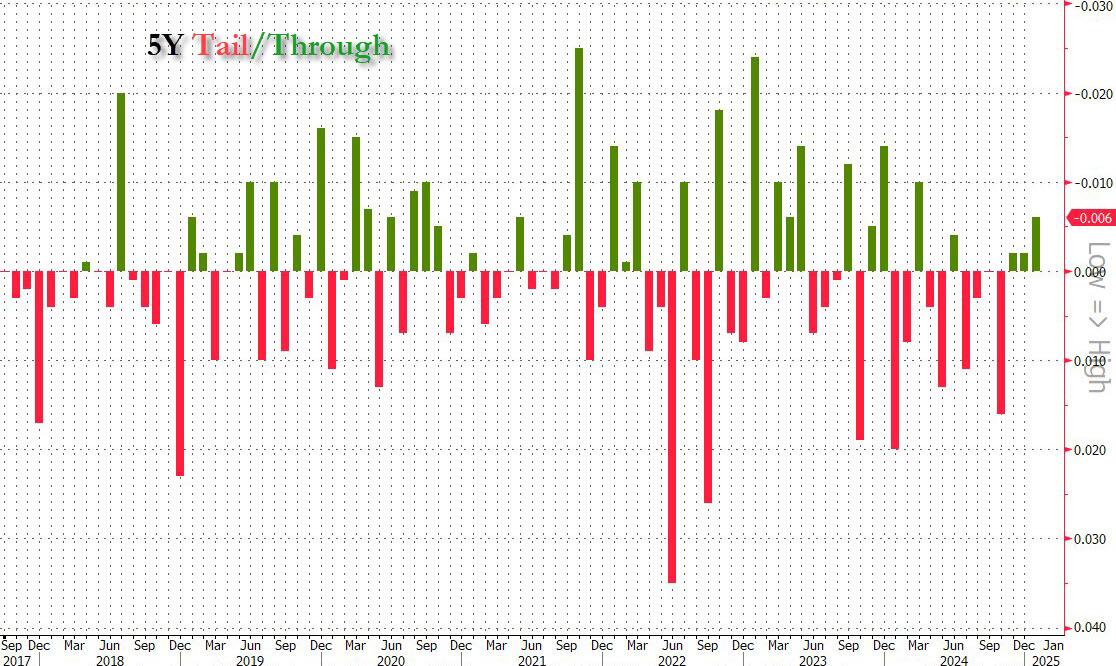

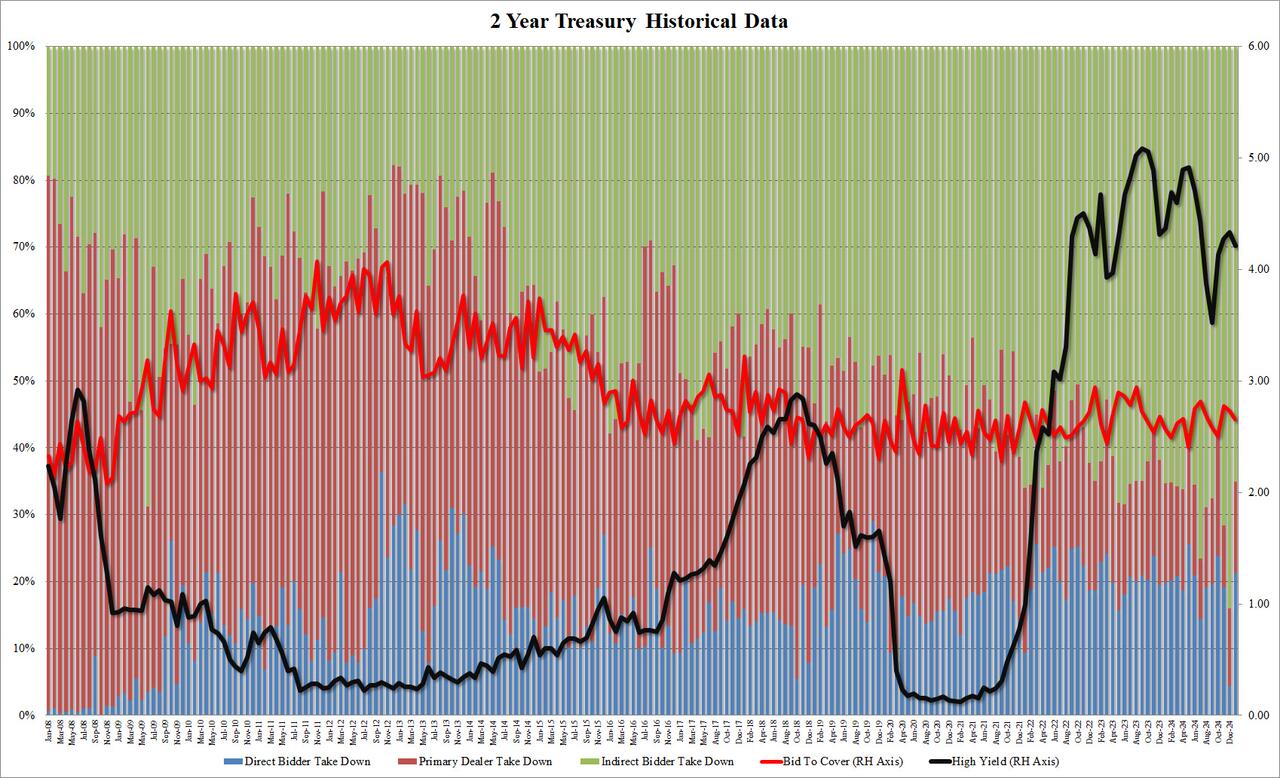

5Y Auction Stops Thorugh With Largest Direct Award In 12 Years

90 minutes after a mediocre 2Y auction hit the tape, the Treasury sold $70BN in 5Y paper in the day’s second auction to start the Fed-abbreviated week, which also sees a 7Y sale tomorrow before the FOMC on Wednesday.

The auction stopped at a high yield of 4.330% which was down from 4.478% in December, and also stopped through the When Issued 4.336% by 0.6bps – this was the third consecutive through auction in a row and followed 4 consecutive tails as sentiment has clearly improved toward the belly of the curve.

