Stagflation Odds Jump In Latest NY Fed Survey As Inflation Expectations Rise, Delinquency Fears Hit 4 Year High

In recent weeks, we have discussed on multiple occasions (here, here and here) how in his desire to get Kamala Harris re-elected by rushing out a jumbo cut before November 5, Fed president Jerome Powell may have triggered the second coming of the Arthur Burns “galloping inflation” Fed, and sure enough recent inflationary prints have certainly raised the threat that the Fed is now aggressively easing even as inflation has not only not been defeated, but is once again rising.

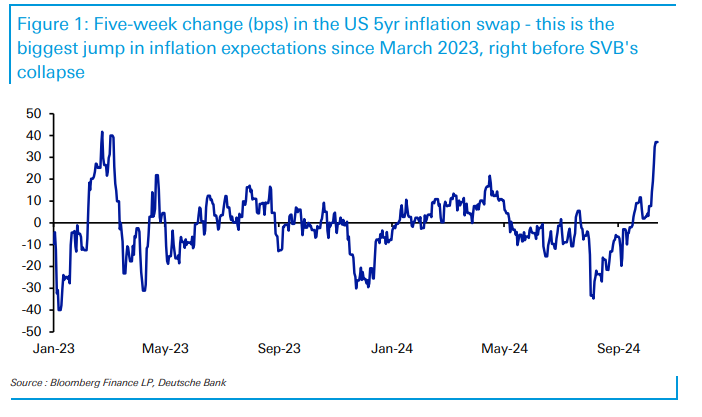

Then overnight, it was Deutsche Bank’s chief credit strategist Jim Reid who observed that US 5yr inflation swaps have seen their “largest 5-week climb since just before SVB’s collapse in March 2023, an event that shifted the narrative away from around 4 more hikes to imminent cuts for a period of time.”

To be fair, it’s not just the 50bps Fed easing in itself that has changed the inflation and rates outlook over the last few weeks. We’ve also seen 1) expectations that the ECB will move more aggressively; 2) renewed geopolitical risk and a potentially large China stimulus turn the Oil price (and other commodities) higher after a late summer slump; 3) a bumper payrolls report; and 4) still generally firm US data, including an upside surprise in the CPI last week.

Then again, these are all dynamics that the Fed should have considered before it launched an aggressive easing cycle at a time when stock prices are at all time highs, when wage inflation ~5%…

