Treasury Dept’s Highest-Ranking Career Official Rage-Quits After Musk’s DOGE Team Probes Payment System

The Treasury Department’s highest-ranking career official quit after a clash with aides of Elon Musk over access to sensitive payment systems, according to the Washington Post, citing (of course), three anonymous sources.

David A. Lebryk, a decades-long Treasury official who President Trump named as acting secretary upon taking office last week, announced his retirement in a Friday email to colleagues. According to the report, Lebryk had a dispute with Musk surrogates over access to the US government’s payment system used to disburse trillions of dollars every year.

[Imagine Musk and team uncover decades of improper payments and shady dealings?]

The Musk surrogates are affiliated with the Department of Government Efficiency (DOGE), and have been asking since the election for access to the system, according to the report. The requests were reiterated after Trump’s inauguration.

After Trump pick Scott Bessent was confirmed as Treasury Secretary on Monday, Lebryk ceased to be acting agency head.

The payment system in question is run by a handful of career officials within the Bureau of the Fiscal Service – which controls the flow of more than $6 trillion annually to households, businesses, and other entities nationwide – and includes Social Security, Medicare, federal salaries, payments to government contractors, tax refunds, grant recipients, and more.

The clash is the latest incident involving career ‘deep state’ bureaucrats vs. the Trump administration. And of course, WaPo, the CIA’s favorite tentacle, frames it as follows:

The clash reflects an intensifying battle between Musk and the federal bureaucracy as the Trump administration nears the conclusion of its second week. Musk has sought to exert sweeping control over the inner workings of the U.S. government, installing longtime surrogates at several agencies, including the Office of Personnel Management, which essentially handles federal human resources, and the General Services Administration, which manages real estate. (Musk was seen on Thursday visiting GSA, according to two other people familiar with his whereabouts, who also spoke on the condition of anonymity to describe internal matters. That visit was first reported by the New York Times.) His Department of Government Efficiency, originally conceived as a nongovernmental panel, has since replaced the U.S. Digital Service.

Translation:

Unfortunately for the career bureaucrats, Trump signed an executive order instructing all agencies to ensure DOGE has “full and prompt access to all unclassified agency records, software systems, and IT systems,” which appear to include the Treasury payment systems.

Musk has previously slammed rising national debt as an existential threat to the country, while DOGE has already made progress in rooting out bullshit programs established by Democrat administrations.

The Director of National Intelligence and the U.S. Attorney General have until Feb. 7 to present a full disclosure plan for the records pertaining to the assassination of President John F. Kennedy, according to an executive order signed by President Donald Trump on Jan. 23.

“I have now determined that the continued redaction and withholding of information from records pertaining to the assassination of President John F. Kennedy is not consistent with the public interest, and the release of these records is long overdue,” Trump wrote in the order.

Since Kennedy was shot in Dallas on Nov. 22, 1963, some have speculated about what the government knows, and the slow release of documents has only heightened suspicions, according to those calling for declassification.

According to the National Archives, more than 5 million documents, photographs, and other artifacts related to the assassination are in the government’s possession.

Approximately 99 percent of the records are available for the public to review, although around 5,000 documents remain sealed or redacted.

Some have additionally questioned the official narratives regarding the assassinations of Robert F. Kennedy and Martin Luther King, Jr.. The order also calls for King’s records to be released—with the plans due by early March.

“Their families and the American people deserve transparency and truth,” Trump’s order states. “It is in the national interest to finally release all records related to these assassinations without delay.”

While signing the executive order, Trump said, “People are waiting for this for years, for decades, and everything will be revealed.”

He instructed his staff to hand the pen he used to sign the order to Robert F. Kennedy, Jr.—the nephew of the deceased president and the son of the slain former senator.

RFK Jr. has long criticized the government for concealing documents and has suggested the Central Intelligence Agency may have played a role in his uncle’s death.

He quoted the 35th president in a Jan. 24. post on social media platform X.

He said JFK warned that ‘The very word ‘secrecy’ is repugnant in a free and open society, and we are as a people inherently and historically opposed to secrecy … We decided long ago that the dangers of excessive and unwarranted concealment of pertinent facts far outweighed the dangers which are cited to justify it.’”

He suggested the lack of transparency has eroded the public’s trust in government.

RFK Jr., who has been nominated by Trump as Health and Human Services Secretary, said the government owes Americans the truth and thanked the president for working to release the documents.

“A nation that does not trust its people is a nation that is afraid of its people,” he wrote. “A government that withholds information is inherently fearful of its citizens’ ability to make informed decisions and participate actively in democracy.”

