Bank of America Trading Results Beat As Net Interest Yield Hits Cycle Lows, Charge-Offs Unexpectedly Hit 11 Year High

It wasn’t just Goldman Sachs that reported better than expected Q3 earnings this morning: on the surface, Bank of America surprised to the upside as well, and in fact its FICC division reported an even better results than Goldman’s. The bank, which had gotten Warren Buffett’s seal of disapproval, after the billionaire investors dumped much of his shares in what was once a Top 5 position, performed better than expected as it benefited from volatile markets while net interest income topped analysts’ estimates. On the other hand, there were also quite a few red flag, with the company’s Net Interest Yield sliding to a cycle low even as charge offs and credit losses jumped to the highest in years.

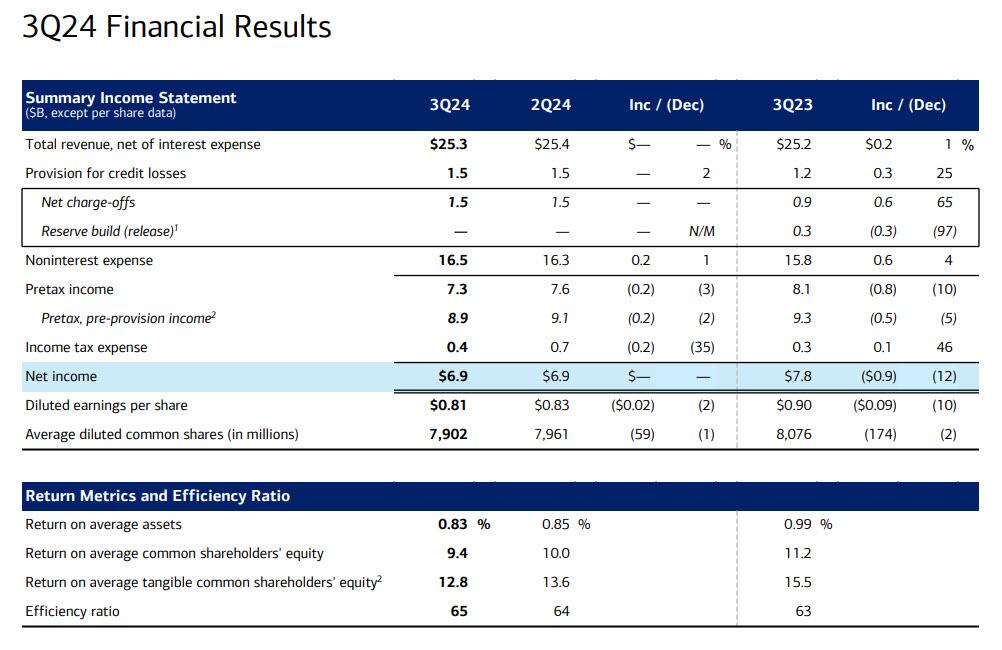

Here is a snapshot of what BofA reported in Q3:

- Revenue net of interest expense $25.35 billion, beating estimate $25.27 billion

