Yen Craters As Japan Gives Up On Further Rate Hikes, Carry Trade Is Back With A Bang

In the past two months, reports of the yen carry trade have been greatly exaggerated, largely as a result of market whiplash to Japan’s schizophrenic approach toward the currency.

Recall, that for years on end, the BOJ and the government were doing everything in their power to crush the Japanese currency in hopes of sparking an inflationary wage-growth conflagration, which to a country stuck in a deflationary debt trap, seemed like the only possible exit from an existential implosion. But then, once the yen did crater and hit a 40 year low earlier this year, Japan scrambled to do the opposite and intervened in the open market on multiple occasions to contain further selling of the currency as the resulting inflation led to devastated standards of living and sparked outrage among the local population over runaway inflation, eventually resulting in the collapse of the Kishida government, just as we warned back in June.

Japan’s standard of living has disintegrated with real wages collapsing.

Meanwhile, the BOJ is pretending there is no inflation and has sparked the latest (and maybe last) Japanese stock bubble pic.twitter.com/ICTPHjajFn

— zerohedge (@zerohedge) June 6, 2023

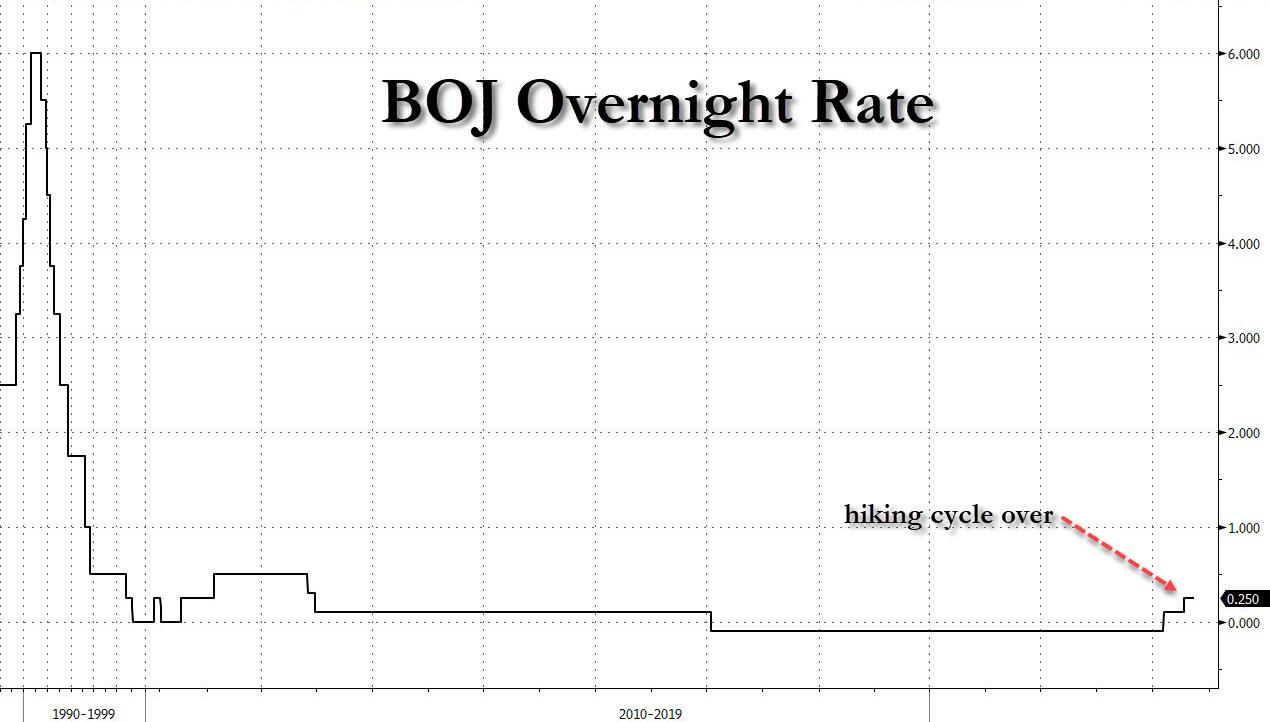

But it was only when the BOJ decided to shock the market with a surprise second rate hike in July – even as the rest of the world was aggressively cutting rates – that the yen soared, and the yen carry trade was allegedly left for dead. Indeed, the plunge in the USDJPY was one for the history books: tumbling from 162 to 140, countless yen shorts were annihilated.

