President Joe Biden will be in Wisconsin on Oct. 8 to announce a $2.6 billion investment to replace lead pipes, according to senior administration officials.

The funding was allocated under the 2021 Bipartisan Infrastructure Law, which set aside $15 billion over five years for replacing lead pipes. The Clean Water State Revolving Fund under the bill gives an additional $11.7 billion that can be used toward this effort.

While in Milwaukee, Biden will also announce a finalized Environmental Protection Agency (EPA) rule that requires water systems nationwide to replace lead service lines within a decade. The new standard for the action level—or how much water in a water system is contaminated—of pipes will be 10 parts per billion. The current standard is 15 parts per billion.

Sen. Tammy Baldwin (D-Wis.), who is running for reelection, will not be with the president as he makes the announcement.

“Senator Baldwin had a previously scheduled event at a family farm in Eau Claire to receive the American Farm Bureau Federation’s ‘Friend of Farm Bureau’ award recognizing her leadership fighting for America’s hardworking farmers, growers, and producers,” the senator’s communications director, Eli Rosen, told The Epoch Times.

One senior administration official said Baldwin is “an amazing partner in this administration and leading the charge in the Bipartisan Infrastructure Law.”

Under the EPA rule, at least 49 percent of the funding must be provided to disadvantaged communities as funds that do not need to be repaid. The rule updates what is called the Lead and Copper Rule, which was first enacted in 1991.

“The EPA’s new lead rule will begin to reverse the massive public health disaster of lead-contaminated tap water that has affected generations of our children. Every person has a right to safe and affordable drinking water, no matter their race, income, or zip code,” said Manish Bapna, president and CEO of the Natural Resources Defense Council, in a statement obtained by The Epoch Times.

Additionally, the EPA announced a $35 million grant program to address lead in drinking water.

The administration has already allocated approximately $30 million from the signature legislation for Milwaukee, Wisconsin, to replace all 3,400 of its lead pipes within a decade.

EPA Administrator Michael Regan warned about the effects of humans drinking water from lead pipes as “there is no safe level.”

“In children, lead can severely harm mental and physical development, slow down learning and irreversibly damage the brain. In adults, lead can cause increased blood pressure, heart disease, decreased kidney function, and cancer,” Regan told reporters on a call.

In May, the administration announced $3 billion to replace toxic lead pipes in Wilmington, North Carolina.

As many as 9 million homes, many of which are in underprivileged neighborhoods, receive water coming from lead pipes, according to the EPA.

“This is a matter of public health, a matter of environmental justice, a matter of basic human rights, and it is finally being met with the urgency it demands,” Regan said.

According to another senior administration official, 99 percent of cities with lead pipes will have them replaced within 10 years.

Finally, the EPA said that the new rule meets legal muster and will be beneficial.

“If you look at protecting up to 900,000 infants from being born with low birth weight for the reducing of 1500 cases of premature death from heart disease, the cost benefits are at a 13 to one ratio,” the official said.

“This is an opportunity to reduce lead exposure to millions of families all across the country, and we believe we’ve done it in a very strategic way, a legally sound way, supported by the science and the health benefits of this rule are undeniable.”

US Antitrust Officials Consider Google Breakup As ‘Trustbusting Era’ May Return

The US Department of Justice and a group of states submitted a document detailing a proposed remedy framework in the ongoing antitrust case against big tech giant Google. The case centers around Google’s violations of Section 2 of the Sherman Act for illegally maintaining monopolies, including general search services and text advertising.

On Aug. 5, US District Judge Amit Mehta, Washington, DC, ruled that Google violated antitrust law by spending billions of dollars to create an illegal monopoly as the world’s default search engine on smartphones, computers, and tablets. The ruling paved the way for antitrust enforcers to submit a 32-page document on Tuesday that explained the potential remedies for the judge to consider as the case moves into the remedy phase.

On page 9 of the remedy framework document, the DoJ specifies the government has a “full range of tools previously identified such as structural and additional behavioral remedies as well as term extensions” to restore competition in the marketplace that would modify Google’s business from using products such as its Chrome browser or Android operating system to create advantages for the big tech firm’s search engine.

“Fully remedying these harms requires not only ending Google’s control of distribution today, but also ensuring Google cannot control the distribution of tomorrow,” DoJ said.

Antitrust enforcers said Google colluded with other big tech companies to make its search engine the default option on devices.

Google Vice President of Regulatory Affairs Lee-Anne Mulholland wrote in the post that the DoJ’s remedy framework is “radical” and could have “negative unintended consequences for American innovation and America’s consumers.”

Google’s market capitalization (as of Tuesday’s close) of just a little over $2 trillion makes it the world’s fourth-largest company. Mounting legal pressure sent shares down around 1% in premarket trading in New York.

Antitrust pressure has been building, with multiple cases being pushed against Google. It also faces the threat of breakup in a separate government lawsuit centered around its online advertising business.

Across the Atlantic, European Union watchdogs have voiced similar concerns with antitrust enforcers in the US about the need to break up Google’s businesses. EU competition chief Margrethe Vestager recently said that “divestiture is the only way” to settle these worries with the big tech firm.

Daniel Ives, managing director and senior equity analyst at Wedbush Securities, commented on Google’s potential breakup, indicating it’s “unlikely at this point despite the antitrust swirls,” adding, “Google will battle this in the courts for years.”

There has been a four-decade lull in the government breaking up major companies. The last major one came with the 1984 breakup of AT&T. Before that, the 20th century was considered the ‘trustbusting era’, with Standard Oil, American Tobacco, and a railroad trust known as Northern Securities forced to spit up by the government.

Futures Drop On DOJ’s Google Crackdown, China Plunge

US equity futures are lower on news that the DOJ is considering a breakup of Alphabet’s Google search engine, in what would be a historic antitrust crackdown on Big Tech; Europe was flat while Asian markets slumped after Chinese A-shares suffered their biggest one-day plunge since February 2020 as investors are getting restless and demand stimulus actions from Beijing instead of just more words. As of 8:00am ET, S&P and Nasdaq futures are down 0.1%, but off session lows, with megacap tech stocks mixed: NVDA rises 1.4%, while Alphabet shares fell about 1.5% after the US Justice Department said it’s considering asking a federal judge to force Alphabet’s Google search engine to sell off parts of its business. Yields remain largely unchanged, the 10Y TSY yielding 4.03%, while the US Dollar rises. Oil prices failed to rebound, and slid to session lows, down 0.5% despite nervousness around Israel response and anticipation on China stimulus. Outside US, China finance ministry unveiled a press conference plan on Saturday; New Zealand Central Bank surprisingly cut 50bp.

In premarket trading, Boeing slid 1% after S&P said the company could be downgraded to junk; Boeing also said negotiations to end an almost monthlong strike collapsed. Alphabet slipped about 1% after the US Justice Department told a federal judge it’s considering recommending that Google be forced to sell off parts of its operations. Here are some other notable premarket movers:

Astera Labs jumps 12% after the company introduced a new portfolio of switches for AI workloads. Morgan Stanley views this as a reason to buy the stock.

Crinetics Pharmaceuticals declines 2% as the drug developer offers $400 million in shares via Leerink Partners and Morgan Stanley.

Helen of Troy rises 14% after the consumer products company behind Hydro Flask water bottles reported second-quarter net sales and adjusted earnings per share that exceeded Wall Street projections.

Zeta Global gains about 4% on an agreement to buy email marketing platform LiveIntent for $250 million in cash and stock plus a potential earnout.

While fears of antitrust crackdowns on Big Tech have been around for a while, the prospect of an actual breakup push is weighing on sentiment, said Kevin Thozet, a member of the investment committee at French asset manager Carmignac. However, he downplayed the eventual impact, because “at the end of the day, when we are looking at individual values of those separate business lines within Google, investors could be better off.”

