Authored by Lance Roberts via RealInvestmentAdvice.com,

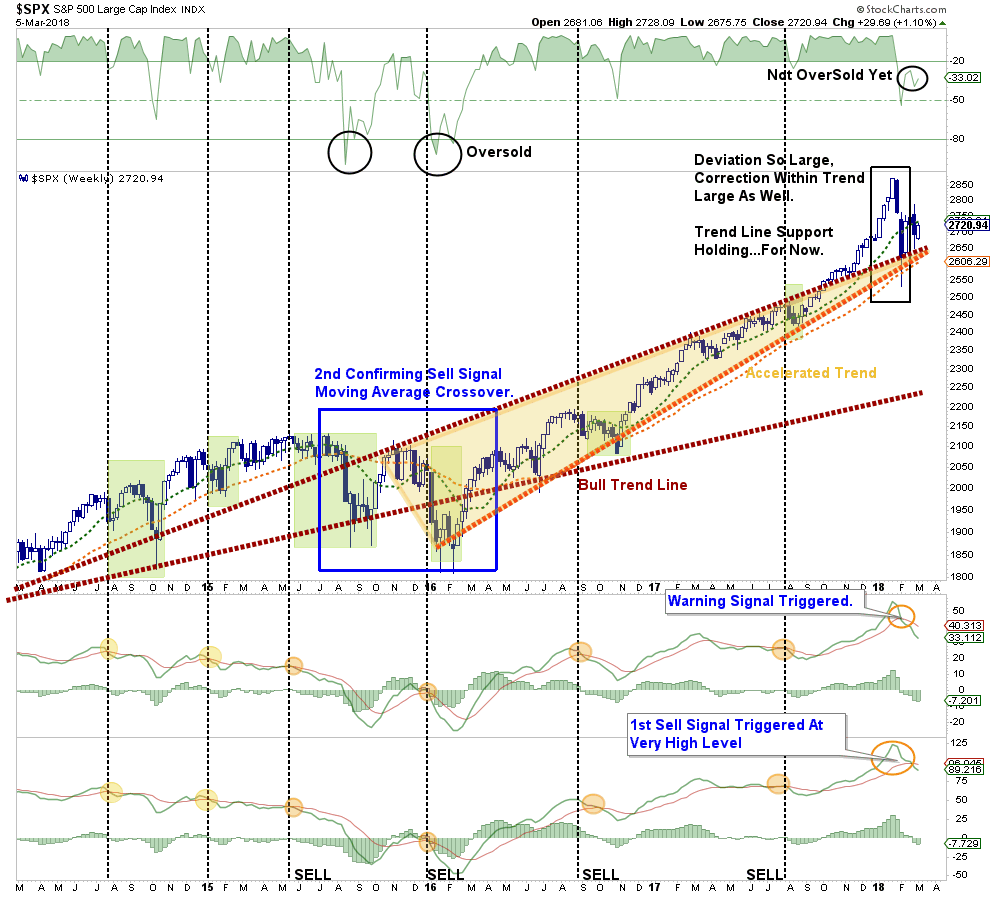

This past weekend, I discussed the recent weekly violation of the market back below its respective 50-dma and the triggering of actions in our underlying portfolios.

‘If the market fails to hold the 50-dma by the end of this week, we will add our hedges back to portfolios, rebalance risk in portfolios and raise cash as needed.

We did exactly that on Friday by reinstating our short-market hedge and raised some cash by reducing some of our long-equity exposure. While previously we had only hedged portfolios, the action this past week to simultaneously reduce some equity exposure was due to both of our primary “sell” signals being tripped as shown below.”

Notice that while the much surged more than 1% on Monday:

- Both “sell signals” remain firmly entrenched at relatively high levels

- The market is not oversold as of yet; and,

- Prices remain below the short-term moving average.

All of this suggests the correction process is not yet complete.