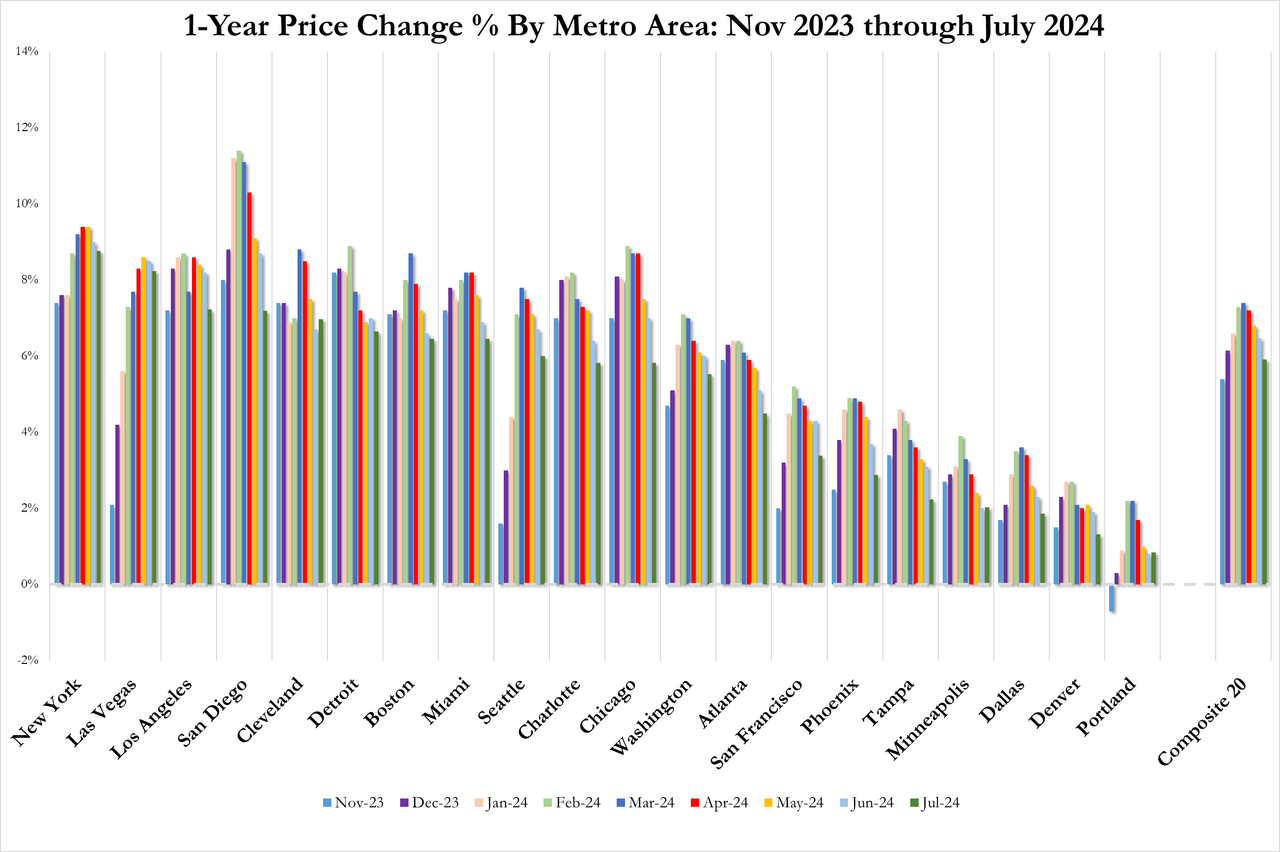

… and when home prices are still rising at a mindblowing 6%!

