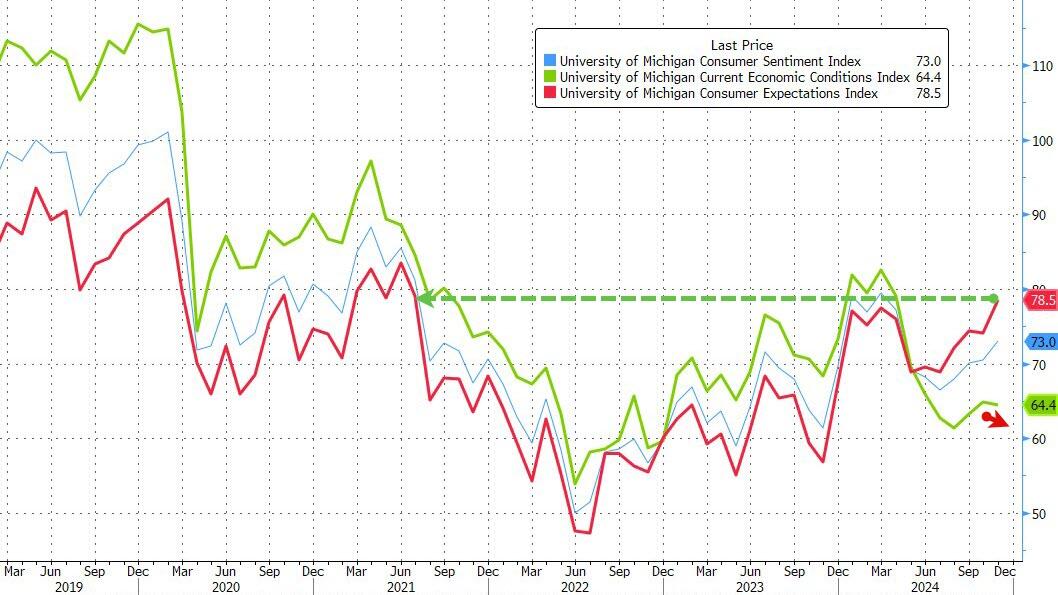

Surge In ‘Hope’ Lifts UMich Consumer Sentiment In Early November Survey

Preliminary November survey data from the University of Michigan showed overall US consumer sentiment jumped higher, led by ‘hope’ as the Expectations sub-index jumped to the highest since July 2021 (while current conditions dipped)…

Source: Bloomberg

Expectations over personal finances climbed 6% in part due to strengthening income prospects, and short-run business conditions soared 9% in November.

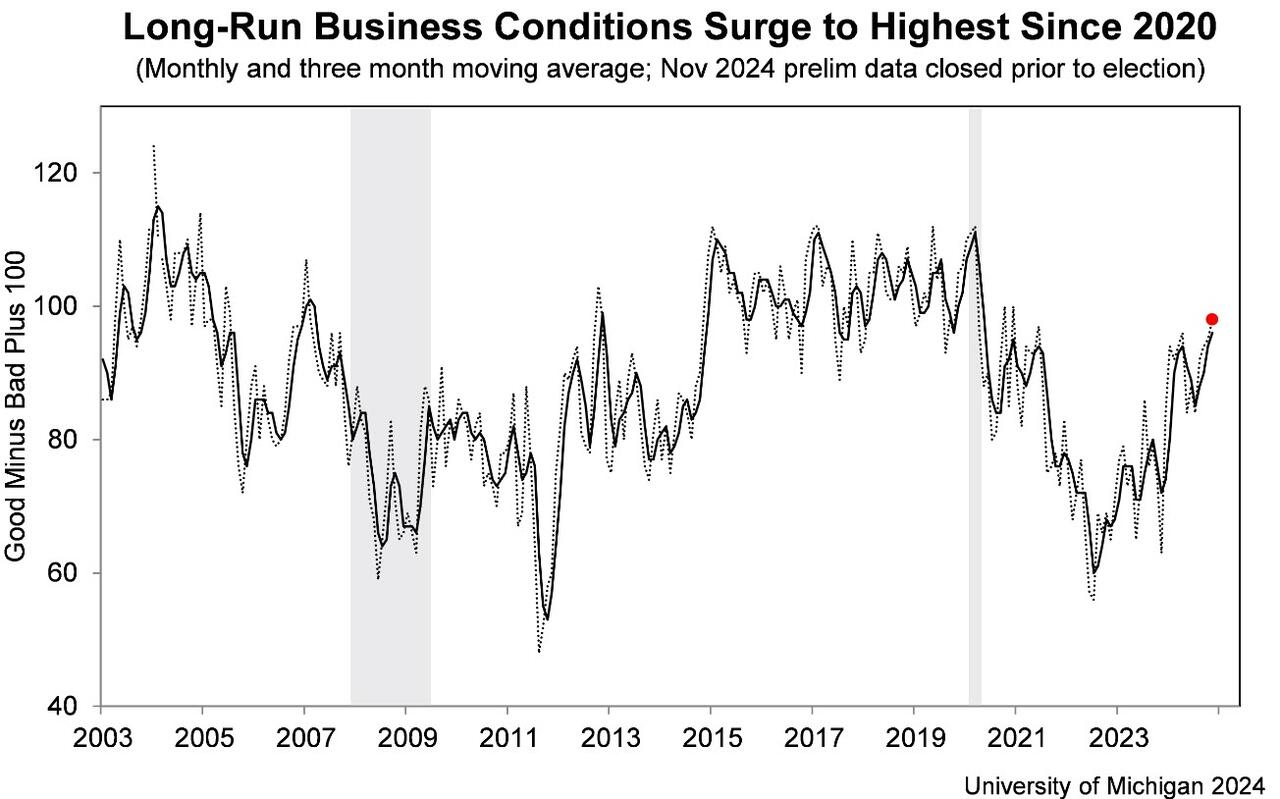

Long-run business conditions increased to its most favorable reading in nearly four years.

Inflation expectations were mixed with 12-month expectations dropping to 2.6% – the lowest since Dec 2020 – while the medium-term expectations inched higher…

Source: Bloomberg

The median value of consumers’ equity market holdings hit a new record high but expectations for future performance dipped a little…

Source: Bloomberg

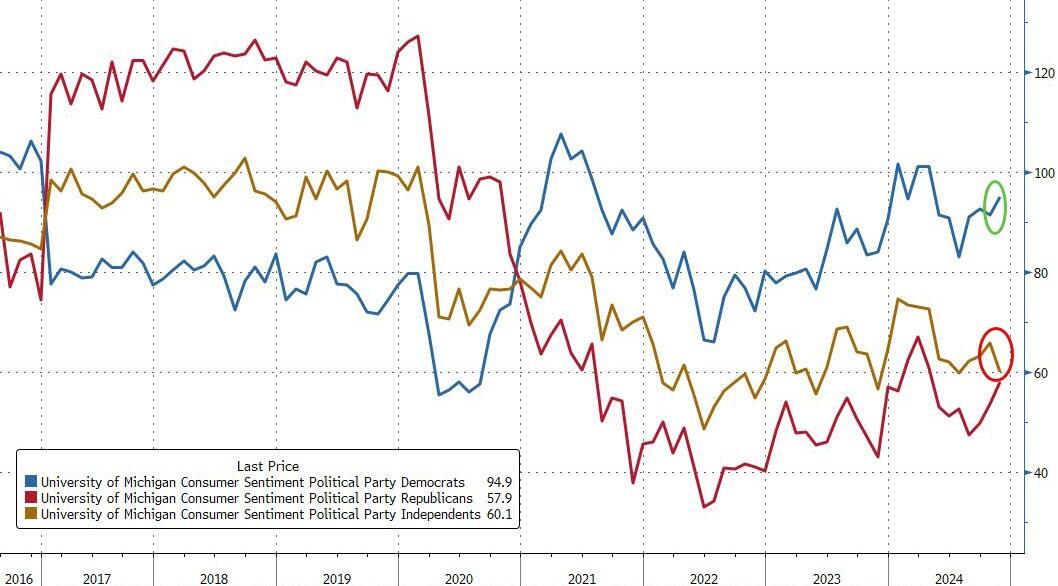

Ironically, Democrats’ confidence rose in the latest survey while Independents tumbled…

With the price of gold rocketing and with gold re-establishing itself as the leading monetary reserve asset for central banks worldwide, the quantities of physical gold held by each central bank and the locations of those reserves are becoming increasingly critical questions.

While most have heard of the Bank of England’s fabled gold vault in London and the New York Fed’s deep underground gold vault in Manhattan — both preferred storage facilities for central banks — did you know that four central banks from Europe claim to store a substantial amount of gold with the Bank of Canada in Ottawa?

These are the central banks of the Netherlands, Switzerland, Sweden and Belgium, known respectively as De Nederlandsche Bank (DNB), the Swiss National Bank (SNB), the Swedish Riksbank, and the National Bank of Belgium (NBB). And the amount of gold that these four central banks claim to hold in Ottawa is not insubstantial, totaling approximately 270 tonnes.

Like nearly everything in the opaque and secretive world of central bank gold, these four central banks had been, for many years, quietly keeping their heads down, never revealing that portions of their national monetary gold holdings were supposedly being stored in Ottawa.

But then a perfect storm of factors aligned that forced them to break the secrecy, factors which interplayed and triggered increased expectations for gold holdings transparency — the Great Financial Crisis of 2007–2009 which intensified scrutiny on central banks; the European Debt Crisis of 2010–2012 which spurred demands for transparency in monetary reserves; political pressure and calls from state auditors for gold holdings disclosure; public activism pushing for gold repatriation and domestic gold storage; and finally the German Bundesbank’s high-profile decision that emerged in 2012 to repatriate some of its gold from storage in New York and Paris.

Swiss, Dutch, Swedish and Belgian

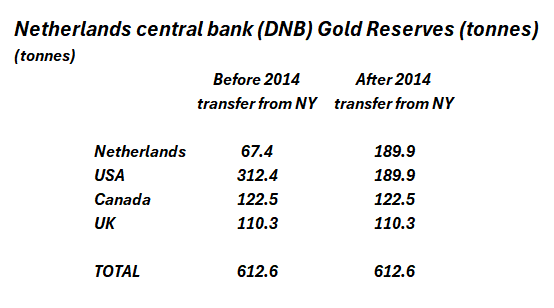

In the case of the Netherlands central bank (DNB), the trigger to reveal the location of its gold reserves came from Dutch members of parliament who in December 2012, noticing that the German Bundesbank was being pressured into explaining if its enormous gold holdings at the New York Fed were actually there, forced the then Dutch finance minister Jeroen Dijsselbloem to reveal that 51% of the DNB’s 612 tonnes of gold was claimed to be held at the New York Fed, 20% of the gold at the Bank of Canada in Ottawa (i.e. 122.5 tonnes), 18% at the Bank of England in London, and the rest stored domestically in the Netherlands.

