Man Runs Over 80-Year-Old Planting Trump Sign In Yard, Then Kills Himself

An 80-year-old man who was placing a Trump sign in a residential yard has life-threatening injuries after being run over by a 22-year-old on an anti-Trump rampage in Michigan’s Upper Peninsula. The assailant later confessed to the crime via a phone call with police, only to kill himself before officers arrived to arrest him.

This latest display of ugly leftist political violence took place at 5:45pm Sunday in Hancock, Michigan, a town of 4,500 located on the Keweenaw Peninsula. Police say the victim was placing Trump campaign signs in his yard when a man riding an ATV accosted him with obscenities and yanked the signs out of the ground. When the resolute octogenarian attempted to re-set the signs, the attacker drove back into the yard, and accelerated before running him over from behind and fleeing the scene.

The victim was left in critical condition. “We’re not sure what could happen. Could he die from these injuries? Possible,” said Hancock Police Chief Tami Sleeman. Daily Wire reports that his injuries include a “brain bleed.”

On Monday, Hancock police received a message from someone saying they wanted to “confess [to] a crime involving an ATV driver within the last 24 hours.” The person provided an address and instructed police to “send someone to pick me up.” When cops arrived, they found a young man dead from a self-inflicted gunshot wound. At the same location, they found a four-wheeler and clothing that matched what was observed during the cruel attack.

While they have yet to release the name of the dead suspect, police say the assault-via-ATV was part of a broader spree of vandalism targeting Trump signage, along with property adorned with stickers and flags supporting law enforcement. Two of the incidents involved vandalism to vehicles.

Sleeman told the New York Times that the suspect used a shovel to smash the windows of a parked truck that had a Trump sticker, and performed an unspecified act of vandalism against the tires of a vehicle with a pro-cop message. In 2020, Trump won Houghton County — where Hancock is located — by a 56% to 42% margin.

This latest savage political violence came 8 days after Trump was nearly assassinated in Butler, Pennsylvania — while a spectator was killed and two others critically wounded. A Kamala Harris campaign spokesperson decried the Michigan incident, telling the Times that “politically motivated violence is always unacceptable and we unequivocally condemn it.”

A screenshot from a campaign video in which Harris says, “Donald Trump is an existential threat to our democracy and our most fundamental freedoms”

Of course, consistent with Harris’s own messaging, we’re guessing that same unidentified spokesperson routinely declares that Trump represents an existential threat to American democracy and that he and his supporters must be stopped before it’s too late.

Just don’t forget…regardless of the bloodshed in Pennsylvania and Michigan in the last two weeks…it’s the right-wing that’s really dangerous!

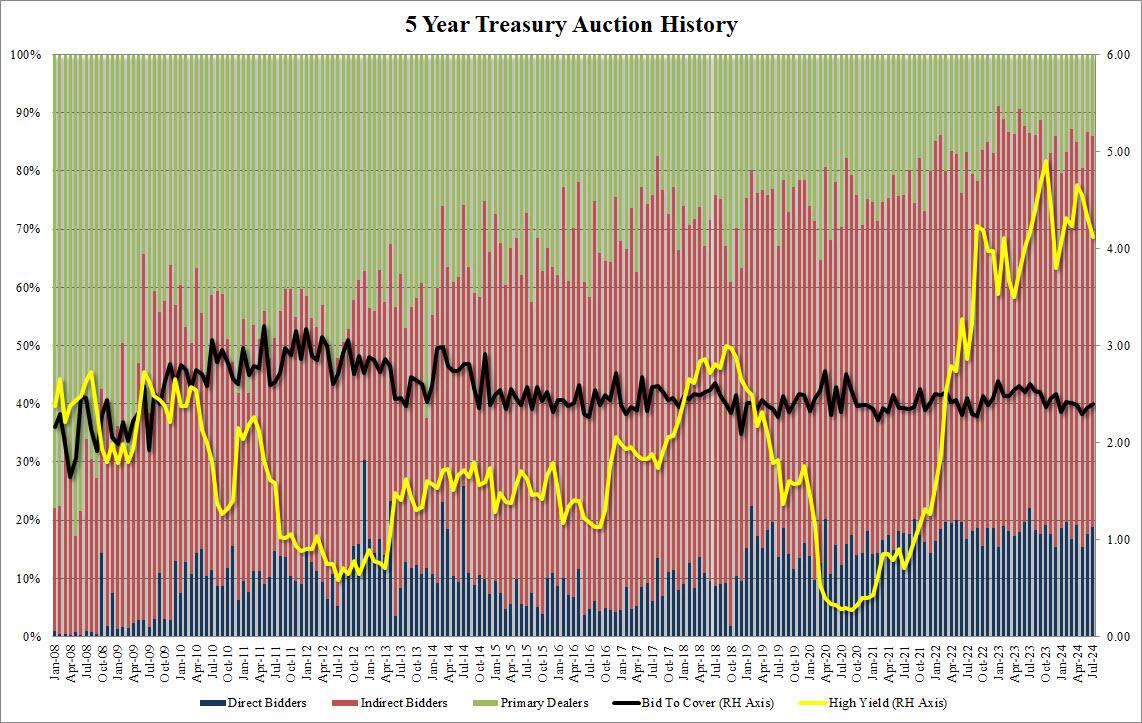

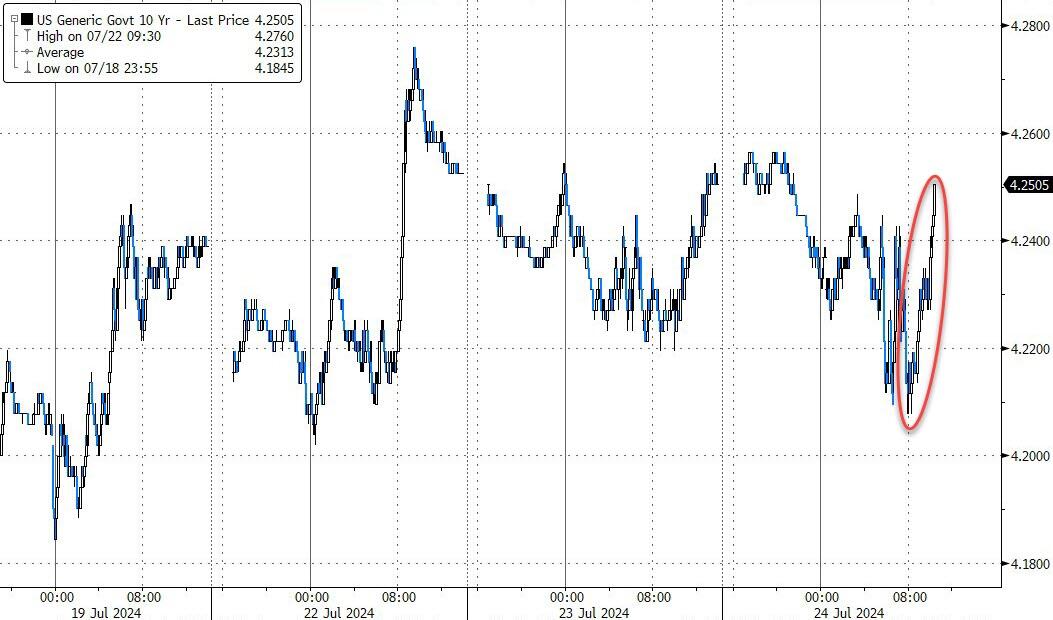

One day after a stellar, record-breaking 2Y auction, moments ago the Treasury dumped a clunker in the form of $70 billion in 5Y bonds which tailed badly and which saw a drop in foreign demand. Here are the details.

The high yield of 4.121% was below last month’s 4.335% but tailed the 4.110% When Issued by 1.1bps. In fact, it was the 4th consecutive tailing 5Y auction and 6 of the past 7.

The Bid to Cover was 2.40, up from 2.35 and above the six-auction average of 2.36.

