Authored by Jeffrey Snider via Alhambra Investment Partners,

Big Things: The Hoard Gets Bigger

I’ve observed a lot that’s purely absurd the last eleven years, trying hard to write up as much of it as I can. It’s worth the effort in terms of education but also to reveal what’s really going on. The catalog is too long to republish here in its entirety.

One of the most ridiculous anecdotes, however, was pieced together in March 2016. The dollar world was a smoldering wreck, and because of that global bond yields were still falling. Liquidity hedging was prevalent as anyone might honestly expect.

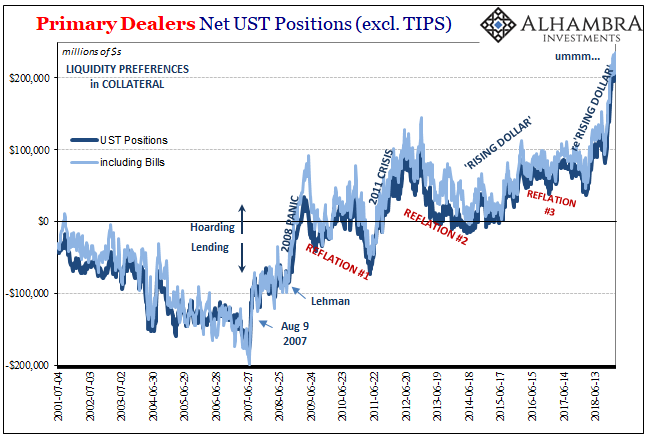

As a consequence, US primary dealers were hoarding UST’s coupons and bills. Their reported (net) holdings of these most prized instruments so very clearly rise and fall with each deflation/reflation cycle.

But there is no such thing according to the Fed narrative. There cannot be because four QE’s caused so much “money” to be “printed” something like that would be unthinkable – if it was ever the real thing it would reveal the whole corrupt nature of moneyless monetary policy. It didn’t matter the global downturn and how the US economy was pushed right up to the edge of recession, there was no liquidity problem in dollars they all said.

How, then, to explain what dealers were doing with all those UST’s?

As the world’s biggest bond dealers — including banks such as Bank of America Corp., Goldman Sachs Group Inc. and JPMorgan — struggled to get rid of the burgeoning pile of debt, the premium for the newest, easiest-to-trade Treasuries soared to the highest since 2011. The firms’ efforts to hedge all the Treasuries collecting on their balance sheets also roiled the futures market and a crucial corner of the financial system where traders lend and borrow securities overnight. [emphasis added]

The first business of any dealer is to warehouse securities; to purchase them in the primary market and then sell them off over time to brokerage customers. It is these dealers who buy at the federal government’s auctions in order to then distribute the bonds, bills, and notes out to the investing public.

That, of course, means they have to hold those bonds on balance sheet while the process plays out. It seems plausible that if the public doesn’t want to buy what’s being warehoused, including US government paper, the dealers will reluctantly have to hang on to, and finance, that paper.

But this was March 2016. The idea that dealers were in any way struggling to place UST’s was so very blatant nonsense. At the time I noted in reply:

The story has problems on both ends; to start with, why are dealers supposedly buying up UST inventory that they will only get stuck with? That has never been a money dealing function, as if there is ever great imbalance it is for dealers to manage but largely get out of the way and let price action take care of it. In other words, primary dealers would likely have been only buying enough to maintain orderly markets, not so much that they suddenly became bloated warehouse units of unhedged risk. It strains credibility already.

The second part is even worse. These banks are supposed to have had trouble selling UST’s during a period when everyone was buying them?

If anything, demand for treasuries was overwhelming. Dealers holding such a large portion back meant only one thing – a conscious choice about their own books. But QE and Janet Yellen’s “resilient” financial system.

That’s why dealer holdings follow the rhythm of the Euro$ squeezes. When it gets bad, they purposefully hold on to what’s in inventory because of perceived liquidity risks arising from all the other things dealers do (repo and FX just the start). After Bear, AIG, Lehman, et al, nobody’s going to be so unprepared for when BONY Mellon comes calling for collateral.

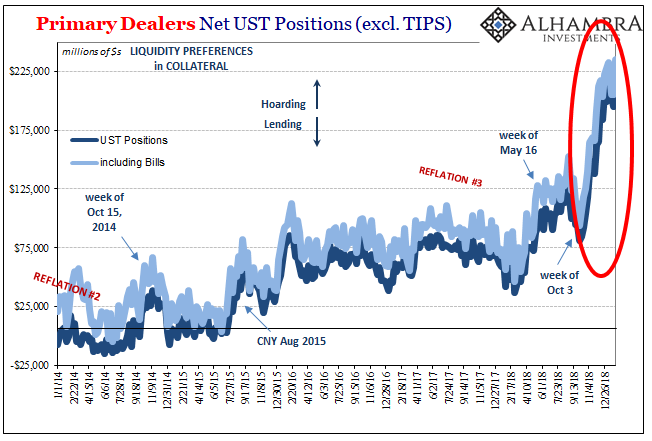

As noted during last December’s chaos, this dealer hoarding took on absolutely immense proportions. It’s like nothing we’d seen before, even during 2008 (admittedly, dealers were still learning about the downside of illiquidity and prudent matching leading up to that big week in September). As of last week, Jan 30, reported holdings (therefore hoarding) surpassed the record set the week of Christmas (when every market was a huge mess, except UST’s).

Are primary dealers having trouble selling their accumulated stock again? Of course not. Global bond markets are on fire, even more so than stocks. There is huge demand for pristine collateral types.

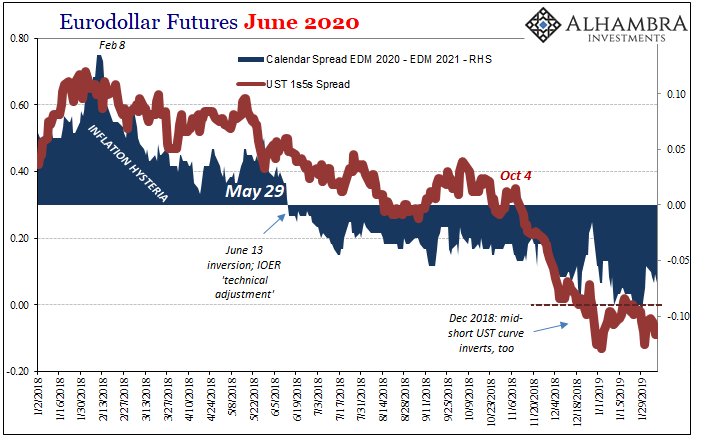

Not only that, both the eurodollar futures and UST curves exhibit absolutely brutal liquidity hedging going on. While everyone is fixated on UST 2s10s, the space between the 12-month bill and 5-year note has gone bananas – during the exact same timeframe dealer hoarding skyrocketed.

Sorry Bill Dudley, massive liquidity risks everywhere – and therefore an overwhelming number of potential buyers for what dealers are holding but won’t sell. Record hoarding. Even more hoarding to start February 2019.

Falling LIBOR and bond yields, confused and dazed central bankers, greater distortions to the major curves; as I wrote yesterday:

What does it say about the state of the world when those hugely contradictory expectations are being fulfilled? Rate cuts, official rate cuts, may be closer than you think.

There’s a lot of big stuff going on right now.

Or, sure, maybe there really is no one to buy all these UST’s piling up on exposed dealer balance sheets. On a totally unrelated note, I’m sure, interesting time for Bill Gross’ retirement announcement.

via ZeroHedge News http://bit.ly/2I2yUrb Tyler Durden