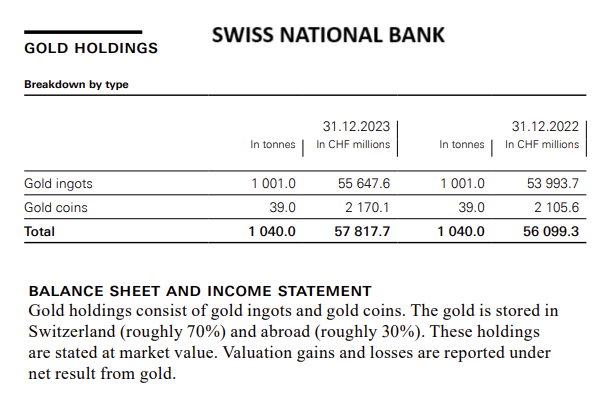

In the SNB’s case it was the “Save Our Swiss Gold” campaign, a national referendum initiative that spanned 2013 — 2014 which among other things called for a ban on SNB gold sales and the repatriation of all Swiss gold reserves stored abroad. In fighting this referendum, which it was successful in doing, the SNB’s then president, Thomas Jordan, in April 2013 was forced to reveal the previously confidential information that only 70% of the SNB’s 1040 tonnes of gold reserves were held in Switzerland, with 20% of the gold held at the Bank of England, and 10% of the gold held with the Bank of Canada in Ottawa (equivalent to 104 tonnes).

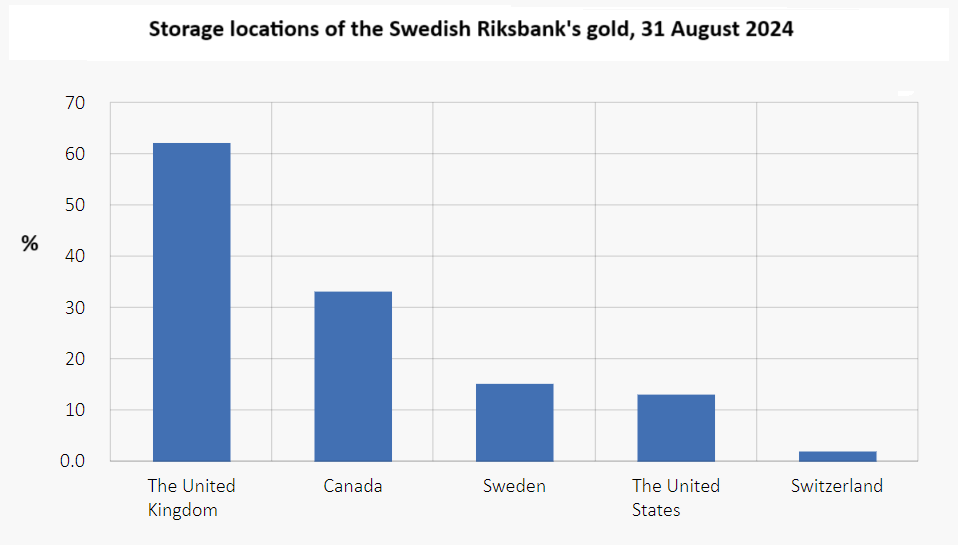

In October 2013, the Swedish Riksbank, up until then secretive about where its gold was located, also revealed that just under half of its 125.7 tonnes of gold was stored at the Bank of England, with another 33.2 tonnes (26.4%) stored with the Bank of Canada in Ottawa, and the rest stored at the New York Fed (10.5%), Swiss National Bank (2.2%), and domestically at the Riksbank (12%).

While the Riksbank at the time said that its new found openness was “part of the Riksbank endeavours to be as transparent as we can”, the real triggers for the Riksbank revelation were peer pressure from other European central banks (for example, in neighbouring Finland, the Finnish central bank revealed the location of its gold reserves during the same week as the Riksbank), and of course the by then in progress German Bundesbank gold repatriation operation from Paris and New York which began in 2013.

Turning to Belgium, following a series of parliamentary questions put to the Belgian Minister of Finance, Koen Geens, during the March 2013 period about the storage locations of the NBB’s gold (in light of the move by the Bundesbank to repatriate some of its gold), Geens reluctantly revealed that of the 227.5 tonnes of gold held by the National Bank of Belgium (NBB) “the largest part of the gold stock of the NBB is held at the Bank of England. A much smaller quantity is held at the Bank of Canada and the Bank for International Settlements (BIS). A very limited quantity is stored at the National Bank of Belgium.”

While this answer did not state how much NBB gold was stored in each location, other media reports from 2014 stated that the NBB held 200 tonnes of gold in London. That being the case, if just less than half the remaining was held by the Bank of Canada (with the rest held by the BIS and domestically by the NBB), that would imply approximately 13 tonnes of Belgian gold claimed to be held in Ottawa.

More than 270 Tonnes of Gold

Adding together all the Swiss, Dutch, Swedish and Belgian gold claimed to be held at the Bank of Canada in Ottawa yields the following: 10% of Swiss gold holdings of 1040 tonnes = 104 tonnes; 20% of Dutch gold holdings of 612.5 tonnes = 122.5 tonnes, Swedish gold 33.2 tonnes; Belgian gold 13 tonnes; for a grand total of 272.7 tonnes, which would be approximately 8.768 million troy ozs of gold, and if in the form of Good Delivery gold bars (400 oz bars) would equate to 21,816 gold bars.

This 272.7 tonnes is quite a sizeable quantity of gold, and to put it into perspective, is approximately equal to the gold holdings of either the Austrian central bank (280 tonnes) or the Spanish central bank (281 tonnes), but has flown totally under the radar among the mainstream financial media. For example, not one mainstream financial news reporter has ever picked up on this topic and asked these four central banks about their gold reserves supposedly stored in Ottawa.

Historic Holdings in a Subterranean Vault

And here is where it gets interesting. The Bank of Canada was an historical gold storage custodian for central bank gold that primarily emerged as a safe place to store gold during World War 2. But its popularity dies down again dramatically from the 1950s onwards. The fact that some of the national monetary gold holdings of the Swiss, Dutch, Swedes and Belgians are claimed to be still held in Ottawa means that the gold in question has been there for a very very long time. For over 80 years to be precise.

Compared to far older central banks, the Bank of Canada was only established in 1935, and its headquarters building on Ottawa’s Wellington Street was only completed in 1938.

This Wellington Street building included a gold vault in the basement, described in the Bank’s head office plans as “a subterranean vault built right into the Laurentian Shield” (i.e. the bedrock). The gold vault, like the HQ, also opened in 1938, and had special shelving added to store the gold, and which one Bank of Canada employee said was “as cavernous as Fort Knox”.

The first three foreign central banks to hold gold with the Bank of Canada were the BIS (1935), the Bank of England (1936), and the Banque de France (1939). Then as World War II broke out in 1939, a further eight central banks clients moved gold to Canada in 1940 to keep it out of reach of the Axis powers, including the Netherlands central bank, Norway’s central bank and the Polish central bank. Then in 1942, the Swiss National Bank and Portuguese central bank began storing gold in Ottawa, followed by the National Bank of Belgium in 1943, the Swedish Riskbank 1944,and the Bank of Mexico in 1945. So can can see straight away how far back in time these gold holdings of Netherlands, Switzerland, Sweden and Belgium in Ottawa stretch.

As Bank of Canada historic documents explain, the European central banks during World War 2 looked at “the sanctity of Ottawa as a safe haven” and considered Ottawa “a faraway, safe place to store gold”. Which is why at its peak, the Wellington Street vault stored more than 2,500 tonnes of gold.

While a few more European central banks opened gold accounts at the Bank of Canada in the 1950s, e.g. Austria and Denmark in 1951, and West Germany in 1954, when the world returned to peace time in the 1950s and following the end of gold convertibility in August 1971, most of these central banks ceased to have any gold holdings in Canada, except strangely the ‘Stay-Behind Quartet’ of Switzerland, the Netherlands, Sweden, and Belgium. The question is, why did these four central banks not bring their gold back from Ottawa to Europe like most other central banks did?

2012: The Gold Goes Walkabout

What’s even more puzzling is as follows. The Bank of Canada’s gold vault used to be located under it’s headquarters building on Wellington Street in downtown Ottawa. However, this building underwent a total renovation between 2013 and 2017 during which time it was literally gutted and the Bank’s 1400 staff moved to other locations. But not only the staff were moved. The gold was also moved.

As well-known Canadian magazine Maclean’s stated in an article titled ‘The Bank of Canada’s move, and what it means for a fabled underground vault’ inJune 2013:

“The renovations, with a price tag of $460 million, and due to be finished by January 2017, will be so extensive as to require the bank to move the entire contents of its Wellington building, including the subterranean vault, which extends from below Wellington and, reportedly, out under the Sparks Street Mall.”

MacLean’s continued:

“Former front-line employees interviewed by Maclean’s, whose work until recently took them beneath the Bank of Canada building, describe vaults that, although depleted, continue to be home to a not insignificant horde of foreign reserves — gold in the form of bullion and coins kept for other central banks. Whatever those holdings entail, all of it is already gone, relocated in advance of the move.”

So you see, the gold that the central banks of Switzerland, Netherlands, Sweden and Belgium claimed over the years 2012–2017 to be “at the Bank of Canada in Ottawa” (Netherlands) or “held with the Bank of Canada in Ottawa” (Switzerland) or “held at the Bank of Canada” (Belgium), was not actually being held at the Bank of Canada ‘s vault in Ottawa. Whatever gold had been there was moved somewhere else. However, at no time did any of the four central banks change the language in their annual statements nor mention the fact that the gold in Ottawa, if it was there at all, moved out of the Bank of Canada’s vault.

When the Bank of Canada moved back into its renovated headquarters building on Wellington Street, there was also absolutely no mention that the vault still existed.

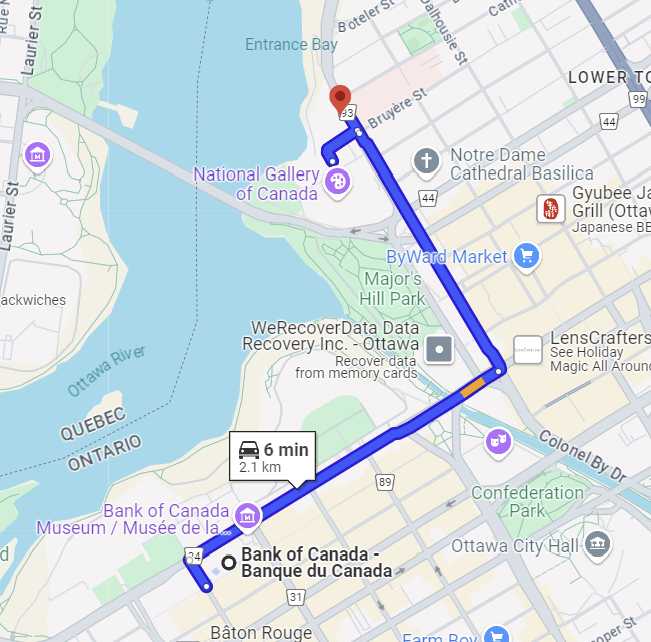

One possibility is that whatever gold bullion had been stored in the Wellington vault before the building renovation was transferred to the Royal Canadian Mint (RCM) on Sussex Drive, which is only 2 kms away from the Bank’s Wellington Street building, and about 5 minutes drive. This theory is plausible because a) the locations are very near each other in central Ottawa, b) both institutions are government organisations known as ‘Crown Corporations’ and c) the RCM, being a precious metals mint and a refinery, already had precious metals storage vaults.