A law passed by Congress, the President John F. Kennedy Assassination Records Collection Act of 1992, ordered all government records related to the incident to be released to the public in full by Oct. 26, 2017.

Exceptions were made for items deemed harmful to intelligence operations, foreign relations, military defense, or law enforcement and that such harm outweighed the public’s right to know.

When the deadline approached during Trump’s first term, he acknowledged in his order accepting redactions proposed by certain unnamed agencies and executive departments.

He subsequently directed the agencies to reconsider the redactions within three years and further disclose information.

The deadline was extended three times during President Joe Biden’s term in office.

Trump said on an episode of the “All-In” podcast in June 2024 that the CIA was “probably behind” the pressure to delay the release of all the documents during his first administration.

He said people have been waiting a long time for the information to be declassified, and they deserve transparency from their government.

“Whatever it is, it will be very interesting for people to see,” Trump said. “And we’re going to have to learn from it.”

The 888-page report produced by the commission has generated questions from researchers since its release in September 1964.

Other investigations followed, including one from the Rockefeller Commission in 1975.

Commissioners studied the CIA’s domestic activities and determined the agency was not involved in the assassination and that the president was not hit by a shot from in front of the vehicle—a claim some have made because Kennedy’s head is seen moving backward in the widely distributed Zapruder film.

Over the course of 1975 and 1976, the Senate’s Church Committee investigated intelligence agencies’ actions.

Initial findings led the committee to call for another look at the assassination.

Lawmakers in the House of Representatives established a Select Committee on Assassinations in 1976.

The group concluded that the president was likely murdered because of a conspiracy that could have included elements of organized crime.

However, the committee agreed with the Warren Commission’s findings that Oswald fired the fatal shot and the one that struck the president and then-Texas Gov. John Connally.

Questions have surrounded the bullet the commission alleges struck both individuals, with the so-called “single bullet theory” a main premise of the Oliver Stone film “JFK” released in 1991

The new order was one of the president’s promises to voters.

“When I return to the White House, I will declassify and unseal all JFK assassination-related documents,” Trump said repeatedly on the campaign trail last year. “It’s been 60 years, time for the American people to know the truth.”

In a 1998 report, the Assassination Records Review Board suggested that releasing documents could help restore trust in the government.

“The suspicions created by government secrecy eroded confidence in the truthfulness of federal agencies in general and damaged their credibility,” lawmakers wrote.

At 5 PM EST, Fed Workers’ Pronoun Use On Emails Will Be ‘Was/Were’

The Trump administration is following through with a mandate the American people gave him to rid the federal government of cultural Marxism, where woke activists have been placed into managerial positions over the years – not necessarily based on merit – but on gender or other nonsense.

ABC News reports that federal employees at the Centers for Disease Control and Prevention and the Agency for Toxic Substances and Disease Registry have until 5 pm EST to remove pronouns from their email signatures. The directive was stated in internal memos obtained by the media outlet, citing two executive orders signed by Trump on his first day to dismantle toxic wokeism in the federal government.

“Pronouns and any other information not permitted in the policy must be removed from CDC/ATSDR employee signatures by 5.p.m. ET on Friday,” Jason Bonander, the CDC’s Chief Information Officer, wrote in a memo to staff on Friday morning.

Bonander said, “Staff are being asked to alter signature blocks by 5.p.m. ET today (Friday, January 31, 2025) to follow the revised policy.”

A similar directive was pushed through the Department of Transportation on Thursday after a US Army Black Hawk helicopter collided with a commercial jet over the Potomac River. President Trump has slammed years of DEI hirings at the Federal Aviation Administration, made by the Biden-Harris administration.

Employees at the Department of Energy also received a directive about pronoun elimination in emails to meet Trump’s executive order requirements for the removal of DEI “language in Federal discourse, communications and publications.”

Apparently, all federal employees have now received 5 pm EST. deadline to eliminate pronouns from email signatures.

All federal employees ordered to eliminate pronouns from all mail signatures by 5PM pic.twitter.com/dBAw0mazEY

Former US Secretary of Transportation Pete Buttigieg, America’s far-left DEI warrior, quietly removed his gender pronouns from social media profiles in recent days. We theorize in the note why…

Trump signed two executive orders calling for an end to what his administration called “radical and wasteful DEI programs” and aiming to restore “biological truth to the federal government.”

Under Obama and Biden, pronoun-wielding gender Marxist activists were being installed across all levels of government – not based on merit – but based on gender, race, and other woke attributes that do not increase job performance.

Wow. So if you call the @DeptVetAffairs, this is one of the first messages you get. It’s instructions on how to add pronouns to your profile.