The problem with this, of course, is that not only did the Nikkei crater, forcing the BOJ to immediately come out and defend the “wealth effect”, i.e., stocks, saying that it would never again hike if markets were unstable thus capitulating on its hawkish strategy just days after the hike, but with Japan extremely sensitive to yen moves, it means that from roaring inflation, China was about to revert back to its status quo: paralyzing deflation (because unlike the US, and thanks to its 400% debt/GDP, Japan is simply unable to find a happy medium and always swings from one extreme to the other). Indeed, just four days ago we said observed that a core CPI measure for Japan tumbled suggesting the surging yen was about to spark a new deflationary tidal wave…

Tokyo core CPI plunged: Japan’s hiking cycle is almost over (after one hike) pic.twitter.com/ign9bphGgI

— zerohedge (@zerohedge) September 27, 2024

.. leading us to conclude that “Japan’s hiking cycle is almost over”, after just one tiny rate hike.

We were right.

This morning, Japan’s new Prime Minister Shigeru Ishiba, who was touted as an uber hawk and the leader that would force the BOJ kicking and screaming to keep hiking for the foreseeable future, plunging Nikkei and inflation notwithstanding, confirming everything we have said in the past two months when he announced that the economy isn’t ready yet for further interest rate hikes, following a first meeting with Bank of Japan Governor Kazuo Ueda on the first full day of his new administration.

As Bloomberg first reported, Ishiba said conditions weren’t right for the BOJ to move again following two interest rate hikes earlier this year, in comments that jolted the yen to its weakest against the dollar for the day, and have sparked the USDJPY’s next move back to 160…. which is another thing we predicted a few days ago.

Takaichi, Negative On BoJ Rate Hikes, Appears To Lead In LDP Election: UBS

USDJPY 160 back on the menu

— zerohedge (@zerohedge) September 24, 2024

The comments came after a flurry of signaling Wednesday that Ishiba’s government has no desire for now to see the central bank raise borrowing costs further. Additionally, ministers played down the premier’s appetite for monetary policy normalization and highlighted the need for the central bank to focus on the unfinished task of eradicating deflation.

In other words, just as we said: Japan’s hiking cycle is over, with the rate rising to a whopping 0.25%. Because when your debt/GDP is 450% that’s as far as it can go.

At the meeting between Ishiba and Ueda, the central bank chief qualified his commitment to raising interest rates if the economy and prices match the BOJ’s forecasts, according to his comments after the talks.

“While we will adjust the degree of monetary easing if the economy and prices match our forecasts and the economy works as we expect, I also told him we want to look carefully to see if that really is the case because we have sufficient time to do so,” Ueda told reporters at the prime minister’s residence.

Which, incidentally, is hilarious because the comments make it quite clear that when it comes to financial repression and monetary policy, “western” central banks are anything but independent and always do the bidding of their sovereign masters. Which is especially amusing considering the western media is abuzz with scaremongering over what could happen to Fed “independence” in the US should Trump win. Well, spoiler alert: central banks have never been independent, and the latest yen interlude just confirmed it!

To mitigate the horrendous optics of this “yentervention” by the PM, even Bloomberg was forced to step in with damage control writing that “while it’s common for Japan’s central bank chief to hold regular meetings with the nation’s leader, Ueda’s visit came at an unusually early stage of the new administration, an indication that Ishiba’s government is determined to coordinate closely with the central bank and dispel any impression it seeks rapid rate hikes.“

Again, so much for central bank independence.

Which brings us to another critical topic: since the BOJ hiking cycle is over, the yen is now free to resume its plunge, and that means the yen carry trade is fully back on, just as one of the best Goldman FX traders, Kerem Cirpan wrote yesterday (full note here) to wit:

Nature is healing for JPY carry trades on the back of the Fed easing into strong growth and BoJ showing no interest for rapid policy normalization. Declining M2 growth in Japan does not bode well for policy plans of Japan’s new PM. Potential equity correction over the next weeks due to US election uncertainty and poor seasonals can offer good entry points for long USDJPY.

It turned out that a great entry point for going long the USDJPY would come just hours later, now that the BOJ is done hiking for good (full Goldman note available to pro subscribers here).

And with that, the USDJPY is cleared to return back to 160, where it was just two months ago.

Tyler Durden

Wed, 10/02/2024 – 10:30

via ZeroHedge News https://ift.tt/Fmy9Vzn Tyler Durden