The Bid to Cover was unchanged, at 2.40, exactly where it was last month, exactly where the six-auction average is, and where it has been within +/- 5bps since June!

The internals were slightly weaker with Indirects awarded 62.80%, down from 67.3% and the lowest since Jan 2024 (this could be some odd seasonal quirk). And with Directs awarded 26.1%, the most since Dec 2012, Dealers were left with just 11.1%, the lowest since May 2023.

Overall, a solid, and certainly stronger auction, than the 2Y this morning and not surprisingly we have seen yields drip by about 1-2 bps since the results, but it is safe to say that other much more important things are behind the move in rates today than today’s auctions.

Anyone active on X over the weekend undoubtedly saw the growing chatter around Chinese AI start-up DeepSeek. Its meteoric rise to the top of the Apple Apps download charts has been impressive. The company released its R1 model last Monday and explained how to build a sophisticated LLM on a fraction of the cost of some of its more powerful competitors, mostly run or sponsored by US tech giants.

DeepSeek’s development has been in an era where China has been restricted from accessing the highest-end AI technology and chips, with limited access to Nvidia’s products. So for now this raises the potential for stratospheric valuations in US tech firms to be questioned. No wonder then why given this news, it has been a messy day for US equities with Nvidia down -18%, one of its biggest drops on record (resulting in over $600bn in market cap lost). Given that 10yr UST yields are -11bps as well this morning it shows how crucial a handful of US stocks are to global macro.

This is an opportunity to show the stunning rise of Nvidia from an earnings point of view. The CoTD shows it’s gone from LTM earnings of around $4bn two years ago to around $63bn in the last quarterly release. For context, this is around half the total earnings made by listed stocks in each of UK, Germany and France over the last 12 months. The forecasts are for Nvidia to continue to see significant earnings growth. Not surprisingly, this is the chart of the day of DB’s Jim Reid. It could, in fact, also be considered the most important chart in the world right now because if Nvidia goes, everything else will follow.

As Reid notes, “this is a company that has gone from relative earnings obscurity to one of the most profitable in the world inside two years and the largest company in the world as of Friday night.” The problem is that the AI industry is embryonic. And it’s almost impossible to know how it will develop or what competition current winners might face even if you fully believe in its potential to drive future productivity. The stratospheric rise of DeepSeek reminds us of this. The collapse and bankruptcy of Global Crossing which at one point controlled most of the internet traffic pipes and was one of the largest companies in the world, is another reminder.

You mean Global Crossing isn’t a trillion dollar company? (Bonus points if you know who that is without googling) https://t.co/d7d4uVl8l6

That said, for those looking for positives, the Mag 7 fell -18% in the space of a month last summer, before bouncing back to all-time highs. And even with the latest selloff, it was only on Thursday that the S&P 500 was at an all-time high. That said, this news is specific to the Mag 7, unlike the turmoil last summer that was driven by fears of a broader downturn thanks to weak data.

Congress Investigating ‘Numerous Instances’ Of Banks Blacklisting Conservatives

The House Oversight Committee is now investigating ‘numerous instances’ of US banks discriminating against conservatives, after Bank of America denied a claim by President Donald Trump, who admonished Bank of America CEO Brian Moynihan at the World Economic Forum.

During an appearance on Fox News’ “Sunday Morning Futures” with Maria Bartiromo, Oversight Chairman James Comer (R-KY) was asked if he’s investigating “whether or not US banks are debanking conservatives.”

“Yes, we are,” Comer replied. “We’ve heard numerous instances of conservatives being debanked.“

“And what we want to know is, is this a process of the banks’ ESG (Environmental, Social, and Governance) policy? Is, or is this our government stepping in like what we found with Twitter and Facebook where the government stepped in and said they wanted certain conservatives deplatformed and censored and certain conservative content removed,” Comer continued, adding “We want to know, again, is this government involvement, another dirty trick by the Joe Biden administration, or this just bad liberal policy that discriminates against conservatives by the banks.”

Bartiromo seemed surprised, replying “Wow. So you have evidence of some banks debanking conservatives.”

“Yes,” Comer replied. “especially people that were involved in different energy-type businesses and things like that as well as very well-spoken or outspoken conservative activists. So there are numerous instances, enough to open an investigation.”

“Again, is this ESG policy? Which is discriminatory and, ironically, the Democrats have passed all this banking legislation that prohibits discrimination. Is this discriminatory because of ESG, or is it the government, are the bank examiners, as President Trump hinted in his remarks you played earlier, are these bank examiners with a wink and a nod saying don’t let this person bank at your bank?”

‘As President #Trump hinted this in his remarks … are these bank examiners with a wink and a nod saying don’t let this person bank at your bank’ @RepJamesComer… pic.twitter.com/RCCCnTUdrM

Bartiromo added: “Well, this is a very important question because with we know what happened with social media. One thousand people from government agencies were working with social media to censor Americans, censor conservatives, certainly. What will be the impact to these banks? What should these what should these banks expect in the coming month from your office?”

Comer responded: “Well, they’re going to be asked a lot of questions, and I will say this for the banks, during the Biden influence-peddling investigation, the banks were the one entity that did cooperate with us. So I expect that the banks will cooperate with our questions. And, hopefully, we can get some answers.

“Number one, find out if our government was involved in this, if this is another side operation by the Biden administration where they were attacking conservatives. At the very least, we want to change this. We’re not talking about debanking meaning they denied a loan. That happens every day in the banking world. This is just opening up saving accounts and checking accounts. I mean this is unheard of, to do this, and it’s against the law. The laws, ironically, that the Democrats created against discrimination.”

During a virtual appearance Thursday at the World Economic Forum, President Trump, who himself was debanked by two Florida-based financial institutions, called out Bank of America CEO Brian Moynihan, saying: “I hope you start opening your bank to conservatives because many conservatives complain that the banks are not allowing them to do business within the bank, and that included a place called Bank of America.”

