Authored by Kevin Muir via The Macro Tourist blog,

Whenever I hear words like “market makers say this is the largest skew they can remember”, my ears perk up. Even if they are incorrect, even if the distortion has been higher in the past – it’s clear something is not quite as it should be. As Han would say, “I have a bad feeling about this…“

What am I talking about? Options on eurodollar futures. No, not the euro currency, but the 3-month US dollar denominated interest rate futures contract. It’s not quite the same as Fed Funds as there is some credit risk (it’s the rate at which banks lend US dollars to one another offshore), yet it tracks closely enough that for all intents and purposes, it’s betting on future Fed policy.

The market for Eurodollar futures is big. And liquid. The open interest is over $1.65 trillion. Yup. Trillion with capital “T”. Most contract months are half a tick wide with more often than not, a 100 million on the bid or offer. The Eurodollar futures contract is the ultimate institutional market and all too often gets completely ignored by the financial news media.

And when it is mentioned, it’s rarely an article about the skew in the option market. But it’s an important story, so I will take some time to explain (or at least try) the intricacies in the eurodollar option market and then speculate on what they might mean.

Elvis-Presley smirk

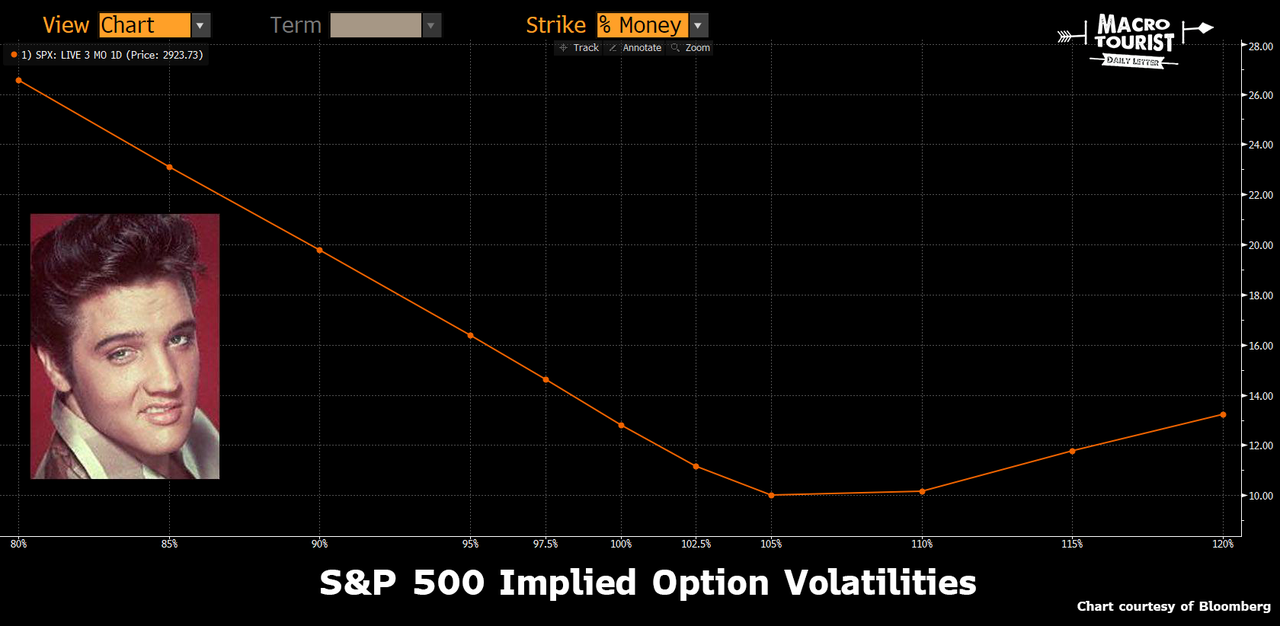

Most everyone understands the Elvis-Presley half-smile in the equity index option market.

What’s that expression? Stocks go up the escalator but come down the elevator. This tendency for stocks to be more volatile on the downside creates a situation where option players price out-of-the-money puts with a much higher implied volatility than the rest of the curve.

