JPY 2.1tln on July 12th, via Bloomberg.

European bourses, Stoxx 600 (-0.4%) are entirely in the red, having opened on the backfoot and continued to extend on losses as the morning progressed. Since then, indices have found support and traverse across worst levels. European sectors hold a strong negative bias; Basic Resources is the clear underperformer, dragged down by losses in the underlying metals complex as well as a poor production update from Rio Tinto (-2.2%). US Equity Futures (ES +0.1%, NQ U/C, RTY U/C) are flat/mixed, with the ES and NQ trading on either side of the unchanged mark, whilst the RTY outperforms. BlackRock Investment raises UK equities to Overweight from Neutral

Top European News

- ECB Bank Lending Survey Credit standards were broadly unchanged at tight levels in the second quarter of 2024. Banks reported a small net tightening of corporate credit standards and a moderate easing for mortgages. Loan demand continued to decline for firms, while recording the first increase for households since 2022. Credit standards for firms displayed some heterogeneity across economic sectors, tightening strongly in commercial real estate

FX

- Mixed performance for the USD vs. peers, performing best vs. JPY, AUD, NZD. Today’s focus will be on US retail sales, whereby a dovish release could prompt DXY to move onto a 103 handle vs current 104.28.

- EUR is steady vs. the USD after a brief incursion above the 1.09 mark to a 1.0902 high. German ZEW was mixed and failed to move the dial for the Single-currency.

- GBP is steady vs. the USD with 1.30 seemingly currently too tough a nut to crack for Cable. The pair got as high as 1.2995 yesterday before running out of steam.

- USD attempting to claw back some lost ground vs. the JPY after last week’s US CPI, dovish Powell and Japanese intervention sent the pair markedly lower. 158.78 is the high watermark for today’s session but is still a far cry from the July multi-decade high at 161.95

- Antipodeans are both suffering at the hands of the USD with commodity currencies seeing a soft start to the week post-Chinese data over the weekend.

Fixed Income

- USTs are firmer and holding near highs of 111-10+, as Powell’s inflation language serves to weigh on short-term yields, alongside an ongoing pullback in crude; action which is also being seen at the long end of the curve which is currently underperforming and the curve as a whole is flattening.

- Bunds are firmer in-fitting with USTs, eclipsing last week’s 132.08 best to a 132.31 peak which now looks to a cluster between 132.56-80 from the 20th-26th June. The latest ECB Bank Lending Survey passed without reaction while the mixed ZEW pushed Bunds away from best levels.

- Gilts remains focussed on upcoming events which commence with CPI and the King’s Speech on Wednesday. DMO outing was robust and spurred an incremental fresh high of 98.62.

- OAT-Bund 10yr yield spread remains steady at 64bps ahead of today’s political risk event whereby President Macron should accept and allow PM Attal to resign, but it remains to be seen exactly who will be appointed as a caretaker.

- UK sells GBP 2.25bln 4.75% 2043 Gilt: b/c 3.29x (prev. 3.67x), average yield 4.519% (prev. 4.580%) & 0.1bps (prev. 0.4bps)

- Germany sells EUR 3.261bln vs exp. EUR 4bln 2.50% 2029 Bobl: b/c 2.0x, average yield 2.39%, retention 18.48%

Commodities

- A subdued session for the crude complex thus far despite the lack of fresh fundamentals, but as the Dollar remains firm and amid the ongoing woes surrounding Chinese demand following several downbeat data releases. Brent September resides near the trough of a USD 84.15-84.86/bbl parameter.

- Mixed trade across the precious metals despite quiet newsflow in the European morning, with spot gold the outperformer amid increased momentum as the yellow metal approaches ATHs. Spot gold probes yesterday’s peak (USD 2,439.59/oz) as it eyes its current ATH at USD 2,449.89/oz.

- Base metals are mostly lower with the complex dampened by the prognosis of the Chinese economy following the recent string of disappointing data, whilst some also flag rising inventory as warehouses.

- Freeport LNG expects to restart the first LNG train this week after damage from Hurricane Beryl and plans to restart the remaining two LNG trains shortly after the first one.

- Bolivia’s President announced the discovery of a 1.7tln cubic feet natural gas reserve in the north of the department of La Paz.

- Some Japaense aluminium purchasers have agreed on a July-September premium of USD 172/T, +16-19% Q/Q, via Reuters citing sources

Geopolitics

- North Korea warned that South Korea will face devastating consequences over anti-North Korea leaflets, according to KCNA.

US Event Calendar

- 08:30: June Retail Sales Advance MoM, est. -0.3%, prior 0.1%

- June Retail Sales Ex Auto MoM, est. 0.1%, prior -0.1%

- June Retail Sales Control Group, est. 0.2%, prior 0.4%

- 08:30: June Import Price Index MoM, est. -0.2%, prior -0.4%

- June Import Price Index YoY, est. 1.0%, prior 1.1%

- June Export Price Index MoM, est. -0.1%, prior -0.6%

- June Export Price Index YoY, est. 1.0%, prior 0.6%

- 10:00: May Business Inventories, est. 0.5%, prior 0.3%

- 10:00: July NAHB Housing Market Index, est. 43, prior 43

DB’s Jim Reid concludes the overnight wrap

I spent a day at a Theme Park yesterday in the driving rain. The good news was that there was hardly any queues for any of the rides given the weather. The bad news was…… …. there wasn’t any queues for any of the rides.

