Authored by 720Global's Michael Lebowitz via RealInvestmentAdvice.com,

When people use the word catalyst to describe an event that may prick the stock market bubble, they usually discuss something singular, unexpected and potentially shocking. The term “black swan” is frequently invoked to describe such an event. In reality, while such an incident may turn the market around and be the “catalyst” in investors minds, the true catalysts are the major economic and valuation issues that we have discussed in numerous articles.

Most recently, in 22 Troublesome Facts, 720Global outlined factors that are most concerning to us as investors. As a supplement, we elaborate on a few of those topics and build a compelling case for what may be a catalyst for market and economic problems in the months ahead.

Debt Burden

Debt serves as a regulator of economic growth and is the focus of ill-advised fiscal and monetary policy. It is no coincidence that no matter what economic topic we explore, debt is usually a central theme. Illustrated in the chart below is the actual trajectory of total U.S. debt outstanding (black) through March 2017 and a calculated parabolic curve (red). The parabolic curve uses 1951 as a starting point and a quarterly 1.82% compounding factor to create the best statistical fit to the actual debt curve. If we start with the $434 billion of debt outstanding on December 1951 and grow it by 1.82% each quarter thereafter, the result is the gray line. If debt outstanding continues to follow this parabolic curve, it will exceed $60 trillion by the first quarter of 2020, or nine quarters from now.

Data Courtesy: Federal Reserve

Many economists point to the stability of debt service costs as a reason to ignore the parabolic debt chart. Despite rising debt loads, falling interest rates have served as a ballast allowing more debt accumulation at little incremental cost. While that may have worked in the past, near zero interest rates makes it nearly impossible to continue enjoying the benefits of falling interest rates going forward. Importantly, social safety net obligations, demographics, and political dynamics argue that debt growth is likely to continue accelerating as implied by the chart above. Without interest rates falling in step with rising debt burdens, debt service costs will begin to rise appreciably.

The power of compounding, extolled by Albert Einstein as the eighth wonder of the universe, is as damning in its demands as it is merciful in its generosity. Barring negative interest rates, debt service costs will be an insurmountable burden by 2020. However, if the debt trajectory slows as it did in 2008 that too will bring about painful consequences. In other words, all roads lead to trouble.

Debt growth illustrated above has been an important cog in the consumption engine in the United States. Personal consumption accounts for about 70% of Gross Domestic Production (GDP) growth. Neo-Keynesian and Modern Monetary Theory (MMT) economists argue that those who worry about government debt and deficits just don’t understand deficit finance. We worry because we understand the basic math that will limit the U.S. economy’s ability to further burden itself with debt.

Despite policymakers’ lack of regard for this burden, it is important to keep in mind that, as debt accumulates and consumers become less capable of repaying those debts, deleveraging ensues. This means that households will become unable to sustain the lifestyle to which they have become accustomed. Whether debts will be resolved through repayment or default, economic progress will falter.

Retail Sales

The chart below illustrates the components of retail sales in July 2017. Retail sales measures the dollar amount of finished goods sold as opposed to the Personal Consumption Expenditures index (PCE) which measures the price changes of consumer goods and services.

Data Courtesy: U.S. Census Bureau

As shown above, autos, department stores (general merchandise) and restaurants account for 45% of total retail sales. If any of these sectors exhibit weakness then it is challenging for another sector to offset that weakness given its relative size. If all three of these sectors soften at the same time, as is happening now, then it serves as a warning that consumption is likely to decelerate. This has been a precursor to broad economic weakness and even recession in the past. The sections below review each of these three sectors to help you assess the underlying strength or weakness of these important drivers of consumption and the economy.

Autos

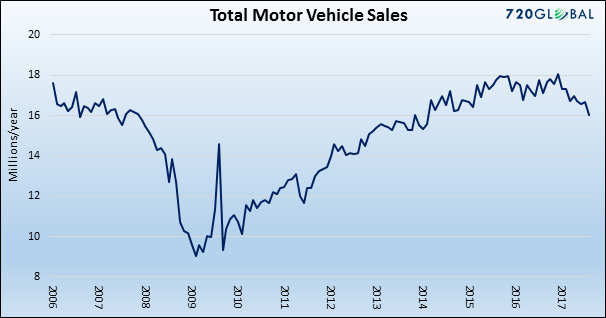

Car and truck sales helped lead the economy out of the recession over the past eight years. The surge in sales to new record levels was not solely due to outright sales but was heavily nourished by extensive use of lease financing. As shown below, auto sales appear to have peaked in late 2016, and used car prices have been in decline since 2014. Both factors raise concerns over the auto sector’s future contribution to economic growth.

Data Courtesy: Bloomberg

Because of the reliance on leasing, cars rolling off leases topped 4 million units last year and are expected to rise by 11% in 2017 and 2018 and top 5 million units by 2019. This is producing a glut of used cars on dealer lots and fueling the decline in used car prices. Projected used car prices, also known as residual value calculations, are a major component of the lease finance equation. As 11-12 million used vehicles hit the market over the next 2½ years, the stage is set for problems in the leased vehicle market and total car sales.