But what about eurodollar futures? What sort of skew should they trade with? If we think back to the past few decades, most of the surprise large moves were from the Fed doing an emergency rate cut, not a raise. Eurodollar contracts are priced off an index which is 100 minus the LIBOR rate. This means that rate cuts result in the eurodollar futures contract rising in price.

We would therefore expect the skew on the eurodollar futures option contract to be tilted in the opposite manner to the equity index market. Market participants should pay higher implied volatilities for strikes that are out of the money on the upside.

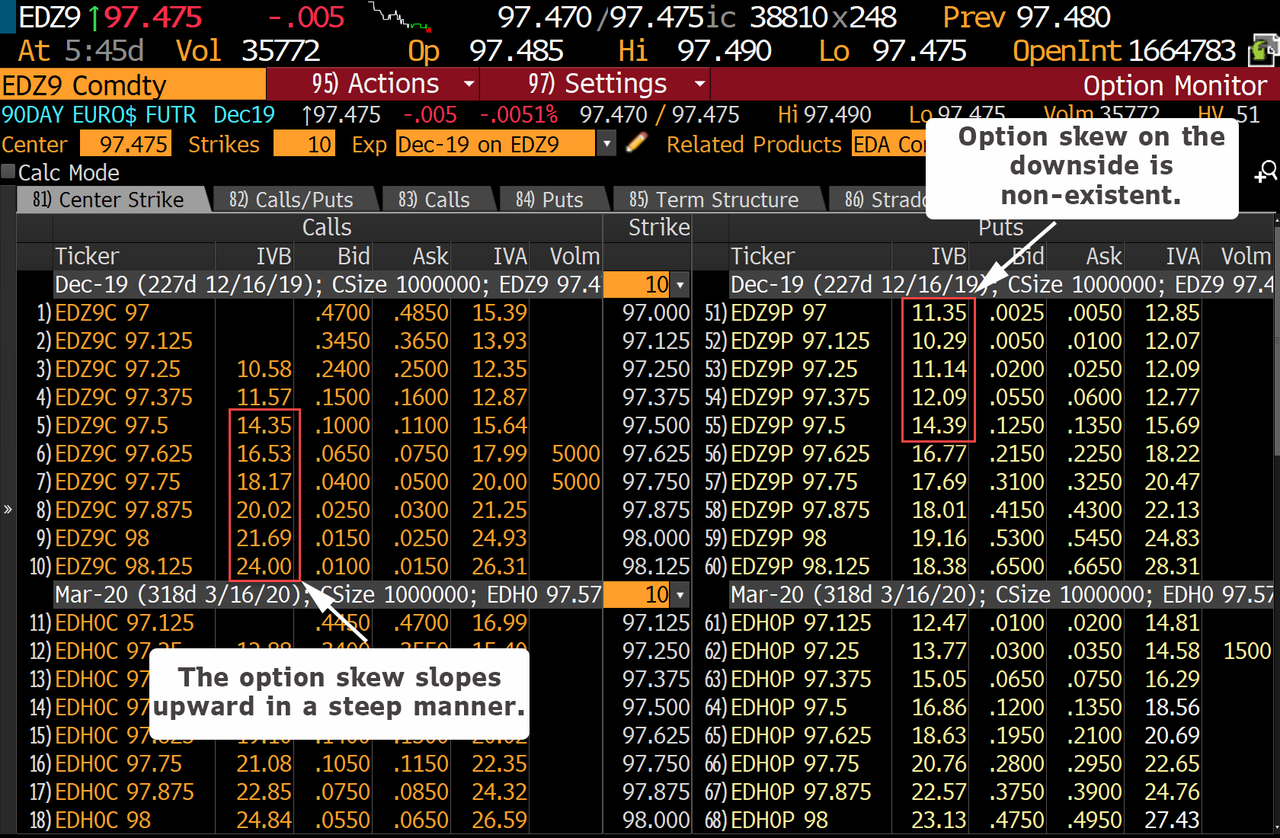

And that is exactly how the market is currently set up.