Customs and Border Protection has ordered agents to avoid using “he, him, she, her” pronouns for illegal aliens “until you have more information about, or provided by, the individual.” https://t.co/FdfWmYh3Gd

“A man’s assertion that he is a woman, and his requirement that others honor this falsehood, is not consistent with the humility and selflessness required of a service member.”

– White House Guidance

Was it the miasma of cognitive dissonance blackening the air-space over the DC swamp that caused the deadly collision of AA Flight 5342 and a Blackhawk Helicopter this week – an impenetrable fog arising from the fetid exhalations of so many hyperventilating swamp creatures brooding between the urges of fight-or-flight as Mr. Trump deploys his chosen pest-controllers across the Potomac Basin?

Altogether, these many parasitical swamp creatures make up the greater DC blob, and the blob convulsing and fibrillating is what you witness in these committee hearings with Bobby, Tulsi, and Kash. For instance, fake “progressive” Bernie Sanders (D-VT) faced with the reveal that he leads his colleagues in pharma “contributions” (just under $2-million) . . . or fake Cherokee Elizabeth Warren (D-MA) in a fugue state over the perceived threat of Mr. Kennedy to pharma profits . . . or presidential pardon recipient Adam Schiff (D-CA) lecturing Mr. Patel on ethical behavior. . . or Ms. Gabbard enduring the meltdown of Senate Intel Committee tool Michael Bennet (D-CO).

Behind these histrionics by the big gators and peccaries of the collapsing Democratic Party is pure scintillating fear.

They are afraid that all of their hoaxes and lies of recent years will be exposed in the months ahead. And they fear that such exposure might lead eventually to legal complications for them. All of that implies loss-of-power, the single element that demonically drives their careers.

The fact is they have already lost their grip on the levers of power and, for the moment, that is all that matters. They especially no longer control the Department of Justice, its subsidiary, the FBI, the many public health agencies under Health and Human Services, and the many-footed intel “community,” as it styles itself. These agencies are where the truth about our national affairs has been locked up. Now, the citizens will either see what’s there, or find out what has been deliberately destroyed – such as the internal agency email correspondence over RussiaGate, the Covid-19 operation (and the deadly vaxx campaign), the J-6 affair (and the pipe-bomb sideshow), the weird, documented irregularities of the 2020 election, the Ukraine War money-laundering shenanigans, the manifold janky DOJ prosecutions of Mr. Trump, and much more.

Every day now since January 20, heads explode all over DC as the executive orders roll out and the insanity of whatever lurked behind “Joe Biden” gets systematically expunged from the order of things.

And as this happens, the more plainly deranged the past four years looks.

Did they really believe that men dressing-up as women would improve the US military?

Or was it a traitorous effort to weaken and demoralize our armed forces?

Was DEI a public ethics exercise or a massive jobs program for incompetents?

In what way did “Joe Biden’s” Department of Homeland Security imagine that funneling known criminals, certified lunatics, and saboteurs across the border squared with their duty to protect and defend the country?

And how did it happen that US taxpayers’ money got shelled out to fake “religious” NGOs in Mexico minting debit cards for border-jumpers, handing them wads of cash, cell phones, airplane tickets, fully-equipped backpacks, and apps for evading arrest?

In effect these NGOs took over the exact job description of “coyote” formerly performed by the criminal cartels — leaving the cartels free for the more lucrative rackets of dealing fentanyl and trafficking women and children.

The corruption in all this has been supernatural, and the fact that, until late 2024, seventy-million Democratic Party American voters thought this was all okay is extra-supernatural.

What happened to their minds?

The cliché of “Trump derangement” doesn’t really answer that.

What it probably comes down to was the stunningly successful mind-fucking operation run by the blob (the CIA and the darker elements of the DOD in particular), in league with captured news media, to bend and distort the consensual perception of reality — all of which leads to the question: why?

The two main answers to that seem to be:

1) Some organized entity seeking to destroy the country for instance, the Chinese Communist Party, or the World Economic Forum, or

2) that the blob had evolved into such an overt criminal racketeering operation that it increasingly and desperately needed to keep covering its mighty ass.

Thus, the Democratic Party became the blob’s enforcer and the news media became its propaganda arm.

And the “thinking class” of America especially got ignominiously hosed by all that.

There’s a pretty good chance that blob agents in the Senate will successfully block the confirmations of Bobby, Tulsi, and Kash.

They are all superlative candidates for the particular jobs at HHS, ODNI, and the FBI. But know this: excellent as they are, there are a great many other worthy, dedicated, and stalwart warriors in this land who can take their places if necessary.

The blob has already lost in the political battle-space. All they can manage at this point is some rearguard action.

