NVDA Doubles AAPL, Trump Blows Up The Dollar, & The End Of OPEC: Saxo’s Outrageous Predictions For 2025

It’s that time of year again…

Saxo’s Outrageous Predictions are not exactly news and not exactly real – at least not yet.

And while they don’t know which stories will drive the global economy in the coming year, their 2025 predictions, from Nvidia trouncing its Mag 7 peers to the fall of OPEC, from a bold bet on reflation in China to a great leap forward in biotech, are just as promised…

Outrageous.

Trump 2.0 blows up the US dollar

Summary: As the new Trump administration turns the global financial system on its head with huge tariffs, the world scrambles to find alternatives to the dollar

The globalist system that formed in the ashes of World War II was built on the combination of a US security guarantee to protect trade routes for the “Free World” and the use of the US dollar as the chief currency for transactions and as a store of value. Even after the greenback’s link to gold was broken by US President Nixon in 1971, the US dollar continued its domination in the globalised economy.

Cue the 2016 US election and the advent of President Trump, the first president in living memory to bash at the foundations of the global system, demanding tariffs for imported goods to right the huge US trade deficit wrongs and decrying the cost of maintaining the vast US security umbrella. US security alliance partners were shocked, and China was put on notice. But then came the pandemic and a new election brought Biden and encouraged the notion that Trump was an aberration, not the new norm. Then there was the 2024 US election and return of Trump. If Trump 1.0 was the warm-up act for deglobalisation, Trump 2.0 will prove the main event, with all of its consequences for the US dollar.

In 2025, the new Trump administration overhauls the entire nature of the US relationship with the world, slapping massive tariffs on all imports, while slashing deficits with the help of an Elon Musk-run Department of Government Efficiency (DOGE). The implications for the US dollar are dire for trade around the world, as it cuts off the needed supply of dollars to keep the wheels of the global USD system turning, ironically risking a powerful spike higher in the US dollar. Instead, safety valves are found, as global financial actors scramble for alternatives. China and the BRICS+ transact with gold-backed digital money and, to a degree, directly in a new gold-backed offshore yuan. Europe rebases its trading relationships increasingly in the euro. Gold-linked crypto stablecoins add to the mix, as this dramatic new chapter in global financial markets begins.

Potential market impact: The crypto market quadruples to more than USD 10 trillion, the US dollar falls 20% against major currencies and 30% versus gold. The US economy continues to reflate, but wages keep up with goods inflation, as production resources reshore to the US. US exporters advantaged.

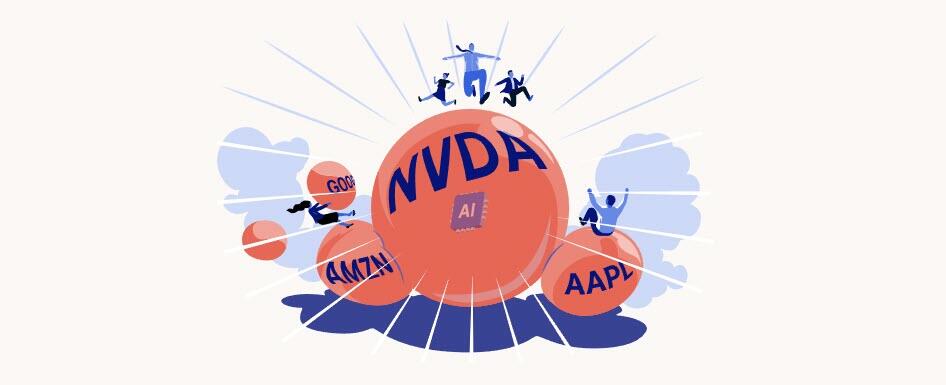

Nvidia balloons to twice the value of Apple

Summary: Armed with its revolutionary AI chips, could tech giant Nvidia grow to twice Apple’s size and become the most profitable company of all time?

The saying goes that in a gold rush, the only operators sure to make a fortune are the sellers of shovels, since most miners will fail to find any gold. What we are seeing in the AI space feels much like a gold rush, as the monopoly info-tech giants and a crush of start-ups have rushed to harness the golden promises of generative AI. These stretch from Meta’s Metaverse to the incredible number-crunching loads to drive new applications like autonomous driving. The primary shovel-seller in the AI gold rush is Nvidia, designer of the juiced-up chips, and just as importantly, the software ecosystem at the heart of the lion’s share of AI data centres.