The internals were average, with Indirects taking down 67.3%, down from 68.9% in June but above the 65.8% recent average. And with Directs taking down 18.8%, above the recent average of 17.9%, Dealers were left holding 14.0%, just below the 6-auction average of 16.3%.

Overall, this was a mixed auction, one where demand was superficially low due to the 4th consecutive tail in a row, even though the internals were in line, if not just above, recent prints with foreign demand clearly on the upper end of the recent range.

And with the market desperate for soundbites, it is not surprising that the focus was on the latter, with 10Y yields jumping to session highs, last trading at 4.25% after dropping as low as 4.21% moments ahead of the auction.

New footage has been released showing local Beaver County police officers and a Secret Service agent on the roof with the neutralised shooter Thomas Matthew Crooks at the July rally where President Trump was almost assassinated.

The footage, obtained by Senator Chuck Grassley from the Beaver County Emergency Services Unit in compliance with congressional requests, shows police and the agent talking about what has transpired while standing over the dead and bloodied body of the shooter, with the rifle he used just a few feet away.

Grassley notes“July 13 Bodycam footage provides more info than Secret Service will share with America. We NEED detailed answers ASAP on security failures TRANSPARENCY BRINGS ACCOUNTABILITY.”

NEW My office has obtained docs from law enforcement on July 13 assassination attempt of Pres Trump I’m writing Secret Service Acting Dir Rowe & DHS Scty Mayorkas AGAIN 2get badly needed answers/clarity pic.twitter.com/LyQMzYGCkD

New police bodycam footage has been released showing local Beaver County police officers and a Secret Service agent on the roof with the neutralised shooter Thomas Matthew Crooks at the July rally where President Trump was almost assassinated. Full report: https://t.co/5zd92uzs6lpic.twitter.com/9OOuiCiVCG

Here is a Rumble embed of the footage in case X blocks it on grounds of it being sensitive:

The biggest takeaway from the footage is that one of the county officers is heard saying that a police sniper in a building overlooking where Crooks was positioned was able to take multiple photos of Crooks before he began shooting.

This corroborates the timeline released by Senator Ron Johnson, chair of the Senate Homeland Security and Governmental Affairs Permanent Subcommittee on Investigations.

Another facet of the bodycam footage that is interesting is the Secret Service agent believes that two other people had been detained, but the local police don’t seem to know anything about it.

In addition, the fact that several people are standing on and moving around the roof completely rubbishes the excuse from the now former head of the Secret Service that the sloped roof was too hazardous to position personnel on.

How are they able to stand and talk on a sloped roof in such severe heat, I was told that was very dangerous

Furthermore, close to the end of the video, someone says through one of the police radios “Do we have access to a drone to clear this water tower?”

The has been much speculation that a possible second shooter was seen on the water tower, however this has not been verified.

In addition to this video, a new eyewitness video of the moment the shooter fired on Trump has emerged. Crooks is also seen pointing his weapon at those filming him, while a former military eyewitness notes that the area was not secured and no one standing along the fence was vetted.

New footage of Trump assassination attempt. Shows the shooter aiming his gun at those filming him. Former military eyewitness says neither he nor those with him were vetted despite being all along the fence and having a clear view of the stage. Report: https://t.co/5zd92uzs6lpic.twitter.com/5zV0behqsG

The new footage only serves to underscore the question, now also being asked by Trump himself, why on Earth was he on the stage when law enforcement knew there was a gunman on the roof?

* * *

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

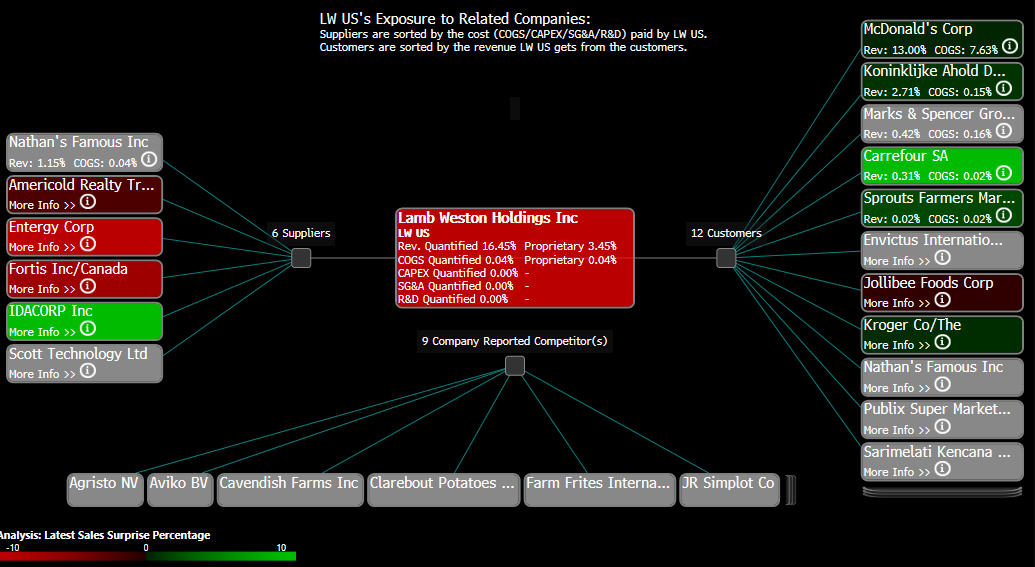

Shares Of Major French-Fry Supplier Crash As Restaurant Traffic Slowdown Worsens

One of the world’s largest producers and processors of frozen french fries, waffle fries, and other frozen potato products reported fourth-quarter profit and sales that missed estimates. The company also issued a below-consensus full-year adjusted EBITDA outlook due to sliding global restaurant traffic. This is an ominous sign, as elevated inflation and high interest rates are squeezing consumers.

Lamb Weston reported adjusted earnings per share of 78 cents for the fourth quarter ending May 26, which was well below analysts’ expectations tracked by Bloomberg of $1.25. Revenue also missed, coming in at $1.61, versus the average estimated $1.7 billion.

Here’s a snapshot of fourth-quarter earnings (courtesy of Bloomberg):

Adjusted Ebitda $283.4 million, estimate $357.4 million

North America adjusted Ebitda $276.5 million

Net sales $1.61 billion, estimate $1.7 billion

North America net sales $1.11 billion, estimate $1.17 billion

International net sales $498.7 million, estimate $530.7 million

North America volume -7%

International volume -9%

Price/mix +3%, estimate +5.41%

North America price/mix +3%

International price/mix +2%

“We are disappointed by our fourth quarter performance,” Chief Executive Tom Werner wrote in a statement.

Werner noted, “Our price/mix results were below our expectations, while market share losses and a slowdown in restaurant traffic in the U.S. and many of our key international markets were greater than we expected. We also incurred losses related to a voluntary product withdrawal.

Lamb Weston’s forward-looking guidance for the year added to the disappointing results:

Sees adjusted Ebitda $1.38 billion to $1.48 billion, estimate $1.63 billion

Sees net sales $6.6 billion to $6.8 billion, estimate $6.79 billion

Sees capital expenditure about $850 million, estimate $878.9 million

“We expect fiscal 2025 to be another challengingyear. The operating environment has changed rapidly over the past twelve months as global restaurant traffic and frozen potato demand softened due to menu price inflation continuing to negatively affect global restaurant traffic,” the CEO said.

According to Bloomberg supply chain data, Lamb Weston is a major french fry supplier for McDonald’s, deriving about 13% of its revenue from the fast food giant.

Shares of Lamb Weston in New York crashed at the start of the cash session, down more than 21%, the largest intraday decline since shares started trading in 2016.

Lamb Weston’s dismal earnings report and outlook reflect consumers pulling back on discretionary spending.