Here is the current bid-offer for the option series on the December 2019 eurodollar futures contract. Pay special attention to the column labeled IVB – that stands for Implied Volatility Bid. This is the calculated implied volatility based on the bid.

Let’s backtrack to the original comment from the market makers. You know, the one about this being the largest skew they can remember. What do they mean?

They are talking about the stunning difference between the implied volatility of the upside calls and the downside puts. Look at the out-of-the-money calls. They are bid in the 20%’s. Then compare it to the out-of-the-money puts. They are giving those puts away with implieds in the low teens.

This skew has been created through a relentless institutional order flow of players buying upside gamma and sell downside protection over the past couple of months.

If we knew the forward price volatility for the eurodollar futures contract would be normally distributed – that there would be no tendency for the up moves to be any larger or more frequent than the down moves, then this option skew would be an absolute phenomenal opportunity. An option market maker would sell the out-of-the-money calls for 20% vol and buy the out-of-the-money puts for 12%. After delta hedging through the life of the option, and assuming the price volatility was normally distributed and didn’t have a fat tail to the upside, the 8% vol difference would be pure profit.

However, we don’t know for sure what the forward price distribution will look like. Yet we can deduce the message the marketplace is sending based on this pricing.

The market overwhelmingly believes the next move for the Federal Reserve is to cut. And even though the curve is already pricing in some easing, participants are concerned there will be a dramatic downside surprise move in rates. That’s why they are willing to pay this record skew in eurodollar futures options.

The pros are bearish

This fits with my narrative that professional investors are increasingly bearish on both the economy and risk assets (”One Group will be Spectactularly Wrong”). Money managers are demanding protection against lower rates. And they are bidding for that protection at levels of skew that is either unprecedented, or close enough to a record to not matter.

Don’t underestimate the signal this eurodollar option skew is sending. Market participants will not be surprised with lower rates. That is what they are expecting. Professional market participants have convinced themselves the economy is rolling over. The business cycle has turned and it’s only a matter of time before Powell is panicking by slashing rates lower. If this scenario does not come to pass, then they will have bet incorrectly.

However, and this is where it gets nuanced, given the record skew even if they are correct about the direction of rates, it might be all priced in. Trading is all about the difference between expectations and reality. Sometimes it’s difficult to judge expectations. Yet other times the record skew screams out loud which way the professionals are leaning.

Not everyone is in that camp

I am less bearish on the economy than most professional investors. Maybe I just don’t get it. Maybe I am a fool for believing the tax cut stimulus has not yet finished making its way through the economy. Perhaps I am not knowledgeable enough to understand that regardless of Powell’s violent flip-flop the Fed cannot extend the business cycle. Yeah, I can understand why you might ignore my ramblings.

