Tesla Pops After Morgan Stanley Doubles Bull Case Target To $1200 One Month After Setting It At $650

Morgan Stanley is looking more and more like a dog chasing its tail in its “analysis” of Tesla. Recall, about one month ago, Tesla was downgraded to “Sell” by Morgan Stanley after the stock’s run up to about $520 per share.

And it was less than 2 months ago, in December, when Morgan Stanley’s Adam Jonas reminded the investing public that he was “not bullish on Tesla longer term” – and that was with the stock at $420 per share.

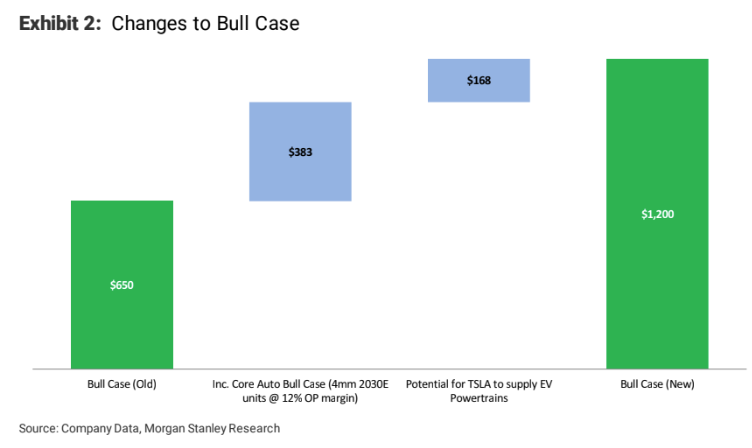

But now that dilution has taken place and the stock has blown past Jonas’ target, it’s back to the drawing board yet again for Jonas and his team. This morning, Jonas has outdone himself once again – raising his bull target case to $1200 per share (from $650 per share in mid-January).

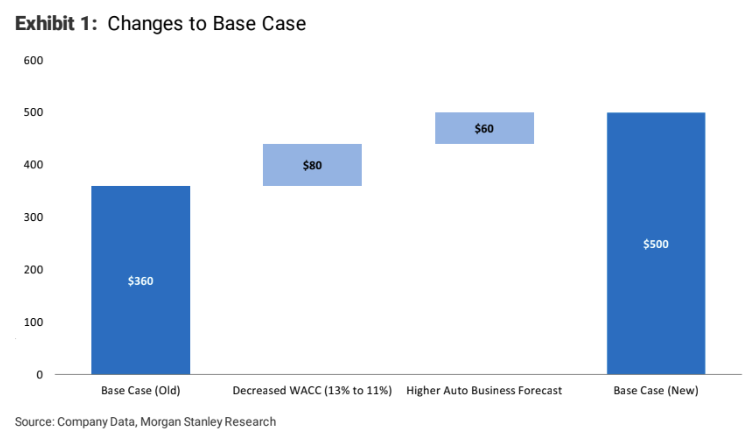

In addition to almost doubling the bull case, Jonas raised his mid-point price target on the stock from $360 to $500 per share. His bull case would give Tesla a market cap of about $220 billion. And ostensibly just to make sure he has an out, Jonas kept the stock rated at “underweight”.

Jonas has cited Tesla’s potential to become a battery supplier as his reasoning for adjusting his price target. He also reiterated his aggressive assumption that Tesla could own 30% of the global EV market down the road. This is inclusive of 4 million deliveries by 2030 plus Tesla potentially becoming a powertrain and battery supplier.

He also casually includes $100 per share of “mobility services and energy SCTY/value”.

Our new bull case reflects 4 million units of auto volume by 2030 with a 12% operating margin. This compares with our base case forecast of 2.2 million units and a 10% OP margin by 2030. Additionally, we have included $168/share of value for the company’s potential to supply EV powertrains (battery + e-motors and supporting ‘skateboard’ architecture) to other OEMs on a 3rd party supply basis. The combined 6 million units of EVs we assume in our Tesla bull case accounts for roughly 30% of the global EV market (on Morgan Stanley forecasts), which we believe is an aggressive assumption. Our bull case also includes just over $100/share of mobility services and energy/SCTY value. The shares offer roughly 50% potential upside to our bull case.

Jonas justified changing his base case scenario for shares by “adjusting” the WACC in his DCF model, which added $80 per share, in addition to raising his forecast in auto – which is an industry we have been constantly reminding readers – is in the midst of a global recession.

The price target change is driven by two factors: (1) our higher forecast for the auto business, which adds $60/share,and (2) lowered WACC in our DCF to 11% from 13% previously, which adds $80/share. We believe the lowered WACC, while still higher than most other companies under our coverage, is justified given the company’s proven track record of attracting new capital under

favorable conditions and a significantly reduced level of balance sheet stress over the past year. The 5-year CDS (150 to 175bps) sits in line with auto companies such as Ford. The stock offers 38% potential downside to our new price target.

Tesla shares are trading higher in the pre-market session on the news.

But in addition to keep his “underweight” rating, Jonas also offers up additional caveats at the end of his note, stating he thinks there is an “unfavorable risk-reward skew” on the name:

Taken together, while we have raised our fair value for the company, we believe the shares offer an unfavorable risk-reward skew vs. other stocks under our coverage and reiterate our Underweight.

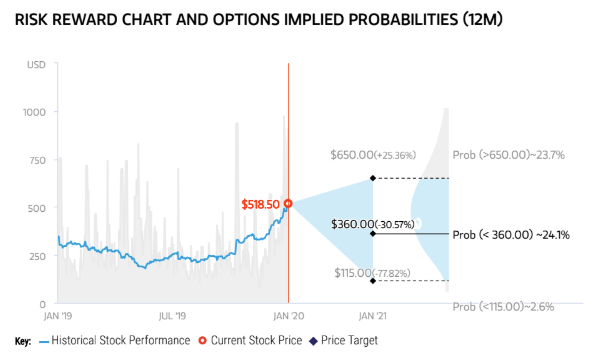

Remember this valuation cone, from January, with a spread of about $535 between Jonas’ bear and bull cases?

Apparently, that wasn’t enough breathing room for Jonas’ “analysis” and so now that chart looks like this (yes, that is now a $980 spread between Jonas’ bear case and his bull case):

Tyler Durden

Tue, 02/18/2020 – 08:56

via ZeroHedge News https://ift.tt/39C3WiK Tyler Durden