We also know for a fact that in late 2012, a large number of old gold coins that had been stored in the Bank of Canada vault under Wellington Street for over 75 years up until that point, suddenly appeared in the vaults of the Royal Canadian Mint on Sussex Drive. These are coins that had been minted between the years 1912–1914, and some of which the RCM then offered for sale to the public as collectors’ items.

Not only that, but as part of the publicity around these old gold coins, the then governor of the Bank of Canada, Mark Carney, appeared in publicity shots with the president of the RCM, Ian E. Bennett, in a precious metals vault at the RCM’s facilitates. While in the photos it just looks like working stock gold bars in the background on the shelves, the fact that the Bank of Canada’s collection of gold coins ended up in the RCM facility suggests that the foreign central bank gold might have been transported there also. If so, what became of the gold bars belonging to the Swiss, Swedes, Belgians and Dutch in the years following 2012?

Note that Mark Carney was Deputy Governor of the Bank of Canada from August 2003 until November 2004, then senior associate deputy minister and G7 deputy at the Canadian Department of Finance between November 2004 to October 2007, and then Governor of the Bank of Canada from February 2008 until the end of June 2013. Therefore Carney would know a thing or two about the foreign central bank gold holdings that are supposedly under the custodianship of the Bank of Canada.

Having foreign central bank gold reserves stored in a working precious metals mint and refinery is by definition very concerning because it opens up the possibility that the custodian (Bank of Canada) would allow the sub-custodian (Royal Canadian Mint) to borrow precious metal and use it in the gold coin production process.

In general, it is also concerning that supposedly sophisticated central banks such as the SNB, DNB, NBB, and Riksbank, would still entrust some of their extremely valuable gold holdings to a central bank (the Bank of Canada) that hasn’t even got any gold holdings of its own. That’s right! Because the Bank of Canada is infamous in having sold all of its huge gold holdings during the late 1980s, and into the 1990s, and into the early 2000s.

By year-end 2002, this total had dwindled further to a mere 18.6 tonnes, and by December 2003, Canada had no gold bullion at all, becoming, as Reg Howe phrased it “the world’s only major economic power to have eliminated its gold reserves”. Interestingly, Ian E. Bennett, the former RCM president in the photo above with Carney, held senior positions in Canada’s Department of Finance between 1984 and 1993, i.e. all through the period during which Canada sold its gold reserves.

Who then would trust a central bank (Bank of Canada) to safeguard their gold holdings when it (and the Canadian Department of Finance) had treated their own gold reserves like a clearance sale at the mall? But incredibly, as we have seen, the Swiss, Dutch, Swedes and Belgians central banks appear to have done so.

While the reason given by the Canadian authorities for selling the gold was to invest the proceeds into interest-bearing assets – itself a huge mistake given the huge rise in the gold price since then – there are various theories that the real reason for selling the Canadian gold was either as part of an internationally coordinated gold price suppression scheme, or as part of a bullion bank rescue operation that needed to pay back out of control gold loan losses.

So perhaps the Canadian custodied gold of the Swiss, Dutch, Swedes and Belgians went the same way, and that gold is now ‘on the books’ of their balance sheets as a smoke and mirrors line item ‘Gold Receivables’. In a similar vein, perhaps the gold of the Swiss, Dutch, Belgians and Swedes has long ago been leased, loaned, encumbered, pledged in loans and swaps, or even driven down to the New York Fed vault in Manhattan — a road which is less than 500 miles away from Ottawa and takes less than 7 hours.

Conclusion

Which brings us back finally to the central banks themselves, and the ways, not surprisingly, in which they have provided misinformation, disinformation and deflection about the true state of the gold reserves which they claim to hold in Canada.

“The same standards are applied to storing gold abroad as to storing gold in Switzerland. The partner central banks keep clearly identifiable gold bar holdings for the SNB. Each bar stored abroad has a bar identification and remains the property of the SNB. The availability of our gold holdings is fully guaranteed at all times.”

Given that there was no gold in the Bank of Canada’s Wellington Street vault in 2014, this quote from the Swiss National Bank is clearing untrue and is at best misinformation. The SNB also said that gold reserves need to be stored where there is “good market access”. As regards the claimed gold at the Bank of Canada, this statement is patently absurd. There is no central bank gold trading market in Ottawa, and remember the SNB claims to have 104 tonnes of gold in Ottawa. Ottawa is a central bank gold market backwater, and hasn’t been a major gold trading centre for many decades.

In October 2014, the SNB also released a media dossier (only in French and German) in the form of a Q & A format (see here), one of the Q&As of which was as follows:

Q to SNB : When was the last visit of the SNB to these sites (abroad)?

SNB A: Representatives of the National Bank inspect the storage rooms of gold at regular intervals and in agreement with the central bank partners. The SNB has been satisfied in all respects by the result of these visits.

Again this is clearly not true as the gold wasn’t even at the Bank of Canada’s Wellington Street vault in 2014.

Likewise, in 2013, in a Q&A with Swedish media publication ‘Dagens industri about the Swedish gold reserves, the Riksbank answered as follows:

Q to Riksbank: “How do you verify that the gold is really where it should be?

Riksbank A:“We have our own listings of where it is. We reconcile these against extracts that we receive once a year. From now on, we will also start with our own inspections.”

Again, how could the Riksbank start its own inspections of the claimed 33.2 tonnes of Swedish gold stored in Canada, when all of the gold that had been in the Wellington Street vault in Ottawa had been moved out in late 2012? And as you can see there was no mention of the transfer out of the vault in the answer given by the Riskbank.

In 2017, I asked the Riksbank by email: “Is there any specific reason why the Riksbank does not publish a gold bar weight list in the way, for example, that a gold-backed ETF does publish such a weight list every trading day?

The Riksbank Head of Communications, answered as follows: “This kind of information is covered by secrecy relating to foreign affairs, as well as security secrecy and surveillance secrecy.”

So you can see that there are many problems with these central bank explanations. Take your pick, but here are a few.

The Riksbank refused to provide a gold bar list. The Swiss National Bank created huge push back against a popular initiative to bring Swiss gold back from Canada and London.

The Netherlands central bank in November 2014, in an announcement which caused great media interest, said it had secretly repatriated 122.5 tonnes of gold from the Federal Reserve vault in New York back to Amsterdam. But … if repatriating gold was so important to the Netherlands central bank at that time, why didn’t it use the logistical opportunity to also bring gold back from Canada in 2014 at the same time that it brought gold back from New York. After all Ottawa is only a few hours drive from New York?

And as regards the National Bank of Belgium (NBB), in early 2015 there was controversy about whether NBB governor Luc Coene had said that the bank wanted to repatriate 200 tonnes of gold from London. This was first reported by one Belgian newspaper as being true, and then reported by another Belgian newspaper as not being true, quoting Coene as saying that “The repatriation from the UK is not true”. But the point to note here is that none of the reports even mentioned the NBB gold claimed to be stored in Canada.

It’s as if in all of these cases, Canada has been conveniently and deliberately forgotten. And none of the four central banks which claim to have gold stored in Ottawa have ever repatriated a single troy ounce of gold from Canada, let alone a few gold bars. Why not? Where is the Netherlands’ 122.5 tonnes of gold? Switzerland’s 104 tonnes? Sweden’s 33.2 tonnes? And Belgium’s ~ 13 tonnes? That’s in total 272 tonnes of gold and nearly 22,000 good delivery gold bars.

In the current gold landscape, there are many central banks across the world increasingly holding their gold domestically and indeed repatriating gold reserves to their home countries (as seen with Poland, Hungary and India). And also calls for the banks to justify why they maintain gold holdings abroad in the first place.

But at the same time, amid lack of transparency, lack of accountability and utter secrecy, the true state of the gold reserves of four foreign central banks in Canada remains unclear. This is indeed a very Curious Case. Has the gold gone AWOL, or is there an innocent explanation? Enquiring minds would like to know.

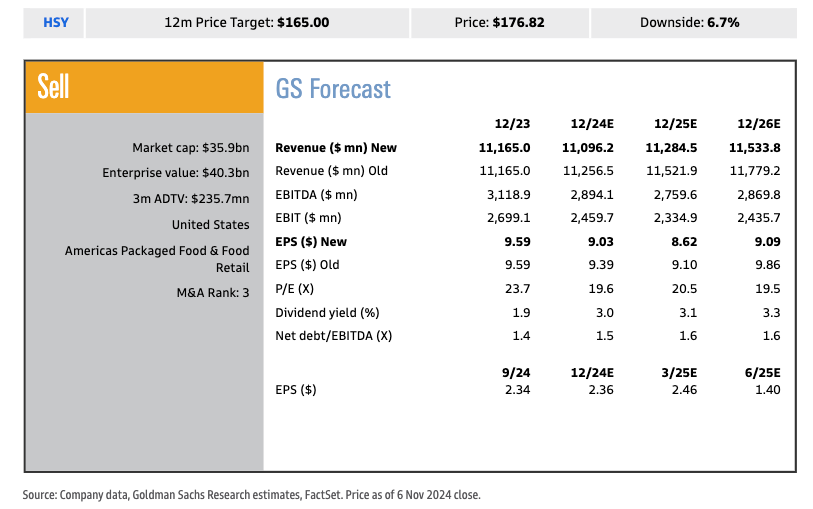

Hershey Cuts Full-Year Sales Outlook As Americans Dial Back On Snack Consumption

Cash-strapped consumers had no joy and happiness in the third quarter as they dialed back spending on chocolate and salty snacks produced by Hershey Co. The company slashed its net sales growth and earnings outlook after consumers balked at rising retail snack prices due to soaring cocoa costs.

Hershey reported third-quarter adjusted earnings per share of $2.34, missing the $2.56 forecast held by analysts tracked by Bloomberg. Salty snack sales in the quarter plummeted in the US, while candy sales were marginally higher.

Here’s a snapshot of the third quarter results:

Adjusted EPS $2.34 vs. $2.60 y/y, estimate $2.56

Net sales $2.99 billion, -1.4% y/y, estimate $3.07 billion

North America confectionery net sales $2.48 billion, +0.8% y/y, estimate $2.53 billion

North America salty snacks net sales $291.8 million, -15% y/y, estimate $313.9 million

International net sales $218.4 million, -3.9% y/y, estimate $243 million

Net sales at organic constant FX -1% vs. +10.7% y/y, estimate +1.91%

North America confectionery sales at constant FX +0.9% vs. +10.1% y/y, estimate +2.86%

North America salty snacks sales at constant FX -15.5% vs. +25.5% y/y, estimate -9.59%

International net sales at organic constant FX +0.2% vs. -1.2% y/y, estimate +8.65%

Adjusted gross margin 40.3% vs. 44.9% y/y, estimate 41.7%

On an earnings call on Thursday, CEO Michele Buck told investors that “pressure in the snacking categories are really driven by the consumers feeling pressured financially.”

