Authored by Mike Shedlock via MishTalk,

St Louis Fed researchers concocted a scheme to pay banks still more free money, but this time hiding all of it.

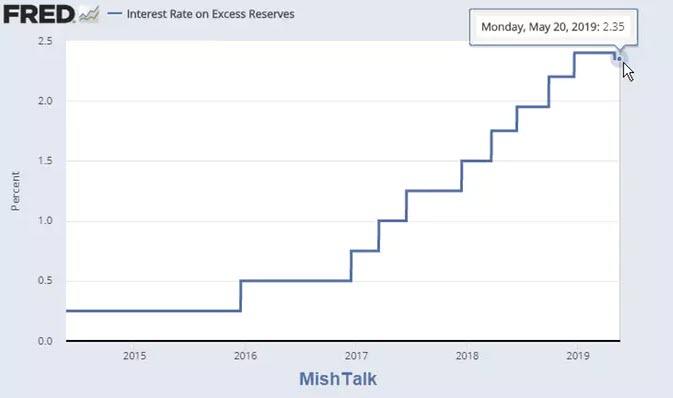

At the current rate of 2.35%, the Fed hands out about $33.58 billion in free money to the banks.

Interest Rate on Excess Reserves

The two charts show the moving target.

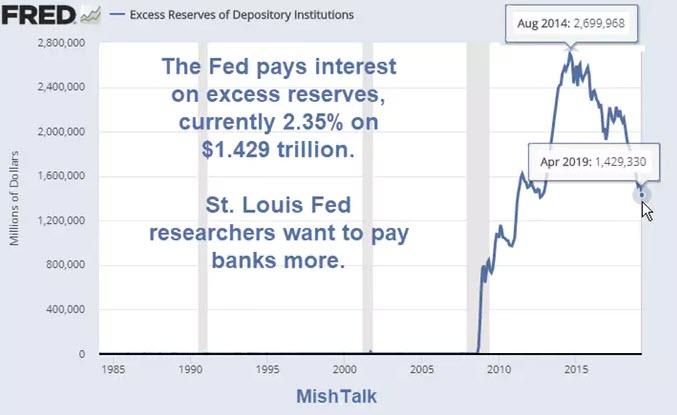

Excess reserves peaked at $2.7 trillion in August of 2014 but the interest rate on excess reserves then was only 0.25%.

0.25% of $2.7 trillion is “only” $6.75 billion in free money at an annualized rate. At the current rate, banks take in over $33 billion in free money.

The peak annualized rate was probably in August of 2017 with the interest on excess reserves at 1.95% on $2.2 trillion. That’s free money to the tune of $42.9 billion at an annualized rate.

St. Louis Fed Proposal

Please consider Why the Fed Should Create a Standing Repo Facility by David Andolfatto, Senior Vice President and Economist, Federal Reserve Bank of St. Louis; and Jane Ihrig, Associate Director and Economist, Federal Reserve Board of Governors.

Market participants are projecting ample reserves in the $1 trillion range—a level much higher than their precrisis average of approximately $20 billion.

Why should banks prefer reserves to higher-yielding Treasuries? One explanation is that Treasuries are not really cash equivalent if funds are needed immediately. In particular, for resolution planning purposes, banks may worry about the market value they would receive in the sale of or agreement to repurchase their securities in an individual stress scenario.

The Fed could easily incentivize banks to reduce their demand for reserves by operating a standing overnight repurchase (repo) facility that would permit banks to convert Treasuries to reserves on demand at an administered rate. This administered rate could be set a bit above market rates—perhaps several basis points above the top of the federal funds target range—so that the facility is not used every day, but only periodically when a bank needs liquidity or when market repo rates are elevated.

With this facility in place, banks should feel comfortable holding Treasuries to help accommodate stress scenarios instead of reserves.

Treasury Sales On Demand – Guaranteed Bid

Lovely. The Fed proposes a facility that would allow banks to hold higher yielding treasuries instead of holding excess reserves, by guaranteeing a bid for the treasuries.

Sweet Spot

Given the inverted nature of the yield curve in many spots there isn’t all that much to gain, but there is some.

The current sweet spot in this scheme is the 6-moth T-bill. It yields about 10 basis points or so more than the 2.35% the Fed currently pays on excess reserves.

Annualized Value

The annualized value of the proposed scheme is only $1.4 billion. Still, that’s nothing to sneeze at.

Hidden Beauty

Please don’t forget about the hidden benefits.

Like what?

See if you can figure it out before reading further.

Poof!

There are no longer any excess reserves.

Banks get to buy treasuries with a guaranteed bid. So they do. En masse. In a flash, the top chart will look like it did in 2005, with everything seemingly back to normal.

Judging from the top chart, one has to wonder how much this has been front-run already, above and beyond stated tapering, now on hold.

via ZeroHedge News http://bit.ly/2HuN3Ly Tyler Durden