Japan’s 10Y Yield On Verge Of Turning Positive As Abe Prepares Massive Debt-Busting Stimulus

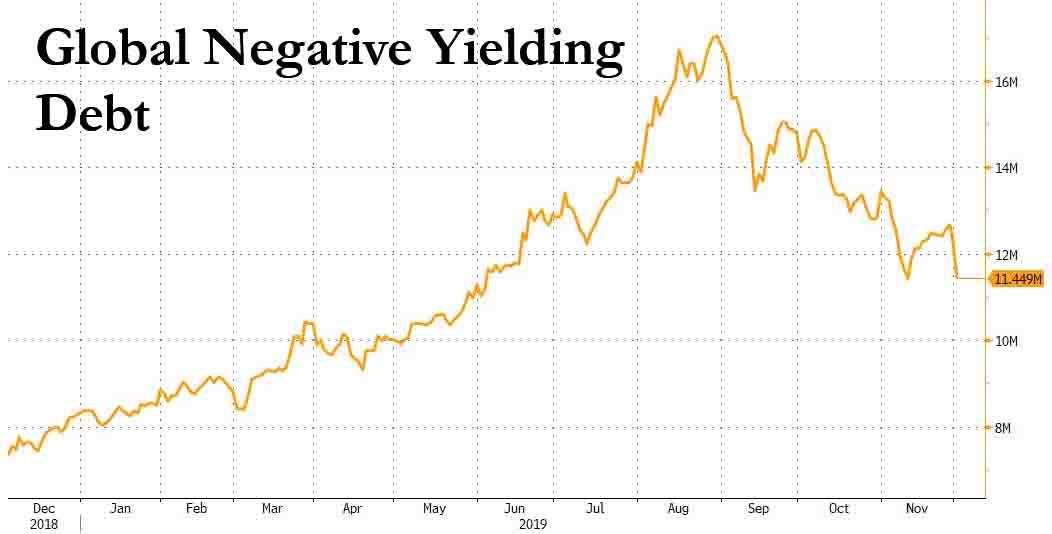

After the world’s negative yielding debt hit a record $17 trillion at the start of September, mostly as a result of Japanese debt the vast majority of which is trading in negative territory, this number has shrank substantially in recent months, sliding to $11.5 trillion in the past three months.

Well, as of today that number is in danger of becoming far, far smaller in the coming days because the one single bond tranche that represents the biggest component of global negative debt, Japanese 10Y bonds, is on the verge of flipping to positive yield territory, for the first time since April.

In fact, overnight the 10Y JGB yield rose as much as just 0.8bps away from 0 following what was the lowest bid to cover for a 10Y auction since August 2016.

So what gotten Japanese bondholders spooked in recent days? The answer: joining the rest of the world in pushing for even more debt, Japan – which currently has a debt/GDP of about 250% – is preparing an economic stimulus package worth $120 billion to support fragile growth (i.e., a debt-funded stimulus), according to the Nikkei and Reuters.

While the package would come to around 13 trillion yen ($120 billion), it would rise to as much as 25 trillion yen ($230 billion) when private-sector and other spending are included. A similar stimulus in the four times as large US economy would be roughly $1 trillion.

Some details: the 13 trillion yen includes more than 3 trillion yen from fiscal investment and loan programmes, as the heavily indebted government seeks to take advantage of low borrowing costs under the Bank of Japan’s negative interest rate policy. In other words, the government is hoping to kick start a lite version of MMT, and with everyone else begging Abe to be the world’s MMT guniea pig, it just may work (if only for a bit). Direct government spending is expected to reach around 7-8 trillion yen.

The Nikkei business daily reported on the weekend that the government was considering putting together a large-scale stimulus package with fiscal spending exceeding $92 billion. Since then the number appears to have only grown.

With the BOJ’s stealth taper meaning Kuroda is now monetizing just a tiny fraction of the bonds the BOJ was mandated with buying for the simple reason that it has almost run out of monetizable debt, a fiscal stimulus may be Abe’s only option, even if it means the ultimate collapse will be even bigger.

Meanwhile, Japan’s collapse – ironically enough, a function of its massive debt load – has resumed, and in the third quarter, its economic growth slumped to its weakest in a year as soft global demand and the Sino-U.S. trade war hit exports, stoking fears of a recession. Some analysts also worry that a sales tax hike to 10% in October could cool private consumption which has helped cushion weak exports.

Such spending could strain Japan’s coffers – the industrial world’s heaviest public debt burden, which tops more than twice the size of its $5 trillion economy.

Despite the headline size of the stimulus, actual spending would be smaller in the current fiscal year, and economists are not expecting much of a boost.

Which said otherwise, means don’t think of Japan’s fiscal stimulus so much as an actual fiscal stimulus – those have been tried repeatedly and failed to actually “stimulate” the economy – but as a way for the BOJ to have more debt to monetize. Without it, Kuroda will run out of bonds to purchase as soon as next year.

“We expect this fiscal year’s extra budget to total around 3-4 trillion yen. We should not expect it to substantially push up the GDP growth rate,” said Takuya Hoshino, senior economist at Dai-ichi Life Research Institute.

Amusingly, the Nikkei claimed that the spending package won’t involve deficit-covering bond issuance; which of course, is hilarious because all debt issuance in Japan, where the “helicopter-money” MMT experiment is about to unfold, is deficit covering.

Tyler Durden

Tue, 12/03/2019 – 17:45

via ZeroHedge News https://ift.tt/360wikY Tyler Durden