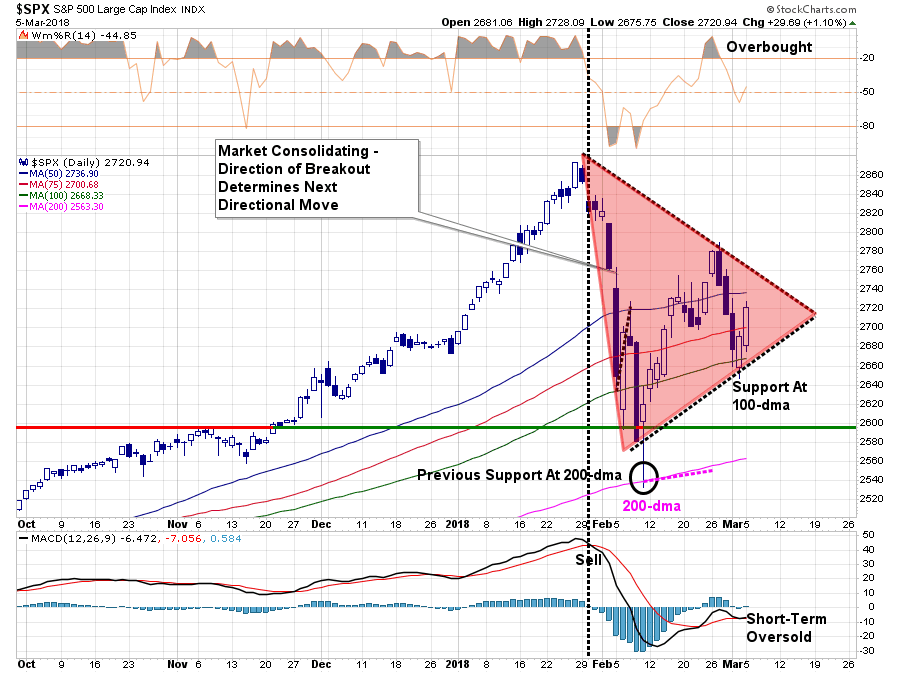

On a short-term trading view, the consolidation process continues with the Monday’s rally also remaining below the 50-dma keeping short-hedges in place for now. This is particularly the case given the confirmed “sell” signal on a weekly basis as noted above.

“Most importantly, the market is currently in the process of building a consolidation pattern as shown by the ‘red’ triangle below. Whichever direction the market breaks out from this consolidation will dictate the direction of the next intermediate-term move.”

“Turning points in the market, if this is one, are extremely difficult to navigate. They are also the juncture where the most investing mistakes are made.”

Over the last several weeks, I have been providing constant prodding to clean up portfolios and reduce risks. I also provided guidelines for that process – click here.

The rally on Monday was not surprising, due to the short-term oversold conditions that existed. However, as discussed in the newsletter:

“It isn’t too late to take some actions next week as I suspect we could very likely see a further bounce on Monday or Tuesday.

Use that bounce wisely.”

For now, it is important to note the “bullish trend” remains solidly intact and, therefore, we must give the “benefit of the doubt” to the bulls. However, with “bearish signals” beginning to mount, the increase in risks certainly justifies become more cautious currently. Goldman Sachs recently noted the potential of a further corrective process:

“As has been discussed in previous updates, the market could also be starting a much bigger/more structurally corrective process, counter to a V wave sequence from the ‘09 lows. If that’s the case, there should be room to continue a lot further over time. At least 23.6% of the rally since ‘09 which is down at 2,352.

Bottom line, it’s worth considering the possibility of continuing further than 2,467-2,449. Doing so might imply that this is not an ABC but rather a 1-2-3 of 5 waves down, in a larger degree ABC count that could take months to fully manifest. While it is still far too early to make this call, the important thing to note is that the 2,467-2,449 area will likely be trend-defining.”

Searching For The Greater Fool

ValueWalk recently published the following note:

Klarman writes when purchasing stocks:

“You may find a buyer at a higher price – a greater fool – or you may not, in which case you yourself are the greater fool.”

Here’s an excerpt from Klarman’s book, Margin of Safety, in which he discusses the importance of doing your homework and avoiding speculation when it comes to investing:

“There is the old story about the market craze in sardine trading when the sardines disappeared from their traditional waters in Monterey, California. The commodity traders bid them up and the price of a can of sardines soared. One day a buyer decided to treat himself to an expensive meal and actually opened a can and started eating. He immediately became ill and told the seller the sardines were no good. The seller said, “You don’t understand. These are not eating sardines, they are trading sardines.”‘

Like sardine traders, many financial-market participants are attracted to speculation, never bothering to taste the sardines they are trading. Speculation offers the prospect of instant gratification; why get rich slowly if you can get rich quickly?

Moreover, speculation involves going along with the crowd, not against it. There is comfort in consensus; those in the majority gain confidence from their very number. Today many financial-market participants, knowingly or unknowingly, have become speculators. They may not even realize that they are playing a ‘greater-fool game,’ buying overvalued securities and expecting—hoping—to find someone, a greater fool, to buy from them at a still higher price.