In 2025, Nvidia’s success is supercharged further with the availability in volume of its revolutionary 208-billion transistor Blackwell chip, a chip that drives up to a 25-fold increase in performance of AI calculations per unit of energy consumed relative to the prior H100 generation. With the intensifying AI arms race as no giant or even government wants to be left behind, and as AI data centre electricity costs have soared, the insatiable demand for the more powerful and yet less power-hungry Blackwell chips sees Nvidia taking the crown as the most profitable company of all time. It handily surpasses Apple’s record USD 105 billion of profits next year, and with far faster growth baked into expectations, its market cap nearly doubles again, making it twice the size of Apple. This sees it tower above all other companies in the world at a value of USD 7 trillion, or 10% of the global equity market. Apple and other tech giants’ valuations suffer in relative terms, as their profitability is weighed down by the need to build titanic data centres to keep up in the AI gold rush.

Potential market impact: Nvidia shares trade well north of USD 250, before the market begins to question its potential to grab an ever-greater share of corporate profits, and as unwelcome regulatory scrutiny on its monopoly status tempers the outlook.

China unleashes CNY 50 trillion stimulus to reflate its economy

Summary: Having created history’s most epic debt bubble, China boldly bets that fiscal stimulus to the tune of trillions of CNY is the only answer.

China is mired in a classic balance sheet recession akin to the Japanese experience of the 1990’s. In an epic binge, the country inflated a corporate debt and real-estate debt bubble without parallel in global economic history. China’s corporate debt alone stands at north of 150% of GDP. Local government debt is on the order of another 80-90% of GDP. Household debt is not as high as elsewhere, but much is linked to a suffering real estate market.

When countries enter a balance sheet recession, every actor in the economy, both public and private, is strongly incentivised to pay down debt to repair balance sheets. But this effort to improve finances only worsens the collective outlook as economic activity and prices crater. The government can choose many paths in a balance sheet recession, but all come with significant risks. If you write off the debt, the economy deflates and the wealthy class of creditors is crushed. If you do nothing, the country can stay in a decades-long malaise. If you run massive trade surpluses to have other countries finance your balance sheet repair as China is already trying to do, you risk the ire of other nations and trade wars. If you force a reflation with massive fiscal stimulus, inflation can create social unrest.

In 2025, China makes a bold bet that reflation is the only answer and thinks it can manage the inflationary risks as it unleashes a gargantuan set of fiscal initiatives that add up to promises of more than CNY 50 trillion (about USD 7 trillion) in 2025 and the following years. Much of the spending goes directly into consumers’ pockets via e-CNY digital currency, so that it will be injected straight into the economy rather than to pay off debt. China also adds heavy doses of social engineering in its stimulus, incentivising companies to reduce working hours to improve quality of life. This boosts leisure time, consumption, company formation, family formation and childbearing.

Potential market impact: A strong reflationary impact in China and the world, outperformance of EM relative to DM and China in particular, higher commodity prices globally, a stronger Chinese renminbi.

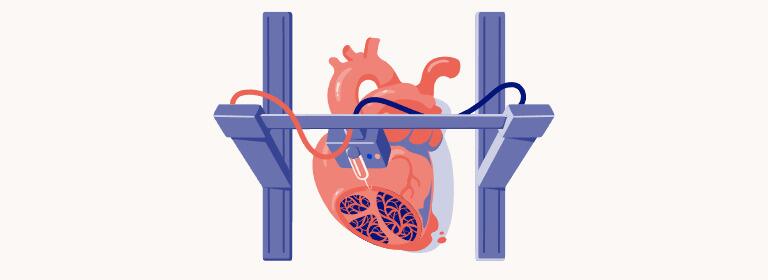

First bio-printed human heart ushers in new era of longevity

Summary: It’s alive! Fusing bioengineering and medical science, scientists successfully bio-print a human heart, promising to extend the lives of millions.

In an unprecedented scientific breakthrough, 2025 sees researchers successfully bio-print a fully functional human heart, using advanced 3D bioprinting technology. Starting with high-resolution CT scans, scientists create an intricate digital model capturing every minute detail of the heart’s complex structure. This model serves as the blueprint for a state-of-the-art 3D bioprinter, which meticulously layers human stem cells and biodegradable scaffold materials to construct the organ with remarkable precision.