We’ve detailed for months about the onset of a consumer slowdown:

The current unemployment rate is 4%, and the core PCE inflation rate is 2.6%. In December 2019, the unemployment rate was 3.6%, and the core PCE was 1.6%. At the time, Fed Funds were 1.5%. Here we sit today, with the unemployment rate .4% higher and core PCE 1% higher than in 2019. Yet, the Fed Funds rate is 4% more than in 2019. Does it seem a bit high?

Nine months ago, we discussed some factors keeping yields above what we believe is their fair value. To wit, we ended Bond Market Noise, with the following statement:

The noise in the bond market is thunderous these days as inflation is still well above norms, deficits remain high, and the Fed continues to promise higher rates for longer. Noise creates differences between the yield on bonds and their true fair value.

Noise is hard to ignore, but it can create tremendous opportunities!

Neither the Commentary nor the article discussed R Star as a culprit behind higher yields. Therefore, given some recent mentions of R Star by Fed members, it’s worth adding to our prior analysis by diving into this wonky economics topic.

Before discussing R Star, we will update you on inflation and deficits, the two factors keeping yields high, as discussed in Bond Market Noise.

Inflation

In our opinion, the primary reason that yields are too high is a pronounced fear from the Fed and bond investors of another round of inflation. The Fed runs an extraordinarily tight monetary policy to ensure it doesn’t reoccur. Investors are demanding a premium on yields to help protect against said fear.

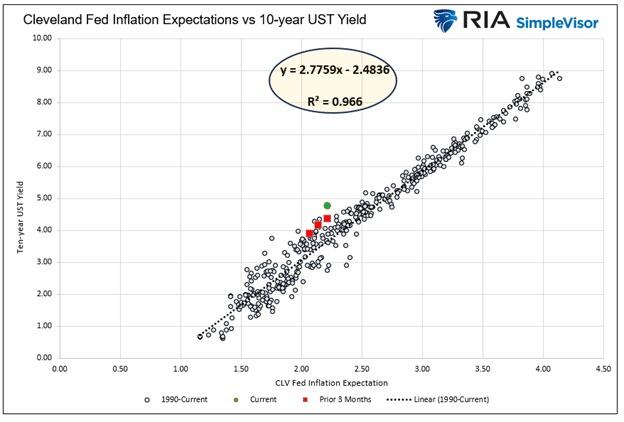

In Bond Market Noise, we shared the best predictor of long-term yields, the Cleveland Fed Inflation Expectations Index. As shown below, the index, using current, surveyed, and market implied inflation is extremely correlated with ten-year Treasury yields.

Since we published the graph, the Cleveland Fed index has fallen by 0.01%, while the yield on the ten-year Treasury is down by .35%. The extreme yield differential that existed when we wrote the article has normalized somewhat. However, the model’s fair value ten-year yield is about .40% below current yields.

If the disinflation trend resumes, as seems increasingly likely, the Cleveland Fed index will likely decline. Every basis point decline in the index results in a 2.75 basis point decline in the model Treasury yield. Therefore, a substantial yield decrease is plausible if the index returns to the pre-pandemic average. Furthermore, a recession could push the index and model yields much lower.

Such may sound absurd given where yields are and what we have experienced over the last few years, but the ten-year yield was 0.50% not so long ago.

Deficits

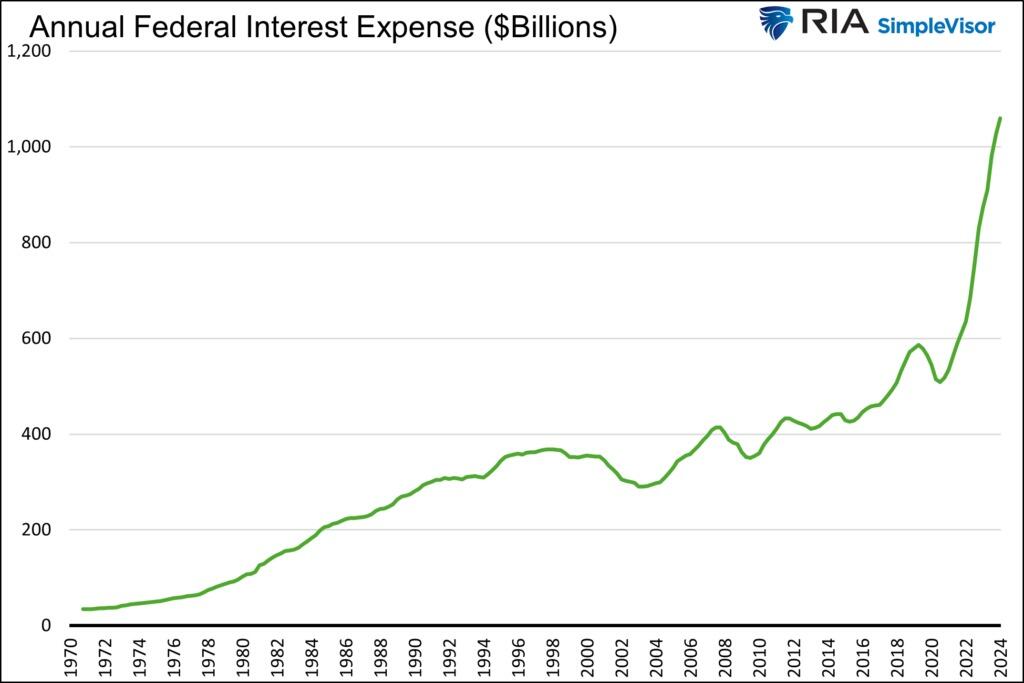

Federal deficits are running larger than average, causing a bearish skew of Treasury debt supply versus investor demand. The imbalance is partially due to an extra $500 billion yearly in interest expenses, almost entirely due to higher interest rates. Of course, significant deficit spending is also responsible.

Assuming no significant changes to the rate of government spending, deficits will fluctuate with interest rates. Therefore, in a circular fashion, when interest rates fall, the market’s fear of fiscal deficits will likely lessen.

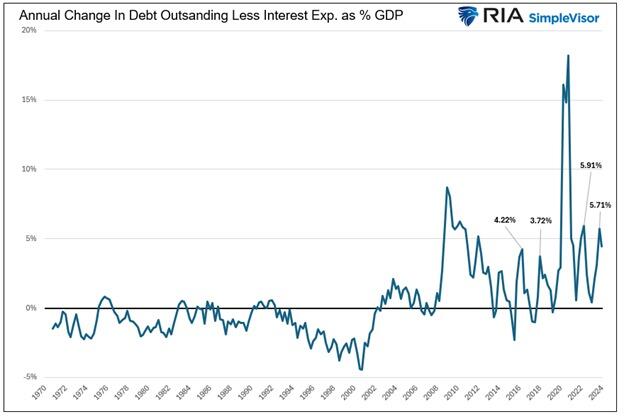

The graph below puts the deficit and interest expenses into context. It shows deficits, sans interest expenses, as a percentage of GDP. The recent peak, 5.71%, is historically high, but notice the deficit spending of the financial crisis and pandemic-related stimulus dwarf it. Further, last quarter’s peak is not far from the 2016 and 2018 highs when spending was not generally considered out of control.

We are not trying to minimize the deficits in how we present the data. However, proper consideration is warranted since interest rates substantially impact deficits and debt issuance.

