Stockman: Next Comes The “Turbulent Twenties”

Authored by David Stockman via PeakProsperity.com,

The past 30 years of False Prosperity is over…

The coronavirus is now exposing a far more deadly disease: Namely, the poisonous brew of easy money, cheap debt, sweeping financialization and unbridled speculation that has been injected into the American economy by the Fed and Washington politicians.

It has turned Wall Street into a dangerous gambling casino while leaving Main Street buried under mountainous debts, faltering investment in growth and productivity and the hand-to-mouth economics of spending more than you earn.

It has also left the American economy exceedingly vulnerable to external shocks. That’s because 80% of households have no appreciable rainy day funds and businesses have hollowed out their balance sheets and artificially extended their supply chains to the four corners of the earth in order to goose short-run profits and share prices.

However, this unprecedented fragility is becoming evident as public health authorities around the world aggressively move to contain the Covid-19 contagion. This will mean separating workers from their workplaces, consumers from the malls, diners from the restaurants, travelers from the airlines, hotels and resorts and much more like and similar disruptions to the supply-side of the economy.

In short, the world’s supply chains are buckling and freezing-up, thereby causing production and incomes to fall abruptly. In turn, shrunken incomes and cash flows will pull the legs out from under the edifice of debt and speculation that has been piled atop the American economy.

So both a renewed financial and economic crisis and an abrupt change of course lie dead ahead. The 30-year era of False Prosperity is over.

Accordingly, the Turbulent Twenties have begun. This will be a decade when the chickens come home to roost. It will be a time when the cans of delay and denial may no longer be kicked down the road to tomorrow.

To the contrary, the 2020s will mark an era when today’s economic and political fantasies are crushed by America’s accumulated due bills.

Bubbles will be burst. Speculators will get carried out on their shields. Easy money wealth will evaporate. Fiscal trauma will ensue. The national joy ride will end.

The decade of reckoning that lies ahead is rooted first and foremost in the fecklessly incurred mega-debts of the private and public sectors alike. Together they have soared to the staggering sum of $75 trillion.

That’s 5X more than the $14 trillion outstanding three decades ago.

Yet the proceeds from these massive borrowings were not used to invest and provide for tomorrow, but to live high on the hog today. After three decades of such artificial debt-fueled “prosperity”, the very warp and woof of American society has been deformed.

For example, eighty percent of U.S. households live essentially hand-to-mouth. But that’s not because they are naturally imprudent; it’s because they have been incentivized to borrow and spend, while being punished for saving and setting aside for life’s unforeseen contingencies and setbacks.

Likewise, the C-suites of corporate America have been rewarded for strip-mining their balance sheets and cash flows in order to pump money into Wall Street for stock buybacks and M&A.

But this has caused investment in productive plant, equipment, technology and human resources to be shortchanged. Consequently, the growth capacity of the main street economy has been progressively eviscerated.

And most especially, the public sector has been fiscally ruined.

During the 32-years since Alan Greenspan launched the present era of reckless and relentless monetization of the public debt in 1987, there have been only four balanced budgets sandwiched between 28 years of sheer fiscal promiscuity.

That has already taken the Federal debt from $3 trillion to $23 trillion, and it’s now heading, inexorably, toward $43 trillion by the end of the 2020s. The public debt-to-GDP ratio will then reach a Greek-style 150%.

Worse still, the nation’s political system studiously ignores this obvious fiscal malignancy. That’s because the Fed and other central banks have removed the sting of rising interest rates and the “crowding out” of private investment.

So politicians have succumbed to the latest version of free lunch economics.

This has permitted, in turn, national governance to degenerate into bitter partisan warfare that has festered so long that it now threatens the very future of constitutional government.

Rather than facing tough policy choices, the Dems have retreated into identity politics and sanctimonious racialist moralizing. They’ve abandoned virtuous pursuit of the public good for cheap virtue signaling to their base.

Likewise, the GOP has prioritized building border walls and keeping people out of America’s historic melting pot on the fear they might not vote Republican. But in feeding red meat to their political base, they’ve abandoned the GOP’s real job—functioning as watchdog of the treasury and guardian of sound money.