NEW: Trump calls out Bank of America CEO Brian Moynihan to his face, says banks should stop debanking conservatives during a virtual appearance at the World Economic Forum.

Lmao. Amazing.

The panel was clearly uncomfortable after Trump made the comment.

In response to Trump’s allegation, Bank of America issued a statement saying it “serves more than 70 million clients and we welcome conservatives. We would never close accounts for political reasons and don’t have a political litmus test.”

First Lady Melania Trump indicated in an October 2024 interview that she herself had been debanked due to her political beliefs.

.@MELANIATRUMP: “I was all agreed they would accept my donations for foster students… The board of directors said we cannot go on. It’s very sad because who suffered? Children from foster communities. They didn’t have a scholarships somebody would provide with them. They didn’t… pic.twitter.com/aUWsrJDSlf

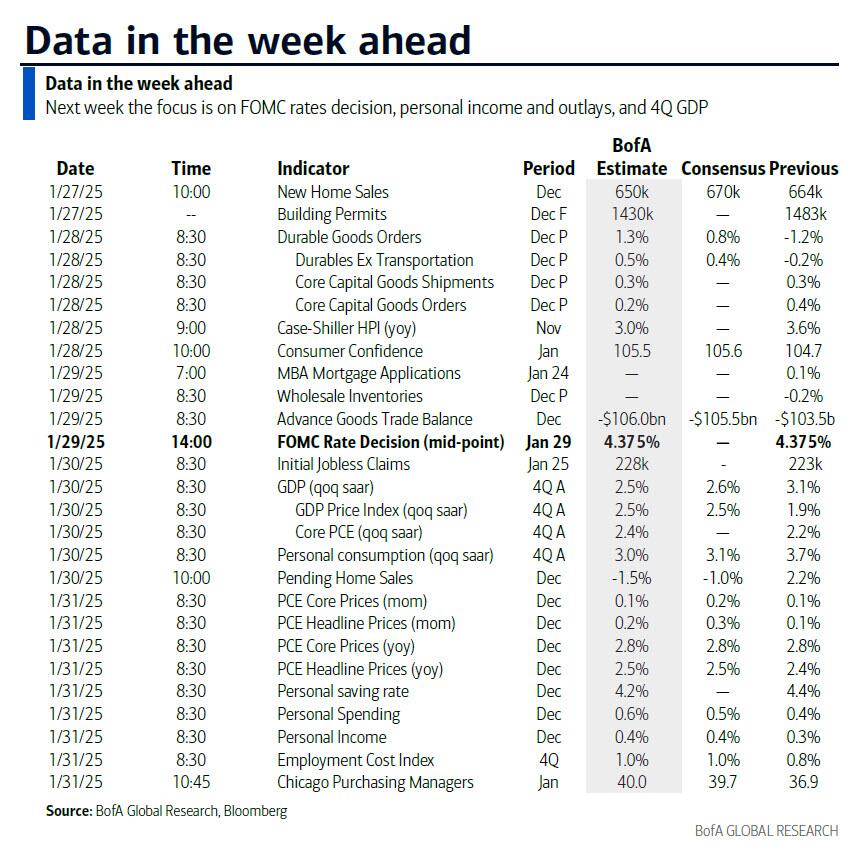

Key Events This Extremely Busy Week: Fed, ECB, Inflation, GDP, And Earnings Galore

One week down, 207 to go of Trump 2.0 and what have we learnt so far?

According to DB’s Jim Reid, it’s hard to say we’ve learnt too much, even with the best part of a hundred executive orders already signed. The market has been relieved that tariffs haven’t been issued on “day one” as previously promised but its only five days until the February 1st date Trump suggested could be the point he puts tariffs on Mexico, Canada and China. So that will be the gorilla in the room this week. In addition, he’s ordered departmental reviews of existing trade practises with an April 1st deadline. So no news on tariffs isn’t necessarily good news. Yesterday Columbia was the latest to feel the wrath of Mr Trump as he ordered an emergency 25% tariff on the country, to be doubled in a week, over the country’s refusal to allow two planes of undocumented migrants returning from the US to land. However, in the early hours of this morning, the US removed the threat after the Colombian leader agreed to grant entry to US military flights deporting migrants. This 12 hour incident feels like a template for how the US will now deal with its foreign policy issues.

Outside of Trump watching, there’s a lot going on this week with rate meetings from the Fed and Bank of Canada (Wednesday), and the ECB (Thursday); inflation data in Europe (Thursday/Friday), US (core PCE Friday), Japan (Tokyo CPI Thursday), and Australia (Wednesday); and Q4 GDP in the US, Germany, France, Italy and Euro Zone (Thursday). If that wasn’t enough, earnings season starts to take off in both the US and Europe with 102 S&P 500 and 53 Stoxx 600 companies reporting with four of the Magnificent 7 (Microsoft, Meta and Tesla on Wednesday, and Apple on Thursday) being the obvious highlight. In the AI world there’s been a lot of chatter in the last few days around Chinese firm DeepSeek’s announcement that it’s produced an open-source AI model that rivals some of the US tech giant’s equivalents for a fraction of the costs and using less sophisticated chips. As this story builds, NVDA is down a whopping 18%, translating in a record market cap loss of $600 billion, driving the S&P 500 down -2%. These are big moves for this time of day. It will be interesting if this story gets momentum and whether the Mag-7 loses some of their luster.

In theory the main event this week would normally be the Fed but most economists expect a relatively quiet meeting with no rate move and limited guidance about future policy decisions. While Chair Powell may not rule out a March cut as he did last January, the broad signals from the meeting should confirm that such a cut is not likely with Powell possibly emphasizing the underlying strength of the economy and signs of stabilisation in the labour market that would require patience in removing further restriction. When asked about Trump’s policies and their impact on inflation expect Powell to play a straight bat and say that the committee wont prejudge policies in advance (even though they clearly have been doing just that).

After the Fed we get Q4 US GDP on Thursday (consensus expects 2.7%), and then the core PCE deflator on Friday, which is expected to rise from 0.1% to 0.2% in December which should keep the YoY rate at 2.8%. The employment cost index (ECI) is also out on Friday and this will be a key release for the Fed as more subdued labour market pressure has given them comfort in recent months.

