FOMC Minutes Preview

The November the FOMC Minutes will be released a day earlier than usual on account of the Thanksgiving holiday on Thursday. Also, the Minutes are an account of the 7th November meeting. Therefore, while they may discuss the Trump victory, they will not incorporate the recent inflation data, which saw an in-line CPI report but hotter than expected PPI report.

Below is a summary of what to expect courtesy of Newsquawk

Summary: The minutes will be released at 2:00 pm EST, but will likely be deemed as stale given recent data and commentary. Recent data saw in line CPI but hotter than expected PPI, with attention turning to the PCE data on Wednesday. Fed Chair Powell, after the two data points, said he projects October Core PCE at 2.8%, up from the 2.7% in September. Recent Fed speak has seen Chair Powell state data shows that the Fed does not need to be in a hurry to cut rates, while hawk Bowman has called for a cautious approach. Meanwhile, many others are keeping their options open, waiting for the data to determine the Fed’s decision making process. The minutes will be eyed to garner the Fed’s views on the balance of risks to the mandate in reference to the recent cooling of the labour market and the “bumpy” inflation readings. Focus will also be on clues for guidance, but it will likely show policymakers want to keep options open and make decisions meeting by meeting.

November FOMC Recap:

- At its November meeting, the FOMC cut rates by 25bps to 4.50-4.75%, in line with market pricing and analyst expectations, and in a unanimous decision.

- The statement saw some changes: it removed language that it “has gained greater confidence that inflation is moving sustainably toward 2%”; it also adjusted its explanation of why the Fed cut rates, to “in support of its goals,” as opposed to “in light of the progress on inflation and the balance of risks.”

- Fed Chair Powell confirmed in the press conference these changes were not meant to send a signal on policy, but the language beforehand was a test for the Fed to cut rates, and now that it has started to ease policy, that test has already been completed.

- The statement changes further confirmed the Fed’s commitment that they are focused on both sides of the Fed’s mandate, as opposed to just inflation.

- The Fed maintained language that risks to both sides of the mandate are “roughly in balance” and it still describes inflation as “somewhat elevated”, while it acknowledged that labor market conditions have generally eased.

Recent Commentary: Recent remarks from Fed officials have seen many echo the line in the statement that risks to the Fed’s mandate are roughly in balance. However, Governor Bowman, the most hawkish on the Fed, sees greater risks to the price stability mandate. Many are also keeping their options open, in fitting with Powell, as they wait to see all the data available before acting. Powell acknowledged that inflation is on a “sometimes bumpy” path back to 2%, but he does expect inflation to continue to come down towards the 2% goal. Nonetheless, after recent inflation data he had said the economy is not sending signals the Fed needs to be in a hurry to lower interest rates.

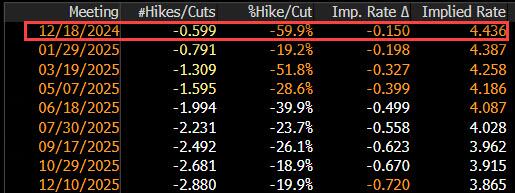

Outlook: The minutes will unlikely give fresh clues to what they are to do in December, but it will likely echo what Powell and Co. have said that they will make decisions meeting by meeting on a data-dependent approach. Regarding December specifically, Fed Chair Powell, before the November meeting, said as long as the economy evolves as expected, then to expect a 25bps rate cut in November, and 25bps in December. However, the Fed cut by 25bps in November, but recent inflation data has shown a lack of progress and is being described as a “bump” in the Fed’s path back to 2%. The Fed Chair then stated that data shows the Fed does not need to be in a hurry to lower interest rates, stressing that policy is not on a pre-set path. There hasn’t been anything committal regarding the December meeting, Fed’s Collins has said a 25bps rate cut is certainly on the table, but it is not a done deal. Goolsbee said he does not like tying Fed hands when asked about December, noting there is still more data to come. Hawk Bowman has expressed cause for concern regarding recent inflation data, and that the Fed should pursue a cautious approach. Note, money markets are currently pricing in around 15bps of easing, which implies a 60% probability of a 25bps rate cut in December, however the latest Reuters survey found that the vast majority of economists (94/106) expect a 25bps rate cut.

Election: Given the latest meeting took place the day after the Presidential Election, the decision would have incorporated the Trump victory. However, the Fed has made it clear they will not front-run policy and it is unlikely to have an impact for the December meeting. Nonetheless, looking ahead Powell did state in the Press Conference, in response to a question about the impact of Trump’s touted policies, said “forecasts of those economic effects would be included in our models of the economy and would be taken into account through that channel”.

Tyler Durden

Tue, 11/26/2024 – 13:00

via ZeroHedge News https://ift.tt/PCvukOt Tyler Durden