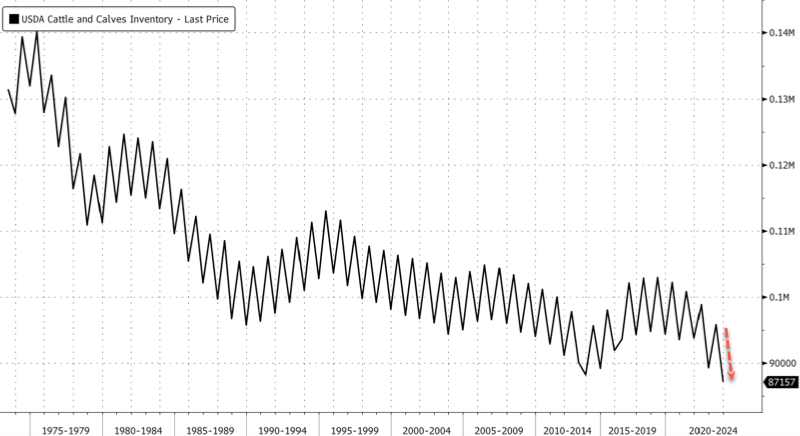

US Cattle Herd Shrinks To 1951 Lows As Beef Crisis Deepens

Update: USDA figures are in: the nation’s cattle herd has plunged to a 74-year low, totaling 86.7 million head.

* * *

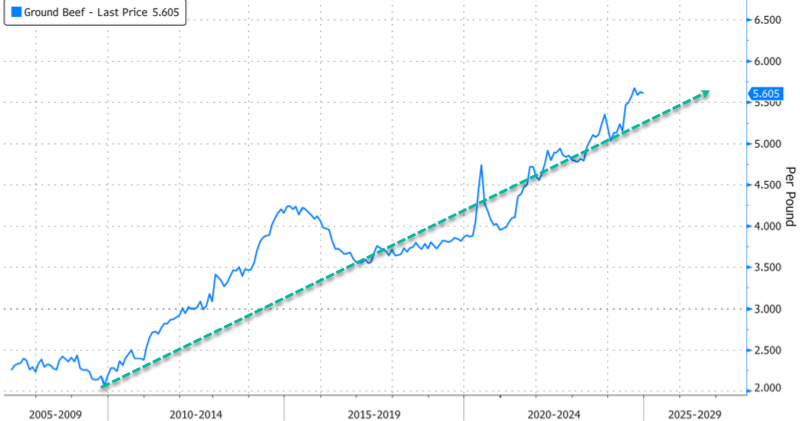

Ahead of this afternoon’s 3 pm est. USDA release of official US cattle inventory data, estimates compiled by Bloomberg forecast the herd will be at its lowest level in more than seven decades. The ongoing cattle supply crunch continues to push supermarket ground beef prices to record highs.

Bloomberg cited estimates from four analysts that expect the US cattle herd as of Jan. 1 will decline by .7% from one year ago. This would mark the lowest level since 1951 and extend the decline for a sixth straight year.

We have thoroughly documented the cattle crisis resulting in higher ground beef prices at the supermarket:

The average retail price for ground beef at the supermarket, calculated by USDA, recently topped $5.61 per pound. Before Covid, that prices was around $3.81.

Live cattle futures on the Chicago Mercantile Exchange have surged to record highs.

The latest CFTC data via Bloomberg shows money managers boosted bullish live cattle bets by 2,764 net-long positions to 161,970 last week, the most bullish in about five years – and nearing levels of the most bullish ever on record.

On top of all this, the nation’s cattle crisis is set to worsen with new pressures: President Donald Trump’s anticipated tariff war 2.0, which is expected to tighten domestic beef supplies.

“All of the things he is talking about have potentially negative consequences more so than anything positive,” Derrell Peel, a professor of agricultural economics at Oklahoma State University, told Bloomberg in a previous report, adding, “Our fate’s pretty well determined in the cattle industry in the US for the next two to four years – and it’s not looking good.”

About a year ago, the USDA projected that the cattle herd could begin rebuilding by 2025. However, that timeline has since shifted to 2027. The reason is primarily because of high interest rates and poor pasture conditions in the Midwest.

“Even as the beef industry has experienced periods of growth over the past decades, the animal count has dropped almost 40% since a peak in 1975. During the current downcycle, which started in 2020, the herd has been shrinking at the fastest pace since the big farm crisis of the 1980s,” Bloomberg noted.

Meta Reportedly In Talks To Reincorporate In Texas, Exit Delaware

First Meta Platforms CEO Mark Zuckerberg dined with Donald Trump at Mar-a-Lago following the presidential election. Then, he appointed UFC CEO Dana White (Trump’s friend) to the company’s board, dismantled its woke fact-checking system, and now is reportedly mulling over relocating Meta’s legal residence from Delaware to Texas—a state that has positioned itself as a pro-business alternative to heavily-regulated blue states run by the radical left.