Over in Europe, the ECB is expected to deliver another 25 bps cut on Thursday taking the policy rate to 2.75% and see the description of the policy stance unchanged relative to December. The ECB will also release its bank lending survey tomorrow and the consumer expectations survey on Friday. Optimism is creeping back into Europe this year and the December 2025 ECB contract has gone up from 1.56% in early December to 2.07% on Friday implying less than four cuts from here. Much of course will depend on the extent that Europe is in the Trump crossfire and so far the market is relieved that nothing specific was announced last week but note that Trump on at least two occasions called out the European Union and said at his virtual Davos address that the EU treats the US “very unfairly” and “very badly”. So it would be wise to brace yourself for more news on this front.

Elsewhere in Europe, this week the focus will also be on flash January CPIs starting with Spain on Thursday. Prints for Germany and France are due Friday, with Eurozone-wide numbers out a week today. DB economists expect headline and core Eurozone HICP to decline by 0.1pp to 2.3% YoY and 2.6% YoY. Their forecasts for Spain, Germany and France are 2.38%, 2.79% and 1.85%, respectively. Don’t forget the GDP prints in Germany, France and the Eurozone on Thursday, as well as Sweden on Wednesday. Other highlights include the Ifo survey in Germany today as well as Sweden’s Riksbank rates decision on Wednesday.

The day-by-day week ahead calendar is at the end as usual with a fuller list of key events, including the main earnings to be realised.

Courtesy of DB, here is a day-by-day calendar of events

Monday January 27

Data: US December Chicago Fed national activity index, new home sales, January Dallas Fed manufacturing activity, China January PMIs, December industrial profits, Japan December PPI services, Germany January Ifo survey, France Q4 total jobseekers

Central banks: ECB’s Lagarde, Holzmann, Kazimir and Vujcic speak

Earnings: AT&T, Nucor, Ryanair

Auctions: US 2-yr Notes ($69bn), 5-yr Notes ($70bn)

Tuesday January 28

Data: US December durable goods orders, January Conference Board consumer confidence index, Dallas Fed services activity, Richmond Fed manufacturing index, Richmond Fed business conditions, November FHFA house price index, France January consumer confidence

Central banks: ECB’s bank lending survey, ECB’s Villeroy speaks, BoJ minutes of the December meeting

Earnings: LVMH, SAP, RTX, Stryker, Boeing, Lockheed Martin, Chubb, Starbucks, Atlas Copco, Royal Caribbean Cruises, General Motors, Sartorius

Auctions: US 2-yr FRN ($30bn), 7-yr Notes ($44bn)

Wednesday January 29

Data: US December advance goods trade balance, wholesale inventories, Japan January consumer confidence index, Italy January consumer confidence index, manufacturing confidence, economic sentiment, Eurozone December M3, Australia December CPI, Sweden December GDP indicator

Central banks: Fed’s decision, BoC decision, Riksbank decision

Data: US Q4 GDP, December pending home sales, initial jobless claims, UK December net consumer credit, M4, Japan January Tokyo CPI, December jobless rate, job-to-applicant ratio, retail sales, industrial production, Germany Q4 GDP, December import price index, France Q4 GDP, December consumer spending, Italy Q4 GDP, December unemployment rate, November industrial sales, Eurozone Q4 GDP, January economic confidence, December unemployment rate

Central banks: ECB’s decision, BoJ’s Himino speaks

Data: US December PCE, personal income, personal spending, January MNI Chicago PMI, Q4 employment cost index, UK January Lloyds Business Barometer, Japan December housing starts, Germany January CPI, unemployment claims rate, December retail sales, France January CPI, December PPI, Italy December PPI, hourly wages, Canada November GDP

Central banks: Fed’s Bowman speaks, ECB’s December consumer expectations survey, survey of professional forecasters

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the Q4 advance GDP report on Thursday and the employment cost index and core PCE inflation reports on Friday. The January FOMC meeting is this week. The post-meeting statement will be released at 2:00 PM ET on Wednesday and will be followed by Chair Powell’s press conference at 2:30 PM ET.

Monday, January 27

10:00 AM New home sales, December (GS +3.0%, consensus +2.4%, last +5.9%)

Tuesday, January 28

08:30 AM Durable goods orders, December preliminary (GS -3.0%, consensus +0.5%, last -1.2%); Durable goods orders ex-transportation, December preliminary (GS +0.3%, consensus +0.4%, last -0.2%); Core capital goods orders, December preliminary (GS +0.2%, consensus +0.3%, last +0.4%); Core capital goods shipments, December preliminary (GS +0.2%, consensus +0.2%, last +0.3%): We estimate that durable goods orders declined 3.0% in the preliminary December report (month-over-month, seasonally adjusted), reflecting a decline in commercial aircraft orders. We forecast 0.2% increases for core capital goods orders and shipments, reflecting mixed global manufacturing data.

09:00 AM FHFA house price index, November (consensus +0.4%, last +0.4%)

09:00 AM S&P Case-Shiller 20-city home price index, November (GS +0.3%, consensus +0.3%, last +0.3%)

10:00 AM Conference Board consumer confidence, January (GS 105.0, consensus 105.6, last 104.7)

10:00 AM Richmond Fed manufacturing index, January (consensus -12, last -10)

Wednesday, January 29

08:30 AM Advance goods trade balance, December (GS -$104.0bn, consensus -$105.0bn, last -$102.9bn)

08:30 AM Wholesale inventories, December preliminary (consensus +0.2%, last -0.2%)

02:00 PM FOMC statement, January 28-29 meeting: As discussed in our FOMC preview, we do not expect the January FOMC meeting to offer much new information. The statement might note that the labor market appears to have stabilized but is unlikely to provide strong guidance about the March meeting or the timeline for further cuts. In the press conference, we will listen for hints about whether the further decline in inflation we expect in coming months could open the door to rate cuts, how strongly the leadership feels that the current level of the funds rate is still “meaningfully restrictive” and not an appropriate stopping point, and how the FOMC intends to navigate uncertainty about potential tariff increases now and their impact on prices later.