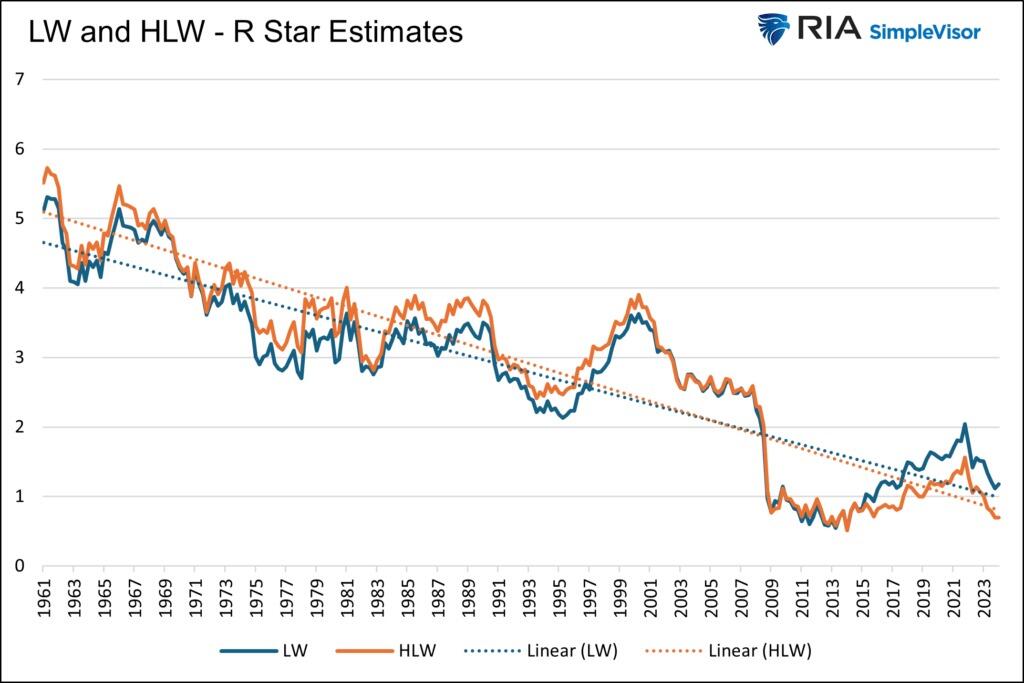

The Mythical R Star

Now, let’s dig into the economic textbooks and share a third reason: yields are higher than expected.

R Star is the real neutral rate of interest that balances the economy. It guides the Fed on how much of a headwind or tailwind their interest rate policy impacts the economy. The problem is that R Star is mythical. There is no definitive R Star. Hence, managing interest rates for the Fed is based on a guessing game of R Star.

Some economists and bond investors believe the R Star has increased over the past four years due to the pandemic. Thus, bond yields should be higher if R Star or the natural economic growth rate has increased.

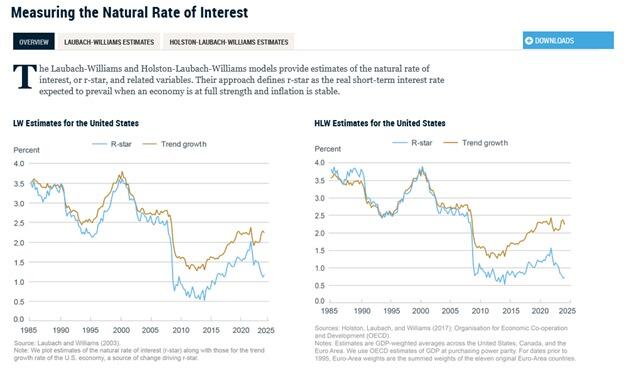

The first graph below, courtesy of the New York Fed, shows two similar R Star models the Fed relies upon.

The second graph charts them together with their trend lines.

As you can see, the two model rates fluctuate, but both have a decidedly lower trend. The Laubach-Williams model (blue) shows that the R Star is 1.18%, while the Holston-Laubach-Williams model (orange) is 0.70%. Assuming the Fed’s 2% target rate is the “stable inflation rate,” the models would argue an appropriate Fed Funds rate is between 2.70% and 3.18%. Currently, the rate is 5.25-5.50%.

Also noteworthy is that the trend lines imply that the R Star will decline by roughly .06% yearly.

Those bearish bond investors who think R Star will trend higher must believe the economic growth rate will reverse its trend of the last 40+ years.

Fed President Williams on R Star

We appreciate the argument that AI can be significant but are not sure we buy into how it affects economic productivity. Furthermore, demographics and massive outstanding unproductive debt will likely detract from economic growth in the future.

“Although the value of R Star is always highly uncertain, the case for a sizable increase in R Star has yet to meet two important tests.“

The first is the “interconnectedness” or the R Star in other developed countries. There is no evidence that R Star is rising in Europe, China, or Japan.

“Second, any increase in R Star must overcome the forces that have been pushing R Star down for decades.“

Have productivity and demographics suddenly changed for the better? Again, there is no evidence that this is happening.

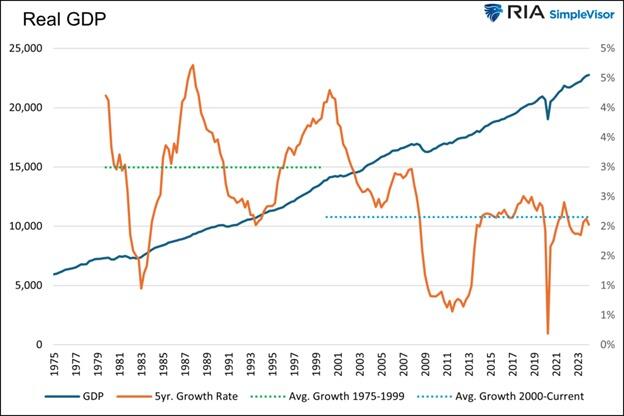

Despite the internet and technology boom of the late 1990s and beyond, the economic and corporate earnings growth rate did not increase. In fact, as shown below, the economy grew at an average rate of nearly 3% from 1975 to 1999. Since then, the average growth rate has been closer to 2%.

Summary

Suppose you think rates have reversed their downtrend of the last forty years and will reside at current levels or even higher. In that case, you must believe something significant has materially changed with the economy. The pandemic and the associated stimulus provided a roller coaster of economic activity, creating an economic mirage, but have the primary factors driving growth changed?

We say no and thus believe that interest rates still have plenty to decline alongside the mythological R Star.

Bill Dudley, Who Urged Powell To Hike Rates in 2019 To Crush Trump, Flip-Flops & Demands Immedate Rate Cut

After fading away into retirement obscurity, punctuated by the occasional op-ed on Bloomberg, where all financial has-beens go to pretend they are still relevant and where they are read by nobody, this morning former Goldman top economist and NY Fed president Bill Dudley made waves again, by violently flip-flopping to his recent stance, in what can only be viewed as another confirmation the Fed is nothing more than a political tool for a faceless, oligarch elite.

In his post-Fed existence, Bill Dudley is of course best known for writing that infamous August 2019 Bloomberg op-ed, in which he called for the Fed to hike rates into the last months of Trump first administration to scuttle his odds of re-election…

… proving beyond a shadow of a doubt that the US central bank is, among other things, a tool to perpetuate the established status quo and to crush any interlopers who may jeopardize the net wealth imbalance which the Fed has carefully established since its founding in 1913. For those who have forgotten, here is the punchline from Dudley’s op-ed.

I understand and support Fed officials’ desire to remain apolitical. But Trump’s ongoing attacks on Powell and on the institution have made that untenable. Central bank officials face a choice: enable the Trump administration to continue down a disastrous path of trade war escalation, or send a clear signal that if the administration does so, the president, not the Fed, will bear the risks — including the risk of losing the next election.

There’s even an argument that the election itself falls within the Fed’s purview. After all, Trump’s reelection arguably presents a threat to the U.S. and global economy, to the Fed’s independence and its ability to achieve its employment and inflation objectives. If the goal of monetary policy is to achieve the best long-term economic outcome, then Fed officials should consider how their decisions will affect the political outcome in 2020.

And so, having sparked a wave of outrage following this op-ed, even among establishment circles for exposing what the Fed’s real game is all about, Dudley then promptly faded back into obscurity, where he relished publishing his occasional dead wrong op-ed every now and then, most recently in May 30, when Dudley wrote “The Fed Thinks It’s Fighting Inflation. Think Again” adding that “Even at more than 5.25%, the central bank’s short-term interest-rate target might not be high enough to cool the economy.”