Meanwhile, investors are monitoring clues on the outlook for interest rates. The 10-year US Treasury yield hovered above the key 4% level after diminished expectations for interest-rate cuts triggered a run of selling in previous days. The latest speeches from Fed Vice Chair Philip Jefferson and Atlanta Fed chief Raphael Bostic pointed to a measured approach.

Carmignac’s Thozet is among those expecting the Fed to slow the rate-cutting pace after September’s 50 basis-point move, as “the probability of a recession on the one hand is falling and probability of no landing is increasing.”

Globally, however, rate-setters are turning more dovish. A European Central Bank rate cut next week is very probable, Governing Council member Francois Villeroy de Galhau said. New Zealand cut rates by half a percentage point, stepping up the pace of easing, while India’s central bank opened the door for its first cut in four years.

In Europe, the Stoxx 600 index was flat despite Chinese stocks listed onshore suffering their biggest drop in more than four years. Real estate and automobile shares gained, while banks and travel stocks are the biggest laggards. Among individual movers, luxury goods firm Kering SA jumped as much as 1.3% on the news of a new CEO for its Gucci brand, while renewable energy companies were lifted by an International Energy Agency report predicting massive growth in renewable power capacity. Here are the most notable European movers:

Continental shares gain as much as 6.3% after the German tiremaker held a pre-close call that reassured analysts about its earnings outlook, amid gloomier profit warnings in the sector

Mondi shares gain as much as 4.3%, the most in over three months, after the paper and packaging company agreed to buy a variety of assets in Western Europe from Schumacher Packaging at an enterprise value of €634 million

United Utilities is the best performer on the Stoxx 600 utilities index on Wednesday, climbing as much as 2.8% after RBC upgraded to outperform, switching its preferences within the UK water sector

Kering advances as much as 2.1% after the company named Stefano Cantino as the new CEO of its Gucci label. The ex-Louis Vuitton exec’s appointment is a positive, though he has “a lot of work to do” to turn around the luxury brand, analysts say

Lonza shares advance as much as 1.7%, best performer in the Swiss Market Index on Wednesday morning, after Goldman Sachs initiated coverage on the drug ingredients maker with a buy recommendation

Redcare Pharmacy shares gain as much as 2.6% after Deutsche Bank raised the online pharmacy’s price target to a new Street high, saying the electronic prescribing ramp-up is showing good growth in Germany in 3Q

CMC Markets shares rise as much as 7.5%, most since June, after the online trading and spread-betting platform said it returned to profit in the first half of the financial year

ING Groep drops as much as 3.8% and is the worst performer in the Stoxx 600 banks index on Wednesday after Deutsche Bank downgraded to hold, removing its buy rating from the lender for the first time in eight years

Zealand Pharma slips as much as 4.5% after the Danish biotech company said it got a Complete Response Letter from the US FDA in relation to its new drug application for dasiglucagon for the prevention and treatment of hypoglycemia in pediatric patients with congenital hyperinsulinism

Earlier in the session, Asian stocks were dragged lower by Chinese shares, which tumbled on growing skepticism over Beijing’s stimulus plans and soft economic data. The MSCI Asia Pacific Index fell as much as 0.6%, declining for a second session, led by Chinese tech names including Tencent Holdings Ltd. and Alibaba Group Holding Ltd. The onshore benchmark CSI 300 Index slumped 7.1%, the most since February 2020, while Chinese stocks listed in Hong Kong also fell. Chinese equities are coming under pressure as investors reassess the outlook for the country’s recovery after a key policy meeting Tuesday yielded little fresh stimulus and holiday-spending data underwhelmed. While the gauges pared declines after the Ministry of Finance said it would hold a Saturday briefing on fiscal policy, selling soon resumed as traders doubted there will be a major spending boost.

“The market’s cautious reaction suggests investors might be waiting for more than just announcements – they want actual fiscal action,” said Billy Leung, an investment strategist at Global X Management. “If the MOF doesn’t deliver solid details, the market could stay volatile.”

In FX, the Bloomberg Dollar Spot Index is up 0.1%, rising for an eighth straight day and set for its longest winning streak since April 2022 as traders priced less US monetary easing. The kiwi dollar is the weakest of the G-10 currencies, falling 0.9% against the greenback to its lowest in seven weeks after the RBNZ stepped up their easing pace with a 50 bps interest rate cut. USD/JPY rises 0.3% to 148.60. Traders will be watching now for minutes from last month’s Fed meeting, later on Wednesday, while US inflation data is due Thursday.

In rates, treasuries dropped after plying narrow ranges during Asia session and European morning. 7- to 30-year yields are about 2bp cheaper on the day with 10-year around 4.03%, lagging bunds and gilts by ~2bp in the sector. Curve spreads, though steeper, remain within 2bp of Tuesday’s close ahead of a busy day of Fed speak and US inflation data on Thursday. Bunds and gilts outperform with more Treasury auctions on deck: $39b 10-year reopening at 1pm New York time and $22b 30-year reopening Thursday. Also Wednesday, six Fed officials have scheduled appearances.

In commodities, oil prices advance, with WTI rising 1% to $74.30. Spot gold falls $4 to $2,617/oz.

Looking at today’s calendar, we get August wholesale inventories at 10am. Fed speakers scheduled include Bostic (8am), Logan (9:15am), Goolsbee (10:30am), Jefferson (12:30pm), Collins (5:30pm) and Daly (6pm), and minutes of FOMC’s September meeting are due out at 2pm.

Market Snapshot

S&P 500 futures down 0.3% to 5,783.50

STOXX Europe 600 little changed at 517.05

MXAP down 0.2% to 191.61

MXAPJ down 0.4% to 608.47

Nikkei up 0.9% to 39,277.96

Topix up 0.3% to 2,707.24

Hang Seng Index down 1.4% to 20,637.24

Shanghai Composite down 6.6% to 3,258.86

Sensex up 0.4% to 81,945.46

Australia S&P/ASX 200 up 0.1% to 8,187.38

Kospi down 0.6% to 2,594.36

German 10Y yield little changed at 2.24%

Euro down 0.2% to $1.0958

Brent Futures up 0.8% to $77.76/bbl

Gold spot down 0.2% to $2,616.79

US Dollar Index up 0.13% to 102.68

Top Overnight News

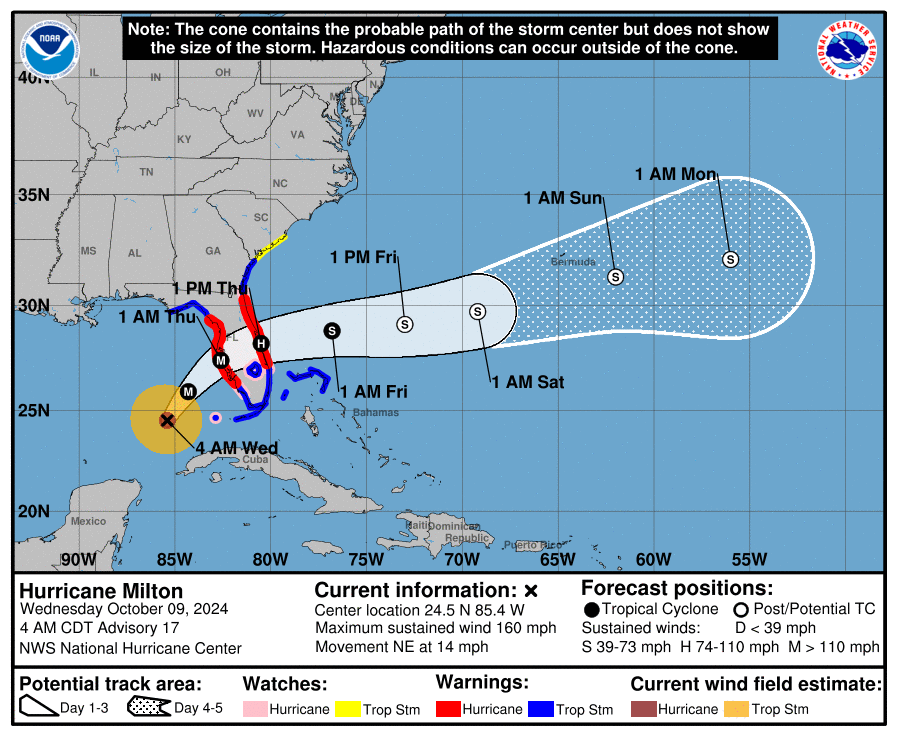

Hurricane Milton churned toward Florida’s west coast as a Category 5 storm and is expected to make landfall overnight. The NHC forecasts a storm surge into Tampa Bay as high as 15 feet. BBG