Hershey has warned several times that record-high cocoa prices would pressure consumers and thus “limit earnings” this year.

On Thursday, Goldman’s Leah Jordan penned a note for clients about the dismal demand story around Herhsey, reiterating a “Sell” rating…

HSY closed down -2.3% (vs S&P 500 +0.8% and XLP +0.4%) after its 3Q miss and lowered FY24 guidance, which revealed incremental demand headwinds given shifting consumption trends (resulting in inventory reductions at retailers) coupled with increasing competitive pressures across the portfolio as smaller brands and private label gain ground. While HSY sounded more constructive on the longer term outlook for cocoa prices and the impact on its business, there is still uncertainty surrounding the margin pressure from higher cocoa costs for FY25. Furthermore, we believe it will be difficult for the stock to work until we see better demand for the category and market share trends for HSY. We reiterate our Sell rating for HSY with an updated 12-month price target of $165.

Jordan offered clients her top three takeaways from earnings:

Softer top line trends due to lower consumption and increasing competitive pressures: Organic Net Sales tracked at -1.0%, primarily driven by lower volumes (-3.0%), partially offset by net price realization (+2.0%). This volume weakness was largely attributed to a more challenged consumer (including a deceleration in c-store trends), while highlighting the estimated impact from rising GLP-1 usage has been mild. As a result of this softer demand, retailers are managing inventory more tightly across both confection and salty. HSY also called out increasing competitive pressures across its portfolio, including smaller brands and private label within domestic confection, along with price investments from peers in international confection (namely Mexico/Brazil). We expect these market share pressures to persist given lower barriers to entry today (supported by social media, lower for sweets vs chocolate), along with rising consumer adoption of private label and increasing investments in its quality by retailers. Additionally, we observed incremental commentary around mis-execution, which keeps us cautious. The company is proactively aiming to address these issues, including new leadership for US confection, a step-up in its innovation pipeline, updated marketing for evolving consumer needs, and refocused efforts for the c-store channel (adding variety brands, expanding its Gold Standard planogram).

Gross margin pressure increases; uncertainty on cocoa costs clouds the outlook: Gross margin of 40.3% (-460 bps y/y) came in well below Street expectations, as well as internal targets by the company, with greater than expected pressure from the volume deleverage (including reduction in inventory from retailers) and mix (from c-store weakness). While detail on the outlook for FY25 was limited, cocoa remains the biggest cost headwind along with pressure in sugar and labor, which the company aims to partially offset through pricing action, productivity gains, and cost optimization. Regarding cocoa, management noted the outlook has improved with a global supply surplus likely in 2025, supported by a better crop expected in West Africa and increased production in ROW. That said, some challenges persist, including a lack of liquidity on the exchange, suggesting a more gradual pricing recovery is likely. As a result, we expect meaningful margin pressure from cocoa in FY25, along with continued mix headwinds due to channel shifts (namely in 1H). While the company’s new allocation methodology creates noise in y/y compares for next year, we generally expect its margin profile to improve throughout year as pricing is implemented and cocoa costs are layered in.

FY24 guidance lowered; initial look on FY25 suggests hitting top-line algo: HSY lowered its FY24 adj EPS guidance to -MSD from down slightly, driven by a reduction in organic net sales to flat vs +2% prior and a lower gross margin outlook (-250 bps y/y vs -200 bps prior), with the implied 4Q outlook light vs expectations. For FY25, management indicated it should be able to hit its top line algorithm for +2-4% growth, supported by pricing (+LSD to +MSD) and a strong innovation line-up, while the longer Easter season next year could generate up to 1pp benefit based on historical trends. That said, margin pressures should be meaningful next year, thus we expect further EPS compression, recognizing the company’s view was limited with formal FY25 guidance expected next quarter. Additionally, HSY noted FY26 could be an on-algorithm year (+6-8% EPS growth) should cocoa stabilize, while declines could lead to potential upside, although we believe investors will also be watching category demand and HSY’s market share trends to gain confidence in this outlook.

Jordan reiterated Hershey’s “Sell” rating and lowered her 12-month price target to $165 from $185.

Here’s what other Wall Street analysts told clients:

DA DAVIDSON (neutral), Brian Holland

3Q “once again lagged tempered expectations,” and in addition to “moving parts around inventory and shipment timing, underlying demand” remains weaker than expected, Holland writes

The reduced 2024 guidance reflects the 3Q shortfall, but also implies that both his and the Street’s 4Q estimates are too high

“Beyond cocoa, the combination of weaker snacking trends and reinvestment needs figures to pressure both the top & bottom line in the near to intermediate term,’ he says

“Without a clearer picture of when/where the bottom is in the cycle, valuation nearer trough levels alone is not compelling enough to make us more constructive here”

BERNSTEIN (market perform), Alexia Howard

“It seems that over and above the obvious cocoa pressures on margins, category growth remains lackluster even against particularly easy” y/y comparables, Howard writes

“Begs the question” of what the GLP-1 drug impact might be having on “indulgent snacking categories and how Hershey’s core chocolate volumes might fare as the company attempts to take pricing, even as it acknowledges that incremental promotion and revenue growth management efforts are needed”

These challenges may intensify as “cocoa input cost pressures step up and the volume outlook for the US chocolate category remains highly uncertain”

MIZUHO (neutral), John Baumgartner

“Halloween shipments/sell-through met expectations (+LSD%), but total US snacking industry consumption decelerated (+0.1% vs. 2Q’s +0.9%),” Baumgartner writes

Market share losses are increasing amid competition from smaller companies, private label and multinationals, while consumer shopping is shifting more toward club stores/dollar stores/online and less at convenience and drug stores

“Our concerns are rising for FY25 (consensus EPS not low enough) as HSY’s main response appears to be pursuing retail productivity/merchandising & promo optimization,” he says

BARCLAYS (equal-weight), Andrew Lazar

3Q results were “well below even our well-below-consensus” hurt by “both industry-wide and Hershey-specific challenges,” Lazar writes

“Total snacking consumption has softened and consumers are channel shifting from c-store and drug [store] where the category overindexes to club and mass merchandisers where the category is less developed” and retailers “continued to take down” inventory levels across both North America Confectionery and North America Salty Snacks

From a company-specific perspective, Hershey continues to lose market share in core confection business amid increased competition, and hit by execution issues in both Confectionery and Salty Snacks

While a 2024 EPS guidance reduction was likely anticipated, the cut is “greater than most had expected” and 2025 EPS will probably decline “well below current Street estimates”

“While sentiment on HSY shares is already quite negative, in our opinion, we think the magnitude of the 2024 EPS cut combined with underlying fundamental trends that remain challenged will still likely result in some additional share weakness on the open,” he says

The big takeaway is that food inflation remains sticky, and cash-strapped consumers have balked at expensive, leading brands and traded down to generic ones – or, in some cases, entirely pulled back on spending.

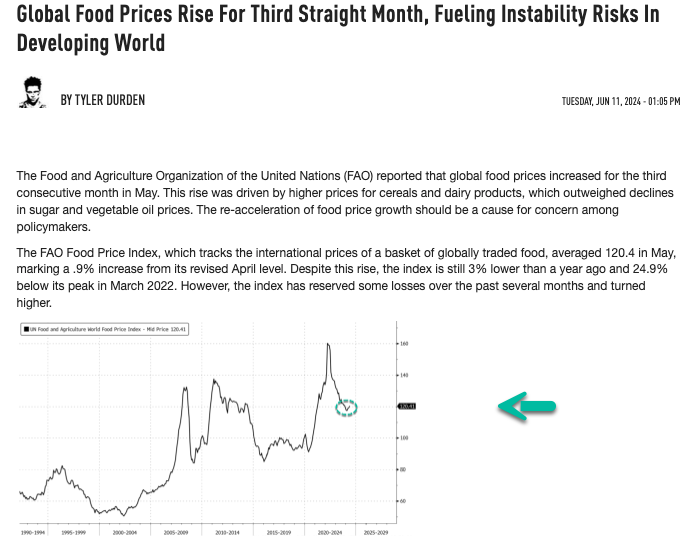

Global Food Prices Re-Accelerate For Second Month As Situation Remains ‘Sticky’

The Food and Agriculture Organization of the United Nations’ Food Price Index, which tracks the international prices of a basket of globally traded food, averaged 127.4 in October, up 2% from the prior month and 5.5% from one year ago. This index bottomed and turned higher earlier this year after peaking and falling for much of 2022-23.

October’s FAO Food Price Index rise is the second consecutive month of year-over-year increases.

The biggest driver of the FAO Food Price Index was the FAO Vegetable Oil Price Index, which spiked 7.3% in October, hitting a two-year high, due to production concerns sending palm, soy, sunflower, and rapeseed oil prices higher.

Here’s how the rest of the index components performed in October:

The FAO Cereal Price Index increased by 0.9 percent in October, led by rising wheat and maize export prices. Global wheat prices were affected by unfavorable weather conditions in major northern hemisphere exporters as well as the re-introduction of an unofficial price floor in the Russian Federation and rising tensions in the Black Sea region. World maize prices rose as well, driven in part by strong domestic demand and transport challenges in Brazil due to low river levels. By contrast, the FAO All Rice Price Index declined by 5.6 percent in October, reflecting lower indica rice quotations driven by expectations of heightened competition among exporters following India’s removal of export restrictions on non-broken rice.

The FAO Sugar Price Index increased by 2.6 percent amid persisting concerns over the 2024/25 production outlook in Brazil following extended dry weather conditions. Rising international crude oil prices also contributed to the increase in sugar quotations by shifting more sugarcane toward ethanol production, while the weakening of the Brazilian real against the United States dollar limited the increase.

The FAO Dairy Price Index rose by 1.9 percent in October, averaging 21.4 percent above its level the same time last year. The increase was primarily driven by higher international cheese and butter prices, while quotations for milk powders declined.

Bucking the general upward trend, the FAO Meat Price Index dropped by 0.3 percent from September, mainly due to lower pig meat prices resulting from increased slaughter rates in Western Europe amid weak domestic and international demand. World poultry prices fell slightly in October, while those of ovine meat remained stable. By contrast, bovine meat prices increased moderately, underpinned by stronger international purchases.

Readers have been well informed about the rising risks of global food inflation re-accelerating. We said in June…

Then, last month:

Global Food Prices Jump Most In 18 Months As Supermarket Inflation Storm Worsens https://t.co/zJgI3QvqBZ

Futures Drop, Dollar Gains After Latest China Stimulus Disappoints

The record election rally has finally fizzled and futs are slightly lower after China’s stimulus package revealed this morning disappointed investors. As of 8:00am ET, S&P futures were trading at exactly 6,000, down 0.1% from the first ever closing high above 6,000 but still on track for its best week in a year on the prospect of tax cuts and deregulation under Trump. Nasdaq futures are down 0.3%. Bond yields are 3bp lower after the Federal Reserve delivered a quarter-point interest-rate cut and left the door open for further easing next month; the dollar reversed some of yesterday’s sharp losses when markets fretted they had taken Trump trades too far (they haven’t). Oil is down but base metals are higher. Overnight, Chinese stock futures and the yuan are lower having extended declines after authorities announced a total 10 trillion yuan ($1.4 trillion) program to refinance local government debt, which was disappointing as (1) There was no lift to the Central Govt debt ceiling, and (2) There was no direct support for consumption or the property market, (3) The only announced a debt swap, not incremental stimulus. Today, the macro focus will be on Univ. of Michigan survey, where consensus expects an increase to 71.0 from 70.5 in October, although the rebound in mortgage rates could weight on sentiment. Later tonight, we will receive China PPI and CPI releases at 8.30pm ET.