His argument was simple: “I think r* is a lot higher than the Fed recognizes — which means the central bank isn’t doing enough to fight inflation” meaning that the neutral rate is much higher than the Fed’s overnight rate, and thus the Fed has not hiked rates enough to fight inflation.

But why “dead wrong”? Well, that’s not our view: it belongs to Dudley himself, because in his latest op-ed this morning, the multi-millionaire who has no idea what a carton of milk or 12-pack of eggs cost, just said ignore everything he has written in the past two years, because – drumroll – the Fed needs to cut rates now.

No really: the op-ed is literally titled “I Changed My Mind” and clarifies that “The Fed Needs to Cut Rates Now” which is hilarious because just over two months ago, the same lunatic argued for (much) higher rates as “the current fed funds rate of 5.25% to 5.50% is exerting negligible restraint on growth and inflation.” What was especially hilarious, was Dudley’s parting paragraph from his May op-ed in which he said “Perhaps the Fed’s mantra, instead of “higher for longer,” should be “higher indefinitely” until inflation moves more convincingly in the desired direction.”

… or, one can now add, “until Trump has a massive lead in the polls against Biden”, because having forgotten everything he advocated at the start of the summer, Dudley, who once upon a time advocated hiking rates to crush Trump’s re-election changes, has reverted back to his basest political animal, and realizing that Biden, pardon Kamala will need all the help from the Fed she can get, Dudley is now advocating for a rate cut… and not just any rate cut but one next week because, well, the US economy may already be in a recession…. a recession which Dudley clearly had no idea about just two months ago and in fact was convinced the economy and inflation were both red hot back then.

So what changed? Well, as usual with Dudley, there are two layers to everything. One is the superficial, i.e., fake and wrong, and then there is the unspoken layer, which is the one that matters.

Addressing the former first, here former Goldmanite Dudley is beyond transparent, taking verbatim the entire Goldman note from last Monday in which his former employer also made the fundamental case for a July rate cut (and which we discussed here). We’ll spare you reading the background, and instead focus on what Dudley said today, which is that after “years of persistent strength of the US economy suggested that the Fed wasn’t doing enough to slow things down” and then, suddenly – and certainly after Dudley’s May 31 op-ed – everything changed:

Now, the Fed’s efforts to cool the economy are having a visible effect. Granted, wealthy households are still consuming, thanks to buoyant asset prices and mortgages refinanced at historically low long-term rates. But the rest have generally depleted what they managed to save from the government’s huge fiscal transfers, and they’re feeling the impact of higher rates on their credit cards and auto loans. Housing construction has faltered, as elevated borrowing costs undermine the economics of building new apartment complexes. The momentum generated by Biden’s investment initiatives appears to be fading.

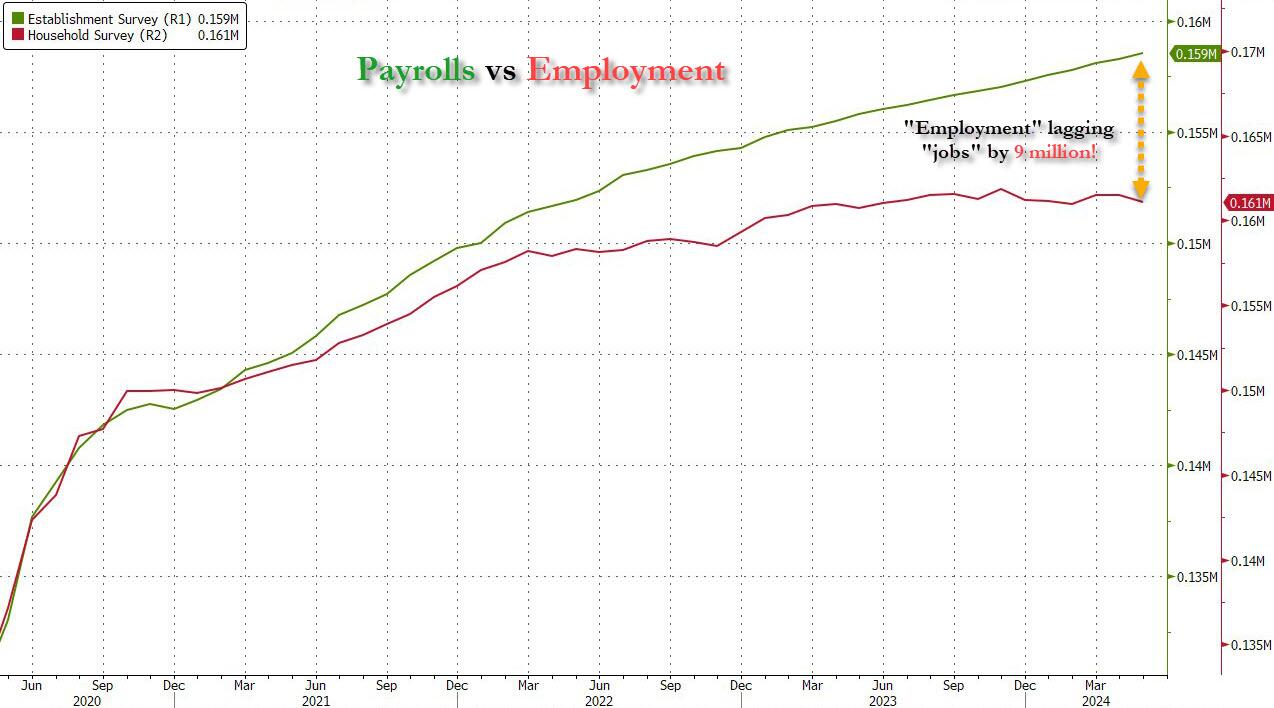

There was more: confirming yet again that the monthly jobs report has become yet another political Rorschach test in which one sees whatever one wants to, Dudley – who a month ago would have been hammering how strong the US labor market is by looking at the Establishment Survey – now flip-flops and turning to the household employment survey finds that “slower growth, in turn, means fewer jobs” to wit:

The household employment survey shows just 195,000 added over the past 12 months. The ratio of unfilled jobs to unemployed workers, at 1.2, is back where it was before the pandemic. Most troubling, the three-month average unemployment rate is up 0.43 percentage point from its low point in the prior 12 months — very close to the 0.5 threshold that, as identified by the Sahm Rule, has invariably signaled a US recession.

And that’s how easy it is to flip what have been “strong” job reports from the past year – at least according to the Biden admin – to weak ones. We, of course, have discussed all this as well, most recently here “Inside The Most Ridiculous Jobs Report In Years” where we specifically highlighted the staggering divergence between the Establishment (i.e., Payrolls) and Household (i.e., Employment) surveys.

So why, Dudley asks rhetorically completely oblivious to the irony of the question after his last op-ed which called for just this, is the Fed not cutting next week? He offers three reasons:

First, the Fed doesn’t want to be fooled again. Late last year, a moderation in inflation turned out to be temporary. This time around, further progress in reducing year-over-year inflation will be difficult, due to low readings in the second half of last year. So officials might be hesitant to declare victory.

Second, Chair Jerome Powell might be waiting in order to build the broadest possible consensus. With markets already fully expecting a cut in September, he can argue to doves that delay will have little consequence, while building more support among hawks for the September move.

Third, Fed officials don’t seem particularly troubled by the risk that the unemployment rate could soon breach the Sahm Rule threshold. The logic is that rapid labor force growth, rather than a rise in layoffs, is driving the increase in the unemployment rate. This isn’t compelling: The Sahm Rule accurately predicted recessions in the 1970s, when the labor force was also growing rapidly.

All perfectly obvious reasons, and all perfectly wrong because as everyone with half a brain knows, the one and only reason why Powell does not want to cut next week is for obvious optics that doing so now would be clearly a political move, one meant to hurt Trump’s election chances and to boost the cackling idiot of a candidate that Democrat voters never picked, but their DNC superiors did for them.