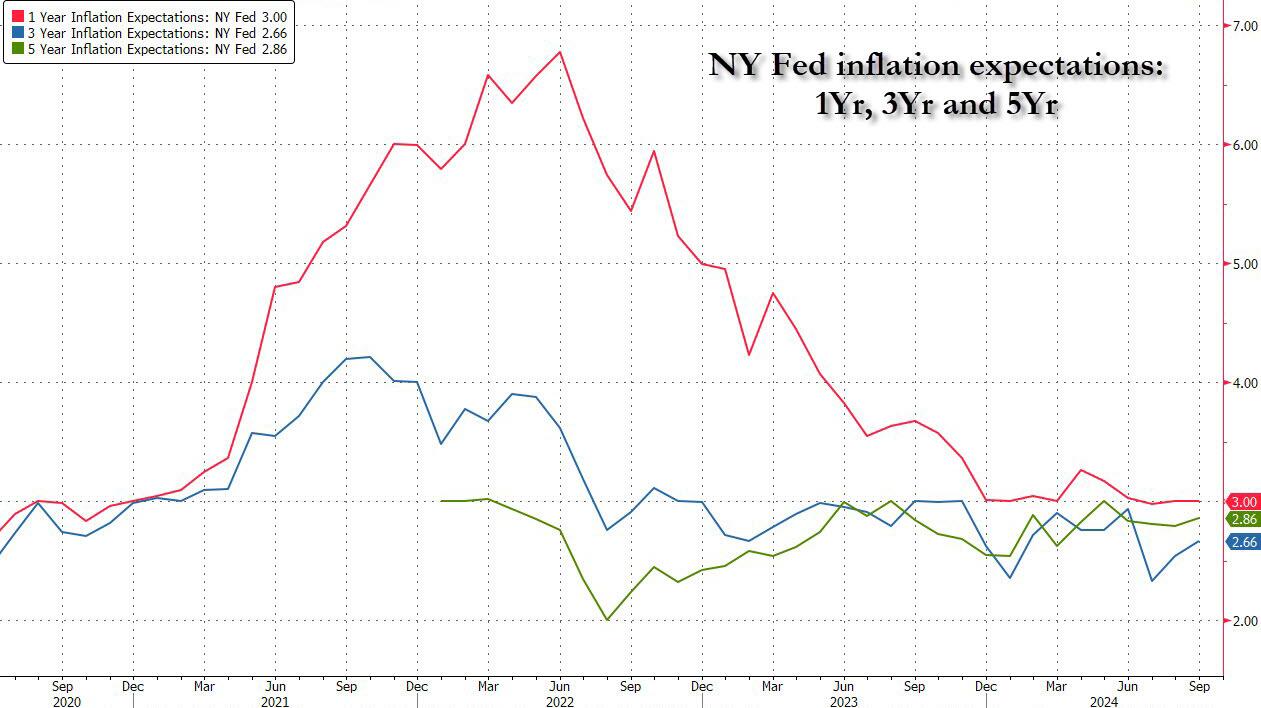

It is therefore not surprising that the latest monthly survey of consumer expectations from the NY Fed found that inflation expectations rose at both the three-year horizon (from 2.5% to 2.7%) and the five-year horizon (from 2.8% to 2.9%), and remained unchanged at the one-year horizon (where they are driven primarily by recent moves in gas prices).

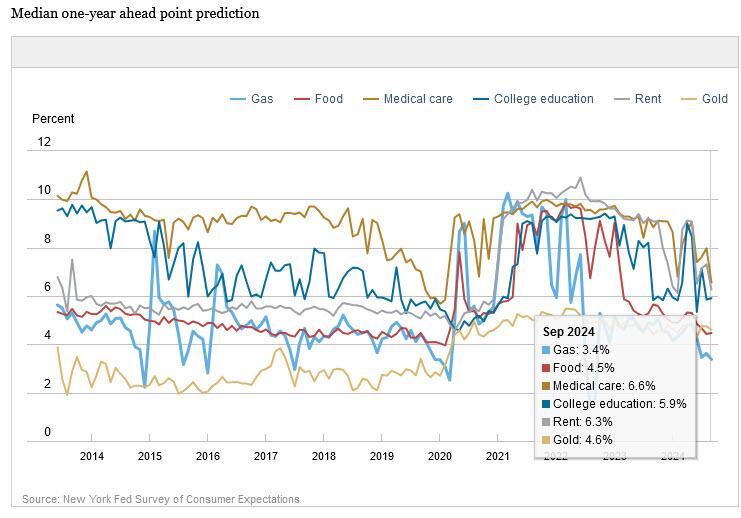

And the reason why the short-term inflation expectations were unchanged – if at the Fed’s raised inflation target of 3% – is because the median respondent saw gasoline up “only” 3.4% over the next 12 months, the least in two years. Expected food inflation ticked higher after falling in August to the lowest level since pre-pandemic, while expectations for rental inflation moderated to 6.3%. Median home price growth expectations decreased by 0.1 percentage point to 3.0%. Some other year-ahead commodity price expectations: an increase of 0.1% for food to 4.5%, college prices remained unchanged at 5.9%; medical care cost expectations dropped by 1.4% to 6.6% (the lowest reading since February 2020).