The Justice Department submitted a filing that presented a federal court with a range of potential options—from conduct restrictions to a breakup—aimed at ending what a judge said was Google’s unlawful monopoly in search. The filing said the government is considering a “full range of tools” to restore competition, including “structural” changes to Google’s business that would prevent it from using products such as its Chrome browser or Android operating system to advantage Google’s engine search. WSJ

China’s finance ministry announced plans for a media briefing on Saturday, sparking hope for fresh fiscal stimulus announcements. WSJ

China consumer spending over the recent Golden Week holiday was relatively subdued, underscoring the need for government stimulus. CNBC

India’s central bank left rates unchanged, as expected, but shifted its forward guidance in a dovish direction (the policy bias is now neutral). WSJ

Greece’s central bank governor says the ECB should slash “highly restrictive” rates as inflation will likely be back to target by H1:25. FT

Couche-Tard boosted its offer for Seven & I to 7 trillion yen ($47.2 billion) last month, people familiar said. That’s a 20% premium to the prior — rejected — offer and the company’s stock price from yesterday. BBG

Rio Tinto agreed to buy Arcadium in an all-cash deal that values it at $6.7 billion, a 90% premium to its Oct. 4 closing price. BBG

Fed Vice Chair Jefferson said the Fed rate cut recalibrated policy to maintain the strength of the labour market and noted that economic growth is solid, inflation has eased substantially, and the labour market has noticeably cooled. Jefferson said he will watch the incoming data, evolving outlook, and balance of risks in considering additional policy rate adjustments and his approach to policymaking is to make decisions meeting by meeting. Furthermore, he said the Fed has not changed its approach to monetary policy and is always thinking about the balance of risks, as well as noted the size of the September rate cut was timely and that the Fed’s rate cut was neither proactive nor reactive: BBG

Fed’s Collins (2025 voter) said further rate cuts are likely needed, and future action is to be data-driven, while she added that September Fed forecasts predicted 50bps of cuts into year-end. Furthermore, Collins is more confident of inflation being on a durable path of ebbing and said core inflation has moderated but is still elevated: Barron’s

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed and initially took impetus from the positive performance on Wall St where the major indices were led higher amid a tech rally, although Chinese stocks clouded over sentiment following the recent stimulus-related disappointment. ASX 200 eked marginal gains as strength in tech and telecoms offset the losses in the commodity-related industries. Nikkei 225 was underpinned at the open and climbed back above the 39,000 level but with gains capped by a lack of drivers. Hang Seng and Shanghai Comp were mixed as the Hong Kong benchmark fluctuated between gains and losses, with a late boost derived from reports China’s Finance Ministry is to hold a press briefing on fiscal policy and economic development on October 12th. The mainland was pressured after the recent stimulus-related disappointment and amid China’s ongoing trade frictions with the EU and US.

Top Asian News

China’s Finance Ministry is to hold a press briefing on fiscal policy and economic development on October 12th at 10:00 local time (03:00BST/22:00EDT), while it will introduce details of intensifying fiscal policy adjustment.

China’s Finance Ministry says they are to continue policy coordination with the PBoC and keep stable development of the bond market. To provide appropriate market conditions for PBoC treasury bond trading. Ministry and PBoC agree that treasury bond trading improves the monetary policy toolkit and improves liquidity management.

RBNZ cut the OCR by 50bps to 4.75%, as expected, while it stated that New Zealand is now in a position of excess capacity and that low import prices have assisted disinflation. RBNZ noted that the Committee assessed annual consumer price inflation within its 1-3% target and it was appropriate to cut the OCR by 50bps to achieve and maintain low and stable inflation. RBNZ Minutes stated the Committee confirmed future changes to the OCR would depend on its evolving assessment of the economy and noted the OCR of 4.75% is still restrictive and leaves monetary policy well-placed to deal with any near-term surprises. Furthermore, the Committee discussed the respective benefits of a 25bps cut versus a 50bps cut in the OCR and stated that a 50bps cut at this time is most consistent with the mandate of maintaining low and stable inflation, while it added the economic environment provides scope to further ease the level of monetary policy restrictiveness.

RBI kept the Repurchase Rate unchanged at 6.50%, as expected via a 5-1 vote (prev. 4-2) and it unanimously voted to switch its stance to neutral (prev. remaining focused on the withdrawal of accommodation), while Governor Das stated that macroeconomic parameters of inflation and growth are well balanced although the moderation in headline inflation is expected to reverse in September and remain elevated in the near term. Das also noted that the growth story remains intact, and prospects of private consumption look bright but added that there is difficulty in navigating the last mile of disinflation and significant risks to inflation still stare at them.

European bourses, Stoxx 600 (U/C) are mixed, in what has been a choppy session thus far; indices opened around flat, and have traded indecisively on either side of the unchanged mark. European sectors are generally firmer, albeit with the breadth of the market fairly narrow vs initially opening with a slight defensive bias. Optimised Personal Care is towards the top of the pile, alongside Media whilst Banks and Tech lag. US Equity Futures (ES -0.1%, NQ -0.2%, RTY -0.3%) are very modestly in the red, taking a breather from the gains seen in the prior session; some of the pressure could be attributed to the Google antitrust case. In recent trade, futures have been edging off worst levels. US Justice Department outlines potential remedies in Alphabet’s (GOOGL) Google antitrust case with the US said to be weighing a Google breakup as a remedy in monopoly case, according to Bloomberg. Says it will respond to the DoJ’s ultimate proposals as the Co. makes its case in court next year, while it is concerned the DoJ is already signalling requests that go far beyond the specific legal issues in this case.

Top European News

UK Chancellor Reeves is pushing ahead with plans to borrow billions of pounds extra for infrastructure investment despite concerns about an increasing cost of UK government debt, with Reeves likely to free up GBP 10bln-20bln worth of borrowing room for capital investment by excluding the losses incurred by the state from the BoE’s previous asset purchase programs when calculating debt, according to The Guardian.

ECB’s Stournaras sees the case for two more rate cuts in the Eurozone this year and further easing in 2025, while he said inflation could be on track to meet the ECB’s target in H1 2025, according to FT.

ECB’s Villeroy says a decrease in ECB rates is “very likely” and will not be the last; French economy is resilient, via Bloomberg.

ECB’s Kazimir says he is not worried about the ECB undershooting the 2% goal; not as convinced as media reports on an October cut. Key information will be available in December.

EU is to robustly challenge at the WTO level the announced imposition of provisional anti-dumping measures by China on imports of Brandy from the EU and is to assess all possibilities to offer appropriate support to EU producers from situations of market disturbance, or threat thereof.

Banks are reportedly pushing the UK to soften its approach to deferred bonuses/clawbacks, via Bloomberg citing sources.

FX

USD is broadly stronger vs. peers after indecisive sessions on Monday and Tuesday. DXY has climbed to a 102.70 peak with focus on a potential test of 103; not breached since 16tth August. FOMC Minutes and a slew of speakers are due.