Dudley, of course, knows this but having been burned by openly suggesting the Fed steamroll Trump in 2019, it would be beyond ludicrous for a former Fed president to go for round two and openly argue that the Fed should cut rates early just to ensure Kamala becomes president, even if that’s precisely what Dudley wants. So, instead of at least having the guts to say what he means – like he did in 2019 – the ex-Goldmanite multi-millionaire tries to virtue signal and blame the Fed for the coming recession which will be its fault if it doesn’t cut rates now.

Historically, deteriorating labor markets generate a self-reinforcing feedback loop. When jobs are harder to find, households trim spending, the economy weakens and businesses reduce investment, which leads to layoffs and further spending cuts. This is why unemployment, having breached the 0.5-percentage-point threshold, has always increased a lot more — the smallest rise was nearly 2 percentage points, trough to peak.

Although it might already be too late to fend off a recession by cutting rates, dawdling now unnecessarily increases the risk.

To be sure, it is possible that Powell will do just what Goldman – and Dudley – want, and shock the market next week with a rate cut which nobody expects and in doing so will hammer the final nail in any remaining speculation it is apolitical and won’t do everything in its power to crush Trump.

And while the market would normally see right thought Dudley’s laughable attempt to once again hammer Trump, this time it’s not so sure, because as Nomura’s Charlie McElligott writes this morning “we see ex Fed and current Bloomberg opinion writer Bill Dudley pulling a full-tilt U-turn, departing the “high for longer” camp, and instead, now calling for a Fed cut, preferably as soon as NEXT WEEK—as the lagged and variable impact of prior tightening is now hitting the economy, with tapped consumers, slowing momentum from Biden’s fiscal stim, softening labor (references Sahm rule, naturally), all while inflation pressures have abated.” In turn, this growing possibility of a shock from the Fed, is hammering yields and hitting consensus FX positioning, which is “now experiencing ~-2.5 to -3 z-score moves lower in G10FX Momentum and Carry –strats over the past two weeks, largely as a function of the Yen rallying through key levels vs USD, but also too, seeing significant movement in GBP / NOK / SEK / NZD / EUR against the Greenback as well.“

The irony of all this is i) just how stupid and transparent it all is and ii) even if the Fed does cut next week, it is unlikely to have any impact on the outcome of the election in November, but it will certainly make Trump notice and when – not if – the president rightfully retaliates at the all out political central bank, taking the next and final step in destroying the dollar’s reserve status – everyone will be so very shocked that Trump finally dragged the current financial regime beyond the Rubicon.

The makeup of a federal labor board is likely unconstitutional, a federal judge ruled on July 24, siding with Elon Musk’s SpaceX.

Members of the National Labor Relations Board (NLRB), and administrative law judges (ALJs) employed by the board, are likely unconstitutionally protected from removal by the president, according to U.S. District Judge Alan Albright.

“Under binding precedent, this court is satisfied that SpaceX has demonstrated a substantial likelihood of success on its claims that Congress has impermissibly protected both the NLRB Members and the NLRB ALJs from the President’s Article II power of removal,” he said in a 15-page decision.

SpaceX, which builds and launches rockets and other spacefaring vehicles, filed the legal action in April in Waco, Texas.

The company pointed to Article II of the U.S. Constitution, which gives the president all executive power.

Under court precedent, the president must have unrestricted power to remove officers, including administrative law judges, who assist him in carrying out his duties.

But under federal law, the NLRB members can only be removed for neglect or malfeasance, and the board’s judges can only be removed if a different board decides there is good cause.

“The statutes’ provision of at least two layers of removal protection prevents that exercise of presidential authority and thus violates Article II of the Constitution,” the suit stated.

SpaceX asked for a preliminary injunction to block proceedings initiated against it by the board.

Lawyers for the firm said the company would be harmed if an injunction was not issued. Government attorneys opposed the request, citing a U.S. Supreme Court ruling from 1935, known as Humphrey’s Executor, that found the president does not have “illimitable power of removal” of executive officers.

Judge Albright ruled in favor of SpaceX and imposed an injunction as the case proceeds. He said the ruling came in part because of the U.S. Court of Appeals for the Fifth Circuit’s ruling that restrictions on removal for administrative law judges in the Securities and Exchange Commission are unconstitutional.

“Allowing Congress to eliminate the president’s ability to remove principal officers for inefficiency would be an unjustified expansion of Humphrey’s Executor,” he stated.

“Finding that NLRB member’s removal protection constitutional would require this court to expand Humphrey’s Executor where the Supreme Court has repeatedly declined to do so.”

The judge added later that no part of the injunction “prevents Congress from using a constitutional means to achieve its goals.”

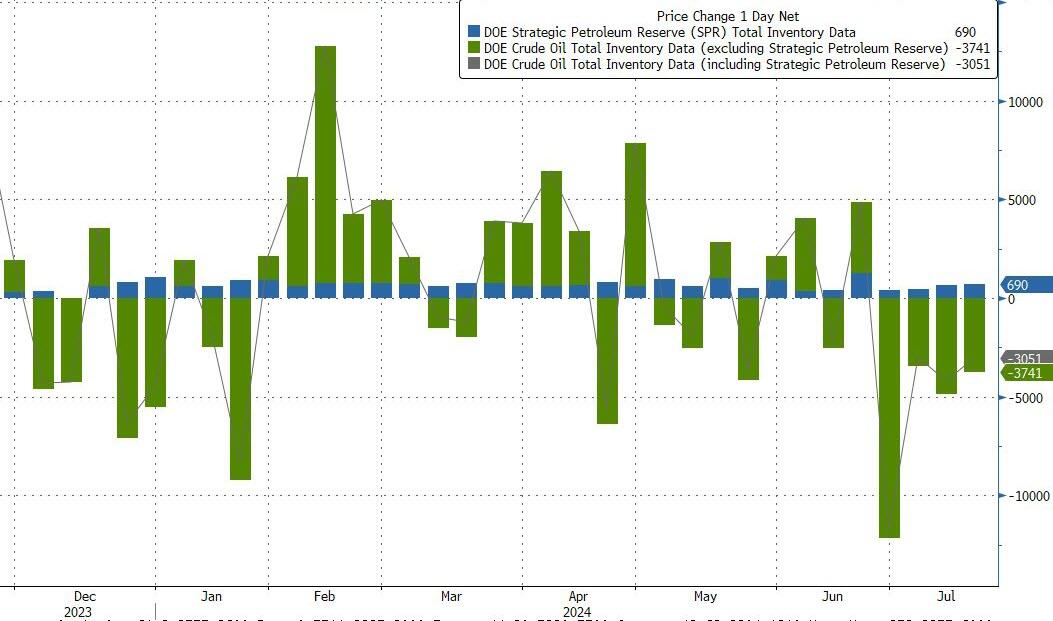

WTI Extends Gains After Across-The-Board Inventory Draws

Oil prices continued to drift higher, after finding technical support yesterday the 200DMA and also buoyed by across-the-board draws reported by API.

API

Crude: -3.9M

Cushing: -1.6M

Gasoline: -2.8M

Distillates: -1.5M

DOE

Crude: -3.74mm

Cushing: -1.71mm

Gasoline: -5.57mm – biggest draw since March

Distillates: -2.75mm

The official data confirmed API’s across-the-board draws with crude stocks down for 4 straight weeks and a large gasoline draw too….

Source: Bloomberg

The Biden admin added another 690k barrels to the SPR last week…

Source: Bloomberg

US Crude production remains at record highs despite the rig count continuing to decline…

Source: Bloomberg

WTI is extending gains on the draws and yesterday supportive bounce from the 200DMA…

Over the past five years, crude prices have averaged monthly declines from August through November, he said. Oil benchmarks have been “dragged lower by renewed concerns over Chinese demand, given the absence of further economic support out of Beijing,” said Tan.