- Trading revenue excluding DVA $4.94 billion, beating estimate $4.57 billion

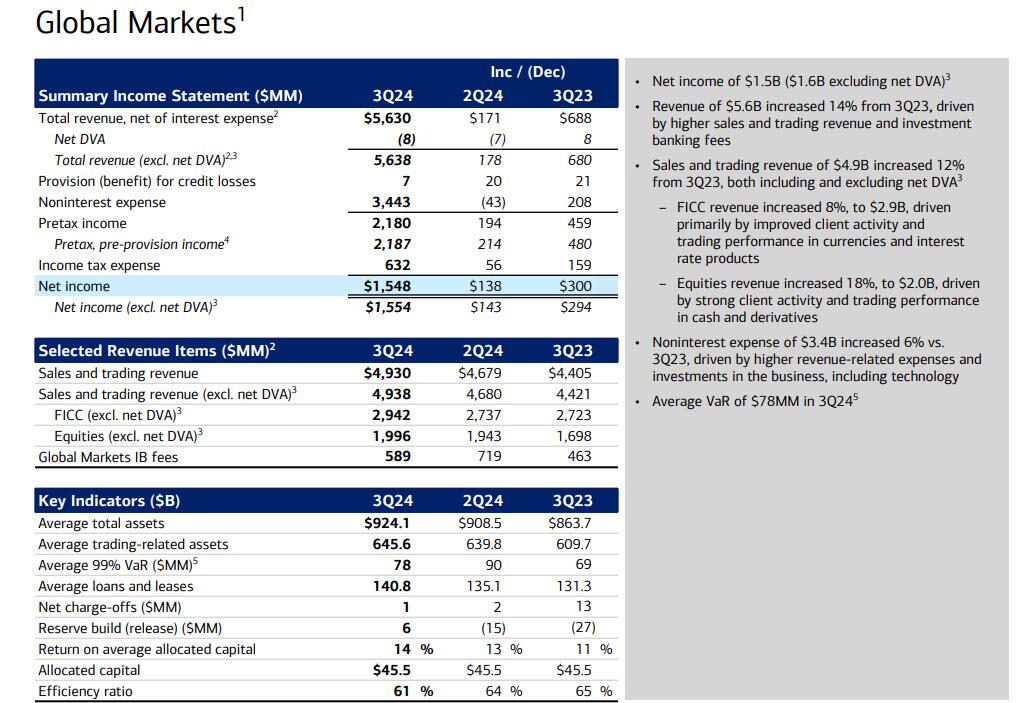

- FICC trading revenue excluding DVA $2.94 billion, beating estimate $2.77 billion

- Equities trading revenue excluding DVA $2.00 billion, beating estimate $1.81 billion

- Investment banking revenue $1.40 billion, beating estimate $1.24 billion

- Wealth & investment management total revenue $5.76 billion, beating estimate $5.63 billion

- Trading revenue excluding DVA $4.94 billion, beating estimate $4.57 billion

- EPS $0.81, beating estimates of $0.77

Taking a closer look at the Global Markets group, revenue from equity and fixed income, currencies and commodities trading rose 12% to $4.93 billion in the third quarter:

- FICC revenue increased 8%, to $2.9BN, beating estimates of $2.8BN, “driven primarily by improved client activity and trading performance in currencies and interest rate products”

- Equities revenue increased 18%, to $2.0BN, beating estimates of $1.8BN “driven by strong client activity and trading performance in cash and derivatives”

Similar to Goldman, BofA’s investment banking also outperformed expectations, a sign that the long-awaiting rebound in dealmaking is taking hold. The company benefited from “year-over-year growth in investment banking and asset management fees, as well as sales and trading revenue,” CEO Brian Moynihan said in the statement.

Investment-banking revenue rose 15% to $1.40Bn, better than analysts expected amid renewed strength in dealmaking. Fees for advising on mergers and acquisitions fell 14%, less than the almost 24% decline analysts had expected. Revenue from equity and debt issuance increased 16% and 37%, respectively.