Wall Street Journal report reveals that Meta has been discussing a potential move to reincorporate outside of Delaware. Sources familiar with the matter said Texas had been heavily considered for the company’s new legal domicile but noted there would be no changes to its corporate headquarters in Menlo Park, California.

Meta Platforms is discussing moving its incorporation from Delaware, where most big U.S. companies are legally housed, people familiar with the matter said. Texas has billed itself as a better destination for companies such as Meta with controlling shareholders like Zuckerberg. The paperwork change wouldn’t relocate its corporate headquarters. The company has talked to Texas officials about the possible changes, one of the people said. It has also considered reincorporating in other states, another person said. -WSJ

The sources continued:

The talks between Meta and Texas predate the new administration, the people said. Meta has been incorporated in Delaware since 2004—well before its 2012 initial public offering. The company is considering the pros and cons of legal setups outside the state and how other companies fared when they reincorporated, the people said. -WSJ

Potential reincorporation of Meta outside of Delaware to Texas, or wherever, comes as Elon Musk has reincorporated several of his companies out of Delaware, including SpaceX and Tesla to Texas, along with Neuralink to Nevada. The exit comes after an activist judge in Delaware rejected Musk’s Tesla compensation package valued at $55.8 billion twice.

“Don’t forget that what the Democrat judge in Delaware is doing to Elon Musk, they could do to anyone else. The State nullified the shareholders, the Board of Directors, and the entire company’s management just to deprive Elon of his pay. Companies must leave Delaware now,” X user Leave Delaware wrote in Decemeber.

Don’t forget that what the Democrat judge in Delaware is doing to Elon Musk, they could do to anyone else.

The State nullified the shareholders, the Board of Directors, and the entire company’s management just to deprive Elon of his pay.

The activist judge in Deleware who went after Musk has been a wake-up call within corporate America. The result will be a continued shift of reincorporation from Delaware to pro-business states – this move will accelerate over the next four years.

We are in far more trouble than most people realize. Fentanyl and other drugs are ravaging our cities, and homelessness, poverty and hunger are rapidly growing all around us. Meanwhile, our federal government, our state governments, and our local governments are drowning in debt, and economic conditions are steadily deteriorating. Corruption is rampant, incompetence is seemingly everywhere, and the moral decay of our society is accelerating. Unfortunately, much of the population is completely oblivious to what is going on because they are deeply addicted to the electronic gadgets that they are constantly staring at.

The following are 11 random facts that show that America is rotting right in front of our eyes…

#1 A new study has discovered that smartphones “are making teenagers more aggressive” and are causing them to “hallucinate”…

Smartphones are making teenagers more aggressive, detached from reality and causing them to hallucinate, according to new research.

Scientists concluded the younger a person starts using a phone, the more likely they would be crippled by a whole host of psychological ills after surveying 10,500 teens between 13 and 17 from both the US and India for the study, by Sapien Labs.

“People don’t fully appreciate that hyper-real and hyper-immersive screen experiences can blur reality at key stages of development,” addiction psychologist Dr. Nicholas Kardaras, who was not part of the team who did the study, told The Post.

Once a month, Kersstin Eshak visits a food pantry in Loudoun County, Virginia to stretch her family’s budget.

Eshak’s husband works at a big box retailer. She works as a substitute teacher. They have income, but with prices up nearly 23% over the past five years — and still rising — their earnings just don’t stretch quite far enough some months.

Food banks across the nation are seeing a similar story: A post-pandemic wave of demand for food driven by working people caught in America’s cost-of-living crunch.

#3 The U.S. national debt was sitting at about 10 trillion dollars when Barack Obama first entered the White House. Today, it is sitting at 36.2 trillion dollars.

#4 Criminals freely roam the streets, but a pastor in Ohio could face jail time for using his church to house the homeless…

The only problem is that while opening up his church — Dad’s Place in Bryan, Ohio — to the homeless, he’s also opened himself up to the reality of city code.

“Pastor Avell has known that this was not permitted use and that he does not have firewalls, he does not have sprinkler systems,” said Bryan Mayor Carrie Schlade. “The kind of things you need in a residential facility. “

#5 A cryptocurrency called “Fartcoin” that was created as a joke currently has a market capitalization of 847 million dollars.

#6 Fentanyl is absolutely destroying communities all over America. For example, check out what has been happing in Las Cruces, New Mexico…

Las Cruces authorities say they first encountered fentanyl in 2018. In 2020, they confiscated a total of 461 pills.