EUR is softer vs. the USD after a marginal session of gains yesterday, which saw the pair advance to a peak at 1.0996. Interim support kicks in via the 100DMA at 1.0932.

GBP is softer vs. the broadly firmer USD and flat vs. the EUR. Cable has slipped below its 50DMA at 1.3088 printing a trough at 1.3056.

JPY is marginally softer vs. the USD with not a great deal of fresh macro drivers to guide the pair. Ahead of the 150 mark, interim resistance is provided by the recent peak at 149.12 set on Monday.

NZD is the standout laggard across the majors after the RBNZ delivered a 50bps rate cut as expected whilst signalling the likelihood of further easing to come. AUD/USD have been stemmed by the rise in the AUD/NZD which vaulted to its highest level since July 31st. Furthermore, markets continue to focus on Chinese easing measures with the Finance Ministry set to hold a briefing on 12th October.

Fixed Income

USTs are firmer but with upside relatively modest in nature though, with USTs shy of Tuesday’s and Monday’s respective highs of 112-24 and 112-28+. FOMC Minutes and a slew of Fed speakers are due.

Bunds are firmer to the tune of 15 ticks and holding just shy of Tuesday’s 133.80 high, which is also just below Monday’s 134.03 peak. ECB speak today has had little impact on the complex, despite interesting commentary from Kazaks who noted that he is not as convinced as media reports on an October cut. The Bund auction passed with little issue.

Gilts are largely following peers, but did see some modest pressure following the UK Gilt auction, but downside which ultimately proved fleeting. Gilts currently around 96.82 after initially going as low as 96.65 following the auction.

UK sells GBP 3.75bln 4.25% 2034 Gilt: b/c 3.25x (prev. 2.84x), average yield 4.17% (prev. 3.757%), tail 0.9bps (prev. 1.3bps).

Germany sells EUR 0.408bln vs exp. EUR 0.5bln 0.00% 2036 and EUR 0.846bln vs exp. EUR 1bln 2.60% 2041 Bund.

Bond investors have to wait as long as a year to transfer investments from their account on the Treasury (TreasuryDirect) to a brokerage, via WSJ citing sources.

Commodities

Crude is firmer attempting to pare back the hefty declines seen in the prior session; focus today is on any geopolitical updates out of the Middle East and as Hurricane Milton is expected to make landfall on the Gulf coast of Florida later on Wednesday. Brent Dec resides in a USD 77.21-77.99/bbl parameter.

Subdued trade across the precious metals complex with some desks citing profit-taking in the absence of a geopolitical escalation yet, although an Israeli attack on Iran is looming. Spot gold currently sits in a USD 2,609.24-2,624.37/oz range.

Base metals are flat with a downward bias following yesterday’s sizeable losses induced by the disappointing Chinese NDRC press conference. 3M LME copper trades closer to the bottom end of a USD 9,719.50-9,855.50/t range.

NHC says Hurricane Milton is forecast to make landfall on the Gulf coast of Florida later on Wednesday, as a dangerous Major Hurricane.

US private inventory data (bbls): Crude +10.9mln (exp. +2.0mln), Distillate -2.6mln (exp. -1.9mln), Gasoline -0.6mln (exp. -1.1mln), Cushing +1.4mln.

Japanese aluminium premium for the October-December shipment has been set at USD 175/T, +1.7% Q/Q, via Reuters citing sources.

India Steel Secretary says steel demand will be more than previously predicted; green steel will be the way forward.

Carlyle Group Chief Strategy Office Jeff Currie says demand dynamic is oil supportive; says oil should be trading in the USD 80/bbl range, via Bloomberg TV.

Russia’s idle primary oil refining capacity has been revised up 67% in October, to 4.0mln/T.

Geopolitics: Middle East

“Dozens of Iranian lawmakers wrote to the country’s Supreme National Security Council calling for urgent action towards developing nuclear weapons as Israeli threats rise in the region”, according to Al Jazeera.

Iran has told Gulf Arab states that it would be unacceptable if they allowed the use of their airspace or military bases against Iran, and warned any such move would draw a response, according to a senior Iranian official cited by Reuters

Israeli PM Netanyahu confirmed that Israel took out Nasrallah’s successor, while it was separately reported that PM Netanyahu summoned ministers for security consultations on Tuesday evening.

Israeli PM Netanyahu had set two conditions for Defence Minister Galant to travel to the US and refused to approve the trip to Washington that had been planned for Tuesday night until he receives a phone call with President Biden and the Israeli cabinet approves the response to Iran’s missile attack, according to Axios sources.

Israeli senior official said they are going to respond to the Iranian attack and there is no question about it but will not do it in a way that will start an all-out war with Iran, according to Axios. It was also reported that Israeli officials cited by Washington Post said that the country is preparing a significant military response to Iran’s attack.

Israeli officials stated that Israel is capable of harming Iran but the possibility of its response requires coordination with the US, while Defence Minister Galant and security leaders push to strike Iran militarily and have already submitted the plans to the political leadership.

Israel’s Channel 12 reported that Washington and Arab countries are discussing with Tehran a proposal for a ceasefire on all fronts except Gaza which would be conditional on Hezbollah’s withdrawal to northern Litani and the dismantling of military structure near the border, according to Sky News Arabia.

White House said the US continues to have discussions with Israel on its response to the Iranian attack. It was separately reported that the White House said despite the fighting, they are working with Israel and Lebanon to define a process for a return to ceasefire negotiations,according to Asharq News

US officials cited by NBC do not believe that Israel has made a final decision on the details of the response to Iran and discussions with Tel Aviv included Washington providing intelligence support or even launching air strikes. However, Washington has not decided on any action despite its intention to support Israel’s right to defend itself and Israel did not inform Washington of plans to retaliate against Iran.

US officials feared that Israel will implement its response to Iran during the planned Israeli Defence Minister Gallant’s visit to Washington although the visit has since been postponed.

Islamic Resistance in Iraq said it attacked with drones a vital target in the north of the occupied territories, according to Al Jazeera.

North Korea’s army said it is to completely cut off roads and railways connected to South Korea from October 9th, according to KCNA.

US Event Calendar

07:00: Oct. MBA Mortgage Applications -5.1%, prior -1.3%

10:00: Aug. Wholesale Trade Sales MoM, est. 0.4%, prior 1.1%

10:00: Aug. Wholesale Inventories MoM, est. 0.2%, prior 0.2%

14:00: Sept. FOMC Meeting Minutes

Central Bank speakers

08:00: Fed’s Bostic Gives Welcome Remarks

09:15: Fed’s Logan Speaks at Houston Energy Conference

10:30: Fed’s Goolsbee Gives Opening Remarks at Payments Conference

12:30: Fed’s Jefferson Speaks on Discount Window

17:30: Fed’s Collins Speaks at Worcester Event

18:00: Fed’s Daly Speaks in Moderated Conversation

DB’s Jim Reid concludes the overnight wrap

While I’ve been away in Berlin for a couple of days my 9-yr old daughter Maisie has been on her first ever residential trip away with school. When I spoke to my wife last night she said that she was missing her so much as she was like a good friend to her. I said what about missing me!? She said “well that’s different”. Such is life. One thing we can be in agreement on though is that when the twin boys do the same trip next year, the peace and quiet will outweigh any missing them feelings.

While I’ve been travelling, the week has started off a bit all over the place and markets have put in another varied performance over the last 24 hours, with sharp differences across regions and asset classes. On the one hand, several risk assets did quite well, with the S&P 500 (+0.97%) closing in on its all-time high again, driven by a strong performance for the Magnificent 7 (+1.71%). However, China-exposed stocks have slumped thanks to disappointment over the scale of China’s stimulus, or at least the lack of detail provided so far, which also helped to drive a sharp downturn in oil prices, even as geopolitical risks remained high.