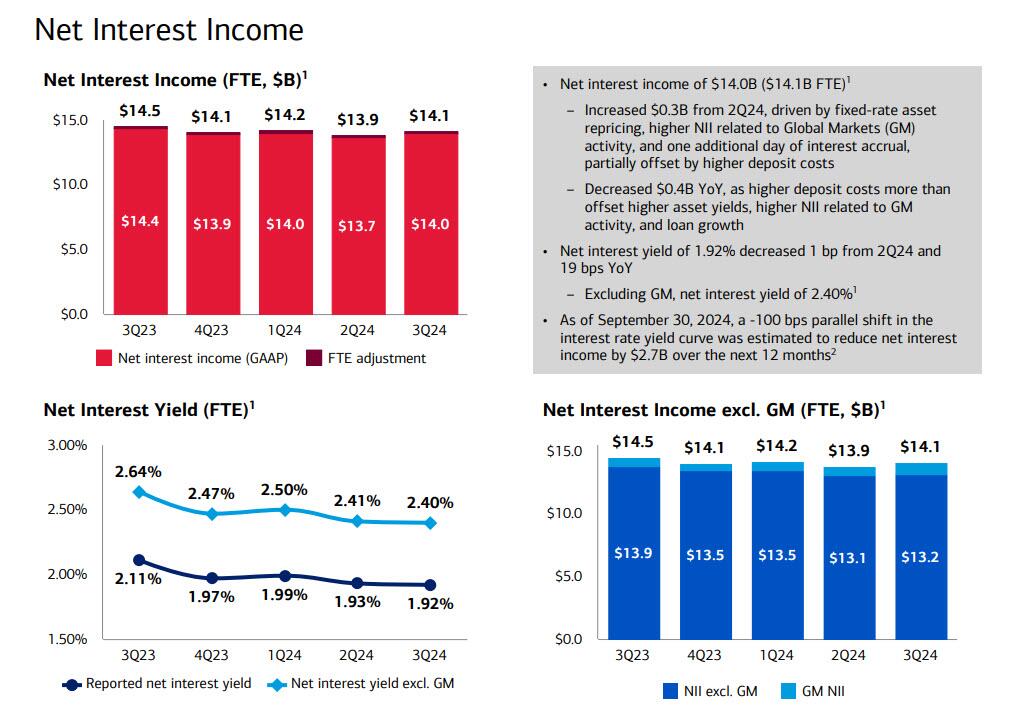

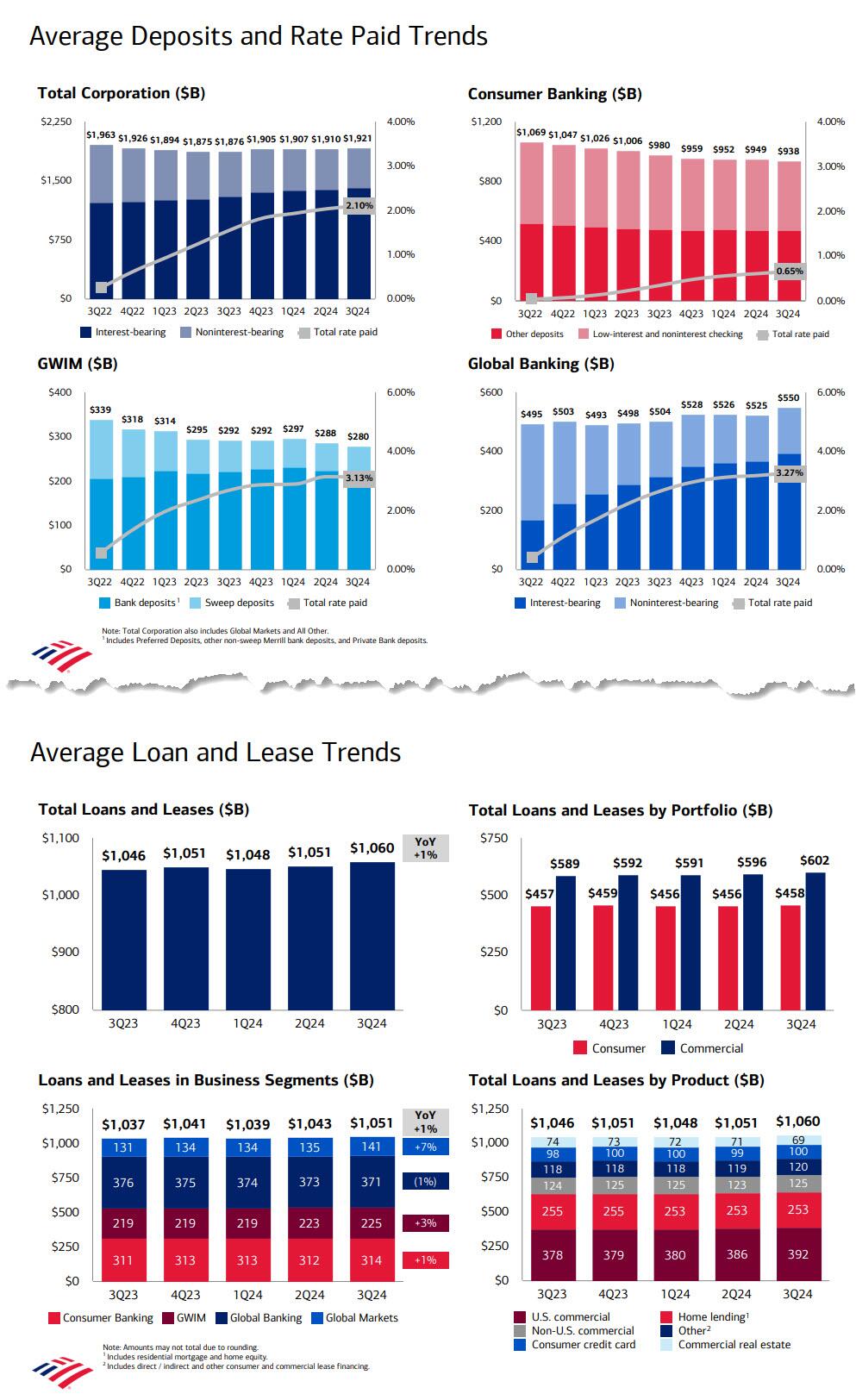

Not everything was stellar however: the second-largest US bank said that net interest income, a key source of revenue for the company, fell 2.9% to $14 billion, the lowest of the cycle; still this was better than the 3.4% drop analyst had expected (on an FTE basis, NII was $14.11 billion, also better than the estimate of $14.07 billion). The number increased $0.3B from 2Q24, driven by fixed-rate asset repricing, higher NII related to Global Markets (GM) activity, and one additional day of interest accrual, partially offset by higher deposit costs; it also decreased $0.4B YoY, as higher deposit costs more than offset higher asset yields, higher NII related to GM activity, and loan growth. Overall, BofA’s net interest yield came in at 1.92%, down both sequentially and YOY, and just below the estimate 1.93%. And now that the Fed is cutting rates again, that’s as good as it gets for BofA’s NII.