Thursday, January 30

08:30 AM GDP, Q4 advance (GS +2.6%, consensus +2.7%, last +3.1%); Personal consumption, Q4 advance (GS +3.1%, consensus +3.2%, last +3.7%); Core PCE inflation, Q4 advance (GS +2.49%, consensus +2.5%, last +2.2%): We estimate that GDP rose 2.6% annualized in the advance reading for Q4, following +3.1% annualized in Q3. Our forecast reflects continued strength in consumption (+3.1%, quarter-over-quarter annualized) and a rebound in residential investment (+4.5% vs. -4.3% in Q3) which more than offset a slowdown in both business fixed investment (+1.5% vs. +4.0% in Q3) and exports growth (+1.2% vs. +9.6% in Q3). We estimate that the core PCE price index increased 2.49% annualized (or 2.80% year-over-year) in Q4.

08:30 AM Initial jobless claims, week ended January 25 (GS 225k, consensus 225k, last 223k); Continuing jobless claims, week ended January 18 (consensus 1,910k, last 1,899k): We estimate that initial claims edged up by 2k to 225k in the week ended January 25, reflecting a continued boost from the wildfires in Los Angeles County and a slight boost from residual seasonality.

10:00 AM Pending home sales, December (GS -3.0%, consensus -0.5%, last +2.2%)

Friday, January 31

08:30 AM Employment cost index, Q4 (GS +0.8%, consensus +0.9%, last +0.8%): We estimate the employment cost index rose by 0.8% in Q4 (quarter-over-quarter, seasonally adjusted), which would lower the year-on-year rate by two tenths to 3.7% (year-over-year, not seasonally adjusted). Our forecast partly reflects the deceleration in the Atlanta Fed’s wage tracker. We also expect a second straight quarter of slower ECI growth among unionized workers—following 1.6% increases on average in 2023Q4-2024Q2 (SA by GS, not annualized)—and slower ECI benefit growth—which reset higher in the first half of the year (0.8% vs. 1.0% on average in H1). On the positive side, we expect slightly firmer compensation growth for incentive-paid occupations after it underperformed broader compensation growth in Q2 and Q3.

08:30 AM Personal income, December (GS +0.4%, consensus +0.4%, last +0.3%); Personal spending, December (GS +0.4%, consensus +0.5%, last +0.4%); Core PCE price index, December (GS +0.16%, consensus +0.2%, last +0.1%); Core PCE price index (YoY), December (GS +2.79%, consensus +2.8%, last +2.8%); PCE price index, December (GS +0.25%, consensus +0.3%, last +0.1%); PCE price index (YoY), December (GS +2.55%, consensus +2.5%, last +2.4%): We estimate personal income and personal spending increased by 0.4%, in December. We estimate that the core PCE price index rose by 0.16% in December, corresponding to a year-over-year rate of 2.79%. Additionally, we expect that the headline PCE price index increased by 0.25% from the prior month, corresponding to a year-over-year rate of 2.55%. Our forecast is consistent with a 0.18% increase in our trimmed core PCE measure.

08:30 AM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will deliver a speech addressing the economic outlook and the outlook for mutual and community banks at the Northern New England CEO Summit in Portsmouth, New Hampshire. Text is expected. On January 9th, Bowman said she supported the FOMC’s decision to lower the fed funds rate in December because “it represented the Committee’s final step in the policy recalibration phase” but noted that she “could have supported taking no action at the December meeting.” Bowman also said that her estimate of the neutral rate was “higher than before the pandemic” and that the FOMC “should be cautious in considering changes to the policy rate as we move toward a more neutral setting.”

09:45 AM Chicago PMI, January (consensus 40.0, last 36.9)

At the start of the year, we are always asked about “Black Swan” events. Given Academy Securities’ Geopolitical Intelligence Group and the number of “hot spots” around the globe, it probably comes up more frequently for us. For the record, I expect more opportunities than risks from Russia/Ukraine and Iran/Israel – see Geopolitical Risks and Opportunities in 2025 if you missed it.

Less discussed are so-called “Gray Rhino” events. Highly probable, highly impactful, yet neglected threats.

The subject of “gray rhinos” came up in our Geopolitical Outlook Webinar, though not in the context of cheap AI. Similarly, we started this month’s Around the World with some “black swan” risks and a deeper dive into the cyber threat from China. Not exactly about cheap AI, but quantum was discussed and with all the cyber issues, we were at least in the vicinity of what has become the subject du jour.

While we only listed DeepSeek as intriguing (rather than outright fearful) in this weekend’s T-Report – Crank Your Amps to 11, that section (if not the entire report) is worth a quick read.

Whether “cheap AI” is a black swan event, a gray rhino event, or pure hype (which is possible), the possibility of it existing is the big question we are all now faced with.

Given privacy concerns (and whatever is going on with TikTok) it is difficult to imagine multinational companies embracing this Chinese technology (if it truly exists), but I suspect (since it is open source) that it will be replicated domestically (maybe even by AI itself) rather quickly.

There have been a lot of questions around current valuations, especially in the AI space. We’ve been part of that crowd. But the questions have been more or less mundane, until today. The typical questions were:

Have the valuations gotten ahead of themselves?

Are the use cases really so compelling to justify the spending and the build-out?

Does the data center build-out have similarities to the fiber build-out? It went from boom, to bust, but eventually worked out.

What we didn’t foresee was the potential for “cheap AI” upsetting the apple cart.

Add In Some Market Structure Fears

In addition to valuation and positioning concerns, we keep coming back to our concerns about the current structure of our markets. These are things that in and of themselves don’t do much, but can accelerate moves when triggered by a catalyst – which is what we might be facing now.

Our usual suspects on the market structure side:

0DTE and weekly options on some of the biggest tech names and big indices could amplify risks.

The leveraged ETFs could amplify risks as well (TQQQ, 3x leveraged QQQ, has $26 billion in market cap, representing over $75 billion of risk). All the leveraged ETFs, with no inflows or outflows, require buying on up days and selling on down days to rebalance ahead of the next day of trading. The leveraged ETFs on single stocks will also likely come into play.