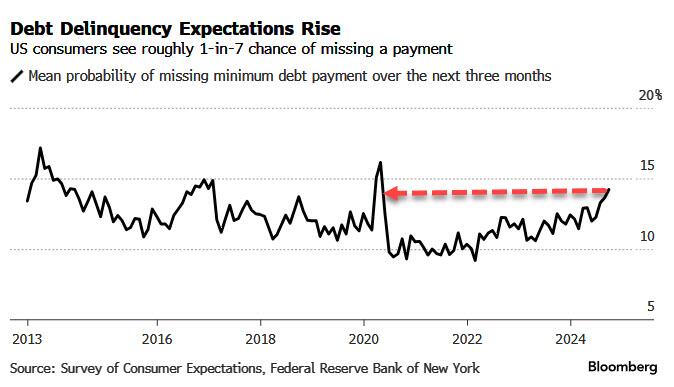

And while inflation expectations rose, sentiment about the broader economy deteriorated as perceptions among households that they might become delinquent on debts increased last month to the highest levels since April 2020. The anticipated probability of missing a minimum debt payment over the next three months rose to 14.2% in September, marking the fourth straight month of increases; the increase was most pronounced for respondents between ages 40 and 60 and those with annual household incomes above $100k.

The latest data confirms the view that the US economy is becoming increasingly split as some households do well while others are getting crushed by rising prices, slower growth and higher unemployment. In other words, stagflation.

While the orchestrated surge in the stock market – and one has the Fed’s recent rate cut to thank for that – has helped propel overall household net worth to a record over the past few months, tens of millions of Americans do not own any equities and have instead been accumulating debt in recent years amid elevated interest rates.

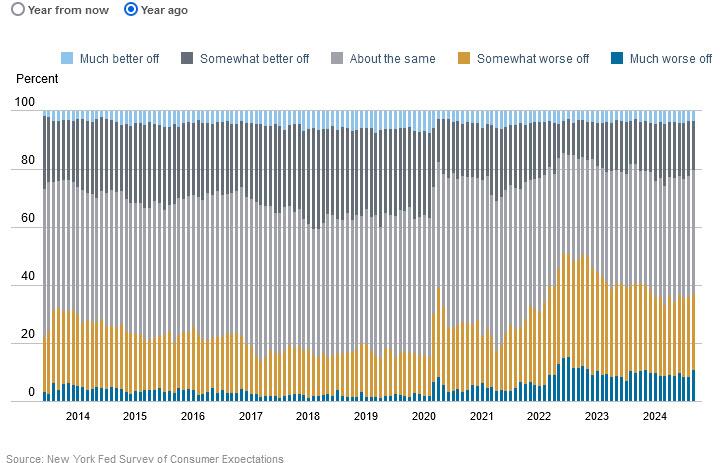

The increased odds of delinquency were mirrored in a broader deterioration of perceptions about households’ current financial situations, with fewer consumers reporting being better off and more reporting being worse off than a year ago, according to the survey.

Sticking with the stagflation theme, year-ahead household income and spending growth expectations declined by 0.1 percentage point to 3.0 percent and 4.9 percent, respectively.

There was slightly more cheer in consumers’ labor market expectations, where the probability of leaving one’s job voluntarily in the next twelve months increased to 20.4% from 19.1%, and the mean perceived probability of finding a job in the event of job loss increased to 52.7% from 52.3% in August.

Hilariously, median year-ahead expected growth in government debt declined by 1.1 percentage points to 8.0%, reaching the measure’s lowest level since February 2020. Spoiler alert: it will be much, much higher.

And confirming that many of the respondents are absolutely clueless, the mean perceived probability that the average interest rate on saving accounts will be higher 12 months from now decreased by 1.5 percentage points to 25.1%. Yes, about 25% of households have no idea that the Fed is now cutting rates and rates on savings accounts will be much lower in 12 months… unless of course we get hyperinflation in the next 3-9 months and the Fed panics into a hiking frenzy

Last but not least, the mean perceived probability that U.S. stock prices will be higher 12 months from now increased by 1.0 percentage point to 40.3%. It was unclear how many bulls also expected lower rates in the coming year.

Overall, an ugly, stagflationary survey, and hardly what the Fed may have expected to see several weeks into the first easing cycle since the global economy was shut down by a genetically engineered flu virus in 2020.

Tyler Durden

Tue, 10/15/2024 – 15:00

via ZeroHedge News https://ift.tt/X7ptzOd Tyler Durden