Those geopolitical risks stayed front and centre yesterday, as investors waited to see what form Israel’s response against Iran might take. Amir Ohana, the speaker of the Knesset, said yesterday that “discussions are still taking place at the highest levels regarding the outline of the response — but it will be significant, and it will come”. In turn, Iran have also warned that they would respond to any attack, with foreign minister Abbas Araghchi saying yesterday that “We advise Israel not to test our will”. So there are still significant fears about how the current situation could escalate. Later on, there was renewed uncertainty over future steps by Israel as the US Pentagon confirmed that a planned visit to Washington by Israel’s defence minister Yoav Gallant had been postponed. Bloomberg and other outlets reported that this came due to last-minute objections to the trip by Israel’s PM Netanyahu.

The latter news caused a decent spike in oil intra-day but the overall market tone was still one of a moderation in geopolitical risk pricing, in part following earlier comments by Hezbollah’s deputy leader that it backed efforts by Lebanon’s officials to reach a ceasefire. This saw Brent crude (-4.28%) fall back to $77.47/bbl, whilst WTI (-4.63%) posted its biggest daily decline of 2024. So that ends a run of five consecutive daily gains, in which oil prices saw their largest increase over 5 sessions since Russia’s invasion of Ukraine began in early 2022. Broader volatility also fell back, with the VIX index coming down -1.22pts to 21.42pts.

Those oil price declines were also driven by disappointment at the scale of China’s stimulus, which had already led to a slump in Chinese equities yesterday. That was echoed across a broader range of commodities too, mainly because of concern about Chinese demand, meaning that industrial metals put in a weak performance, with copper (-2.41%) seeing its biggest daily loss in over a month. Indeed, Bloomberg’s Commodity Spot Index (-1.58%) suffered its worst daily performance since June, albeit after a significant advance in the last month as US recession risks have eased and the geopolitical situation in the Middle East escalated.

That China news meant that equities in the US and Europe with China exposure also performed very poorly. For instance, the NASDAQ Golden Dragon China Index (made up of companies traded in the US who do a majority of their business in China) slumped by -6.85% yesterday, which was its worst daily performance since October 2022. A similar pattern was clear in Europe, where the CAC 40 (-0.72%) was one of the weakest European indices given its concentration of luxury goods firms. Meanwhile in Germany, the DAX fell -0.20%, with several automakers leading the decline given their exposure to China as well, and the STOXX 600 was down -0.55%.

By contrast, US equities posted renewed gains, with the S&P 500 (+0.97%) ending the day just two tenths of a percent from its all-time high on September 30. That was primarily driven by the Magnificent 7 (+1.71%), with the moves in the two indices near mirror images of Monday’s declines (-0.96% and -1.86%). All of the Mag-7 were higher on the day, with Nvidia (+4.05%) extending its 5-day gain to +13.58%. On the other hand the small-cap Russell 2000 (+0.09%) posted only a minor advance, while energy (-2.63%) and materials (-0.37%) sectors within the S&P 500 declined amid the reversal in commodities.

For rates it was a quieter day, but ultimately most sovereign bonds rallied, as the commodity price declines helped to ease concerns about inflationary pressures. For instance, the US 10yr yield was down -1.4bps to 4.01%, but that was entirely driven by lower inflation breakevens, as the 10yr real rate was actually up +1.1bps to 1.73%. Meanwhile at the front end, the 2yr yield came down -3.7bps to 3.96%. In Europe, there were similar modest gains, with yields on 10yr bunds (-1.2bps), OATs (-1.4bps) and BTPs (-2.8bps) all moving lower.

These bond gains came even as near-term pricing of Fed and ECB rate cuts was flat to slightly lower on the day amid some cautious commentary. The Fed’s Collins noted that “a careful, data-based approach to policy normalization will be appropriate”, suggesting that further large cuts are unlikely as things stand. A similar tone was visible from ECB’s Centeno who said “we have to be cautious — maintain gradualism in decisions”. So one of the of the most dovish ECB voices alluding to a high bar for more aggressive cuts. Later in the evening, Bundesbank’s Nagel commented that a Trump victory in the US election could lead to US policy shifts that “could lead to noticeable losses in growth” and “also bring inflation risks for the euro area and Germany”.

In Asia Chinese markets are continuing to reverse from their post holiday opening highs yesterday with the CSI down -6.95% and the Shanghai Composite falling -5.30%. The Hang Seng is also down -1.74%, extending its losses after the worst drop (-9.41%) since 2008 the previous day. In contrast, the Nikkei is up +0.62% and the S&P/ASX 200 has gained +0.11%. South Korean markets are closed for a public holiday. S&P 500 (-0.16%) and NASDAQ 100 (-0.25%) futures are lower with Google under pressure given the DoJ pronouncements overnight that the company may be forced to be broken up in the continued antitrust case around their online search monopoly.

In monetary policy news, the Reserve Bank of New Zealand has cut interest rates by 0.5 percentage points, lowering the Official Cash Rate from 5.25% to 4.75%. This marks the central bank’s second consecutive reduction, following a quarter-point cut in August. Following the decision, the New Zealand dollar has weakened by – 0.86%, trading at 0.6086 against the US dollar, as the RBNZ expressed a cautious outlook on the economy, suggesting the possibility of further cuts.

There wasn’t much data again yesterday, although German industrial production did grow by a stronger-than-expected +2.9% in August (vs. +0.8% expected). Otherwise, the US trade deficit for August came in at $70.4bn (vs. $70.5bn expected). Finally, the Atlanta Fed’s latest estimate for Q3 GDP in the US now stands at 3.2% following yesterday’s update.

To the day ahead now, and we’ll get the minutes from the September FOMC meeting, and also hear from plenty of central bank speakers, including Fed Vice Chair Jefferson, the fed’s Bostic, Logan, Goolsbee, Collins and Daly, along with the ECB’s Elderson and Villeroy. Data releases include the German trade balance for August.

Energy has become a hot-button issue as voters prepare to head to the polls, with Republicans gaining a narrow upperhand. According to a recent Rasmussen poll, 82% of likely U.S. voters see energy policy as an important factor in the upcoming election. With rising fuel costs and the future of domestic energy production hanging in the balance, this topic could prove even more pivotal.

The poll indicates that Republicans hold an edge over Democrats when it comes to trust on energy issues.

The poll surveyed 1,044 likely U.S. voters, conducted on September 26 and September 29-30. The poll asked “In terms of how you will vote in this year’s election, how important is the issue of energy policy?”

82% of the respondents categorized U.S. energy policy as important, including 45% who felt it was very important.

When asked, “Which political party do you trust more to handle energy policy?” the result was not as clear, with 44% trusting the Republic party more, 43% trusting Democrats more, and 12% undecided.

While Democrats have focused on renewable energy and climate action, Republicans have honed in on energy security and affordability, particularly through oil, gas, and fossil fuels.

Voters are feeling the pinch of higher prices at the pump and rising home heating costs, which may explain the trust in the GOP’s approach to energy policy.

The push for continued exploration, investment in fossil fuels, and regulatory rollbacks appears to be resonating—but perhaps not the clear winner that some seem to believe.

The Rasmussen poll had a sampling error of +/- 3 percentage points, with a 95% level of confidence.

Milton Barrels Towards Tampa-Area As A Cat. 5 Hurricane

Milton strengthened overnight into a devastating Category 5 hurricane with maximum sustained winds in excess of 160 mph. The National Hurricane Center reported early Wednseday that Milton was located about 300 miles southwest of Tampa, traversing the warm waters of the Gulf of Mexico towards the northeast at 14 mph.

“On the forecast track, the center of Milton will move across the eastern Gulf of Mexico today, make landfall along the west-central coast of Florida late tonight or early Thursday morning, and move off the east coast of Florida over the western Atlantic Ocean Thursday afternoon,” NHC wrote in an advisory note.

The latest forecast states Milton will make landfall near Sarasota between 0200 ET and 0600 ET Thursday morning as a Category 4 storm.