In 2021, the first year of the Biden administration, fentanyl seizures exploded to more than 22,600 – and continued rising: roughly 70,000 pills were seized in 2022 and nearly 86,000 in 2023.

“It wasn’t in Las Cruces, and then it was, and then it was everywhere. In 2021, it really intensified and we’ve seen that the past few years. During that same period from 2018 to 2021, we saw a huge increase in crime: an 85% increase in violent crime and a 71% increase in property crime,” Las Cruces Chief of Police Jeremy Story stated last year during a virtual press conference on New Mexico’s fentanyl epidemic.

#8 We don’t hear much about cargo theft, but it reached a staggering 454 million dollars in 2024. That was a brand new all-time record high…

Cargo theft hit a record high in the U.S. and Canada for the second consecutive year, and the trend is expected to continue as criminal enterprises have become more sophisticated in their methods.

Verisk CargoNet’s annual analysis released this week found that cargo theft surged 27% from 2023 to 2024, hitting a record 3,625 reported incidents last year with an average value of $202,364 per theft. All told, the losses are estimated at more than $454 million.

#9 According to the New York Times, 15 percent of the “women” in our federal prisons are transgender.

#10 Most of the foods on our grocery store shelves are “highly processed”, and since “highly processed foods” are less expensive many U.S. consumers tend to gravitate to them…

Next time you walk down the aisles of your local grocery store, take a closer look at what’s actually available on those shelves. A stunning report reveals the majority of food products sold at major U.S. grocery chains are highly processed, with most of them priced significantly cheaper than less processed alternatives.

In what may be the most comprehensive analysis of food processing in American grocery stores to date, researchers examined over 50,000 food items sold at Walmart, Target, and Whole Foods to understand just how processed our food supply really is. Using sophisticated machine learning techniques, they developed a database called GroceryDB that scores foods based on their degree of processing.