Beyond the water’s edge, the bipartisan duopoly has immersed itself in the projects of Empire and pretensions to being the world’s indispensable nation and global gendarme. So doing, it has actually undermined homeland security while saddling the nation with trillions of debt to fund Forever Wars that are illegal, immoral and pointless.

These perversions of governance ultimately resulted in the freakish 2016 election in which the GOP accidentally nominated a bombastic outsider—a Great Disrupter who had not been house-trained by the Washington establishment.

Yet the very prospect of a Trump presidency caused the incumbent Dems to baldly and illegally deploy the surveillance tools of the national security apparatus to detour his candidacy. And then to attempt to abort his presidency via the RussiaGate and UkraineGate/Impeachment hoaxes once the voters had spoken.

At the same time, even as the Donald has brashly and pugnaciously fought the unconstitutional coup against his presidency, he, too, has gone about the business of filling the Swamp even deeper, rather than draining it as he promised on the campaign trail.

In fact, the Federal Leviathan—including its national security branch—has never been bigger, fatter and more wasteful than under Trump.

The Donald has increased Federal spending in constant dollars (2019 $) by $180 billion per year during his term to date. That compares to $120 billion per year under George Bush the Younger, $80 billion under Obama and $40 billion per year under Clinton.

So there isn’t anything which resembles MAGA coming down the pike during the 2020s and beyond. Trump has only made the inherited trend of soaring debts and diminishing growth measurably worse with his four-pronged assault on sound economics.

Trade Wars. Border Wars. Fiscal Debauchery. Easy Money attacks on the Fed.

These are not the route to MAGA. They are the path to bigger government in Washington, dangerous bubbles on Wall Street and diminished prosperity, opportunity and liberty on Main Street.

Accordingly, it is now way too late for a stick save from either political party or any state institution bivouacked in the Imperial City. And that especially includes the madcap money printers at the Federal Reserve.

The fact is, the engines of free market capitalism have been corroded and paralyzed by three decades of bad money and bad policy.

What has passed for “recovery” since the Great Recession has been only a temporary debt-fostered reprieve. Likewise, the soaring stock market reflects the greatest monetary deformation in history, not the rational discounting of a beneficent future.

Accordingly, ten malefic trends will dominate national life during the long night of reckoning which lies ahead.

-

The spectacular failure of Keynesian central banking;

-

A prolonged, painful reversal of the three-decade long hyper-inflation of financial asset prices that has resulted in the Everything Bubble;

-

The violent implosion of America’s fiscal accounts;

-

An intensified central bank war on savers, fixed income retirees and holders of cash;

-

Peak Debt-induced suffocation of domestic economic growth;

-

Ferocious global economic headwinds arising from the demise of the Red Ponzi;

-

An outbreak of unprecedented partisan acrimony rendering Washington completely dysfunctional and imperiling America’s very constitutional foundation;

-

The lapse of Imperial Washington into belligerence, retreat and failure all around the planet;

-

The Baby Boom retirement tsunami, which will cause entitlement spending to soar and generational conflict to erupt like never before; and

-

A virulent outbreak of class warfare and redistributionist political conflict unprecedented in American history owing to a stagnating economic pie.

Moreover, there is a powerful reason to keep abreast of these Turbulent Ten trends.

To wit, these baleful developments are not just possibilities. They are well nigh certainties!

And they are ultimately rooted in a common cause.

Namely, the three decade long explosion of debt, speculation and financialization that was initiated in October 1987 when Alan Greenspan bailed out Wall Street gamblers and launched what has become a toxic worldwide regime of Keynesian central banking.

Consequently, America’s current $74 trillion mountain of public and private debt has become contagious.

On a worldwide basis, total debt outstanding now totals $255 trillion or a staggering 3X global GDP of $85 trillion. It now constitutes the greatest barrier to continued growth, prosperity and financial stability in all of economic history.

Even more crucially, these brobdingnagian figures did not materialize during the last three decades because everyday people suddenly lost their senses and became addicted to unsustainable levels of debt, leverage and financial speculation.

To the contrary, the people here and abroad were misled, induced and baited into burying themselves under crushing debts by agents of the state—especially its central banking branch.