At their peak in February 2016, auto leases accounted for one-third of new car sales and the 6-month moving average remains above 30%. As the leasing option becomes more expensive and the used car supply continues to grow, new auto sales are likely to suffer.

Data Courtesy: Bloomberg

The impact of the used car market on leasing can be seen through the purchase versus lease analysis table shown below. A decline in used car prices (residual values) as is currently forecast dramatically alters lease payments, eliminating leasing as a lower-cost alternative. The bull, base and bear case for used car prices below is based on forecasts from Manheim/Morgan Stanley.

In response to weaker car sales, dealers have slashed prices by the most since the last recession. The auto sector, which represents over 20% of retail sales, is an important economic barometer.

Department Stores

The travails of department stores in recent months have been well-covered. Stores closings and down-sizing stems from weakness in consumer spending but has been rationalized by the “Amazon effect” and preferences for on-line shopping. As recently observed by Evergreen/GaveKal, it’s not the “Amazon Effect”, it’s the “Healthcare Spending Effect” as the average family of four pays $26,000 in healthcare costs. The other problem with the “Amazon” excuse is that, while store traffic has dropped, all department stores have functional, secure websites that consumers can access as easily as Amazon’s web site. According to the Department of Commerce, retail sales for the past 12 months totaled $4.9 trillion of which $403 billion or 8.2% were online. Amazon’s total sales of $150 billion were approximately 3% of total retail sales. Needless to say, there is more to the story than Amazon stealing market share.

On-line retailers are making it hard for department stores to maintain market share but the Amazon narrative sounds more like an attempt to downplay the real problem.

Squeezed by weak income gains, higher healthcare and education costs, and the burdensome load of debt from years past, consumers simply have less money to spend and appear less inclined to spend what they do have on apparel and other department store goods. Further, they have little propensity to borrow to consume more. Since January 2016, department store sales (year over year) declined in every month except two. A continuation of these trends has major implications for retail stalwarts like Macy’s and Nordstrom as well as commercial and retail real estate.

Data Courtesy: Bloomberg

Restaurants

Restaurants face similar issues as retailers with problems extending across all categories of the food service sector except the high-end segment. Restaurant same store sales have experienced 17 consecutive months of year-over-year declines. According to the July 2017 Restaurant Industry Snapshot, Black Box Intelligence reported:

“These are the weakest two-year growth rates in over three years, additional evidence that the industry has not reversed the downward trend that began in early 2015.”

Adjusting for inflation further clarifies the difficulties the sector faces. Wolf Richter at Wolfstreet.com adjusted sales at food service and drinking places for inflation (as shown below) and found that sales, as reported in June 2017, are up only 22% from the post-recession lows and have been stagnant since December 2015.

Not going out to eat is one of the easiest ways to tighten a household budget. The decline in restaurant sales seems to reinforce the increasingly tepid state of consumption.

Consumer Credit Outstanding – Record Highs

Evidence of a challenged consumer drowning in debt continues to build. Credit card debt recently hit a record high at $1.02 trillion, and total consumer credit, which includes auto and education loans and excludes mortgages, is fast approaching $4 trillion.

Data Courtesy: Federal Reserve

Economist Joel Naroff, President of Naroff Economic Advisors, elaborated on the weak consumer: “One of the clearest indicators that households are spending cautiously is the softening of big-ticket purchases… households are maintaining their lifestyles by reducing their savings rate and that is likely restraining spending on discretionary goods.”

Summary

The growth of public and private debt is occurring at a rate faster than wage growth or economic growth. Debt remains the single most important factor in assessing the outlook for the U.S. economy. The business cycle has become incredibly dependent upon the credit cycle which has been hi-jacked by monetary policy. More borrowing leads to better economic growth in the short term, but eventually the music stops, debts must be repaid, and the painful process of deleveraging begins.

Central bank interventions have imprudently disrupted the normal cycle and likely extended it. Unless the Fed can somehow remove human decision-making from the equation, the swings in business cycles remains a permanent feature of the economic system no matter how disfigured from bad monetary policy. What seems to be taking place in the economy today is consumers nearing a point of maximum debt accumulation or consumption exhaustion. Their willingness or ability to take on more credit is slowing and is beginning to become a drag on consumption.

Our assessment of the amount of debt outstanding in conjunction with what we are observing on new and used car lots, at department stores and restaurants offers some indication that we may be near a turning point in the credit cycle. This does not necessarily mean that a recession is imminent but if our concerns are valid, it certainly raises the probability of an economic downturn and quite possibly a catalyst to reverse the direction of asset prices. Given these dynamics and current market valuations, we continue to urge investors to proceed with caution.

via http://ift.tt/2f4Ijhb Tyler Durden