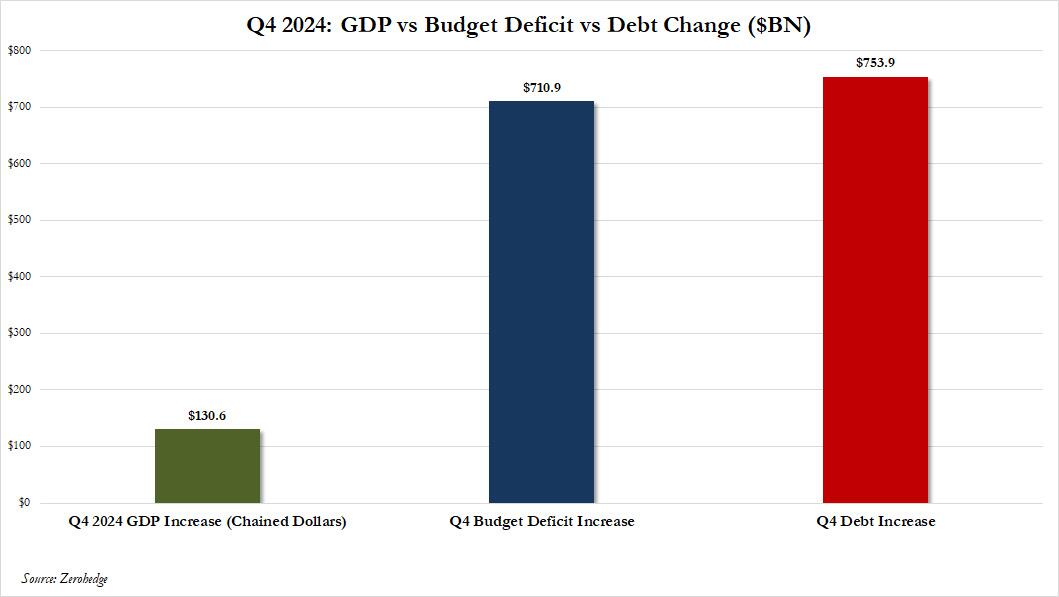

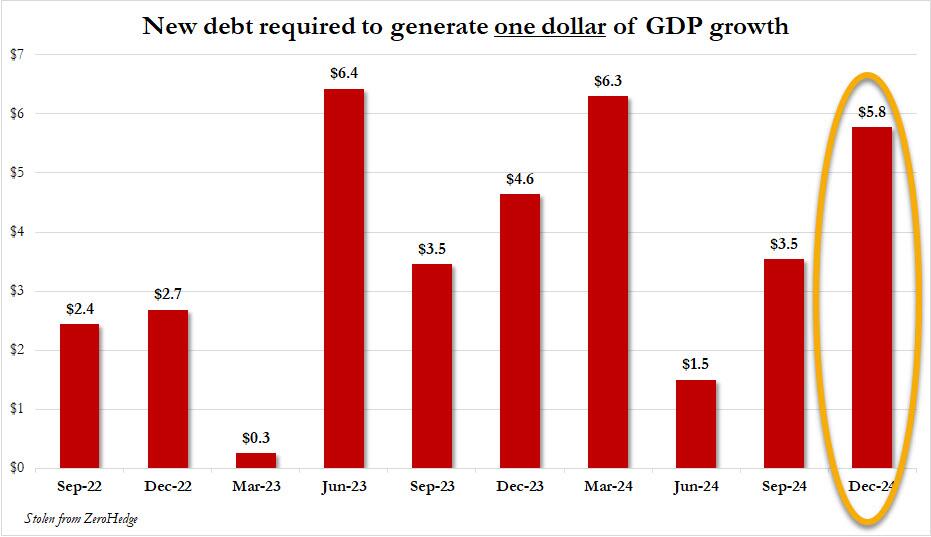

It Took $5.8 In Debt To Generate $1 Of US “Growth” In The Fourth Quarter

We will have much more to say on the composition of yesterday’s first estimate of Q4 GDP which as we highlighted was a very ugly print, and only another quarter of extensive government spending (the 10th quarter in a row) and a record beat of consumer spending relative to expectations, prevented the GDP print from sliding into the 1% range…

… but even if one assumes that there was nothing abnormal about the number itself, the context in which it was derived was astounding. Here’s why.

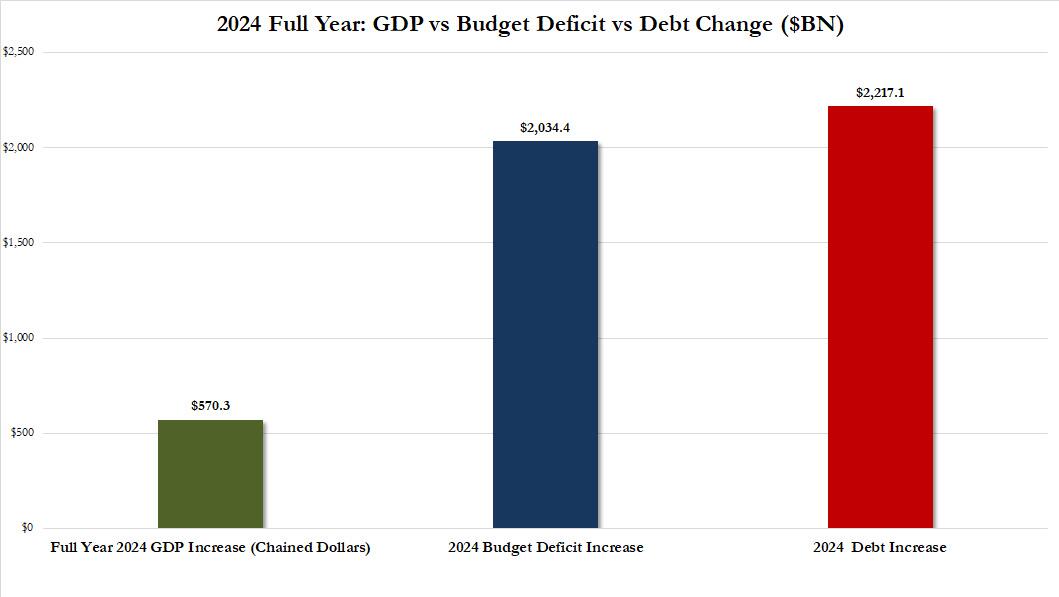

As the BEA reported, in Q4 US GDP grew at a seasonally adjusted rate of 2.3%, below the 2.6% estimate and down from the 3.1% growth pace in Q3. More specifically, the number represented the annualized increase in the 131BN change between what the BEA calculated was chained Q3 GDP ($23.400 trillion) and Q4 GDP ($23.531 trillion). In other words, to keep it simpler, in Q4 the US economy actually grew some $130.6 billion chained dollars.

So far so good. The only problem is what funded this growth, and as regular readers are well aware, in the US the source of all growth is – and for the past 100 years – has been debt, and boy was Q4 a doozy.

As the chart below shows, while the US generated $131bn in chained GDP growth in Q4, this was the result of a $711 billion increase in the US budget deficit, which in turn was funded with a $754 billion increase in debt which, as of Dec 31, 2024, stood at a record 36.218 trillion. The Q4 snapshot is shown below.