There is great allure to treating stocks as pieces of paper that you trade. Viewing stocks this way requires neither rigorous analysis nor knowledge of the underlying businesses. Moreover, trading in and of itself can be exciting and, as long as the market is rising, lucrative. But essentially it is speculating, not investing.

You may find a buyer at a higher price—a greater fool—or you may not, in which case you yourself are the greater fool.”

I really enjoyed this analysis as it epitomizes the problem facing investors today. Investors are currently faced with a “binary” choice given an overvalued, overly bullish and extended market.

- Stay out of the market and miss out on short-term gains but remain protected against a future “mean reverting event;” or,

- Chase the market for short-term capital appreciation but potentially suffer severe capital destruction in the future.

It is an impossible choice.

Let me explain.

In an overly valued, extended and bullish market, the logical choice would be to go to cash (sell high) and wait for a “mean reverting” event to redeploy capital (buy low) at much better valuations. The chart below shows, even using a simplistic process for doing so, the long-term returns have far outpaced those of “buy and hold” investors.

Yes, as notated, investors would have “missed out” of the market for nearly 3-years in 2000, almost 2-years in 2008, and 6-months in 2016. Yet, using even a simplistic method of risk-management, in this case a 12-month moving average, the net result greatly outweighed the mainstream “buy and hold” approach.

But it’s impossible for most individuals to actually do.

The reality is that most investors “sold” the lows in 2002, and 2008, and waited far too long to get back “in.” As has always been the case, investors tend to do the exact opposite of what they should.

“Buy high and sell low.”

As study after study shows, investors are driven by their emotions of “greed” and “fear.” Those emotional biases are fed by the mainstream media who consistently berate individuals for “missing out” and “not beating the market.” Yet, scream “panic” at the first sign of trouble.

This drives investors to consistently do the wrong things at the wrong time. Repeatedly.

Currently, investors are riding a nine-year-old bull market with an inherent belief they will be smart enough to get out before the next bear market begins. This is the very essence of the “greater fool theory.”

Unfortunately, most individuals will once again be “eating their sardines.” As discussed previously:

“While the answer is ‘yes,’ as there is always a buyer for every seller, the question is always ‘at what price?’

At some point, that reversion process will take hold. It is then investor ‘psychology’ will collide with ‘margin debt’ and ETF liquidity.

When the ‘robot trading algorithms’ begin to reverse, it will not be a slow and methodical process but rather a stampede with little regard to price, valuation or fundamental measures as the exit will become very narrow.

Importantly, as prices decline it will trigger margin calls which will induce more indiscriminate selling. The forced redemption cycle will cause catastrophic spreads between the current bid and ask pricing for ETF’s. As investors are forced to dump positions to meet margin calls, the lack of buyers will form a vacuum causing rapid price declines which leave investors helpless on the sidelines watching years of capital appreciation vanish in moments.“

Currently, the markets remain above their 12-month moving average which keeps portfolios allocated on the long-side.

However, such will not always be the case.

Trying to beat a “benchmark index” is a fool’s errand and should be left to the “fools.”

1) The index contains no cash

2) It has no life expectancy requirements – but you do.

3) It does not have to compensate for distributions to meet living requirements – but you do.

4) It requires you to take on excess risk (potential for loss) in order to obtain equivalent performance – this is fine on the way up, but not on the way down.

5) It has no taxes, costs or other expenses associated with it – but you do.

6) It has the ability to substitute at no penalty – but you don’t.

7) It benefits from share buybacks – but you don’t.

In order to win the long-term investing game your portfolio should be built around the things that matter most to you, and your money.

– Capital preservation

– A rate of return sufficient to keep pace with the rate of inflation.

– Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

– Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

– You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

– Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

Investing is not a competition and, as history shows, there are horrid consequences for treating it as such. So, do yourself a favor and turn off the media. Focus instead on matching your portfolio to your own personal goals, objectives, and time frames. In the long run, you may not beat the index from one year to the next, but you are much more likely to achieve your investment goals which is why you invest in the first place.

Unfortunately, the rules are REALLY hard to follow. If they were easy, then everyone would be wealthy from investing. They aren’t because investing without a discipline and a strategy tends to have horrid consequences.

Personally, I hate the “taste of sardines.”

via Zero Hedge http://ift.tt/2oPvMTy Tyler Durden