Goldman Sachs is the latest to cut its Tesla price target, with analyst David Tamberrino cutting his target to $158 from $200 due to a lower likelihood of the company hitting his upside volume scenarios and continued questions about demand heading into the second half of the year, according to a new note released Thursday morning.

Tamberrino says he “expects shares to be on a downward path as it becomes more clear that demand for the company’s current products are below expectations”.

While stating that Q2 deliveries might reach the FactSet consensus, he identified his cause for concern about estimates beyond Q2, which he feels may have to come down:

“…we do believe 2H19 (and beyond) volume estimates look high considering there are fewer levers to pull to stoke demand going forward (i.e., company released lower priced variants of the Model 3, a leasing option was introduced, and right-hand drive orders have begun).”

He continues, commenting how the drop off of the Federal Tax Credit and cannibalization between models is a concern:

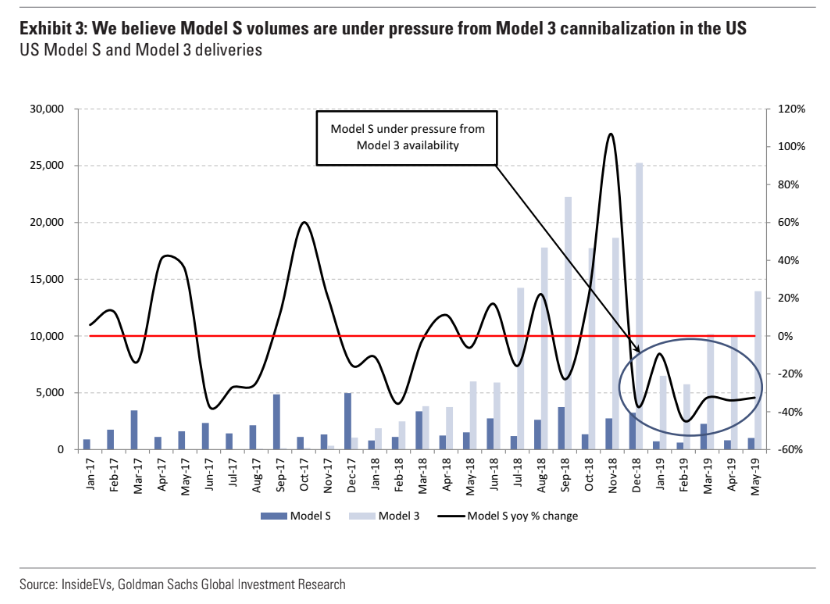

Further, when coupled with a lack of direct impetus to open up new demand pockets (other than introducing incentives or more attractive financing rates) and another step-down in the US Federal Tax Credit for TSLA vehicles beginning on July 1 — we believe 2Q19 was a better environment for demand and thus deliveries, but to a level that is likely not sustainable. We believe that is the largest question for investors to underwrite at this point — what are sustainable demand levels for the Model S, Model X, and Model 3 — and how does that change with the introduction of Model Y production. While there is potential upside surprise from a faster ramp or pull forward of Model Y ahead of schedule (i.e., 2H20 volume production targeted, but with 70% parts commonality to the Model 3 and decision to manufacture in Fremont — this could be accelerated), there is likely cannibalization of current Model X and Model 3 product demand with a crossover variant.

Tamberrino also raises the all important question of cash: when is Tesla going to need it again and, as he asks, “does being a net-debt Auto OEM make sense?” He writes:

In our view, there is an incremental risk associated with carrying a net-debt position, particularly for companies that fit into more mature, cyclical industries that have higher fixed costs and potential for quick cyclical volume declines. Along those lines, we continue to believe TSLA’s net-debt leverage (3.5x on TTM 1Q19 EBITDA) is high — particularly relative to OEM peers that carry net-cash balance sheets — and could become an issue in the event secular growth from electric vehicles slows or declines (not our current view).

The note then reviews what type of volume declines would result in a “tighter liquidity” environment for the company:

Along those lines, we believe that the company would need to have volumes be cut in half from our 2019 forecast in order to see that tighter liquidity environment — i.e., decline from approx. 320k to 160k. Of course, with a declining volume environment the company would likely cut back on its growth capex spend (among other initiatives) and it would likely necessitate a further decline in volumes to eat into the current cash cushion. We recognize that this exercise is subject to several moving parts (inclusive of TSLA tying up cash/working capital into vehicles that could be produced but not sold), and for illustrative purposes we show a range of outcomes below in Exhibit 7.

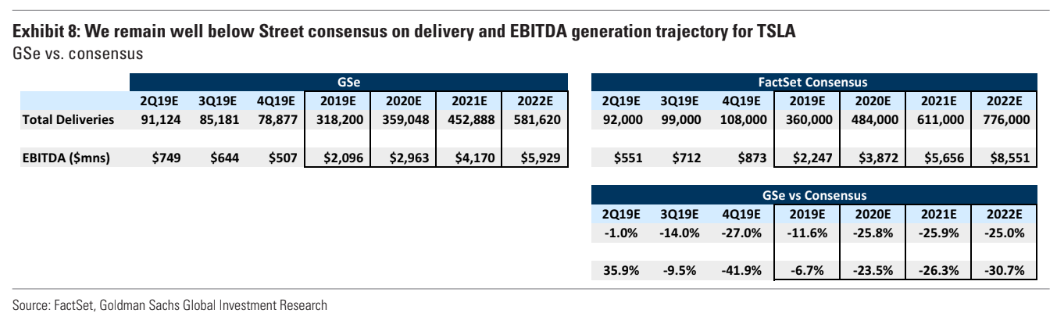

Tamberrino also makes a point of noting that Goldman is “well below” other estimates across Wall Street.

He concludes:

12-month price target declines to $158 (from $200) on our lowered aggregate delivery estimates for Automotive in combination with a shift in probability weighting from the Upside scenarios (from 35% to 25%) toward our Base (from 45% to 50%) and Downside cases (from 20% to 25%) as we now see a lower likelihood of TSLA achieving production and delivery of multiple millions of vehicles by 2025. Further, we lower our applied P/E multiples given a lowered unit trajectory out through 2025. Broken down by segment, our probability-weighted valuations for the Automotive segment decline to $138 (down from $180), Tesla Energy segment is unchanged at $16, and the SolarCity segment is unchanged at $4.

Among key risks to this estimates, Tamberrino identifies “faster-than-anticipated Model Y introduction, increased demand for current products (Model S, X, 3), increased EV subsidies, improved cost structure, sustained positive free cash flow generation, successful new product launches (Solar Roof, Pickup truck, semi), and a breakthrough in autonomous technology development.”

We’re not holding our breath on any of those.

via ZeroHedge News http://bit.ly/2L3OS4n Tyler Durden