Authored by Alasdair Macleod via GoldMoney.com,

The major economies have slowed suddenly in the last two or three months, prompting a change of tack in the monetary policies of central banks. The same old tired, failing inflationist responses are being lined up, despite the evidence that monetary easing has never stopped a credit crisis developing. This article demonstrates why monetary policy is doomed by citing three reasons. There is the empirical evidence of money and credit continuing to grow regardless of interest rate changes, the evidence of Gibson’s paradox, and widespread ignorance in macroeconomic circles of the role of time preference.

The current state of play

The Fed’s rowing back on monetary tightening has rescued the world economy from the next credit crisis, or at least that’s the bullish message being churned out by brokers’ analysts and the media hacks that feed off them. It brings to mind Dr Johnson’s cynical observation about an acquaintance’s second marriage being the triumph of hope over experience.

The inflationists insist that more inflation is the cure for all economic ills. In this case, mounting concerns over the ending of the growth phase of the credit cycle is the recurring ill being addressed, so repetitive an event that instead of Dr Johnson’s aphorism, it calls for one that encompasses the madness of central bankers repeating the same policies every credit crisis. But if you are given just one tool to solve a nation’s economic problems, in this case the authority to regulate the nation’s money, you probably end up believing in its efficacy to the exclusion of all else.

That is the position in which Jay Powell, the Fed’s chairman finds himself. Quite reasonably, he took the view that the Fed’s marriage with the markets was bound to go through another rough patch, and the Fed should use the good times to prepare itself. Unfortunately, the rough patch materialised before he could organise the Fed’s balance sheet for its next launch of monetary bazookas.

The whole monetary planning process has had to go on hold, and a mini-salvation of the economy engineered. To be fair, this time it is Washington’s tariff fight with China and its alienation of the EU through trade protectionism that has interrupted the Fed’s plans rather than the Fed’s mistakes alone. But by taking early action the hope is the Fed can keep confidence bubbling along for another year or two. It might work, but it will need a far more constructive approach towards global trade from America’s political-security complex to have a sporting chance of succeeding.

However, buying off a crisis by more money-printing does not represent a solution. It is commonly agreed that the problem screaming at us is too much debt. Yet, the inflationists fail to connect growing debt with monetary expansion. The Fed’s objective is to encourage the commercial banks to keep expanding credit. What else is this other than creating more debt?

Powell is surely aware of this and must feel trapped. However, what his feelings are is immaterial; his contractual obligation is to keep the show on the road, targeting self-serving definitions of employment and price inflation. He will be keeping his fingers crossed that some miracle will turn up.

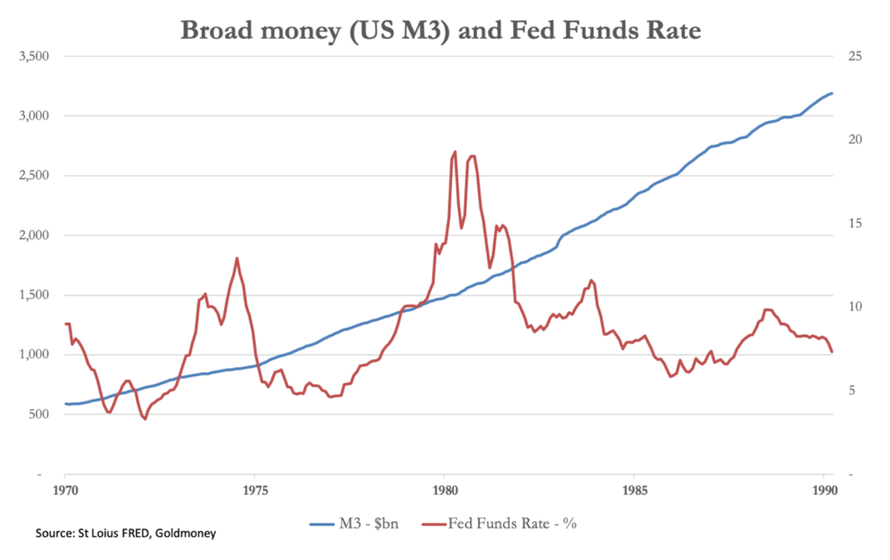

It is too early to forecast whether the Fed will manage to defer for just a little longer the certainty that the monetary imbalances in the economy will implode into a singularity, whereby debtors and creditors resolve their differences into a big fat zero. That is not the purpose of this article, which is to point out why the underlying assumption, that interest rates are the cost of money which can be managed with beneficial results, is plainly wrong. If demand for money and credit can be regulated by interest rates, then there should be a precisely negative correlation between official interest rates and the quantity of money and credit outstanding. It is clear from the following chart that this is not the case.