Once printed, the nascent heart is placed in a specialised bioreactor that mimics the physiological conditions of the human body. Here, the heart matures over several weeks, allowing the cells to organise and differentiate properly, establishing vital networks of blood vessels and electrical pathways necessary for normal heart function. In a groundbreaking surgical procedure, the matured human heart is then transplanted into a pig for testing.

The implications of this achievement are monumental. It promises to alleviate the global shortage of donor organs by providing bio-printed hearts tailored to the DNA of individual patients, thus reducing the risk of rejection. This breakthrough paves the way for extending human longevity by replacing failing organs with custom-made, fully compatible ones. Additionally, it opens avenues for innovation in bio-printing other complex organs, revolutionising regenerative medicine and personalised healthcare.

This massive advance in biotechnology history captures global attention. The fusion of bioengineering and medical science promises to improve and lengthen the lives of millions in years to come.

Potential market impact: The success in bio-printed organs sees growth expectations jump for the biotechnology and 3D printing sectors. Most companies in this space are in the start-up phase, but watch for a rash of IPOs in the space. More generally, this surge in innovation and investment could reshape the healthcare industry, leading to improved patient outcomes and significant economic growth.

Electrification boom ends OPEC

Summary: As electric vehicles become more affordable, could oil-rich OPEC become irrelevant in 2025 and find itself on the ash heap of history?

In the space of just a few years, China has made a mockery of all prior assumptions about the potential scale of both EV production and adoption. Schroders, a nearly trillion-dollar asset manager, touted growth potential for Chinese EV production back in early 2021, projecting that EV sales might reach close to 5 million vehicles by the end of 2024 and a market share of 15%. The ensuing reality blew the roof off these projections, as Chinese EV registrations rose above 8 million already in 2023. And by September of 2024, EV market share of new car sales was reaching north of 45% in China, as overall EV sales growth rose above 40% year-on-year. This is some six years quicker than expected.

China is showing the way in the transportation electrification boom. As other countries join China in rapidly building out exponential growth in production capacity, battery prices will deflate further, making EVs cheaper than their petrol-burning counterparts, with a crossover point in costs within 12 months, even on an unsubsidised basis. With an exponential adoption rate curve dead ahead, it brings forward projections of peak oil to as early as 2025 and the anticipation of an accelerating decline in demand in the years ahead.

In 2025, with the writing on the wall on the forward demand picture since two-thirds of oil ends up as gasoline or diesel in cars and trucks, OPEC finds its relevance shrinking further and its multi-million barrel per day production limits irrelevant. With some members already cheating production quotas to grab what income they can and export demand falling, a majority of members quickly realise the jig is up. Amidst the bickering and in-fighting, key members leave. This consigns OPEC to the ash heap of history. Former members max out production to ensure market share, driving a large drop in oil prices.

Potential market impact: Crude oil slumps in price, a boon for airlines, chemical, paint and tire manufacturers and freight and logistics companies. But the market balances quickly and oil prices stabilise, as higher cost suppliers, especially in North America, shut down expensive shale oil production. Japanese carmakers find themselves in a desperate race to catch up with other EV players.

US imposes AI data centre tax as power prices run wild

Summary: With tech giants sucking up power supplies for their new AI data centres, utility bills skyrocket and an outraged public demands action.

The AI revolution is a power-hungry one. The tech giants see that current electricity supply falls far short of what is required to power the massive new AI data centres they hope to build. They are already taking dramatic steps to secure stable, long-term power sources. Microsoft has contracted with Constellation Energy to reopen one of the old nuclear reactors at Three Mile Island. Google and Amazon are striking deals with US utilities and other providers to create small modular nuclear reactors (SMRs) for their planned AI data centres. But these are all long-term projects – for 2030 and beyond in the case of the latter two. What about the energy needs right here and now, as the AI arms race reaches new white-hot intensity already in 2025?

In 2025, US power prices spike higher in several populated US areas, as the largest tech companies scramble to lock in baseload electricity supplies for their precious AI data centres. This inspires popular outrage, as households see their utility bills skyrocket, aggravated by the huge spikes in power prices for electricity consumed at home during peak load periods in the evening. In response, many local authorities move in to protect political constituents, slapping huge taxes and even fines on the largest data centres in a move to subsidise lower power prices for households. The taxes incentivise investment in massive new solar farms with load balancing battery packs, but also dozens of new natural gas-driven power stations, even as the demand for ever more power continues to rise faster than supply. Rising power prices drive a new inflationary impulse.