Bitcoin has dropped below $100k, and now has a fairly direct connection to the Nasdaq 100 via MSTR (and MSTX, which is one of those leveraged single stock ETFs).

The concentrated nature of today’s indices is worth highlighting (upwards of 50% of the market value in the indices is concentrated into a small proportion of the total names in the index). It makes “index investing” somewhat the equivalent of “momentum investing” (rather than the traditional concept of “passive”) which could also become problematic if “buy the dip” doesn’t materialize, or worse, we get large outflows.

The sheer dollar amount dedicated to selling vol (from covered calls to open puts) is astounding and may also be problematic. The proverbial, picking up nickels in front of a steam roller.

For all the fear, I think down almost 4% on the Nasdaq 100 warrants some small buying.

There has been a large overnight move, and many are sure to question the validity of the claims being made. But make no mistake: if true, this could change the main narrative around the stock market. It may also be a catalyst to help Chinese stocks, which haven’t had a great couple of months (some serious stimulus would also help, if we ever get that).

As a “side note,” President Trump “suddenly” slapping tariffs on Colombia (then coming to a deal) doesn’t help things either. It can be viewed as a confirmation that there is still a reactive nature to some of his decision making, which is not what the markets are currently betting on, especially when it comes to tariffs. Seriously, the Colombia tariff story would normally be “top of the fold” but will be relegated to the back pages as investors try to figure out what is going on with AI.

I remain skeptical (or maybe dubious is a better word) of some of the “cheap AI” claims, but this moment could be as important to the markets as the unveiling of ChatGPT. Though presumably in the opposite direction, aided and abetted by a market structure conducive to sharp (overdone) declines.

At least DeepSeek has taken my mind off another season where the Bills have solidified their reputation as the best team never to win anything.

Europe Sneers As Lukashenko Boasts Of ‘Dictatorship Of Kindness’ After Securing 7th Term

European leaders aren’t happy that Belarusian President Alexander Lukashenko has once again been reelected on Sunday, which secures him another five years in power, after already having led the former Soviet satellite state for 31-years.

Belarus’s Central Election Commission declared that Lukashenko claimed 86.82 percent of the vote, in an election which only included ‘accepted’ or vetted opposition candidates. They were all seen as sympathetic to to the Belarusian strongman’s continued leadership.

He himself has used some interesting words and phrasing to describe his rule as be beings a seventh term in office. Lukashenko recently spoke of his rule representing a “dictatorship of order, kindness, and justice.”

“We will preserve the most important things — the dictatorship of order, justice, kindness, and respect for people, first of all for laboring people,” Lukashenko said.

But in Europe, news of his reelection was met with scorn and mockery:

German Foreign Minister Annalena Baerbock described the day as “bitter for all those who long for freedom and democracy.”

Polish Foreign Minister Radosław Sikorski expressed mock surprise at the result, sarcastically questioning whether the “only” 87 percent support for Lukashenko would leave space in the nation’s prisons for dissenters.

Czech President Petr Pavel joined the chorus of condemnation, stating, “Lukashenko’s ‘elections’ were a mockery, they were intended to silence dissent.”

The European Union reinforced its stance, with foreign affairs chief Kaja Kallas and Enlargement Commissioner Marta Kos pledging to maintain sanctions against the Belarusian regime while supporting civil society and exiled opposition figures.

But as expected, China’s Xi and Russia’s Putin hailed Lukashenko’s securing another term. “Xi Jinping sent a congratulatory message to Lukashenko on his re-election as President of Belarus,” state news agency Xinhua confirmed Monday.

And Putin said Sunday’s election affirms that he has the “undoubted” backing of the people. “Your convincing victory in the elections clearly testifies to your high political authority and the undoubted support of the population for the state policy Belarus is pursuing,” Putin said.

“You are always a welcome and dear guest on Russian soil. As agreed, I look forward to seeing you soon in Moscow,” he added. Russia and Belarus have long formed a ‘union state’ which involves close economic and defense cooperation.

Belarus’ election commission has declared Alexander Lukashenko the winner of the presidential election for the seventh consecutive time. The vote is widely regarded as neither fair nor free. pic.twitter.com/Vme0wxGfig

Belarus has lately hosted Russian tactical nuclear weapons. These are reportedly housed at Belarusian bases, but with the oversight of Russian officers. The country has come under sanctions for this and for serving as a logistical hub for Russian forces which invaded neighboring Ukraine.