This chart covers the most violent moves in Fed-directed interest rates ever, following the 1970s price inflation crisis. Despite the Fed increasing the FFR from 4.6% in January 1977 to 19.3% in April 1980, M3 (broad money and bank credit) continued to increase with little variation in its pace. Falls in the FFR designed to stimulate the economy and prevent recession were equally ineffective as M3 continued on its straight-line path after 1980 without significant variation, and it is still doing so today. There is no correlation between changes in interest rates, the quantity of money, and therefore the inflationary consequences.

Gibson’s paradox disproves the efficacy of monetary policy

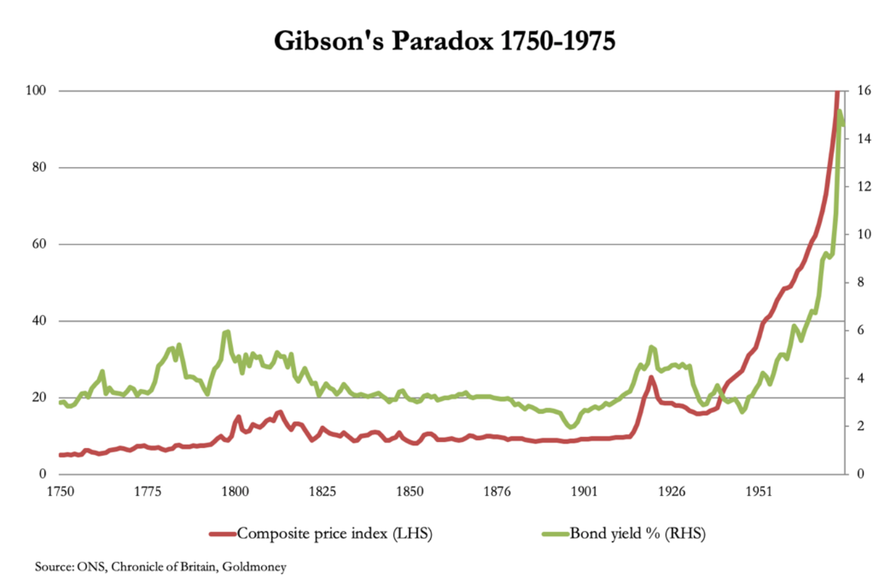

From the chart above, it is clear that the central tenet of monetary policy, that the quantity of money can be regulated by managing interest rates, is not borne out by the results, and therefore the role of interest rates is not to regulate demand for credit as commonly supposed. This is confirmed by Gibson’s paradox, which demonstrated that a long-run positive correlation existed between wholesale borrowing rates and wholesale prices, the exact opposite of that assumed by modern economists. This is shown in our second chart, covering over two centuries of British statistics.

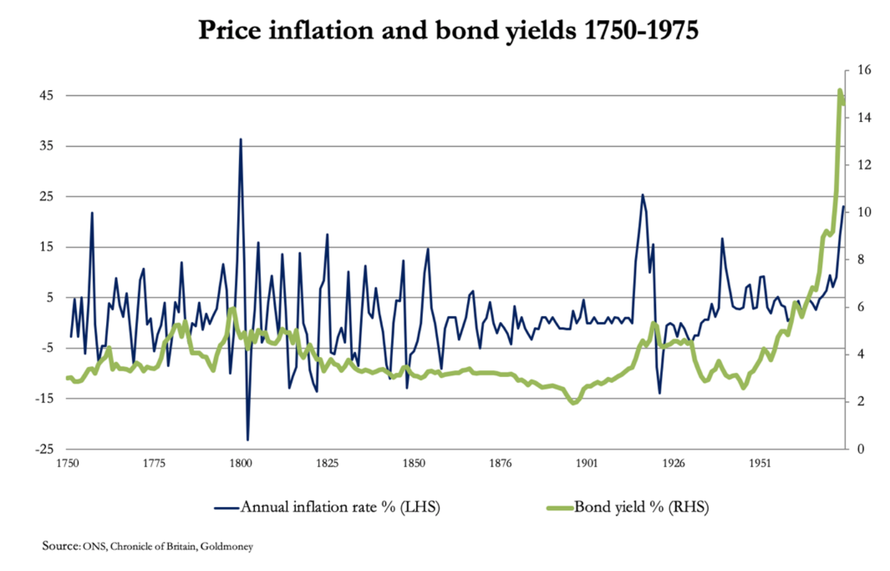

Economists dismissed the contradiction of Gibson’s paradox because it conflicted with their set view, that interest rates regulate demand for money and therefore prices[i]. Instead, it is ignored, but the evidence is clear. Historically, interest rates have tracked the general price level, not the annual inflation rate. As a means of managing monetary policy, interest rates and therefore borrowing costs are ineffective, as confirmed in our third chart below.