The tools of deceit were falsified interest rates, artificially inflated asset prices and a hoary theory that debt-fueled “stimulus” injections by the state can create a permanent increase in economic growth and societal wealth.

No they can’t!

These mountains of debt can temporarily goose GDP, of course, because GDP accounting is inherently incomplete: It views the economy as simply a matter of sequential flows—quarter after quarter, year upon year– without regard to balance sheets and the accumulated carry cost of debt over time.

Moreover, this Keynesian blindness to balance sheets and their systematic impairment has gotten far more consequential since Greenspan launched a wholly new form of monetary central planning in October 1987.

Under the latter, the price of debt has been deeply and systematically falsified by the central banks, thereby providing a powerful artificial incentive to borrow and a misleading signal to debtors about its longer-run implications.

Balance sheets have been deeply impaired for households and governments especially because they do not borrow in order to acquire productive assets capable of defraying the accumulating cost of carry. Instead, all the added debt went into living high on the hog today.

Nor has the private business sector escaped the damage caused by deep repression of interest rates. That’s because the cost of benchmark debt (i.e. the 10-year U.S. treasury note) is really the master “cap rate” or valuation multiple for the entire financial system.

Artificial and sustained repression of cap rates, therefore, results in proportionately higher asset prices and increased price/earnings multiples—meaning that cheaper debt and richer share prices are one of the most toxic consequences of Keynesian central banking.

It provides powerful incentives to the corporate C-suites to borrow at sub-economic costs and use the proceeds to fund stock buybacks, thereby increasing per share earnings and goosing the value of top executives’ own ample stock options.

Likewise, cheap debt causes a huge distortion in the M&A market. Acquisitions are made to look “accretive” not because the make business sense or because there are true, sustainable synergies, but because they carry cost of purchase debt is so low.

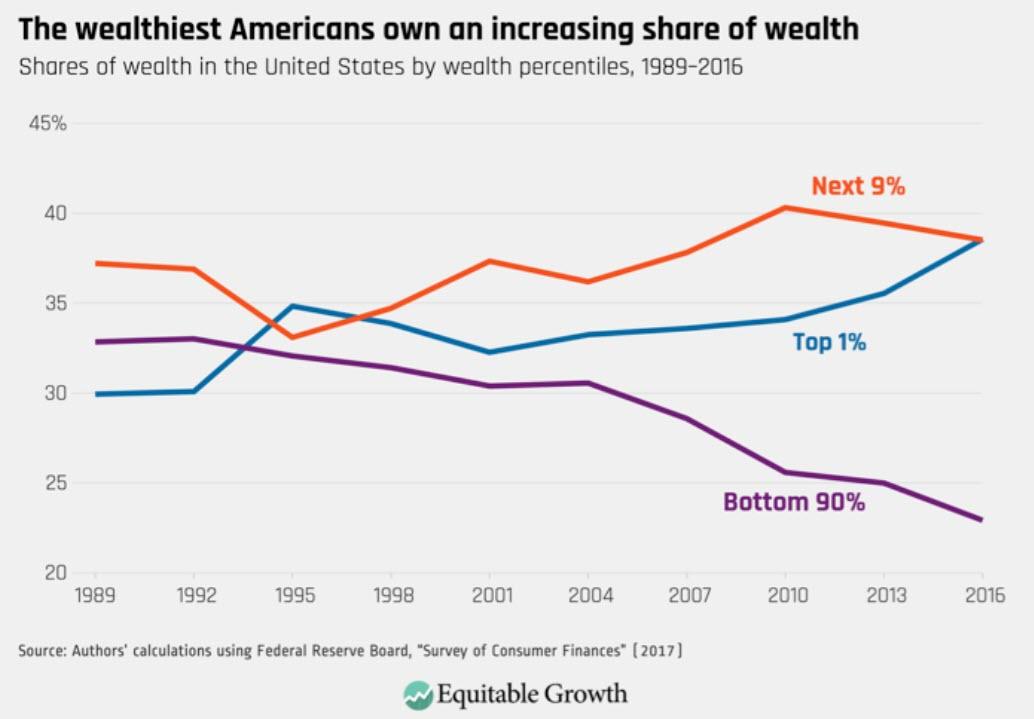

Needless to say, these forms of financial engineering redistribute financial wealth to the top 1% and 10% of households. The latter own 40% and 85% of the stock, respectively, and they have gained mightily since Greenspan initiated the present era of Keynesian central banking in the late 1980s.