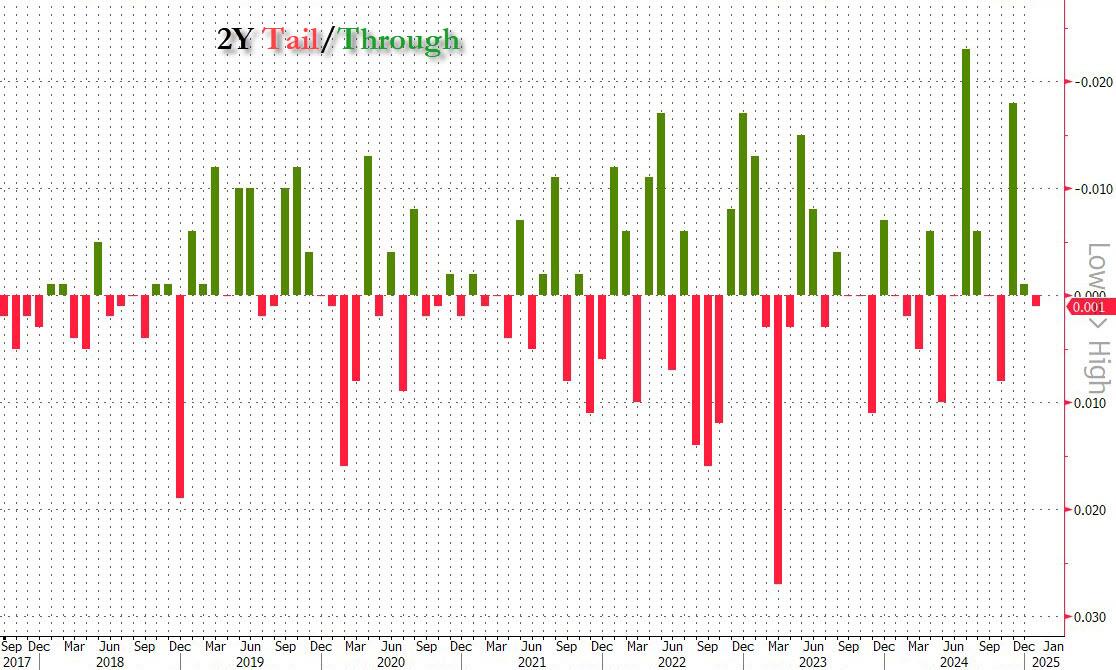

With markets focused on the tech rout, it is easy to forget that ahead of the Wednesday FOMC there is not one but two coupon auctions, the first of which was just concluded.

At 11:30am ET, the US sold $69 billion in 2Year notes, at a high yield of 4.211%. Courtesy of the sharp jump in Treasuries in the past week and especially today, this was 12 bps below last month’s stop of 4.335%, however, it tailed the When Issued 4.210% by 0.1bps, the first tail on 2Y paper since Oct 24.

The bid to cover dipped from 2.73 to 2.66, the lowest since October and just below the six-auction average of 2.68.

The internals were also rather subpar: Indirects, i.e. foreign bidders, tumbled and took down only 65.02%, down sharply from 82.09% and the lowest since October (and below the 70.8% six-auction average). And with Directs awarded 21.27%, the most since October, Dealers were left holding 13.71%, up from 11.26% and the highest since – you guessed it – October.

Overall, this was an unremarkable, somewhat soft auction but hardly anything to worry the market, and the result was that the 10Y barely budged in the secondary market.

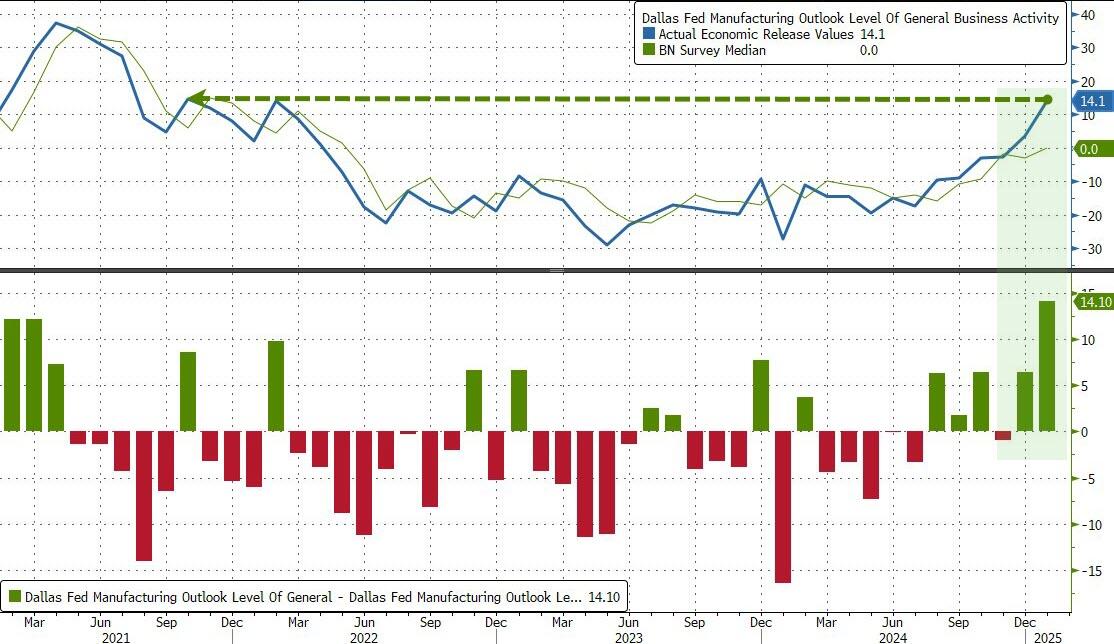

“2025 Is Going To Be Great” – Dallas Fed Manufacturing Survey Soars Near 4-Year-Highs

Three succinct responses sum up the Dallas Fed Manufacturing survey results in January:

“Tariffs, tariffs, tariffs.”

“Inflation is killing us. “

“2025 is going to be great.”

Against expectations of a decline to 0.0, January’s print of 14.1 is above all analysts’ expectations and is the biggest beat since June 2020 (when the economy was recovering from deepest COVID lockdown slump…

Source: Bloomberg

The 14.1 print is the highest since October 2021.