One of the main concerns across the Tampa to Sarasota region will be the storm’s dangerous eye and eyewall unleashing record storm surges. Warnings have already been posted for much of Florida’s western coast.

“Tampa is on a knife’s edge, but Sarasota, Siesta Key, Venice, Englewood, Port Charlotte, and Punta Gorda continue to look to experience the worst of the storm surge under this scenario,” Ben Noll, a meteorologist with New Zealand’s National Institute of Water & Atmospheric Research, wrote on X.

The overnight ECMWF nudges slightly north with #Milton, with the eye forecast to pass near the southern end of Tampa Bay.

Tampa is on a knife’s edge, but Sarasota, Siesta Key, Venice, Englewood, Port Charlotte, and Punta Gorda continue to look to experience the worst of the… pic.twitter.com/DAqnVxHJ4v

As of early Wednesday, #Milton remained a category 5 storm with a central pressure of 907 hPa, continuing to rank in the top-10 most intense Atlantic hurricanes on record from a pressure perspective.

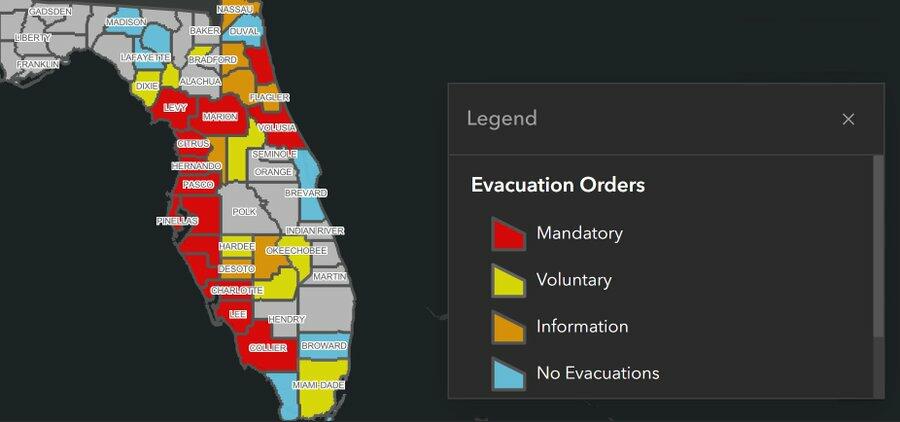

Since Sunday, evacuations in the state have been the largest since 2017.

According to the Florida Division of Emergency Management, here are the areas under mandatory evacuation orders:

Charlotte County; Citrus County; Collier County; Hillsborough County; Hernando County; Lee County; Levy County; Manatee County; Pasco County; Pinellas County; Sarasota County; St. John’s County and Volusia County;

And voluntary evacuation orders:

Glades County; Okeechobee County; Dixie County; Hardee County; Miami-Dade County and Union County.

Evacuation order map:

GTFO.

Officials are urging residents along Florida’s Gulf Coast to evacuate ahead of Hurricane Milton, with the Tampa mayor saying, “If you choose to stay in one of those evacuation areas, you’re going to die.” pic.twitter.com/NTg683IJRH

A mass evacuation is in progress in Sarasota, Florida, following the upgrade of Hurricane Milton to a Category 5. Here’s a look at the northbound traffic on I-75 as residents make their escape.@MyRadarWX#flwx#hurricane#miltonpic.twitter.com/vC2pEvxLR2

Meanwhile, Tampa-area Sheriff Chad Chronister of the Hillsborough County Sheriff’s Office told residents anyone who has not evacuated is “on their own.”

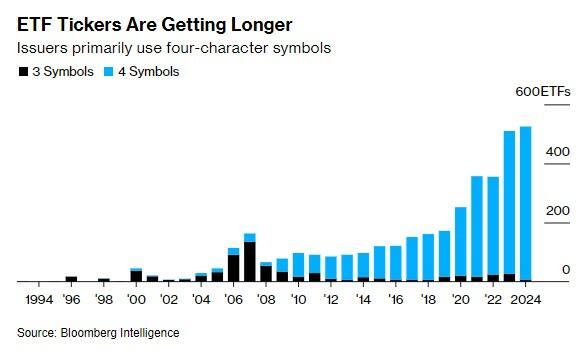

There’s So Many Single-Stock ETFs, We’re Running Out Of Ticker Symbols

“Competition for them has never been fiercer. In a way similar to ‘cybersquatting,’ we can see market participants constantly grabbing tickers, especially as certain sectors or themes become more crowded.”

Those were comments by Gavin Filmore, chief revenue officer of white-label firm Tidal Financial Group, to Bloomberg, addressing the accelerating depletion of ticker symbols for use by ETFs on U.S. markets.

As a new article notes, securing a catchy ticker for ETFs has now become a “high-stakes” challenge in the $10 trillion market, especially for funds tracking individual stocks.

With US exchanges allowing only four-character tickers, the potential combinations are vast—456,976 in theory, according to Bloomberg. But for single-stock ETFs, the options shrink drastically since the ticker must incorporate the stock symbol it’s based on.

One example is MSTR-related ETFs, where MST- should be in subsequent ETFs to identify them (since MS is taken), leaving just 52 choices – placing 1 of 26 letters before or after the ‘MST’.

The Bloomberg report says that in the crowded ETF space, a snappy ticker is more than just branding—it can lead to lower spreads and better liquidity. That’s why issuers are scrambling to secure unique symbols, sometimes resorting to hoarding, as the competition heats up.

Matthew Tuttle, chief executive officer of Tuttle Capital and most famous for his SARK anti-Cathie Wood ETF, told Bloomberg: “There are guys who are going to stockpile symbols — maybe me, for example — and on the good names, you are potentially going to run into an issue.”

“You also really want like the ‘U’ or something like it for the bull, and a way to discern between the bull and the bear if you do both sides,” he added.

Will Rhind, CEO of GraniteShares, says it’s getting tougher to secure tickers for single-stock ETFs as exchanges increasingly reject their requests due to reserved or delisted symbols. Some believe expanding the character limit could offer issuers more flexibility, as four-letter tickers have dominated new ETF launches for nearly 15 years, according to Bloomberg Intelligence.

But that doesn’t seem to be in NASDAQ’s plans.

“I don’t think there are any concerns today around a ticker shortage. We do occasionally get questions from companies saying, hey, how can I get more creative on these tickers? Can I include numbers in addition to letters?” said Jeff Thomas, its chief revenue officer and global head of listings.

Rhind concluded, talking about the idea of adding numbers to tickers: “I personally think that would be a good addition. Certainly for leveraged products, that makes all the difference in the world. All our products in Europe follow that naming architecture, so I think that does help and would add some additional breathing space for people who find it difficult to find tickers.”

In the midst of growing demand for low-carbon base-load electricity, nuclear power is increasingly regarded as a clean, reliable option; but multi-year regulatory approval processes, a dearth of capital, and chronic cost overruns when constructing new plants have made utilities reluctant to build.

For many in the nuclear power industry, one way to address these issues is to become smaller.

Small Modular Reactors (SMRs) are nuclear reactors assembled from pre-manufactured components, which are generally 300 megawatts or less in size. They are designed to be cheaper and more flexible than larger-scale nuclear power plants, with enhanced safety features such as automatic shut-down technology.

By contrast to most existing nuclear reactors, which are uniquely designed for each site, SMRs offer the potential to expedite regulatory approvals and construction time, bringing costs down substantially.

“They bring more regulatory certainty and an ability to get through that process much more quickly,” Todd Abrajano, CEO of the U.S. Nuclear Industry Council, an industry advocacy group, told The Epoch Times.

“The fact that these designs can be modular,” Abrajano said, “that most of the construction can be done in-house, in a factory, and then assembled at the site, requires much less work and much less bespoke design.”