At the end of the day, the relentless and ever deepening financial repression—especially during the decade since the financial crisis— has generated precious little gain in national output and jobs beyond what capitalism does on its own.

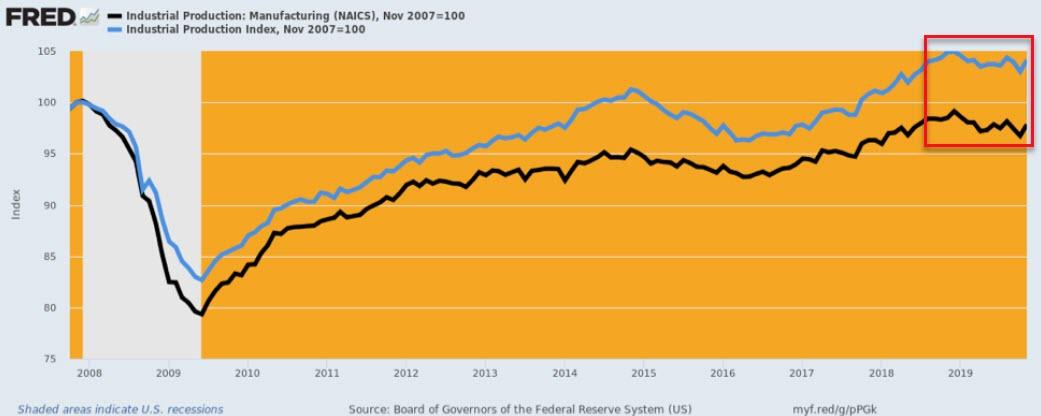

For example, manufacturing production is still 2% below pre-crisis levels of November 2007. And total industrial production has crept just 4% higher over 12 years.

Moreover, even the huge one-time inflation of financial asset prices on Wall Street didn’t embody sustainable real wealth because it was primarily based on multiple expansion, not earnings growth.

Exactly 31-years ago in early 1989, for instance, the S&P 500 index stood at 295 where it represented 12X earnings of $25 per share.

At the same PE multiple today, the index would weigh in at just 1600 or less than half of the 3240 level where it ended 2019.

Stated differently, 56% of the S&P 500 gain since 1989 is owing to PE multiple expansion, not earnings growth, and it materialized during a three decade interlude when the long-term growth capacity of the US economy was being ground to the vanishing point.

That is, PE multiples should have been falling, not soaring to the nosebleed section of history.

Indeed, this “bad money” regime of the Keynesian central bankers has now finally taken itself hostage.

The central bankers have fostered such massive and egregious bubbles that they are literally terrified by the prospect of another stock market meltdown like those of 2000-2002 and 2008-2009.

In turn, the latter would bring a renewed bout of desperate restructurings, layoffs and asset liquidations in the C-suites and a new round of recession on main street.

So the Fed has simply launched a Hail Mary which is so transparent and incendiary that it will surely catalyze the final blow-off top early in the 2020s.

After it had distorted, falsified and inflated financial asset prices beyond all recognition—the Fed dithered and delayed shrinking its balance sheet, thereby putting the lie to Bernanke’s solemn pledge that after the unusual and exigent conditions of the financial crisis had passed they would reduce the Fed’s massive trove of Treasury and GSE debt to pre-crisis levels.

It didn’t. After a tepid 15% balance sheet retrenchment through August 2019, the Fed actually turned tail and ran in the face of bitter attacks from the White House and unrelenting pressure from the bully boys and crybabies of Wall Street.

And now the last bit of sanity in the Eccles Building has vanished. From a low of $3.76 trillion on August 28, the Fed has already pumped $406 billion into the bond pits. That represents a staggering $1.1 trillion annualized rate of balance sheet expansion.

That’s money printing on steroids. It is also the great monetary match. Stated differently, the repo ruckus last September was the warning bell that the 30-year era of Bubble Finance was fixing to blow.