In premarket trading, US-listed Chinese stocks declined as Beijing’s latest fiscal policies underwhelm. China announced a plan to refinance local government debt, but stopped short of announcing other measures to boost housing and consumption. Airbnb shares dropped 5.4% after the home-rental company reported third-quarter results. While analysts viewed the results as solid, they flagged the impact of investments on margins. Here are some other notable movers:

Arista Networks (ANET) shares drop 5.1% after the computer networking company projected fiscal 2025 revenue growth of 15% to 17%, compared with 18% estimated by analysts.

Cloudflare (NET) fall 8.3% after the infrastructure software company’s forecast for fourth quarter revenue fell short of consensus.

Doximity (DOCS) shares soar 44% after the healthcare-software company raised its full-year forecast for both revenue and adjusted Ebitda. Analysts say the results are strong, highlighting the client portal roll-out as a catalyst.

Five9 (FIVN) shares rally 22% as the call-center software provider raised its full-year guidance.

Pinterest (PINS) shares fall 12% after the search and discovery network gave a weak revenue forecast for the fourth quarter. Analysts flagged weakness in food and beverage ad spend.

Friday’s moves follow a cross-asset rally on Thursday that was supported by Jerome Powell’s comments. He pointed to the strength of the US economy and said he doesn’t rule “out or in” a December rate cut. Powell added the election will have no effect on policy in the near term, and said he would not step aside if asked by Trump. Following yesterday’s cut, traders are betting on 82 basis points of Fed easing by September 2025. The yield on 30-year US bonds declined about two basis points to 4.51% Friday, falling for a second day to retrace some of its post-election spike. Bloomberg’s dollar gauge gained 0.2%.

After an initial stampede into “Trump Trades,” investors in some asset classes are tapering their enthusiasm as they question whether he will push through his ambitious tariff proposals as US president. “Even with red majorities across Congress, it’s likely that these policy actions will take time,” said James Athey, fund manager at Marlborough Investment Management. “That might make significant further gains in the short term a little harder to come by.”

Meanwhile, US equity funds attracted $20 billion on Wednesday when Trump secured victory in the election, the biggest daily addition in five months, according to BofA’s Michael Hartnett. US stock funds overall added $32.8 billion in the week through Nov. 6.

Halfway across the globe, Beijing’s disappointing stimulus measures “look like it is just a debt swap, which is frankly not going to be that exciting for markets,” said Bernie Ahkong, global multi-strategy alpha chief investment officer at UBS O’Connor. “The big factor between now and the end of the year is if we are going to get some incremental stimulus from the consumer side.”

“To me, there is little alternative to the US,” said Marija Veitmane, a senior multi-asset strategist at State Street Global Markets. “The US is already the best performing equity market globally and we expect that outperformance to continue. US companies are the most profitable and likely to remain so, helped by the potential for lower taxes and less stringent regulation.”

European stocks were also hit by the China disappointment, with mining and consumer products shares leading declines, while real estate and healthcare subsectors were the biggest outperformers leading declines on the Stoxx 600 which falls 0.6%. Here are the biggest movers Friday:

Dino Polska shares surge as much as 12% after Polish food supermarket chain reported improvement of Ebitda margin, despite challenging environment and slow same-store sales

Zealand Pharma shares rise as much as 8.5% in Copenhagen, after JPMorgan initiated coverage on the stock with an overweight recommendation, saying amylin is the “next wave in obesity.

EDP shares rise as much as 5.4% in Lisbon after Portuguese utility reported nine-month net income of EU1.08 billion vs. EU946 million y/y

IAG shares jump as much as 7.9%, reaching the highest level since June 2020, after reporting a significant Ebit beat in the third quarter. The airline group also announced a share buyback program of €350 million to end no later than Feb. 28

IMCD shares rise as much as 7.1%, the most since early August, after the Dutch chemicals firm’s results showed improving organic growth that analysts praised. ING says the market could focus on the positives in the context of troubling macro and chemicals news

Miners are underperforming the broader European market as copper and iron ore joined a slump in commodity prices after China’s debt-swap plan left traders disappointed, with stimulus seen remaining in the slow lane

Richemont shares drop as much as 5.6%, dragging shares in luxury peers lower, after the jeweler and watchmaker’s first-half sales and operating profit missed estimates amid weakness in its Chinese market

Vistry Group shares plummet as much as 21%, slumping to their lowest level since October 2023, after cutting its profit guidance yet again. The housebuilder warned it will build fewer homes than previously expected

Serco shares plunge as much as 15%, hitting their lowest level in almost a year, after the outsourcing company failed to win a renewal to provide immigration services and facilities in Australia

Greggs shares drop as much as 7.6% after Deutsche Bank downgraded the bakery chain to sell from hold, as the broker flagged measures from the Autumn Budget that are “disproportionately relevant to the labor-intensive leisure sector”

Asian equities rose, capping their first weekly gain in six, as the Fed’s rate cut drove broader risk-on trading despite declines in Chinese stocks. The MSCI Asia Pacific Index rose as much as 0.8% Friday before paring some gains, with TSMC, Recruit Holdings and Hitachi among the biggest boosts. The regional benchmark was on course for a weekly advance of around 2.6%. Key gauges in New Zealand, Singapore, and Australia were among the biggest gainers, tracking a rally in US stocks after the Fed lowered its key interest rate by a quarter point. Comments from Fed Chair Jerome Powell that he doesn’t rule “out or in” a December rate cut also helped boost investor sentiment. Sentiment was gutted, however, by the latest disappointing stimulus announcement out of Beijing, which sent Chinese futures and the yuan sliding. After market close, authorities announced a total 10 trillion yuan ($1.4 trillion) program to refinance local government debt, which disappointed investors who were expecting stronger fiscal spending. The disappointment spread to assets often correlated with the health of the Chinese economy. Market watchers are now turning their focus to upcoming policy meetings for further stimulus clues.

“The announcement is a letdown and indicative of the underlying conservative framework that reduces the scope for large positive surprises in the next few months,” said Homin Lee, senior macro strategist at Lombard Odier. “It appears that the authorities are kicking the can to December policy meetings, including the Central Economic Work Conference.”

In FX, the Bloomberg Dollar Spot Index rose 0.3%, hitting a session highs after China announced a disappointing 10 trillion yuan ($1.4 trillion) program to refinance local government debt as part of policy support measures to boost flagging growth. The yen is the best performer among the G-10’s, rising 0.4% against the greenback. The Aussie dollar drops 0.6% to the bottom of the G-10 FX leader board.

In rates, treasuries rise, with US 10-year yields falling 3 bps to 4.30%, underperforming bunds in the sector by 2.5bp, gilts by 0.5bp. Bunds outperform, supporting Treasuries, as euro-area stocks fall on global-growth concerns after China’s debt swap plan fell short of expectations. US data and Fed speaker calendars are light for Friday, and expectations for a heavy corporate issuance slate next week may drive hedging flows.

In commodities, the China disappointment hit prices with iron ore futures down 3%, and Brent crude down 1.5%. Spot gold fell $23 to $2,684/oz.

The US economic data calendar includes November preliminary University of Michigan sentiment at 10am New York time. Fed members scheduled to speak include Bowman at 11am on banking topics. Next week, Chair Powell speaks at an event put on by the Dallas Regional Chamber, Dallas Fed and World Affairs Council of DFW

Market Snapshot

S&P 500 futures little changed at 6,008.75

STOXX Europe 600 down 0.2% to 508.65

MXAP up 0.2% to 189.95

MXAPJ little changed at 603.31

Nikkei up 0.3% to 39,500.37

Topix little changed at 2,742.15

Hang Seng Index down 1.1% to 20,728.19

Shanghai Composite down 0.5% to 3,452.30

Sensex down 0.1% to 79,461.04

Australia S&P/ASX 200 up 0.8% to 8,295.13

Kospi down 0.1% to 2,561.15

German 10Y yield down 6 bps at 2.38%

Euro down 0.2% to $1.0784

Brent Futures down 1.4% to $74.59/bbl

Gold spot down 0.7% to $2,687.50

US Dollar Index little changed at 104.43

Top Overnight News

Advisers close to President-elect Donald Trump have been in discussions with House Ways and Means Chair Jason Smith (R-Mo.) on a broad tax package that is partially paid for by tariffs approved by Congress. As part of those conversations, staffers and advisers close to the Trump team have also investigated whether House rules need to be changed to use tariffs as offsets for tax cuts. Politico

President-elect Donald Trump plans to drastically increase sanctions on Iran and throttle its oil sales as part of an aggressive strategy to undercut Tehran’s support of violent Mideast proxies and its nuclear program, according to people briefed on his early plans. WSJ

A dollar rally triggered by Republican Donald Trump’s victory in the U.S. presidential election could heighten pressure on the Bank of Japan to raise interest rates as soon as December to prevent the yen from sliding back toward three-decade lows. Reuters

Japan’s households cut spending for a second month deterred by inflation, backing the case for the BOJ to take a cautious approach to rate hikes. BBG

China announced a $1.4 trillion program to allow local governments to refinance debt, finally putting an amount on long-anticipated stimulus. Markets weren’t impressed: The offshore yuan, bond yields and commodities all fell. The finance chief promised more measures next year. BBG

China auto sales jump 11.2% Y/Y in Oct (this is the second consecutive month of Y/Y increases, and the fastest growth since Jan). Reuters

The Biden administration is racing to complete Chips Act subsidy deals with Intel, Samsung and others before Trump takes office. TSMC and Global Foundries are said to be readying announcements, but more than 20 companies are still in the process. BBG

Susie Wiles — one of the top architects of Trump’s political campaign — was named his White House chief of staff. She’ll be the first woman to hold the position. Jared Kushner won’t join the administration, though he may advise on Middle East policy, the FT reported. BBG

BlackRock is said to be in talks to take a minority stake in Millennium. BBG, FT

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were ultimately mixed despite the early momentum following the fresh record levels on Wall St and a bout of rate cuts by major central banks, with gains capped as participants awaited a potential Chinese fiscal stimulus announcement. ASX 200 outperformed its major peers amid gains in nearly all sectors and with financials kept afloat post-ANZ earnings. Nikkei 225 traded higher but with gains capped after a contraction in household spending and the recent currency rebound. Hang Seng and Shanghai Comp wiped out early gains despite the HKMA’s 25bps lockstep rate cut with price action cautious as participants awaited the conclusion of the NPC Standing Committee’s session and potential stimulus announcement.