In 1848, a 29-year-old Sacramento shop owner named Samuel Brannan was tending the cash register at his store when a pair of shoppers asked if they could pay him in gold.

Brannan was stunned when the shoppers pulled out solid gold nuggets. The gold, they said, had been found at Sutter’s Mill, about 35 miles northeast of Sacramento.

In addition to owning the only shop between San Francisco and the gold site at Sutter’s Mill, Brannan also happened to own a newspaper. And so he immediately used his paper to start spreading the word about the gold discovery.

According to legend, Brannan supposedly kept a small vial of gold to show prospective miners, and he once allegedly ran through the streets of San Francisco shouting, “Gold! Gold from the American River!”

Brannan’s newspaper constantly ran stories claiming that all you needed was a shovel, a pick, and a pan, and you too could get rich digging gold in California.

His hyping of the gold discovery is rumored to have helped spark the rush of 300,000 people to California to dig for gold— many in 1849, giving rise to the moniker “the San Francisco 49ers.”

But Samuel Brannan was NOT among them digging for gold.

Instead, during the peak of the Gold Rush, he sold about $5,000 worth of shovels, picks, pans, and other equipment to miners each DAY at his store on the way to the Mother Lode.

That would be nearly $200,000 per day in 2024 dollars. And Brannan is cited as California’s first millionaire.

“Picks and shovels,” has become a common descriptor in investments— sometimes the best opportunity when a new “gold mine” is found is to sell the “picks and shovels” needed to mine the gold.

Right now, the biggest new gold mine out there for investors is artificial intelligence.

And Nvidia is almost single-handedly responsible for producing the hardware (GPUs) for many of the most popular AI applications like ChatGPT.

But in addition to the hardware required to run AI, there is also an ongoing energy need. And it’s not trivial.

In fact, for every dollar companies spend on a GPU (which can easily run $40,000+ each), they will have to spend another dollar for the energy to run it.

AI applications like ChatGPT can generally be broken down into two stages: training, and querying. The training phase is where they feed vast amounts of data into the algorithm so that it can ‘learn’.

And this training phase is absurdly power-hungry; training a single algorithm can be the equivalent electricity of tens of thousands of homes. It’s like a small city.

Then there’s the ongoing querying phase, i.e. the power consumed when users say “Generate an image of a cat playing the harmonica”. Millions upon millions of queries in real time require substantial energy, about 10x as much as Google uses for its entire search function.

And that figure is growing.

The problem for America’s power infrastructure is that it is already strained.

And exacerbating the problem is that the people in charge now keep pushing for extremely inefficient and intermittent “green energy” like wind and solar, which simply cannot produce electricity in the same quantities as conventional sources.

In short, America’s power grid is already struggling. And AI will continue to create a surge in electricity demand that utility companies may not be able to meet.

Big technology companies know this, which is why many of them are looking at building out their own power plants… just to ensure that their data centers never run out of electricity.

The best solution by far would be small scale nuclear reactors. But that technology just isn’t quite ready yet.

So the next best reliable and inexpensive way to produce electricity is through natural gas.

US natural gas is priced at around $2.50 per million BTUs. If you look at this in terms of pure energy, $2.50 natural gas is the energy equivalent of a barrel of oil selling for about $15.

In other words, US natural gas is absurdly cheap, one probably one of the most underpriced commodities in the world.

Tech companies and electrical utilities know this. So there’s a good chance that natural gas becomes the favored energy commodity for new power plants that will continue to drive the AI boom.

That’s why I believe natural gas is currently the best “picks and shovels” investment to scoop up in the AI space: energy is the one thing that these power-hungry AI applications need. And natural gas is the cheapest form of energy in the world.

It also helps that the stock prices of many of the highest quality and most profitable natural gas producers are laughably cheap. So there’s clearly a lot of upside potential from here.