And it’s not just Q4. Extending this analysis to all of 2024 we find an almost identical pattern: in the full year 2024, US GDP grew by $570 billion from $22.961 trillion to $23.531 trillion, growth which was made possible by a near record $2.034 trillion increase in the budget deficit, which in turn was funded by a mammoth $2.2 trillion increase in debt.

The bottom line: in Q4 it took $5.8 dollars of debt to create $1 dollar of growth, an increase from $3.5 in Q3 and from $1.5 in Q2, which is to be expected: as we revealed in the summer of 2023, US growth was one giant illusion and was entirely the result of the Biden admins’ massive debt creation spree. No surprise that with the election in Q4 2024, that’s when the bulk of the debt-fueled frenzy would take place.

Taking a bigger picture look, for the full year 2024, it took $3.9 dollar in debt to generate $1 in growth, an increase from the $3.6 in 2023.

What this means is that the only hope the US ever has to grow is to issue debt, or rather issue lots and lots of debt. So good luck to Trump and Elon and DOGE if they hope to slow down the firehose of US debt issuance. They may be successful, but they better have a plan for how to deal with the deep recession that will be immediately triggered as a result.

Chuck Todd, the former moderator of “Meet the Press,” is leaving NBC News, he told colleagues in a Friday memo.

Todd, much like Jim Acosta who rage-quit CNN a few days ago, says he’s going to be ‘pursuing ventures’ outside the NBCUniversal empire.

In recent weeks, Todd has been meeting with other news outlets and potential employers, Variety reports. So unlike Acosta who stomped off to Substack after CNN stuck him in the midnight bitch seat, it looks like Todd is actually making a lateral move of some type.

“There’s never a perfect time to leave a place that’s been a professional home for so long, but I’m pretty excited about a few new projects that are on the cusp of going from ‘pie in the sky’ to ‘near reality,'” Todd told NBC News staffers in a Friday memo reported by Variety. “So I’m grateful for the chance to get a jump start on my next chapter during this important moment.”

He said his “Chuck Toddcast” podcast would be “coming with me,” and urged colleagues to “stay tuned for an announcement about its new home soon.” Todd plans “to continue to share my reporting and unique perspective of covering politics with data and history as important baselines in understanding where we were, where we are and where we’re going.” -Variety

In a statement, NBC News said “We’re grateful for Chuck’s many contributions to our political coverage during his nearly two-decade career at NBC News and for his deep commitment to Meet the Press and its enduring legacy,” adding “We wish him all the best in his next endeavors.”

Todd’s departure – which was a rumor two weeks ago, follows the likes of Don Lemon and Megyn Kelly in terms of well-known TV anchors who have moved on to digital media.

According to Semafor on Jan. 12,NBC host Chuck Todd has “quietly been meeting with Washington media organizations about his post NBC-future,” reportedly telling top editors and leaders from other media organizations that he’s outta there when his contract is up this year, and has discussed potential roles with the network in both broadcast and digital media.

Todd was once a key part of NBC’s broadcast offerings, hosting Meet The Press and a daily Meet The Press politics program on MSNBC and writing for its website. But while NBC announced that Todd would focus on longform projects after stepping down from Meet the Press in 2023, he has been a far less visible presence across the news network and its cable counterpart. –Semafor

Oil traders are making big moves in the Brent-Dubai spread, a contract that lets them bet on the price gap between Middle Eastern crude and global benchmark Brent. The action has hit record levels, thanks to U.S. sanctions on Russian oil that are forcing buyers to look elsewhere for supply, with the situation presenting a lucrative opportunity for traders willing to play.

This week, open interest on the Brent-Dubai contract surged to an all-time high of 448,000 contracts, Bloomberg stated on Thursday. That spike comes as Dubai crude recently hit its highest premium over Brent in at least a decade.

The reason?

Buyers that once relied on Russian oil are scrambling for alternatives, and many are turning to the Middle East.

With demand soaring, Middle Eastern oil prices are climbing faster than crude from other regions. That’s creating ripple effects across the market. European refiners, who might typically buy oil from the North Sea or Kazakhstan, are seeing their usual supplies rerouted to Asia instead. Asian refiners, eager for stable and competitively priced barrels, are snapping up whatever they can get–from wherever they can get it.

For traders, Russian sanctions and Trump’s squeeze on Canada and push on OPEC is a golden opportunity. For refiners and buyers, it’s another challenge in a world where energy flows are anything but predictable.

As long as sanctions stay in place and Russian crude remains off-limits to many, expect more big bets on Middle Eastern oil and continued price swings in global crude markets.

The latest Reuters survey published over the weekend suggested that Saudi Arabia would raise its official selling prices to Asia for March—the highest against the benchmarks since January 2024.