Top Asian News

PBoC says they will firmly guard against the risk of exchange rate overshooting. Further interest rate cuts face dual constraints of net interest margin and exchange rate

PBoC Q3 Monetary Policy Report: Reiterates monetary policy is to be flexible & targeted. To enhance the guiding role of central bank policy rates. To keep expanding monetary policy toolbox. Sticking to accommodative monetary policy stance. Maintain yuan exchange rate. To further improve monetary policy framework

China’s MOFCOM says China made progress in talks with EU on EV tariffs, with technical talks next week.

Hong Kong Monetary Authority cut its base rate by 25bps to 5.00%, as expected, in lockstep with the Fed.

China’s Ambassador to the US Xie Feng said there are no winners in tariff wars, trade wars, science and technology wars, and industrial wars, while he added that the Taiwan issue is the first red line that cannot be crossed in Sino-US relations and words must match deeds. Furthermore, he said no challenge can stop China’s progress and that any containment and suppression will only “hit a wall.”

Japanese Finance Minister Kato said they will closely monitor the impact of Trump policies on the Japanese economy, while he wouldn’t comment on the FX level but reiterated it is important for currencies to move in a stable manner reflecting fundamentals and that they will take appropriate steps on excessive moves.

Sony (6758 JT) 6-month (JPY): Net 570bln, +36%; Operating 734bln, +42.3%; PBT 767bln, +43.8%.

Softbank (9434 JT) 6-month (JPY) Sales 3.15tln, +7.4% Y/Y, Op. Income 585.89bln, +13.9% Y/Y; Sees FY Net Income 510bln (prev. guided 500bln); Op. Income 950bln (prev. guided 900bln)

China Q3 (USD) Prelim current account surplus 146.9bln (prev. 54.5bln Y/Y), via China FX Regulator

Acer (2353 TT) Oct consolidated revenue TWD 18.82bln Year to October +10.1%

China NPC Press Conference

China’s top lawmakers have approved the local debt swap plan; to raise the local gov’t debt ceilings to replace existing hidden debts, via Xinhua.

China’s NPC Vice-Chairman says they intend to raise the local gov’t debt ceiling by CNY 6tln. Moves to reduce local gov’t debt will help to promote growth, expect to save CNY 600bln in interests for local gov’ts over five years; In addition to the 6tln debt limit approved, the local debt repayment resources will be directly increased by 10tln. New debt quota will help to replace existing debts. Will help to increase the local debt ceiling. Will raise the end-2024 local gov’t special bond ceiling to CNY 35.5tln from CNY 29.52tln. Debt burdens in some regions are “big & heavy”. Must resolutely curb new “hidden” debt.

China’s Finance Minister (Q&A): must resolutely curb new “hidden” debt; China Government debt burden relatively low and still has relatively big room to raise debt; will increase counter-cyclical measures. Will roll out new policy measures. Will issue measures to support the property market. To implement more forceful fiscal policy in 2025. Will soon issue special sovereign bonds to replenish the capital of big state banks. Issue special local bonds to support the purchase of idle land and unsold flats. Will issue ultra-long special treasury bonds.

European bourses, Stoxx 600 (-0.7%) are entirely in the red and to varying degrees vs futures initially indicating a positive open. Sentiment was hit following the China’s NPC press conference, where it largely refrained from providing specific details on fiscal stimulus, but did promise more forceful fiscal policy in next year. Bourses continued to trundle lower and currently reside just off worst levels. European sectors hold a negative bias; Healthcare takes the top spot, lifted by AstraZeneca after it reported a positive update on one of its treatments. Basic Resources and Consumer Products sit at the foot of the pile, with the former hampered by losses in underlying metals prices whilst the latter is weighed on by poor results from Richemont. Additionally, sentiment across these China-exposed sectors was hit given the lack of fresh stimulus measures from China’s NPCSC. US equity futures (ES -0.1%, NQ U/C, RTY U/C) are flat/incrementally lower, but have been edging ever so slightly lower in recent trade, given the weakness also seen in Europe. TSMC (2330 TT) has reportedly informed Chinese customers that it will be suspending production of some of their AI and high-performance chips, via Nikkei citing sources; as the Co. increases efforts to comply with US export controls

Top European News

Grifols Profit Rises on Biopharma Sales, Repeats Guidance

Erdogan Expects Lower Interest Rates With Slower Inflation

German Economy Minister Habeck Returns to X After Five Years

Cartier Owner Richemont’s Profit Slumps on Weak China Demand

Logitech CEO Takes Diving Lessons to the Metaverse: Leader Q&A

Scholz Under Mounting Pressure to Agree to January German Vote

FX

DXY is slightly higher, with USD stronger vs. most peers (DXY is sluggish on account of JPY strength). DXY has been as high as 105.44 post-election but has since returned to a 104 handle.

EUR is on the backfoot vs. the USD with the pair unable to hold above the 1.08 mark after venturing as high as 1.0824 on Thursday. For now, today’s session low is at 1.0762 is still comfortably above yesterday’s base at 1.0712.

GBP softer vs. the USD to a similar magnitude as peers. Downside for Cable is limited relative to Thursday’s moves with the current session low at 1.2936.

JPY is the only of the majors to be up against the USD in an extension of yesterday’s price action. Markets seem willing to fade some of the post-election rally seen in USD/JPY with Japanese officials out in full force attempting to jawbone the pair lower. USD/JPY has been as low as 152.28 with the next targets coming via the 200 and 21DMAs at 151.67 and 151.66 respectively.

Antipodeans are both softer vs. the USD after yesterday’s post-election recovery vs. the USD. Today it is likely that some of the disappointment surrounding the Chinese NPC meeting is acting as a drag on both pairs.

Yuan is on the backfoot vs. the USD with the outcome of the Chinese NPC meeting judged to be somewhat of a damp squib as some expectations for bazooka stimulus were left disappointed.

Rates

USTs are in the green, as markets digest the 25bps move from the Fed and continued data-dependent and meeting-by-meeting guidance alongside Powell saying he intends to serve the entirety of his term (mid-2026). Given the cut, yields are lower across the curve though there is no overt flattening/steepening bias currently. USTs at a 110-16+ peak, just off the 110-21+ WTD high. No real follow through from the underwhelming Chinese press conference.

Bunds are firmer, taking directional impetus from USTs but primarily bouncing back from the marked pressure seen yesterday when the German coalition essentially collapsed. Stopped two ticks shy of the 132.00 mark but remains in striking distance.

Gilts are directionally echoing peers but the modest outperformer. Action which comes as Gilts pare back the hawkish-skew from yesterday’s BoE. Gilts currently above the 94.00 mark but just off a 94.21 peak, resistance at 94.34 and 94.73 from Monday and last Friday.

Commodities

A softer session for the crude complex complex thus far in a continuation of the weakness seen overnight following yesterday’s choppy performance but with price action contained amid light oil-specific newsflow and against the backdrop of ongoing geopolitical risks. Weakness this morning also emanated from China’s NPC press conference which was overall a damp squib – China’s much anticipated NPC Standing Committee meeting concluded today with an announcement on a debt swap plan to rein in hidden local government debt, whilst future fiscal stimulus was promised. Brent trades towards the lower end of a USD 74.45-75.61/bbl.

Precious metals are softer across the board after rebounding yesterday as the dollar softened on a Trump trade fade, with the broader commodity complex overall underwhelmed by the Chinese NPC press conference.

Base metals are lower across the board following the underwhelming Chinese NPC announcement which omitted specifics regarding sizes of fiscal stimulus, although China’s Finance Minister said China will roll out new policy measures.

US President-elect Trump reportedly intends to drastically increase sanctions on Iran and throttle its oil sales, via WSJ citing sources.

Geopolitics

“Deputy Speaker of the Lebanese Parliament to Sky News Arabia: A ceasefire is possible within a few weeks”, according to Sky News Arabia; details light

Iranian Supreme Leader said Iran should put an end to Israel and make a sound decision on responding to its attack, according to Sky News Arabia.

Israeli PM Netanyahu is aware of serious violence against Israeli citizens in Amsterdam and directed that two planes be sent immediately to assist citizens in Amsterdam after reports of Israeli football fans being attacked by assailants chanting ‘Free Palestine’. Furthermore, Israel’s Foreign Minister asked his Dutch counterpart to help get Israelis out safely following the security incident in Amsterdam.

Israeli occupation forces stormed the city of Dhahriya, south of Hebron in the West Bank, according to Al Jazeera.

US Event Calendar

10:00: Nov. U. of Mich. Sentiment, est. 71.0, prior 70.5

Nov. U. of Mich. Current Conditions, est. 65.5, prior 64.9

Nov. U. of Mich. Expectations, est. 75.0, prior 74.1

Nov. U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.0%

Nov. U. of Mich. 1 Yr Inflation, est. 2.7%, prior 2.7%

DB’s Jim Reid concludes the overnight wrap

Markets put in another very strong performance over the last 24 hours, with US risk assets continuing their post-election surge. In fact after yesterday’s moves, the S&P 500 (+0.74%) is now up more than +25% on a year-to-date basis, and the last time it was up this much YTD by November 7 was back in 1995. Moreover, US IG credit spreads tightened another -2bps yesterday to just 75bps, which is their tightest closing level since 1998. So there’s an incredibly buoyant mood right now, and the S&P 500 has also just recorded its strongest 3-day move (+4.56%) since 2022.

Of course, the main news yesterday came from the Fed, although the policy decision was a widely-expected 25bp cut, which took the target range for the fed funds rate down to 4.50-4.75%. The language in the FOMC statement was largely unchanged, keeping the view that “the risks to achieving its employment and inflation goals are roughly in balance.” Looking forward, Powell avoided sending any signal about the December meeting, emphasising the data still to come before then. But relative to the previous meeting in September, the overall tone leaned slightly hawkish, as Powell mentioned how the recent data pointed to “diminishing downside risks” as “the economy remains strong”. He also added that “the right way to find neutral… is carefully, patiently”. Our US economists continue to expect another 25bps cut in December, but they think the bar for a skipping a cut at that meeting isn’t high. See their full reaction here.

In terms of recent political developments, Powell steered clear of discussing the implications of the election for the Fed, saying that “We don’t know what the timing and substance of any policy changes will be”. He also replied “No” when asked if he’d resign if Trump asked him, and said that dismissal of any Fed board members was “not permitted under the law”. Separately, a CNN report earlier cited a Trump advisor saying that Trump would allow Powell to serve out the rest of his four-year term until May 2026.

When it comes to the election results, the only outstanding question now is whether the Republicans will take the House of Representatives. That’s still not formally confirmed, but the chances of a Republican sweep on Polymarket have now risen to 97%, and the latest seat count from AP now stands at 211 for the Republicans and 199 for the Democrats, with 218 required for a majority. Meanwhile in the Senate, the latest total now stands at 53-45 for the Republicans, with two seats left to be called. Finally, Trump announced his first appointment yesterday, saying that Susie Wiles, his campaign manager, would become his White House chief of staff.