Potential market impact: A massive boom in US investment in power infrastructure. Companies like Fluor rise on signing massive new construction deals. Tesla’s accelerating Megapack gets increasing attention. Long-term US natural gas prices more than double, a significant contributor to a more inflationary outlook.

A natural disaster bankrupts a large insurance company for the first time

Summary: After a year of wild weather in 2024, a catastrophic storm hits the US in 2025, sinking a large insurer that has underestimated climate change risks.

Climate change is driving an intensification of the earth’s water cycle. As the atmosphere warms, it can hold more moisture, and rainfall intensity has been rising sharply in recent years. This past year has seen wild weather events around the world, from a deluge that created temporary lakes in some of the driest areas of the Sahara, to deadly flooding in Slovakia and Poland as rivers burst their banks and in Connecticut and New York after a “once in a thousand year” rainfall event. Climate scientists have charted that rainfall amounts that fall in heavier rains around the world are marching ever higher. This means the risk that what was formerly considered a 100-year or even 1000-year rain and flooding event could happen on the order of once a decade, or even more frequently.

In 2025, a catastrophic storm and rainfall event in the US catches the insurance industry unprepared, inflicting damage stretching into many multiples of the USD 40 billion in claims linked to Hurricane Katrina in 2005. One of the largest US insurers significantly underestimated the insurance risks from climate change, leading to underpriced policies in the affected region. With insufficient reserves to cover claims and inadequate reinsurance to mitigate the costs of this extreme event, panic spreads across the entire industry. A crisis unfolds, prompting government-level discussions on whether to bail out the failing company and the other walking wounded in the industry to prevent widespread risk contagion. The disaster forces a reset in natural disaster pricing, profoundly marking down real estate values in many housing markets. Consumer confidence takes a hit on the insecurity of the value of many homeowners’ largest asset, their house.

Potential market impact: Berkshire Hathaway shares rise as Buffett’s company has enough capital to weather the panic and the company gains market share.

Sterling erases post-Brexit discount versus the euro

Summary: As Europe’s economy struggles, fresh fiscal policy winds are blowing in the UK, driving sterling back to levels versus the euro not seen since before Brexit.

The UK outlook is as constructive as ever in the post-Brexit era. That is, it is the most positive relative to the sick man of Europe, which is, well…Europe, or at least the core Eurozone countries, France and Germany. Fresh fiscal policy winds are blowing in the UK, where the new UK Labour government announced budget priorities ahead of 2025 that avoided the most growth-damaging types of tax hikes on income, while trimming the least productive public sector spending in moving to shrinking its deficits. By cutting unproductive subsidies like winter fuel aid for pensioners, encouraging investment in the property and manufacturing sectors and raising incomes for public sector workers, the UK is primed for solid nominal growth in the years ahead, keeping the Bank of England policy rate at a high level compared to major global peers.

On the European continent, the situation couldn’t be more different. France has a dysfunctional government that is mired in a five-year exercise of getting its out-of-control budgets in order. It has already announced growth-killing taxes on personal and corporate income and austerity. Shield your eyes! Meanwhile, Germany remains the sickest of the sick in Europe, unwilling to debt finance desperately needed domestic investment in housing and infrastructure that it could easily afford. Its former economic model of cheap Russian energy inputs to drive its huge industrial base and manufactured exports lies in ruins. And its non-luxury car producers have been rendered uncompetitive by both high energy input costs and China running away with new EV battery technology and gobbling up a dominant global export share in the critical auto sector. Germany must find a new way – but that is perhaps an outrageous prediction for 2026…

In 2025, sterling rises through 1.27 versus the euro, the level it traded ahead of the Brexit referendum, thus erasing its entire post-Brexit vote discount.

Potential market impact: Encouraging domestic investment and a more robust growth outlook support sterling versus the flailing euro, seeing the Euro/Sterling rate fall as low as 0.7500, below the rate the day before the Brexit vote at 0.76. The UK FTSE 100 posts a strong performance.

* * *

Tyler Durden

Tue, 12/03/2024 – 10:05

via ZeroHedge News https://ift.tt/74Pp9wd Tyler Durden