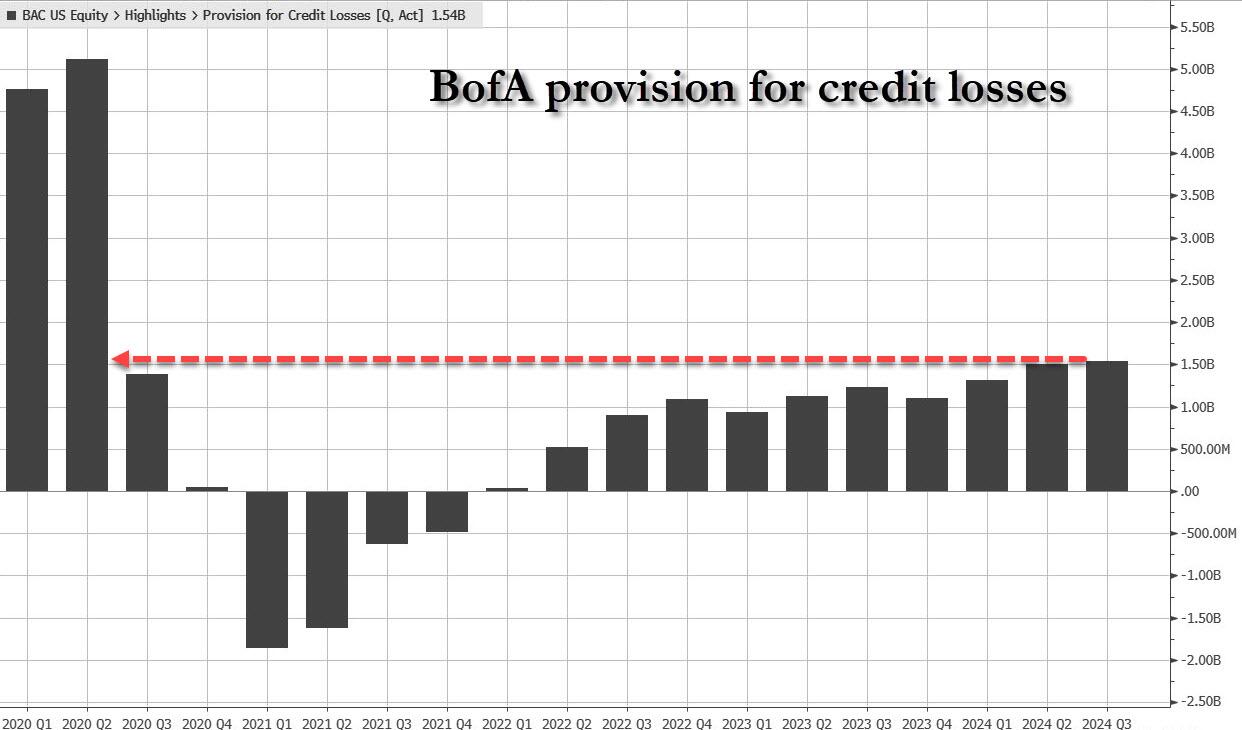

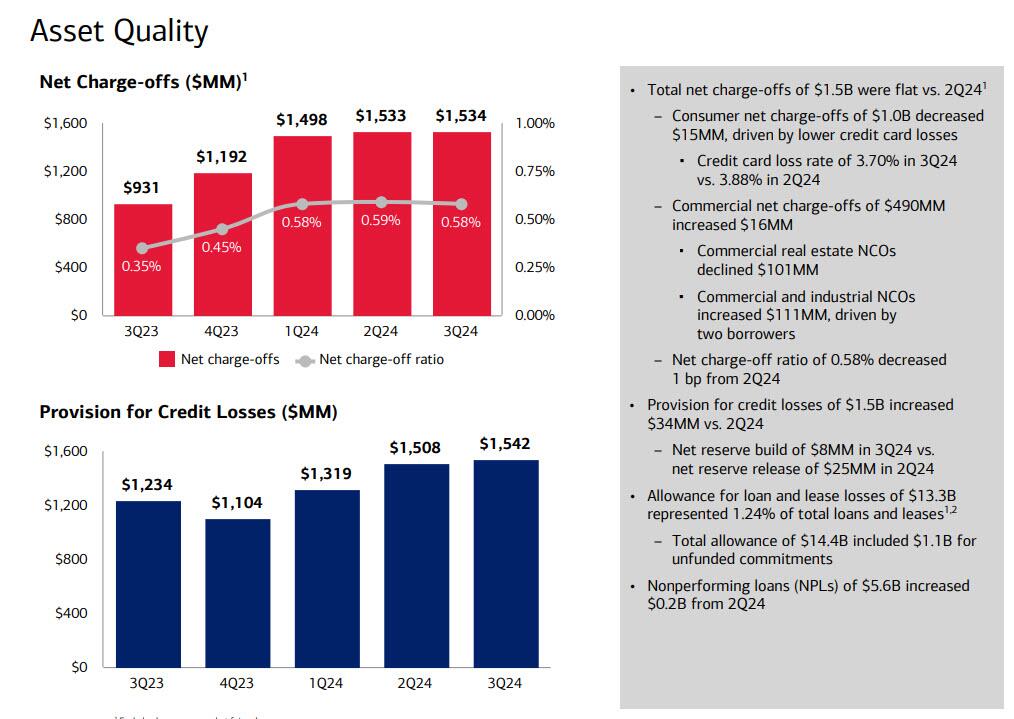

It wasn’t just the Net Interest Yield that left much to be desired: similar to JPM, BofA’s provision for credit losses unexpectedly rose to the highest in years, and was $1.54 billion in Q3, higher than the $1.53 billion estimates with a Q3 net reserve build of $8MM in 3Q24 vs. net reserve release of $25MM in 2Q24; This was the highest since the covid crash!