Before the Fed’s decision, US Treasuries actually unwound some of their post-election moves yesterday, with 2yr Treasury yields ending the day -6.2bps lower at 4.20%, whilst the 10yr yield fell -10.6bps to 4.33%. This also meant the dollar index (-0.55%) posted its worst day since August, albeit giving up just a third of Wednesday’s +1.61% gain. And looking forward, investors believe that another 25bp cut in December is likely, but far from certain, with futures only giving that a 71% probability as we go to press this morning.

Elsewhere, US equities saw continued gains as Powell struck an upbeat tone on the economy. That saw the S&P 500 (+0.74%) reach its 49th all-time high this year, with its YTD gains crossing the +25% mark. Tech stocks led the advance, with the NASDAQ (+1.51%) and the Magnificent 7 (+2.28%) reaching new highs of their own. That said, some of Wednesday’s strongest performers did see a reversal, with the Russell 2000 (-0.43%) and the KBW Bank index (-2.68%) retreating. But positive sentiment dominated overall, with the VIX index (-1.07pts) falling to its lowest level since August at 15.20.

Overnight in Asia, the focus is now on the Standing Committee meeting of China’s National People’s Congress, and what measures they may announce, particularly with the prospect of higher US tariffs under a Trump administration. Ahead of that, equity markets have seen little moves in either direction across Asia, with the Hang Seng (-0.29%), the CSI 300 (-0.09%), the Shanghai Comp (+0.14%), the KOSPI (-0.12%) and the Nikkei (+0.11%) all seeing pretty modest moves. That’s been reflected among US equity futures as well, with those on the S&P 500 up just +0.05% this morning.

Ahead of the Fed, the Bank of England also delivered a 25bp rate cut yesterday, taking their policy rate down to 4.75%. The move was widely expected, and the Monetary Policy Committee voted 8-1 in favour of the decision, with the dissenting vote to keep rates unchanged. Their latest forecasts also included the impact of the government’s budget the previous week, which announced higher borrowing plans for the years ahead. Their statement said that the budget was “provisionally expected to boost CPI inflation by just under ½ of a percentage point at the peak”, and Governor Bailey said that the Budget changes “are expected to reduce the margin of spare capacity in the economy over the forecast period”. Looking forward, the BoE signalled that rates would continue to move lower, and Governor Bailey said that “a gradual approach to removing policy restraint remains appropriate”. From here, our UK economist expects the BoE to leave rates on hold at the next meeting, before delivering another cut at the subsequent decision in February, and eventually moving to a terminal rate of 3.25%.

With the BoE cutting rates, UK gilts saw a strong outperformance yesterday, which saw the spread of 10yr gilt yields over bunds tighten by -10.4bps to 205bps. That took it down from its two-year high the previous day, and it also marked the biggest move tighter in the spread since July 2023. But even as gilts rallied, sovereign bonds elsewhere in Europe struggled, with yields on 10yr bunds (+4.0bps) and OATs (+2.8bps) both moving up to their highest level since July, at 2.44% and 3.20% respectively. For equities it was the reverse picture however, with the UK’s FTSE 100 (-0.32%) lower amidst the stronger pound, whilst Germany’s DAX (+1.70%) posted its best daily performance of 2024 so far. Otherwise, the broader STOXX 600 posted a +0.62% gain.

Elsewhere in Europe, there’s been plenty happening in German politics after the federal coalition broke up on Wednesday night. As a reminder, the breakup happened after Chancellor Scholz of the SPD dismissed finance minister Christian Lindner, who also leads the FDP, and the other FDP ministers then left the coalition as well. In turn, Scholz said he would call a vote of no confidence on January 15, which would pave the way for new federal elections after that. There were calls yesterday for that vote to be brought forward, including from opposition leader Friedrich Merz of the CDU/CSU, but Scholz said again that he wouldn’t put the vote of confidence to the Bundestag until the start of next year.

Looking at yesterday’s other data, the US weekly initial jobless claims were broadly as expected at 221k (vs. 222k expected). However, the continuing jobless claims for the previous week ending October 26 ticked up to 1.892m (vs. 1.873m expected), their highest level since November 2021. Over in Europe, German industrial production contracted -2.5% in September (vs. -1.0% expected), and Euro Area retail sales were up +0.5% in September (vs. +0.4% expected).

To the day ahead now, and data releases from the US include the University of Michigan’s preliminary consumer sentiment index for November, and there’s also Italy’s retail sales and industrial production for September. Central bank speakers include the Fed’s Bowman and Musalem, the ECB’s Vujcic, and the BoE’s Pill.

Cryptocurrencies have undergone an astonishing evolution over the past 15 years.

What began with Bitcoin’s (BTC) launch in January 2009 has grown into a dynamic yet highly volatile asset class, capturing the attention of individual investors, financial institutions, and governments worldwide.

Bitcoin, often referred to as “digital gold,” has generated phenomenal, unprecedented returns for early adopters, as shown in the chart below. However, despite this dramatic ascent, the cryptocurrency market remains a speculative and often misunderstood corner of the financial world. Wild price swings, regulatory concerns, and complex underlying technology make cryptocurrencies both exciting and risky.

In the lead-up to Tuesday’s Presidential election, investors closely watched market movements, with some speculating that a victory by former President Donald Trump could act as a catalyst for crypto prices. For crypto enthusiasts, the election results did not disappoint. Bitcoin’s price surged nearly 8% in early trading, crossing the $75,000 mark for the first time and breaking its previous all-time high set in March. Other cryptocurrencies followed suit; Dogecoin, for example, saw significant gains, partly due to its association with its most notable supporter, Elon Musk. Musk’s frequent endorsements of Dogecoin have fueled its popularity, despite its origins as a “joke” cryptocurrency.

The recent price jumps following the election raise two crucial questions:

1. Is the Price Jump in Cryptocurrencies a Knee-Jerk Reaction or Sustainable Momentum?

History has shown that cryptocurrency markets often react to macroeconomic and political events, with sharp price increases or decreases around significant news.

In this case, the election results have likely fueled short-term speculative buying. When large investors and traders anticipate a favorable outcome, they can inject a wave of capital into the market, driving up prices. However, the long-term sustainability of this momentum is less certain and depends on multiple factors, such as post-election regulatory policies, interest rates, and investor confidence in the broader economy.

Many analysts argue that Bitcoin and other digital assets are increasingly viewed as a hedge against inflation and economic instability, much like gold. If this narrative continues to hold, these assets may find more sustained support from both retail and institutional investors, especially if inflation remains high or the economic landscape is uncertain. Additionally, the cryptocurrency market will almost certainly benefit if support from the new administration remains strong.

2. Does a Change in Administration Provide Tailwinds to Cryptocurrencies?

Shifts in political leadership often influence regulatory landscapes, which could, in turn, affect the future of the cryptocurrency market. President-elect Trump has signaled his support for the industry, declaring his affection for the digital currency on several occasions. Additionally, he has promised to remove existing SEC leadership leading the US government’s crackdown on the crypto industry.

On Tuesday night, Coinbase CEO, Brian Armstrong, offered his perspective on what the change in leadership means for the industry: “Tonight the crypto voter has spoken decisively — across party lines and in key races across the country. Americans disproportionately care about crypto and want clear rules of the road for digital assets. We look forward to working with the new Congress to deliver it.”

Many governments continue to explore central bank digital currencies (CBDCs), which could bring legitimacy to digital assets while also create regulatory competition for cryptocurrencies. Should the U.S. choose to advance its own CBDC initiatives, there could be an indirect benefit to the crypto space by fostering broader digital asset literacy and infrastructure improvements.

Looking Ahead: What’s Next for Cryptocurrencies?

The cryptocurrency market remains unpredictable, and investors should remain cautious.

While speculative rallies provide opportunities for quick gains, the risk of rapid declines is ever-present.

Moving forward, the path will likely be shaped by a combination of policy changes, economic conditions, and technological developments.

For those who embrace the potential of digital currencies, this election-induced rally serves as a reminder of both the opportunities and the risks inherent in this asset class.

Whether Bitcoin and other cryptocurrencies can sustain their momentum, or if they will once again face turbulence from political and economic shifts, remains an open question.

However, the increasing integration of these assets into mainstream finance suggests that cryptocurrencies are evolving from a speculative fringe to a central component of the modern financial landscape.

Restructuring Underway At Soros Fund Management As Hong Kong Office To Shut

An administrative restructuring is underway at Soros Fund Management, founded by billionaire George Soros in the 1970s, as it plans to shutter its Hong Kong office, according to a Bloomberg report. Although the exact reasons were not disclosed, this move comes just days after Soros’ son, Alex Soros, through the family’s Open Society Foundations, wasted tens of millions of dollars backing the biggest Democrat loser in a generation: Kamala Harris.

The New York-based investment firm, best known for its $10 billion trade against the British pound in 1992, explained in an emailed statement that its Asia investments will now be managed by traders in its New York and London offices. The firm added that it will continue allocating capital to managers in Japan, Singapore, and Hong Kong.

Bloomberg reporters working on the story could not obtain further comment from the investment firm.

A key question remains: Why is Soros Fund Management shrinking its Asian physical footprint? Bad china bets?

This administrative restructuring at the investment firm comes months after a major restructuring occurred within OSF over the summer. OSF reportedly laid off over 40% of its workforce worldwide and implemented a new operating model.

Even with all this restructuring, the philanthropic organizations controlled by the Soros family, with Alex Soros somewhere at the helm—and even further off the reservation than his father—wasted a lot of daddy’s money on supporting the biggest Democratic loser in a generation: Harris-Walz. This historic loss will be detrimental to the Soros family and far-left Davos elite, who push nation-wrecking globalist policies. The tide has turned.