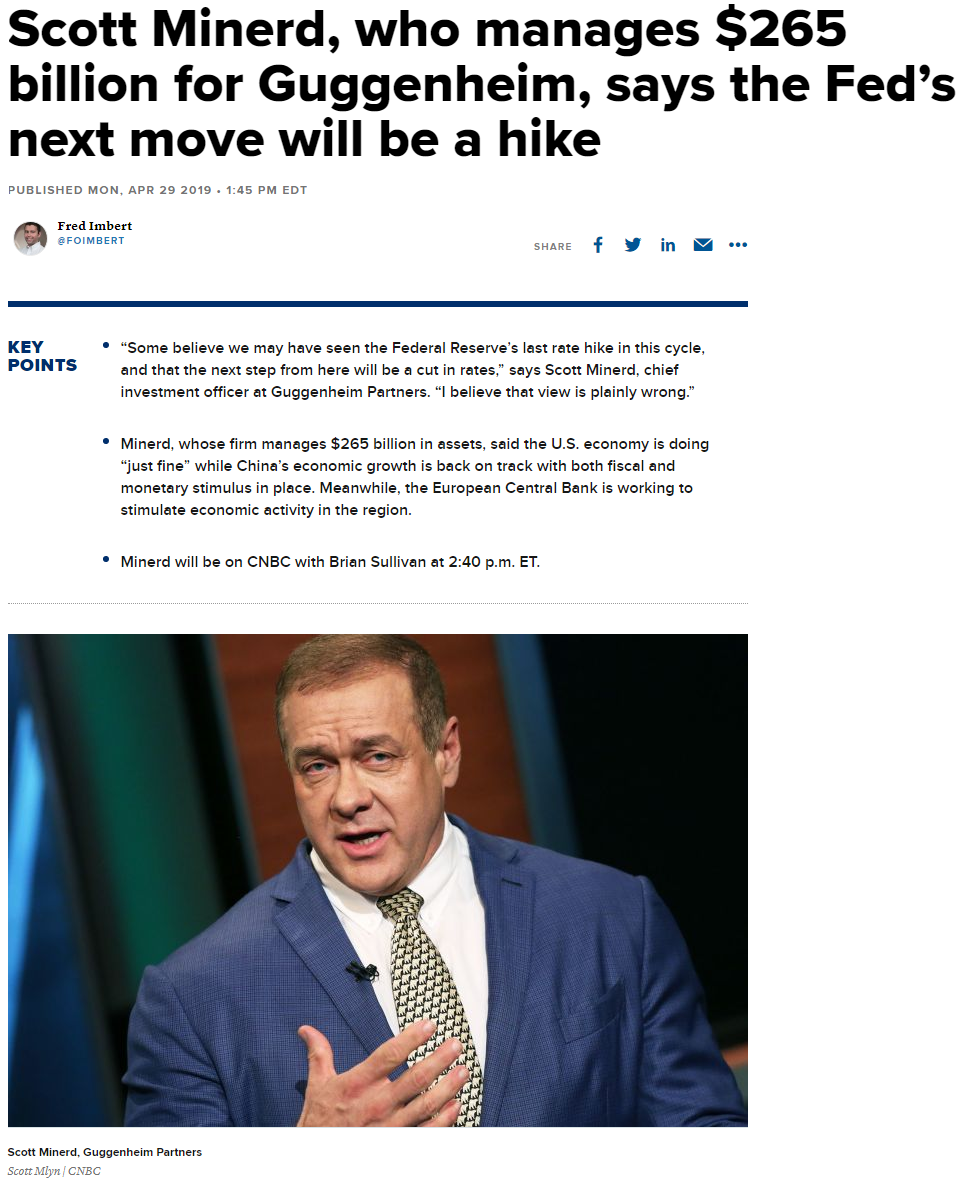

However, it might be easy to dismiss my ridiculous world-will-not-end-tomorrow call, but what about Guggenheim’s Scott Minerd’s forecast?

Scott believes the Fed’s next move is a hike! Talk about an out-of-consensus view.

This goes against what almost everyone else believes.

It’s above my pay grade to predict if the Fed’s next move is a hike or a cut, but I know one thing for certain – the market will react violently differently between those two scenarios.

Assuming the Fed is not cutting because of some geopolitical disaster, but rather because the economy has simply rolled over, an easier Fed policy move would be welcomed by the market. But make no mistake – it would be largely priced in. It would be met with muted price changes and most likely disappointment the Fed was not even more aggressive.

However if the Guggenheim view ends up playing out, the violence in the short end of the fixed-income market will be epic.

We have rallied hard off the lows from when Powell was leaning heavily hawkish with his “we are a long way from neutral” comments.

But have we rallied too much? Doesn’t the fact that even with this rally, market participants are gobbling up record amounts of out-of-the-money calls, not cause you pause?

I can tell you one thing for sure – when all the pros are leaning one way, I wouldn’t want to be in their camp.

Cheap way to bet

Yet if you believe that Scott Minerd is correct and that the next move is a Fed hike, there is probably no better way to play that outcome than snapping up some of these cheap puts. The distorted skew means they are practically giving them away.

Getting long cheap gamma in out-of-the-money eurodollar puts is probably the best way to express the view that the American economy is not quite as late-cycle as the market suspects. And here is a thought I would like to leave the economic bears with; given the record steep skew, hedging a long eurodollar futures position with protective puts is probably a strategy to seriously consider.

via ZeroHedge News http://bit.ly/2DKhUSg Tyler Durden