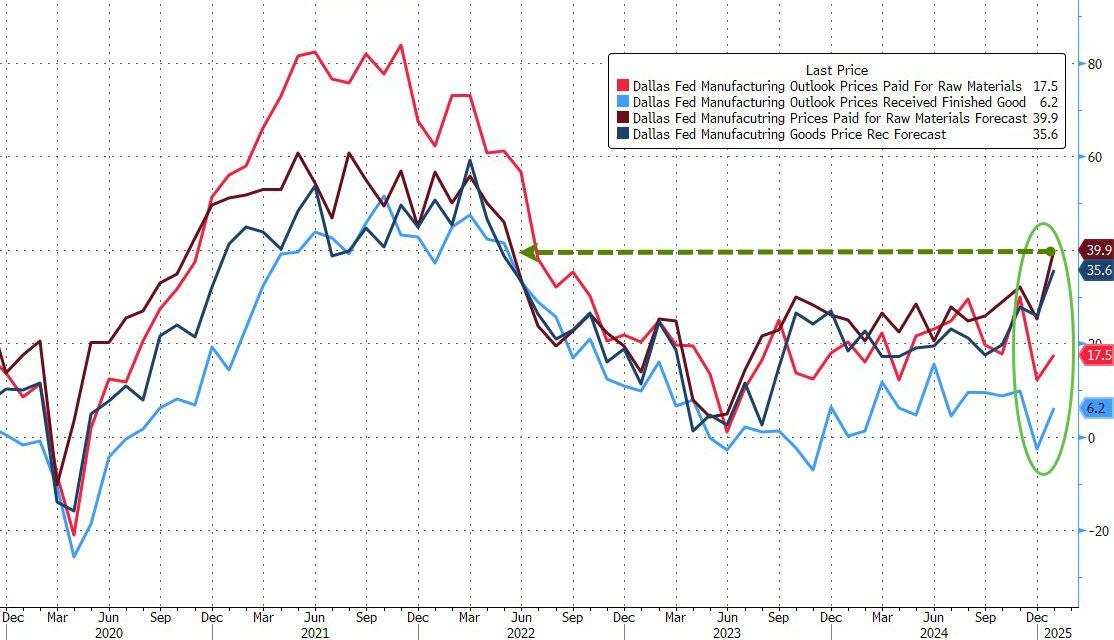

However, while growth and employment expectations are improving, inflation expectations are ripping higher…

Source: Bloomberg

But, overall, the tone of the survey responses is incredibly positive…

“We are starting to see an improvement in the confidence of our customers with the new administration.”

“The start of the year has been extremely positive with a sharp increase in volume of new orders received. With a positive business environment, we expect this trend to continue.“

“There are clear signs of markets starting to inflect up with the exception of automobiles. “

“We are seeing generally good spirits among our customers. We continue to see pushback against price increases, and people are more aware of pricing than they had been in the past, especially during 2021–22.”

“There is a lot of chatter in the market about President Trump’s plans. We believe that they will turn into a robust economy over the next few months.“

“The pall has lifted. Our industry is absolutely giddy with November’s election outcome and the proposed Cabinet members hopefully soon to be confirmed. Personally, I feel our state is more optimistic now that an open border will close, common sense in policymaking will prevail, and free enterprise will be the beneficiary. Our phones are thankfully ringing like they haven’t in quite some time.”

The question is – can Trump follow-through on his promises and fulfill these expectations.

US New Home Sales Rise For Second Straight Year In 2024

Sales of new US homes ended 2024 on a high note in December as customers took advantage of incentives from builders, leading to a second straight year of increased purchases.

For the full year, customers purchased 683,000 homes, up about 2.5% from 2023’s total.

Source: Bloomberg

The annual pace of new single-family home sales accelerated 3.6% to 698,000 last month (better than the 2.4% MoM rise expected), reflecting a sharp advance in the West…

Source: Bloomberg

Median sale prices, meantime, rebounded despite a gradual cooling trend, increasing 2.1% to $427,000. Prices continue to pinch consumers, having risen nearly 30% since the end of 2019.

As Bloomberg reports, the market for new homes has held up better than that for existing ones thanks in part to widespread use by builders of incentives, including mortgage rate “buydowns” in which they make up-front payments on customers’ behalf to lower mortgage costs.

More than 60% of builders report using sales incentives, data from the National Association of Homebuilders show, while 30% say they are cutting prices. Mortgage rates rose to 7% earlier this month for the first time since July.

However, the drop in rates has stabilized here suggesting this rebound is not likely to accelerate…

Source: Bloomberg

Finally, unlike the existing-home market, where the available inventory is only slowly rebuilding from historic pandemic-era lows, builders have plenty of new homes to show customers. The supply on the market rose to 494,000 in December, the most in 17 years.

“They hired—were trying to hire 88,000 new workers to go with you, and we’re in the process of developing a plan to either terminate all of them or maybe we move them to the border,” Trump remarked at a speech in Nevada, while also saying, “On day one, I immediately halted the hiring of any new IRS agents.

“I think we’re going to move them to the border where they are allowed to carry guns. You know, they’re so strong on guns. But these people are allowed to carry guns. So we will probably move them to the border,” he said.

He was repeating a claim made in 2022 by Republicans that some of the IRS agents who would be hired would be able to carry firearms, although the bill did not designate money specifically for a large number of armed IRS employees. At the time, the IRS said it would also obligate about $8.64 billion of the new funding during the 2023 and 2024 fiscal years, and that 7,239 of the new hires during those years will be enforcement staff.

In his administration, President Joe Biden approved plans to direct $80 billion to the IRS under the largely Democrat-passed Inflation Reduction Act of 2022. House Republicans later clawed back billions of dollars from the legislation, most recently in the attempt to avert a government shutdown in December.

The original 87,000 or 88,000 IRS agents figure appears to have come from a U.S. Treasury Department estimate in 2021 to determine the level of hiring of agents to maintain the agency’s efficiency in collecting taxes.

Last year, the IRS said it was going to hire nearly 20,000 new employees and deploy new technology over the next two years as it ramps up an $80 billion investment plan to improve tax enforcement and customer service.

Soon after taking office, Trump signed an executive order to freeze the hiring of federal civilian employees across the government, stating that “no Federal civilian position that is vacant at noon on January 20, 2025, may be filled, and no new position may be created except as otherwise provided for in this memorandum or other applicable law.”

“Except as provided below, this freeze applies to all executive departments and agencies regardless of their sources of operational and programmatic funding,” it adds.

Aside from the hiring freeze, the president suspended Inflation Reduction Act and Infrastructure Investments and Jobs Act funding disbursements in what his office said was “terminating the green new deal,” including pausing funds “supporting programs, projects, or activities that may be implicated by the policy established in Section 2 of the order.”

Section 2 of the executive order mainly focuses on how to direct agency actions including protecting U.S. national and economic security and removing a federal electric vehicle mandate.

Trump also has said he wants to set up an External Revenue Service to collect “tariffs, duties, and other foreign trade-related revenues,” while Trump has proposed imposing a 25 percent tariff on Canada and Mexico over border security.

During his Nevada speech, the president also suggested that he would like to end federal income tax and funding the government solely through tariffs. “How about just no taxes, period? We could do that,” he said.

Right before Trump took office, former IRS Commissioner Danny Werfel stepped down from his position. Trump has named former Rep. Billy Long (R-Mo.) to head the agency, pending Senate confirmation.