But the fools in the Eccles Building, blindly fixated on enforcing their interest rate pegs, effectively got out a gasoline hose and fueled what is now the blow-off top.

And that will pave the way for the Turbulent Twenties, and for the unfolding of all the baleful factors listed above.

There has rarely been such a fraught moment in American history.

During the Turbulent Twenties ahead we are heading for the double whammy of a political/constitutional crisis and a thundering financial breakdown at the same time.

Indeed, this perfect storm will gravely impact the personal liberty and economic welfare of every American citizen—so you need to understand what’s coming down the pike and how it will impact Washington and Wall Street alike.

You also need to understand that there has been no Trump b0om, whatsoever—even if the Donald was right during the campaign. That’s when he castigated Washington’s failed economic policies and labeled the faux prosperity of 2016 as a big fat ugly bubble that was fixing to implode on the American people.

Still, just because Donald Trump targeted the symptoms correctly that doesn’t mean he had a plan to fix the American economy or the skills and know-how to move the turgid, essentially paralyzed, machinery of the Federal government constructively forward.

In fact, the mainstream media has the whole story wrong. The Donald is not remotely the force of nature he’s been made to seem by the Trump-obsessed journalists and talking heads.

To the contrary, he’s actually a political flyweight, megalomaniacal incompetent and bile-ridden bully who stumbled into the Oval Office against all odds; and then lucked-out a second time by riding high on the final three-year crest of a deeply impaired and unsustainable economic recovery and monumental stock market bubble.

And here is where experience comes in. Since starting in Washington as a legislative assistant in 1970, we have seen every business cycle and President up close and personal.

So we know that the Donald committed the most egregious rookie mistake in the history of the American presidency.

That is, he insouciantly embraced a financial bubble that was destined to crash and took ownership of a struggling, geriatric business cycle expansion that had “recession ahead” written all over its forehead.

After all, the Donald was sworn in during month #90 of what was already the third longest business expansion in American history. It is now month #126 and it will be month #138 when his first term ends.

Here’s the thing. We are already at a point never, ever reached before.

Even the tech boom of the 1990s—previously the longest ever cycle—ended in recession during month #119, and back then there were plenty of tailwinds to keep it going.

Those year 2000 tailwinds, of course, have now become ferocious 2020s headwinds.

Europe is rolling over into recession. The Red Ponzi is floundering under its massive load of $40 trillion of debt and staggering malinvestments.

And the US economy is imperiled by $74 trillion of public and private debt and egregious Wall Street bubbles whose days are clearly numbered.

Moreover, recessions have not been outlawed by the economic gods and there are overwhelming odds that the next one will hit sometime soon as the 2020s unfold.

And when it does, Wall Street, the US economy and the Donald’s fantasy of MAGA will come tumbling down with it.

Accordingly, we think the Donald will mainly be remembered not as the restorer of MAGA nor as the statesman who rescued America from a day of reckoning that has been building for more than three decades.

Instead, the Donald is destined to be remembered as the Great Disrupter. His lasting contribution will be that he rambunctiously discredited the handiwork of Imperial Washington.

And that will prove to be progress itself as the Turbulent Twenties unfold.

After all, it is the self-serving consensus of the bipartisan ruling class in favor of permanent war, unchained entitlements, fiscal incontinence, unsustainable debt-fueled household spending, rampant corporate financial engineering and Keynesian monetary repression and “wealth effects” based central banking that lies at the roots of our current economic malaise.

At the same time, it should be crystal clear by now that Trump has no real program to restore domestic prosperity and that he has actually made matters inestimably worse with his four misbegotten wars on the American economy.

We are referring to the above referenced Trade War on domestic consumers; Border War on needed immigrant labor; political war on the Fed when it was belatedly trying to normalize; and what amounts to a war on the nation’s solvency embedded in the Donald’s runaway additions to the soaring national debt.

As to the “undrainable swamp”, it should never be forgotten that its deep-end lies on the Pentagon side of the Potomac. Yet the Donald has fed the military/industrial- surveillance complex like never before, thereby defeating his own stated goal.

That is, America’s desperately needed pivot to fiscal and national security sanity was stopped cold by Trump’s mindless $140 billion per year boost to an already vastly excessive and waste-ridden national defense budget.