While I was loop the looping, politics dominated most of the session yesterday with markets trying to price potential Trump presidential trades after the weekend developments with a steeper Treasury curve the key theme in the rates space. Equities saw a clear rotation into stocks that stand to benefit from Trump’s policies and closed (+0.28%) less than a tenth of a percent below last week’s record high, whilst the small-cap Russell 2000 (+1.80%) surged to a two-and-a-half year high as well.

The other major story of the day was Fed Chair Powell’s interview at the Economic Club of Washington DC. Powell’s initial comments noted that “ the three readings in the second quarter… do add somewhat to confidence” that inflation is returning to the 2% target, and that the inflation and labour market mandates are now “in much better balance”. However, he did not get drawn on the timing of rate cuts and commented that policy is “restrictive but not severely restrictive”. The pricing of Fed cuts for rest of the year rose by +3.7bps on the day to 67bps, the highest since early April, but the move came largely outside of Powell’s comments.

In terms of Treasuries, the 2yr yield was marginally (+0.7bps) higher on the day at 4.46%, having traded as low as 4.42% during Powell’s initial comments. By contrast, the 10yr yield (+4.6bps to 4.23%), and the 30yr yield (+6.1bps to 4.46%) saw sizeable increases. At one point intraday, we even saw the 2s30s yield curve un-invert for the first time since January, although it was just about negative at -0.2bps by the close. Similarly, the 2s10s curve steepened by +4.1bps to -23.0bps, which is the least inverted it’s been since January. This morning in Asia, 10yr UST yields (-1.9bps) have moved back down, trading at 4.21% as we go to print with a similar move at the front end. Next stop an important US retail sales print today.

A Trump-driven shift in market pricing was also apparent for equities. For instance, Trump’s own media company, Trump Media & Technology Group, surged by +31.37%. Another beneficiary were private prison groups, with GEO Group (+9.35%) and CoreCivic (+8.02%) both experiencing their strongest daily performances for over a year. With Trump seen as a more pro-crypto candidate, Bitcoin (+5.57%) moved back up to $63,469, and Coinbase (+11.39%) had its best performance since March. In the meantime, the best-performing sectors in the S&P 500 were energy stocks (+1.56%) followed by financials (+1.42%).

But whilst many assets benefited from the prospect of a Trump presidency, there were also clear points of weakness. For instance, solar energy firms lost ground given the view they’d fare better under a Democratic administration, including decent losses for Sunrun (-8.95%), SolarEdge Technologies (-15.36%) and SunPower (-7.06%). The broader utilities sector (-2.39%) was the main underperformer within the S&P 500. Elsewhere, there was a significant underperformance for Mexican assets, with the Mexican Peso down by -0.96% against the US Dollar, making it one of the worst-performing global currencies yesterday. Moreover, Mexico’s equity index, the S&P/BMV IPC (-1.11%) fell back, with the decline being even larger in USD terms.

In terms of the politics itself, yesterday saw Trump confirm that his running mate on the ticket would be J.D. Vance, the Senator from Ohio. At 39, Vance is the second youngest member of the current Senate and the pick is seen as embracing the Trump campaign’s populist leanings. Vance’s notable policy comments this year have included criticism of the Biden administration on border control and on military aid to Ukraine . We’ll have to wait for some polls to get a better sense of how public opinion has shifted after recent events, but from betting and prediction markets, there’s no doubt that a Trump victory is now viewed as more likely. For instance, the average betting odds from RealClearPolitics now give Trump a 66% chance of victory, up from around 55% on Friday. One thing to bear in mind is that it’s fairly common for the party with a convention to experience a “convention bounce” in the polls as it becomes the focus of media attention. But this time, it could be more difficult to disentangle the effect of the convention if public opinion has also shifted as a result of the assassination attempt.

Over in Europe, markets followed a completely different pattern to the US, with equities sliding alongside a rally in sovereign bonds. That meant the STOXX 600 (-1.02%) posted its worst daily performance in the last month, although the backdrop was already a tough one given the weaker-than-expected Chinese GDP data before the open. Those declines were echoed across the continent, and the CAC 40 (-1.19%) underperformed given the implications for luxury stocks. Meanwhile for bonds, there was a clear risk-off move, which left yields on 10yr bunds (-2.3bps), OATs (-4.0bps) and BTPs (-4.6bps) all lower on the day.

In Asia, China risk continues to be mixed to weaker but the rest of the region is largely higher. The Nikkei (+0.23%) is up as it has resumed trading after a public holiday with the CSI (+0.19%) and the KOSPI (+0.25%) also edging higher. Meanwhile, the Hang Seng (-1.38%) is sharply lower with the Shanghai Composite (-0.21%) also trading down. S&P 500 (+0.19%) and NASDAQ 100 (+0.30%) futures are higher.

In FX, the J apanese yen (-0.36%) is extending its losses for the second consecutive day trading at 158.64 against the dollar despite last week’s suspected intervention by Japanese authorities.

There was very little other data yesterday, although Euro Area industrial production was down -0.6% in May (vs. -0.7% expected). Elsewhere, the New York Fed’s Empire State manufacturing survey fell to -6.6 (vs. -7.6 expected).

To the day ahead now, and data releases include the German ZEW survey for July, US retail sales for June, the NAHB’s housing market index for July, and Canada’s CPI for June. From central banks, we’ll hear from the ECB’s Villeroy and the Fed’s Kugler, and also get the Euro Area Bank Lending Survey from the ECB. Finally, earnings releases include Morgan Stanley and Bank of America.

Tyler Durden

Tue, 07/16/2024 – 08:16

via ZeroHedge News https://ift.tt/njkVMau Tyler Durden