According to the U.S. Department of Energy (DOE), due to the smaller size of SMRs, they require less capital to build and can be sited in locations that are not possible for larger nuclear plants.

“Accordingly, the Department has provided substantial support to the development of light water-cooled SMRs, which are under licensing review by the Nuclear Regulatory Commission (NRC) and will likely be deployed in the late 2020s to early 2030s,” the DOE’s Office of Nuclear Energy states.

While Russia and China have taken the lead as the only countries currently operating SMRs, western nations are racing to catch up, envisioning huge new markets for both domestic energy production and exports. Today, there are more than 80 SMR designs in development across 19 countries, including the United States, the United Kingdom, Canada, Japan, and South Korea, according to the International Atomic Energy Agency.

A report by Natural Resources Canada projects that the global market for SMRs could exceed $150 billion by 2040. According to Valuates, a market analytics firm, the global market for SMRs was $4.13 billion in 2023 and is projected to reach $10.23 billion by 2030, an annual growth rate of approximately 14 percent.

In March 2023, GE Hitachi Nuclear Energy (GEH) announced that its SMR model BWRX-300 had “achieved a significant pre-licensing milestone” toward regulatory approval in Canada, and that deployment of this model is in various stages of planning or contracting in Estonia, Poland, as well as the United States.

Private Companies, Military Want SMRs

While power generation has to date been the domain of electric utilities, SMRs may also see demand from private companies.

Increasingly, tech companies are signing contracts to ensure a steady, reliable supply of electricity, and they are often choosing nuclear energy as that source.

In September, Microsoft inked a deal with Constellation Energy to restart the Unit 1 reactor at Three Mile Island, which famously shut down its Unit 2 reactor after an operating accident in 1979.

This reactor will provide power exclusively to Microsoft for the next 20 years. And while Three Mile Island uses standard-size reactors, other tech companies are looking to SMRs to power their data centers, including Amazon and Google.

Oil and gas companies, steel companies, and chemical companies are also potential customers. In March 2023, Dow and X-energy signed a joint development agreement to install an SMR at the company’s Seadrift industrial site in Texas.

SMRs are the ideal choice for companies that want a smaller, dedicated power source on-site versus being dependent on the electric grid. However, these companies typically lack the expertise to operate plants, nor do they want to take responsibility for waste disposal or assume the liability that comes with owning a nuclear reactor.

“The one thing I’m consistently hearing from industrial application end users is that they don’t want to own and operate a nuclear plant,” Abrajano said. “So there’s going to have to be a utility that’s running these, or there are a number of other companies that are now starting to pop up which are pure-play development companies that are looking to find sites and find customers, and then they will either own and operate those reactors and do long-term power purchase agreements or figure out another way to bring these things online going through a utility.”

The military is another market for SMRs.

A White House fact sheet issued on May 29 stated: “Small modular nuclear reactors and microreactors can provide defense installations resilient energy for several years amid the threat of physical or cyberattacks, extreme weather, pandemic biothreats, and other emerging challenges that can all disrupt commercial energy networks.”

While SMRs can be used to provide uninterrupted power to large military bases, microreactors can power forward operating bases. Microreactors are currently in use for submarines and aircraft carriers, and can be transported in an 18-wheel truck.

“When you think in terms of the size of a nuclear reactor, most people don’t think, as they’re driving down the highway, that they could be driving past a reactor that could be operational, but certainly that’s the case,” Abrajano said.

The portability of SMRs and microreactors means that they could be transported to natural disaster sites that have lost power. While the grid is being restored, smaller reactors can power essential facilities like hospitals and grocery stores.

Regarding regulatory approvals, the nuclear power industry anticipates a faster process due to a new bipartisan consensus, in which the left regards nuclear as a low-carbon energy source and conservatives see it as a means of providing continuous base-load power to meet the escalating demand for electricity.

Both the Biden and Trump administrations have been supportive of nuclear power, and Congress has recently thrown its support behind the industry as well.

Streamlining Approval Process

In July, the Accelerating Deployment of Versatile, Advanced Nuclear for Clean Energy (ADVANCE) Act was signed into law and is designed to streamline the approval process at the Nuclear Regulatory Commission (NRC) for new nuclear plants. Two issues that have plagued the nuclear power industry are the multi-year process of getting regulatory approvals, and construction that chronically exceeds budget and deadlines once approvals are in place.

Among the few recent nuclear reactors to be built in the United States, Plant Vogtle Units 3 and 4 in Georgia began commercial operations in July 2023 and April 2024, respectively. These reactors, designed by Westinghouse, were built with modules manufactured off-site and then assembled onsite, but were completed seven years behind schedule and went $17 billion over budget.

Together with Units 1 and 2, they comprise the largest nuclear power plant operating in America and provide a highly dense, reliable, and carbon-free energy source. By comparison, a wind farm that could produce the same amount of energy as Plant Vogtle would cover an area of more than 1,000 square miles, with a capacity factor—the amount of electricity it actually produces as a fraction of its installed capacity—of about one-third that of a nuclear power plant, due to its weather dependence.

According to Abrajano, the average time for the NRC to approve new nuclear plants has been about five years, but he estimates that, with the passage of the ADVANCE Act, regulatory approvals could be completed within 18 to 24 months. New, modular designs are already getting fast-tracked approvals.

In December 2023, a modular plant built by Kairos Power in Oak Ridge, Tennessee, received regulatory approval in just over two years. This plant, called Hermes, is a low-power reactor that uses a TRISO fuel pebble bed design with a molten fluoride salt coolant; it is expected to be operational by 2027.

As the nuclear power industry gears up to bring this new technology to market at scale, it is also assessing whether it still has the physical infrastructure and the human talent it needs, particularly given that America has built few new nuclear plants during the past 50 years. Despite initial ambitions in the 1970s to build as many as a thousand nuclear plants across the United States, only 54 plants, containing 94 nuclear reactors, are currently in operation, with an average age of 42 years old.

By contrast, China has been aggressively moving forward in building out its nuclear fleet.

Over the past decade, China added more than 34 gigawatts of nuclear power capacity. It now has 55 operating reactors, with 23 additional reactors under construction, according to a report by the U.S. Energy Information Administration (EIA).

“The United States has the largest nuclear fleet, with 94 reactors, but it took nearly 40 years to add the same nuclear power capacity as China added in 10 years,” the report states.

Does the US Have the Resources to Manufacture?

U.S. industry insiders say that, with so much manufacturing, including key energy infrastructure components like transformers, largely existing outside the United States, the nuclear industry currently lacks the resources it needs to produce at scale. Of the top 10 transformer manufacturers, General Electric is the only one that is based in the United States.

“We still have a lot of manufacturing as it relates to work done at SpaceX, and I would say we still produce a lot in terms of engine manufacturing,” Juliann Edwards, chief development officer of The Nuclear Company, told The Epoch Times. “And you see an increase of grant money coming out of the Department of Energy to serve universities as they invest more into nuclear engineering and the surrounding engineering functional areas, like materials and chemical and mechanical.”

The Nuclear Company plans to build nuclear plants according to a “fleet-scale model [that] combines using proven, licensed technology and a design-once, build-many approach,” a company press release states.

According to the U.S. News 2024 university rankings, the top-rated schools for nuclear engineering are the University of Michigan, Massachusetts Institute of Technology, North Carolina State University, University of California, University of Wisconsin, Texas A&M, University of Illinois, University of Tennessee, and Georgia Institute of Technology.

For younger students, the American Nuclear Society has established several K–12 programs to educate grade school students and teachers about opportunities in the nuclear energy field. This includes a science curriculum called “Navigating Nuclear,” and a “Nuclear Ambassadors” program to bring nuclear professionals into schools for classroom discussions.

“We have a foundation, but we’re behind right now and we’ve got to onshore a lot of the capabilities that we’ve lost,” Edwards said.