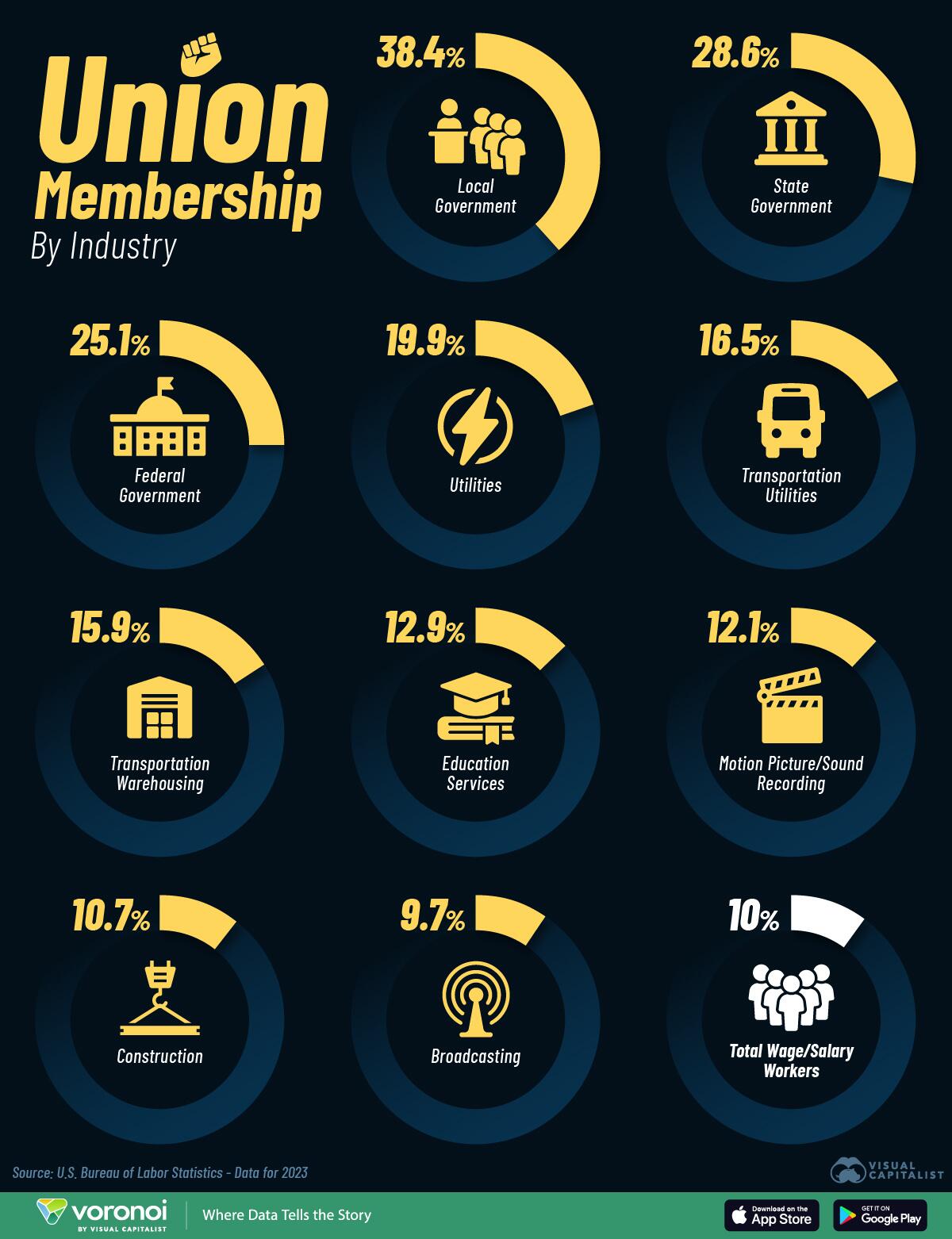

Today, union membership stands at historic lows of 10%, a stark decline from the 33.5% peak seen in 1954.

Despite a surge in unionizing efforts last year, from Starbucks and Amazon to Trader Joes and Uber, national membership rates fell for the second year in a row. This was due to the rise in non-union jobs, which largely offset the 191,000 new private sector unionized jobs.

As we can see in the table below, roughly a third of public sector jobs are unionized, led by the local government sector by a wide margin:

When it comes to the private sector, utilities and transportation have the highest union membership rates, both providing essential services in highly-regulated industries.

For instance, the Utility Workers Union of America represents 45,000 members across the country, including employees at major firms such as Exelon, Duke Energy, and Southern Company. While 19.9% of utilities workers are unionized, it has fallen from 28.3% since 2010.

In the transportation and warehousing industry, over one million workers are unionized, at 15.9% of the workforce. However, it too has seen unionization declines, falling from over a quarter of workers in 2000.

As one of the largest unions in the country, the International Brotherhood of Teamsters has 1.3 million members across the U.S. and Canada, and is one of the primary unions for the transportation sector. Often, union members receive regular wage increases, pension plans, job security, and wages that exceed industry standards.

We can see that unionization rates in the film industry also falls above the national average, at 12.1%. Last year, the historic Writers Guild of Americas strike led to key pay negotiations, minimum staffing requirements, and new guidelines on the use of artificial intelligence as technological advancement reshapes the entertainment industry.

Overall, 14.4 million workers in America are unionized, with the country ranking 27th across 31 OECD countries by union density based on the most recent figures. By contrast, five countries have over 50% of workers that are unionized, including Iceland, Denmark, and Sweden.

To learn more about this topic from a geographic perspective, check out this graphic on union membership by state.

When asked to picture a flame, most people probably envision an orange streak dancing to and fro over a pyramid of burning wood, or a tidy blue radiance emanating from a cooking stove. Both are correct conceptions. But in each instance, fire’s purest form is masked by periodic table ‘pollutants’, so to speak.

Above a roaring campfire, we only perceive orange and yellow hues as tiny carbon and sodium particles from the wood fuel are illuminated in the burning maelstrom.

Under a boiling pot of water on a stove, we see blue flames as methane combusts into carbon dioxide and water.

But there’s a more elemental flame that most people have never witnessed. Not only because it’s rare in everyday modern life, but because it’s nearly invisible in daylight and only seen as the faintest pale blue in darkness. This is a hydrogen flame.

When combusted in the presence of oxygen, hydrogen (the lightest element on the periodic table) transforms into water, a chemical process that yields almost no visible light. To see such a flame at all, thermal imaging cameras are often needed.

While hydrogen flames are an infrequent sight today, they could grow more common. As the cleanest burning fuel in existence, hydrogen may become an integral part of a green energy economy, finding use in steel furnaces, heavy-duty vehicles, and aircraft. A phasing out of fossil fuels will not only change the world, it might even alter our view of fire itself.

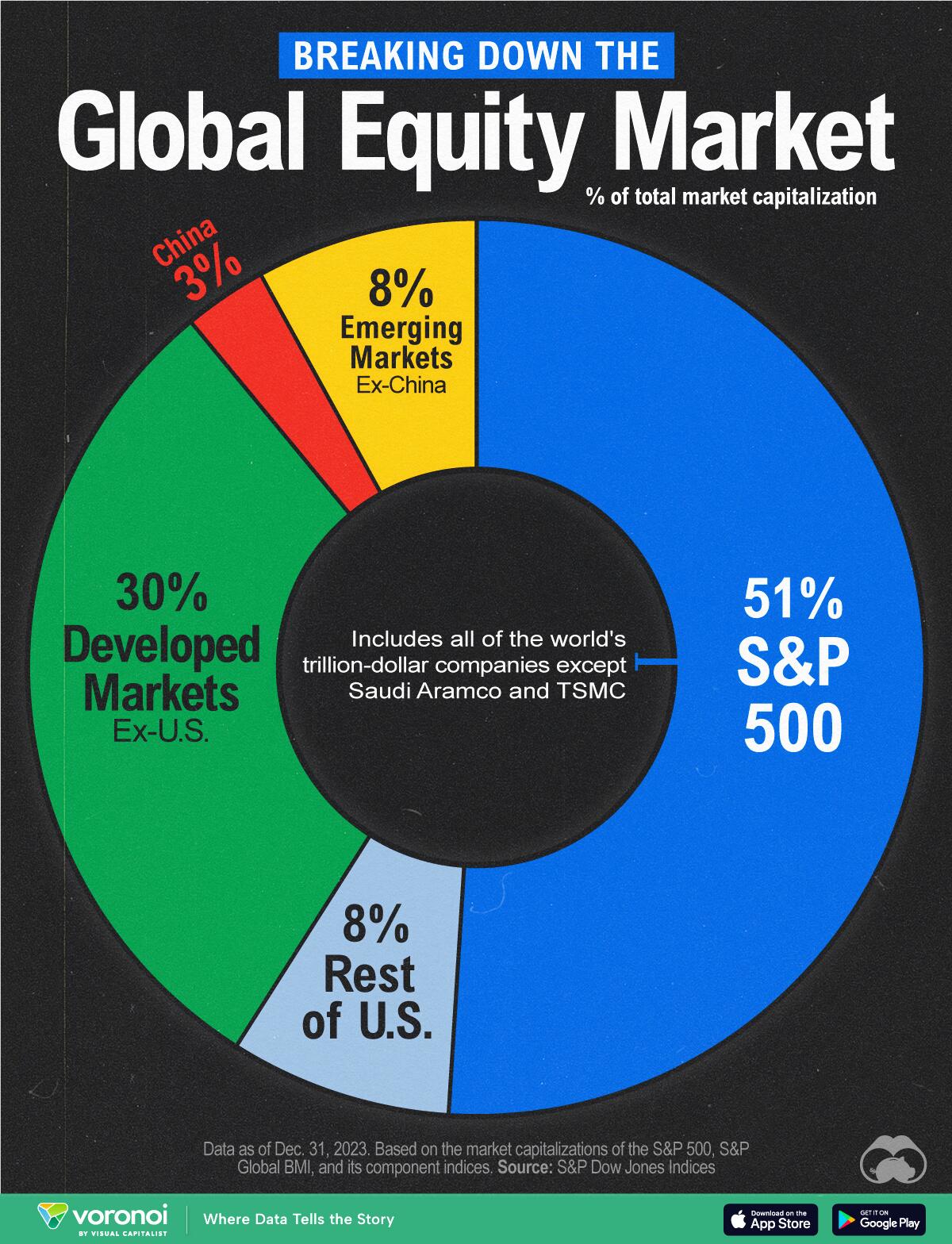

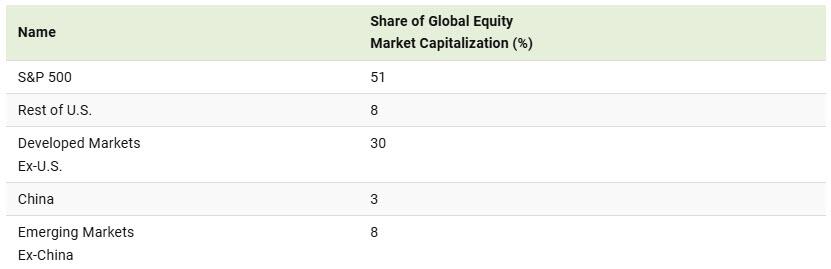

The S&P 500 Makes Up 51% Of Global Stock Market Value

This graphic breaks down the global equity market into five major pieces as of Dec. 31, 2023, using data from S&P Dow Jones Indices.

Visual Capitalist’s Marcus Lu highlights the massive share of market capitalization that is located in the U.S., particularly within the S&P 500 index.

Data and Key Takeaways

The figures we used to create this graphic are listed in the table below.

As of the end of 2023, companies listed in the U.S. accounted for 59% of global stock market value. Most of this value is in the S&P 500 index, which consists of the 500 largest publicly traded companies in the country.

Nearly all of the world’s trillion-dollar companies belong in the S&P 500: Apple, Nvidia, Microsoft, Alphabet, Amazon, and Meta (also known as the Magnificent Seven)

Looking Outside the U.S.

After U.S. markets, Developed Markets ex-U.S. account for the next biggest share. Shown as the green segment in the chart, developed markets are economies with established financial systems and high levels of income.

Excluding the U.S., the largest developed markets (by capitalization) according to S&P are Japan, UK, Canada, France, and Switzerland.

Finally, there’s Emerging Markets (yellow section) and China (red section). China is considered an emerging market, but was shown separately given its significance to the global economy.

According to S&P, the largest emerging markets (by capitalization) are China, India, Taiwan, Brazil, and Saudi Arabia. Emerging markets are economies in the process of rapid growth and industrialization, as well as higher volatility.

As of October 2024, the most valuable emerging markets companies are Saudi Arabia’s Saudi Aramco and Taiwan’s TSMC.