The only apparent correlation between borrowing costs and price inflation occurred in the 1970s, when price inflation took off, and bond and money markets woke up to the collapsing purchasing power of the currency.

The explanation for Gibson’s paradox, which embarrassingly eluded all the great economists who tackled it, is simple. It stands to reason that if the general price level changes, in aggregate businessmen in their calculations will take that into account when it comes to assessing the level of interest they are prepared to pay and still make a profit. If a businessman expects higher prices in the market, he will expect a higher rate of return and therefore be prepared to pay a higher rate of interest. And if prices are lower, he can only afford to pay a correspondingly lower rate. This holds true when capital in the form of savings is limited by the preparedness of people to save, and businesses have to compete for it.

Today, Gibson’s paradox does not appear to apply, partly because capital is no longer scarce (thanks due to central banks) and partly because the abandonment of the Bretton Woods agreement has led to indices of the general price level rising continually. To these factors must now be added wilful misrepresentation of price inflation in official statistics, a deceit that will almost certainly end up destabilising attempts at economic management even further when discovered.

These points notwithstanding, the belief that interest rates are a price which regulates demand for money is disproved. The mistake is to ignore the human dimension of time preference and assume there is no reason for a difference in intertemporal values, the value of something today compared with later. To understand why the degradation of value over time becomes a necessary element of compensation in lending contracts, we must examine in more detail what interest rates actually represent. Only then can we fully understand why they do not correlate with changes in the general level of prices and the growth of credit, which makes up the bulk of M3 in the first chart.

The role of time preference

In all lending agreements, interest represents a number of factors. There is an element representing a risk premium, depending on the credit standing of the borrower, the entrepreneurial risk, and the purpose for which the loan is made. There is also a generally agreed underlying rate which in a market economy reflects pure time preference, referred to by Austrian economists as the originary rate. Time preference is the difference in the value placed on an action intended to satisfy sooner compared with the value placed on the same satisfaction achieved at a later date.

Mainstream macroeconomists deny the existence of time preference, claiming that interest represents the rental of money. If that is all interest represents, then it can be reduced for the benefit of producers and consumers, and beyond savers losing out, no other consequences need occur. Furthermore, the denial of a subjective human element is always necessary for a mathematical approach to prices to be credible.

Despite it being unfashionable, we must briefly summarise pure time preference theory. Time preference is always present because time for any economic actor is finite and therefore has value. The more immediately that an action results in a satisfaction the more valuable that satisfaction compared with an action which leads to the satisfaction being delayed. It has been referred to by the old adage that a bird in the hand is worth two in the bush.

The key to understanding the importance of time preference is to realise it is a human characteristic, and not something that emanates from the properties of individual goods and services. Intertemporal price differences can vary considerably between products, mainly due to their individual supply and demand characteristics. Because pure time preference is an underlying determinant of human action, the general rule is that the greater the difference in time between deciding on a course of action and the delivery of the satisfaction, the less the present value of that future action. From our individual experiences, we all know this to be true.

Time preference is therefore the general intertemporal value placed on goods and services by consumers. It is not under the control of the producer, or for that matter a central bank. It is the consumer, the end-buyer of everything, that confirms the level of discount on future values, because consumers are humans acting with their human preferences.

In order to obtain monetary capital for any reason, the owners have to be persuaded to temporarily part with it for a compensation related to their general time preference. This is because they are being asked to defer their consumption, which is represented by the money borrowed. For convenience and by convention, compensation for the loss of the availability of money for immediate spending is expressed as an annualised interest rate. In this way, the variations of time preference for the full range of opinions and judgements of consumers over the whole gamut of goods and services finds expression in a basic, or originary rate of interest on money.

This fundamental human ranking of values matters to businessmen, because the longer it takes to produce a consumer good, the less the distant value of that good can be expected to be, expressed in today’s money. In assembling their capital resources, they take this time-related expense into account.

Therefore, in order to reduce the loss in value due to time preference, businessmen will always prefer the most efficient route available to final production. If, as is always the case today, a central bank commands through interest rate policy that the discount on future values is reduced, businessmen are no longer disciplined to prefer the most efficient route to production. The intertemporal discount is still there, but the suppression of originary interest rates by a central bank imposing a lower rate on the market creates an opportunity unrelated to the singular objective of providing consumer satisfaction.

This is why suppressing interest rates leads to malinvestments, exposed when interest rates subsequently rise. This is what the current hiatus in the stalling US economy is really about.

It is clear, irrespective of monetary policy, that the originary interest rate is set by individuals in their roles as economic actors. That is not to say that in their decisions they are uninfluenced by official interest rates, but there is a tight limit to that influence. Instead, individuals will seize the opportunities presented by the difference between their own originary rate of interest and that set by the monetary authorities. An obvious example is residential property, where supressed interest rates persuade individuals to borrow cheap mortgage money to buy houses, purely because the interest payable is less than that suggested by personal time preferences. The same is true of financing the purchases of purely financial assets, and it is also a key reason behind the expansion of consumer credit.