More than 11.5 million customers of privately owned utility companies in California will automatically receive an average credit of $71 on their October utility bills, Gov. Gavin Newsom said in an Oct. 2 statement.

The climate credits are intended to help “offset increases while preserving the incentive for customers to conserve energy and reduce [greenhouse gas] emissions,” according to the California Public Utilities Commission’s website.

Funding comes from the state’s cap-and-trade program, which regulates the amount of carbon produced by companies and requires those that exceed limits to pay fees.

Credit amounts vary for utility providers. The more than 5 million households that rely on the largest energy company in the state, PG&E, will receive $55.17.

About 46,000 Californians served by Pacific Power—an energy company operating in the far northern part of the state—will see the largest credits of $174.25.

Bear Valley Electric Service—offering power to 23,000 residents in the Alpine County region known for its ski area—customers will receive the smallest credit at $32.24.

“Not only does this credit provide much-needed relief for families, it’s helping Californians make the switch to cleaner energy,” Gov. Gavin Newsom said in the statement.

A similar credit was applied to customers’ bills in April, with the total for the year averaging $217.

Households have received an average of $971 in climate credits since 2014, amounting to more than $14 billion across the state, according to the governor’s office.

Some critics have said the state’s climate policies amount to high-priced fees that negatively affect consumers.

“To reduce greenhouse gases marginally in this state, we have this very expensive program called cap-and-trade, which is a hidden tax on energy,” Susan Shelley, a journalist based in Southern California, told EpochTV’s “Leaving California” documentary last year.

“It’s on utilities, it’s on refineries, it’s on manufacturing, it’s on everything.”

A study titled “Zapped: How California’s Punishing Energy Agenda Hurts the Working Class” published in 2022 found that higher utility prices were affecting millions of Californians.

“There is nothing unique about California that should cause the state’s electricity rates to be significantly higher than the rest of the country,” Wayne Winegarden wrote in a report analyzing the study.

“Instead, the results are the expected and desired outcome from … Sacramento’s energy policy agenda of recent years.”

The regulator in charge of overseeing the industry said the state’s green energy policies are, in part, responsible for rising electricity prices.

“This all comes at a cost,” Alice Reynolds, president of the California Public Utilities Commission, said during a March hearing of the Assembly’s Utilities and Energy Committee when questioned by lawmakers about energy prices.

“Any investment in clean energy technology … is funded through electricity bills.”

Lawmakers began discussing the cap-and-trade program in 2006, with an agreement reached in 2012, and the law took effect the following year.

Since then, energy prices have increased significantly in the state with more than a dozen increases since 2019. Californians paid about 67 percent more than the national average for electricity in 2022, and some Golden State residents pay more than five times the rate per kilowatt hour charged in the lowest-priced areas in the country, according to statistics from the U.S. Energy Information Agency.

Utility companies, including PG&E, included comments in rate request filings noting that some added costs are attributed to the state’s decarbonization strategy.

“We are also experiencing the impact of the State’s decarbonization strategy, particularly on our gas distribution system,” PG&E said in the 2021 filing.

“Numerous cities have adopted ordinances prohibiting gas appliances in new construction. The projected decline in throughput may lead to a declining base of core customers who will pay for our gas system costs, with rate increases needed to cover that gap.”

Legislators on both sides of the aisle pointed to the state’s climate agenda as contributing to the high cost of living in California.

“These energy mandates jacked up utility rates,” Republican Assembly Minority Leader James Gallagher told The Epoch Times on Feb. 26.

“All of this stuff has a cost.”

He said the state is forcing taxpayers and electricity and fuel consumers to pay for inefficient climate policies.

“All of this stuff we’ve been doing on climate is super-expensive, and it’s just going to get more expensive,” Gallagher said in March.

Lawmakers from the Democratic Party have also spoken about calls they were receiving from constituents concerned about energy prices jeopardizing their finances and the unintended consequences of some legislative policies.

“Rates are skyrocketing in California. The harsh reality is that millions of Californian families are at the breaking point right now,” Assemblywoman Cottie Petrie-Norris, chair of the energy committee, said during the March hearing while highlighting statistics that showed California has the highest utility rates in the nation. “Our constituents want to know what’s going on and more importantly, they want to know what we, as their elected officials, are doing to address this issue and contain costs.”

Businesses are also paying the price, she said.

“High energy prices are also a major challenge for California businesses, particularly our small businesses, who are struggling to keep their doors open, and, quite literally, keep their lights on,” Petrie-Norris said.

More than a million small businesses will also receive credits on their October bills, according to the governor’s Oct. 2 statement.

Denmark looks to commission a cross-border green hydrogen pipeline to Germany in 2031, three years later than the previous timeline, the Danish government said on Tuesday.

Denmark has been working with local transmission system operator Energinet to have the timeline to commissioning shortened to 2031, from 2032 as Energinet’s latest plan says, according to a statement from the Danish Ministry of Climate, Energy, and Utilities.

Energinet has been cooperating with Gasunie on the development of the Danish-German hydrogen network as part of a cooperation agreement. Initial plans envisaged that a cross-border transmission connection between Denmark and Germany would enable the transport of green hydrogen from 2028.

However, after Energinet’s market dialogue on the hydrogen infrastructure ended, the booking requirement was recalculated and the schedule updated, the operator said today.

“Several activities on the critical path have proven to be more extensive and time-consuming than originally anticipated. Therefore, Energinet now assesses that the ‘Lower T’ can be commissioned by the end of 2031 at the earliest, and the interconnections to Holstebro and Lille Torup by the end of 2032 and 2033,” the system operator added, referring to the initial and follow-up branches of the hydrogen network.

“We are still ready to bring state co-financing to the table if the industry commits to booking capacity in the pipeline,” said Lars Aagaard, Denmark’s Minister for Climate, Energy and Utilities.

The Danish Government will work on measures to support the possibility of commissioning the first part of the hydrogen backbone in 2031, it said today.

Green hydrogen has seen several setbacks in Europe recently, due to a lack of customers.

Most recently, Shell and Equinor have ditched plans for low-carbon hydrogen production and transportation in north Europe, due to a lack of demand.

Uncertainty around demand and incentives coupled with cost pressures are weighing on the global adoption of low-carbon hydrogen despite an uptick in final investment decisions in the past year, the International Energy Agency (IEA) said in a report last week.

The next year will be crucial for the French army, which has undergone a major transformation in recent years to prepare for a possible conflict with Russia, reports Politico.

Next May, thousands of French soldiers will take part in a large-scale military exercise in Romania. The purpose of the exercise is to assess how quickly they can reach NATO’s eastern flank if necessary, which is crucial if Russian President Vladimir Putin were to attack an allied NATO country.

Hungarian news outlet Magyar Nemzet points out that the moves from France show “Paris is preparing for a world war. The pro-war French president has already come up with alarming plans in recent months, which could clearly lead to a war between NATO and Russia. As reported earlier, Emmanuel Macron did not rule out sending troops to Ukraine either.”

Regardless of the potential threats of an open conflict with Russia, NATO seems to be preparing for that possibility.

“We used to play war. Now, there’s a designated enemy, and we train with people with whom we’d actually go to war,” said General Bertrand Toujouse.

Such military exercises “are a strategic signal,” he added

In recent years, French ground forces have undergone a “profound transformation” to prepare for a conflict as intense as the war in Ukraine.

The main challenge is for French forces to reach Romania in such a short time.

“There is still no military Schengen, and we need to decisively improve military mobility in Europe,” said General Pierre-Éric Guillot.

The first troop deployment in Romania in 2022 has been hampered by bureaucratic hurdles, border control procedures and inadequate trains for transporting military equipment. The affected countries have since worked to eliminate these problems.

“We may still be hampered by a few customs measures, but we’ve made a lot of progress in diversifying our routes,” Guillot told reporters.