And now that crucial pivot has been further blocked by a reckless economic and political war against Iran that will do exactly nothing to further the security and safety of the American homeland.

Needless to say, even if the Donald’s policies were better focused, his efforts to make MAGA never had a chance owing to the utterly groundless Russia-collusion investigation, the Mueller witch hunt and now the UkraineGate/Impeachment farce.

These political attacks are groundless, but nevertheless have functioned to disable Trump’s presidency.

In fact, the Donald’s fluke elevation to the Oval Office has finally caused the Deep State to come out of hiding and bare its fangs against American democracy itself.

So doing, it has finally awakened the sleepwalkers of the Foxified Right about the immense dangers of the Warfare State and the sweeping surveillance and police state apparatus that has been created in the service of the neocons’ misbegotten war on terrorism and quest for Empire.

Moreover, the terrifying capabilities, resources and (purported) credibility of the nation’s $75 billion per year intelligence community were literally hijacked by Obama officials led by then CIA director, John Brennan.

It is now more than evident that they illegally pursued a plot to first forestall Trump’s election, and then to re-litigate the outcome and eviscerate his Presidency after the voters had spoken.

At the end of the day, however, the result will be a thoroughly paralyzed government in Washington.

As the 2020s unfold, therefore, the latter will prove to be utterly incapable of stopping the twin fiscal menace of the Warfare State and Welfare State—a monster that the Donald has made immeasurably worse.

After taking the $2 trillion per year of uncontrolled entitlements off the table, Trump then added insult to injury via his unfunded $1.7 trillion tax cut and massive defense and domestic spending increases.

All told, the result will be a guaranteed $20 trillion explosion of the Federal debt (on top of the existing $23 trillion) over the coming decade.

Stated differently, crunch time is coming to the casino and that’s what is sure to bring the Donald down.

The stock market is heading not only for another 50% correction (1600 on the S&P 500), but also a long L-shaped bottom rather than a quick V-shaped rebound which occurred after 2009.

So the combination of the mess he inherited and the compounding damage from his four misguided wars on the American economy add-up to a looming catastrophe.

To be sure, we do not know exactly when the brown stuff will hit the fan. But we do know that Washington’s Empire abroad and phony prosperity at home are terminally failing and that the sell-by date draws near.

We also know that whatever comes next, it won’t be MAGA. Not by a long shot.

Indeed, once upon a time the prospect of $43 trillion of public debt—even a decade down the road— was literally unfathomable.

In fact, in one of our favorite remembrances from our White House days, we recall telling President Reagan in the photo below that America was on the verge of having a $1 trillion national debt.

That was in January 1981, and at the time crossing the $1 trillion mark was almost a nightmarish prospect.

But President Reagan was not intimidated. He properly insisted that this looming Rubicon was emblematic of the mess he had inherited, and that under his watch the nation’s soaring public debt would finally be stopped cold.

Alas, it wasn’t. By the time he left office, the national debt was pushing $3 trillion, and it was off to the races from there.

When Bill Clinton packed his bags to leave the White House the public debt was $5.7 trillion, then soared to $10.7 trillion by the end of George W. Bush’s two terms, stood at $19.9 trillion when Obama moved on and has already passed $23.0 trillion on the Donald’s watch.

But here’s the thing. President Trump is no Ronald Reagan. If the Gipper couldn’t stop the Washington deficit and debt brigades, there is not a snowball’s chance in the hot place that the Donald will.

In truth, unlike all of the Gipper’s successors, who relentlessly added to the debt during their turn at the helm but at least gave lip service to the notion of fiscal rectitude, the Donald just flat-out doesn’t care and he’s taking the GOP with him into fiscal fantasy-land.

What this means is that America is now fast drifting toward the Debtberg. It is only a matter of time before the impending collision shatters the faux prosperity and wanton complacency that prevails on both Wall Street and in Washington.

Still, it is not too late to get prepared.

* * *

For those concerned about the economic threat David has has highlighted, we highly recommend considering subscribing to his Contra Corner financial newsletter, published daily.

Tyler Durden

Thu, 03/05/2020 – 16:45

via ZeroHedge News https://ift.tt/2vHiJu8 Tyler Durden