The suppression of interest rates to levels below those collectively determined by consumers in their time preferences is the fundamental source of inflations, booms, bubbles, and subsequent busts.

Essentially, a central bank’s interest rate policies distort markets, but they cannot significantly change that originary rate of interest. That is in the lap of time preference, set semi-consciously by consumers. The relationships between lenders and borrowers of monetary capital are further distorted by tax, because today’s governments commonly regard interest income as quasi-usurious and therefore a target for reducing the implied inequality of some individuals possessing significant levels of savings compared with others.

Taxation on interest interferes with time preference, which was demonstrated through its absence on savings in the two most successful post-war economies, those of Japan and Germany. In Japan, tax-free post office savings accounts grew as a means of earning interest without being taxed, and in Germany the Federal Central Tax Office didn’t much bother collecting the withholding tax on bond interest at least until the 1980s, because to do so simply chased money out of Germany into savings accounts in Luxembourg and Switzerland beyond the reach of the tax office. Consumers in both Japan and Germany still retain a general savings habit that contributes to a relatively stable level of time preference, characteristics which have been central to their economic success.

The examples of Germany and Japan contrast with other socialised economies where savings have been discouraged through tax discrimination. The replacement of savings in the US and UK by bank credit and central bank base money has been a sad failure in comparison.

So far, we have only addressed time preference on the assumption there is no change in money’s purchasing power. If, as is always true today, money’s purchasing power is continually declining, then to the extent the general public is aware of it, that widens the gulf between official interest rates and time preference even further. And if savers realise the true extent that the currency of their savings is losing purchasing power instead of believing self-serving government statistics, they could be forgiven for discounting future satisfactions even more heavily.

This explains why, when the authorities respond to rising price inflation by raising interest rates, all they are doing is belatedly attempting to narrow an already widening gap between their version of where interest rates should be and the market’s rising originary rate. The expansion of bank credit does not slow, because the gap is still there and increasing as well.

We saw this demonstrated in the 1970s, when rising interest rates failed to slow demand for credit, which continued to rise regardless. The rate of price inflation was also rising, persuading borrowers that the purchasing power of money was falling at an accelerating rate, thereby increasing their time preferences faster than compensated for by official interest rates.

That ended in the early 1980s, when expectations of escalating prices were finally broken by 20%+ prime rates. In the 1980s demand for credit continued to increase, despite falling interest rates, because of financial and banking liberalisation which more than offset the failures associated with malinvestments. Broad money continued to grow with minimal variation as if nothing had happened, as it still does today.

The European Central Bank should pay attention to its failures as well. Its introduction of negative deposit rates, in defiance of all-time preference, has failed to stimulate production and consumption beyond government spending. Admittedly, negative rates have not generally been passed on to businesses and borrowing consumers, often for structural reasons. Instead, the ECB’s negative interest rates have benefited profligate Eurozone governments, allowing them to tax savers deposits instead of paying for time preference. It should be clear that negative interest rates cannot be justified so long as humanity values a satisfaction today more than the same satisfaction at a future date.

The implications for today’s economy

While the evidence is that interest rate policies fail to regulate the pace of monetary inflation, the seeds of economic crisis were sown by earlier interest rate suppression. Because suppression of interest rates below the originary rate set by the public’s time preference always leads to malinvestments, subsequent increases in interest rates always lead to those malinvestments being exposed. The response by businesses is always the same: mothball or dispense with the malinvestments.

Banks sense the mood-change in their customers and the associated increase in lending risk. They restrict their credit lines and working capital facilities to those they deem vulnerable, usually the medium and smaller enterprises that make up Pareto’s 80% of the economy[ii]. The economy then runs into a brick wall with a rapidity that surprises everyone. Labour shortages disappear, followed by employees being laid off. An unstoppable process of correcting earlier malinvestments gathers pace.

This is the point in the credit cycle at which we appear to have arrived today. If only central bankers had taken the long-run evidence of their own statistics seriously, if they had only paid attention to the message from Gibson’s paradox, and if they had noted the madness of doing the same thing time after time despite it not working, we would have been blessed with a far greater degree of economic stability, instead of the increasing certainty of another financial and systemic crisis.

As for the hope that cutting interest rates will somehow lead to an expansion of bank credit, don’t hold your breath. The other lesson we should all learn is money supply continues to increase, if not in the form of bank credit then in the form of central bank base money. This is because the alternative of widespread bankruptcies is always unpalatable to a socialising state.

via ZeroHedge News http://bit.ly/2SIGNqX Tyler Durden