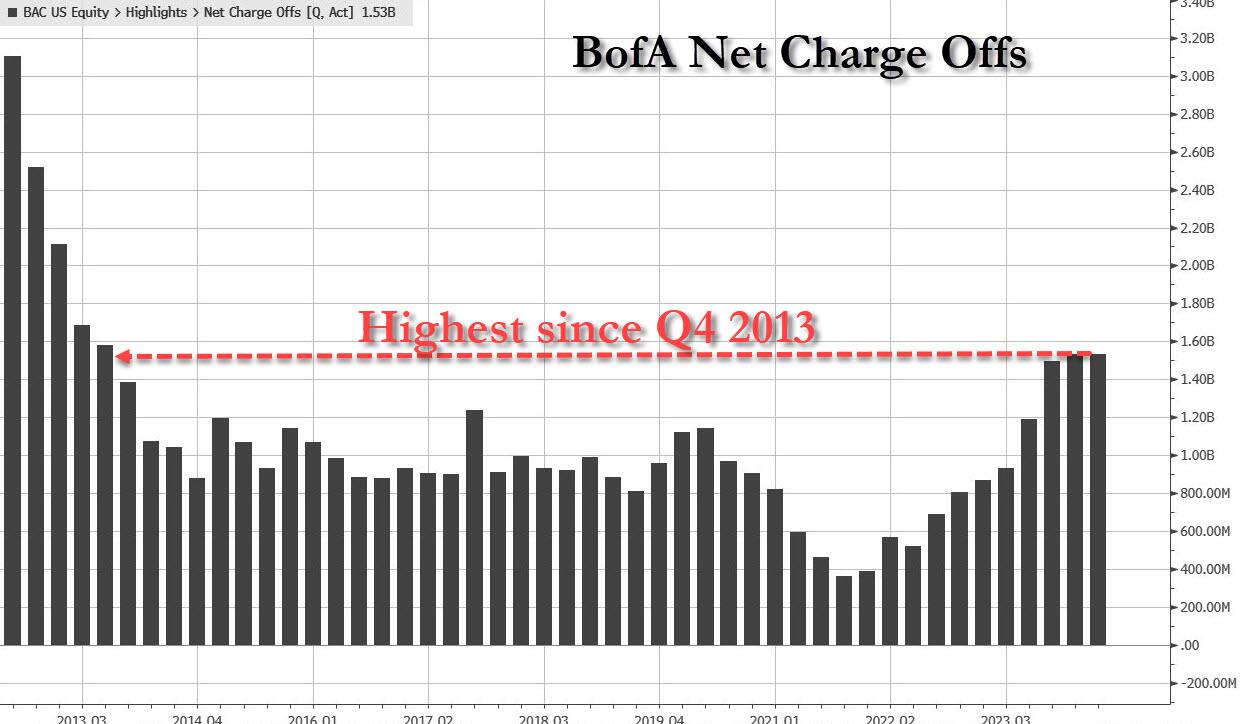

Charge offs also rose to $1.534 billion, above the $1.5 billion estimate and a 0.58% charge off ratio. This may come as a surprise to anyone looking at the stock which is still up, if not for long, and thinking that the results were somehow much better than expected.

According to the bank, commercial net charge-offs of $490MM increased $16MM; this was driven by commercial and industrial NCOs which increased $111MM, driven by two borrowers; at the same time commercial real estate NCOs declined $101MM.

On the spending side of the income statement, things were generally in line with expectations:

- Non-interest expenses $16.48 billion, estimate $16.49 billion

- Compensation expenses $9.92 billion, estimate $9.9 billion

Here is some other data:

- Return on average equity 9.44%, estimate 9.01%

- Return on average assets 0.83%, estimate 0.78%

- Return on average tangible common equity 12.8%, estimate 12.2%

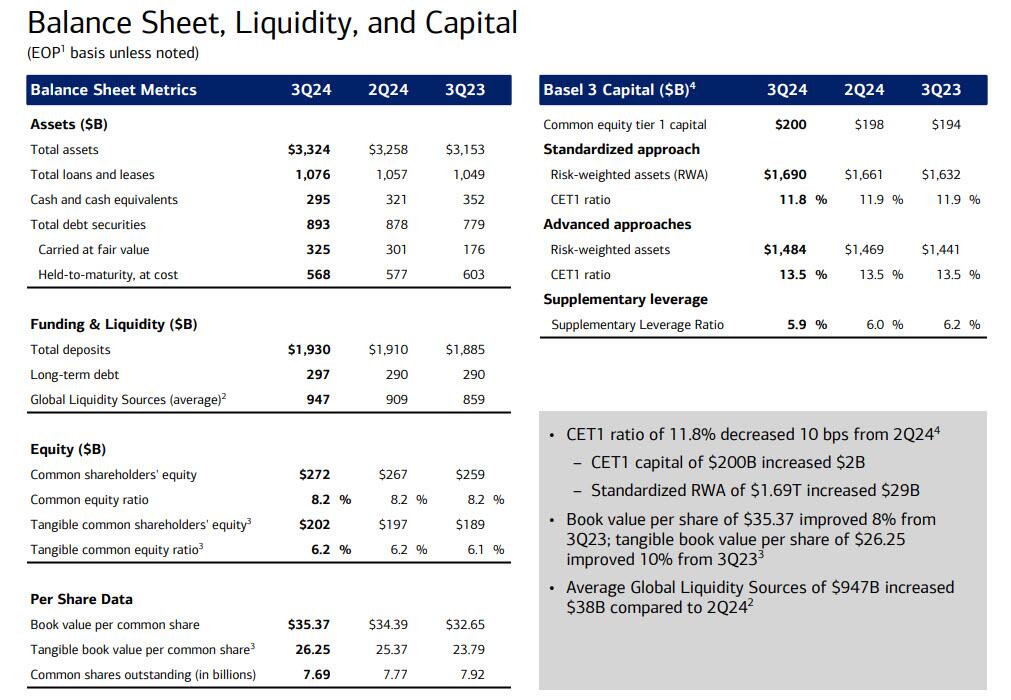

- Basel III common equity Tier 1 ratio fully phased-in, advanced approach 13.5%, estimate 13.5%

- Standardized CET1 ratio 11.8%, estimate 11.9%

Looking at the balance sheet, we find:

- Loans $1.08 trillion, estimate $1.07 trillion

- Total deposits $1.93 trillion, estimate $1.93 trillion

Shares of Bank of America, which gained 24% this year through Monday, climbed 1.4%, but were well off session highs, and we expect it to close red as investors override the euphoria algo kneejerk reaction.

BofA Q3 investor presentation below (pdf link)

Tyler Durden

Tue, 10/15/2024 – 11:00

via ZeroHedge News https://ift.tt/mW1RsXh Tyler Durden