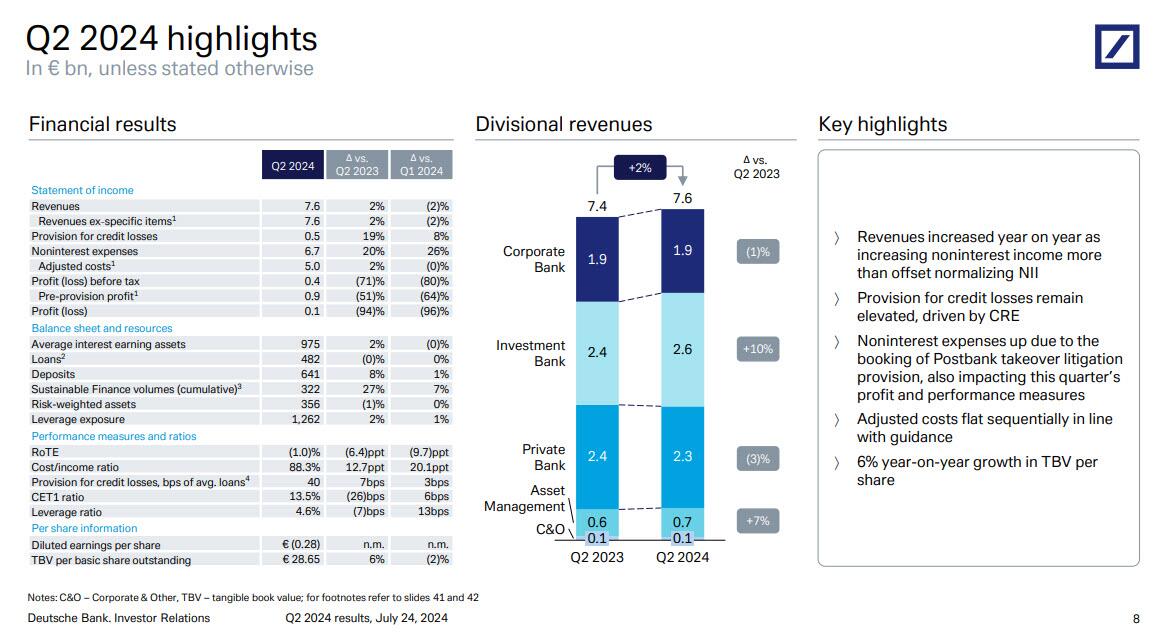

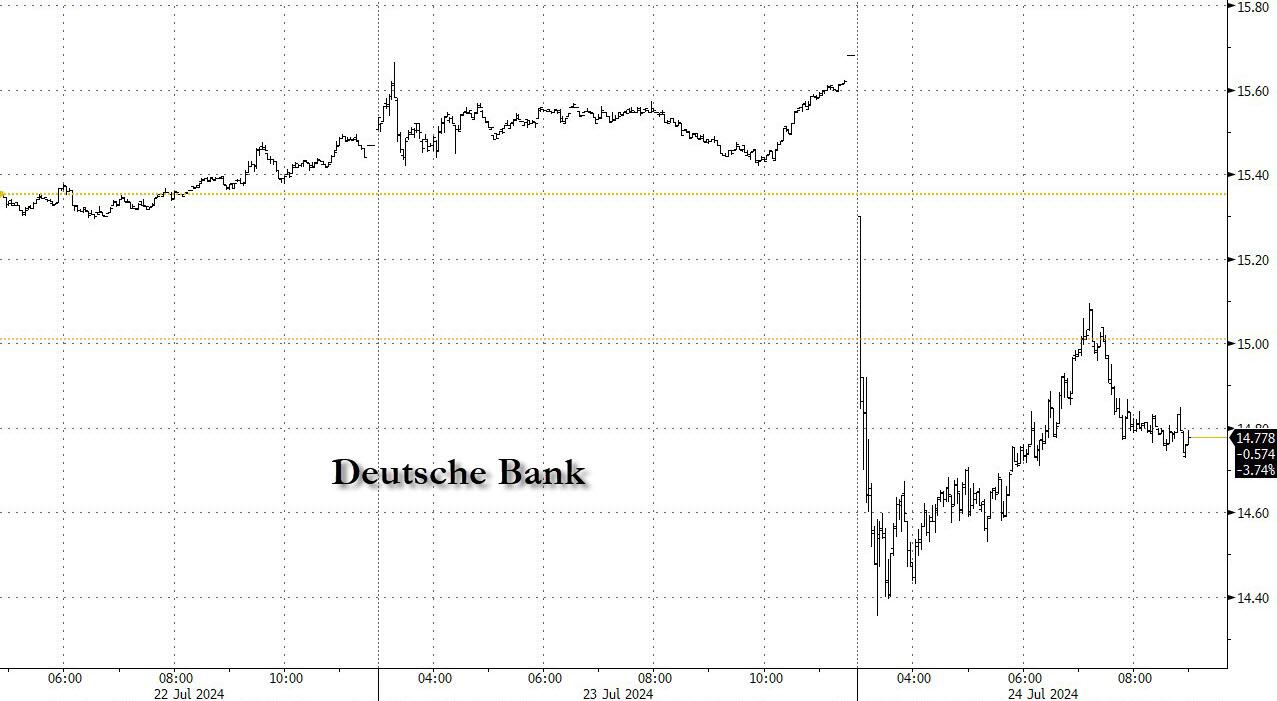

Deutsche Bank Plunges After Jump In CRE Loss Reserves, Shelves Plans For Buyback

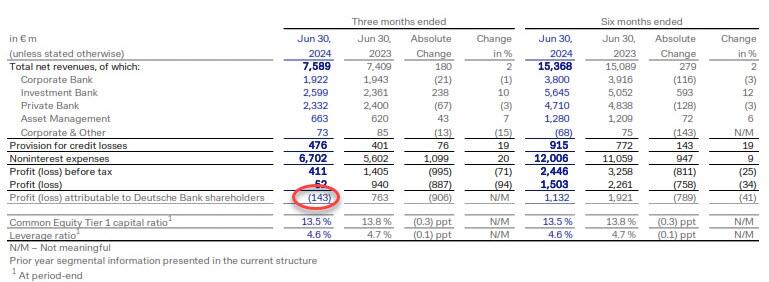

After a seemingly endless streak of stronger than expected earnings reports, this morning Deutsche Bank posted its first quarterly loss in four years as revenue from fixed-income and currencies fell about 3%, trailing the average 5% gain on Wall Street (even as IB income rose about 10%).

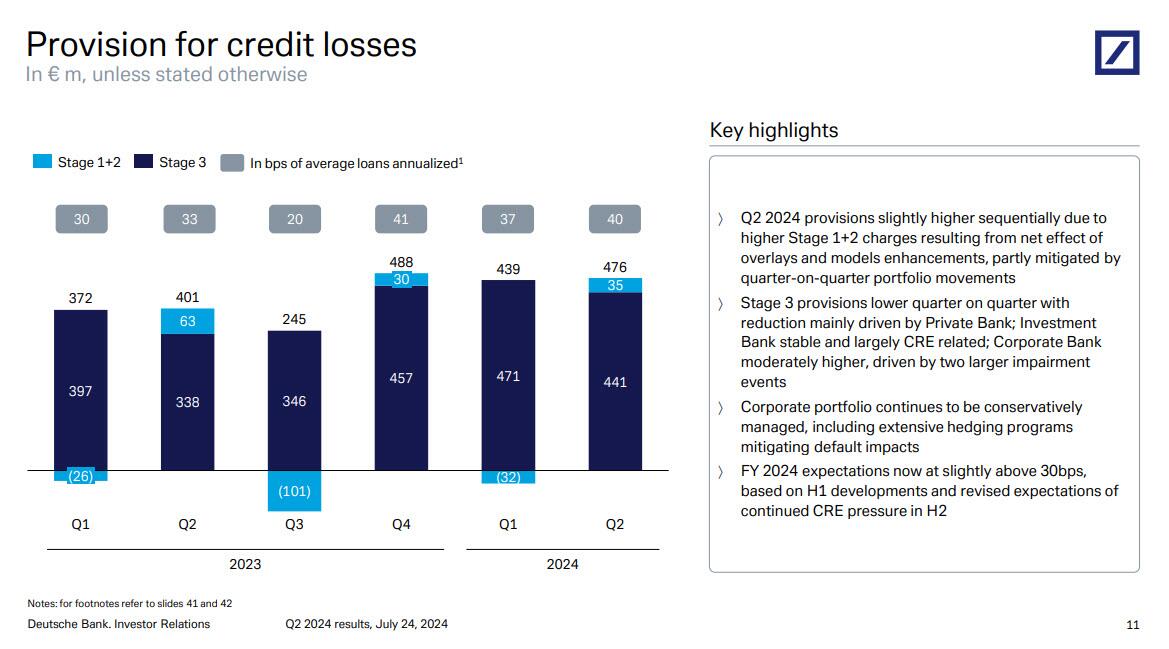

Also, the bank’s decision set put aside a bigger loss reserve for souring loans to companies and the commercial real estate sector did not help, and cast a shadow over an otherwise solid quarter for several of Europe’s largest lenders.

Deutsche Bank’s quarterly loss, a €143 million shortfall in profit attributable to shareholders, was the first since the second quarter of 2020, when it began to emerge from the restructuring kicked off by Sewing in the previous year. Last quarter’s figure included a €1.3 billion litigation provision tied to its Postbank retail unit.

More importantly, as a result of the earnings fiasco, Germany’s largest bank also shelved plans for a second buyback this year as a previously disclosed litigation charge pushed it to the first quarterly loss since 2020. The shares plunged as much as 8.5% Wednesday, the steepest drop in almost three months, as the market realized it will no longer be frontrunning stock buying by the bank itself. They since recovered some losses, and were down 5.6% at last check, the worst performer among the large European lenders. BNP and UniCredit declined as well, with only Santander posting gains.

“The beginning of a recovery that I might have expected three months ago hasn’t happened yet,” Chief Financial Officer James von Moltke said on an analyst call, referring to the lender’s exposure to commercial property loans.

According to Bloomberg, the disappointing results from Deutsche Bank dented optimism about lenders across the region, sending a broader index of European banks lower even as Italy’s UniCredit SpA and Spain’s Banco Santander SA both raised their revenue guidance. France’s BNP Paribas SA beat the profit estimate from analysts after it reported a 57% jump in equities trading. Santander raised its target for revenue growth this year and said it would continue to focus on controlling costs after posting a record profit in the second quarter. The bank’s key retail business was boosted in the quarter by its two main markets, Spain and Brazil.

By contrast, investors were disappointed with BNP Paribas despite the profit beat. The French bank posted a decline in fixed-income trading revenue that compared with an average gain for the US competition. The equities business was the biggest positive surprise at the Paris-based lender, highlighting how a strategy to build the unit out over the past years is paying off. BNP bought a part of Deutsche Bank’s equities business several years ago when the German bank put it on the market as part of a large-scale turnaround strategy.

Despite the unexpected crunch for Deutsche Bank in the second quarter, the bank said it remains positioned to exceed a pledge for €8 billion in shareholder payouts over the “medium term.” CEO Christian Sewing also reiterated targets for higher profitability and revenue of €30 billion this year as he cuts back office costs.

Sewing has built out the advisory unit with last year’s purchase of Numis Corp. to boost fee income. Deutsche Bank is also one of the few lenders that has chosen to take advantage of a downturn in dealmaking to add staff to its M&A unit, which saw a strong rebound in revenue during the quarter.

The firm is also among a dozen lenders in the focus of the ECB over risks from leveraged finance, i.e., extending credit to companies that are already highly indebted. The ECB is considering asking banks to set aside about €7 billion in additional provisions for such debt, Bloomberg reported on Tuesday. Sewing and von Moltke both said they were confident that Deutsche Bank has made adequate provisions for the leveraged finance business.