Futures Accelerate Slide On “Second Wave” Fears Ahead Of Jobless Claims

Tyler Durden

Thu, 06/25/2020 – 08:02

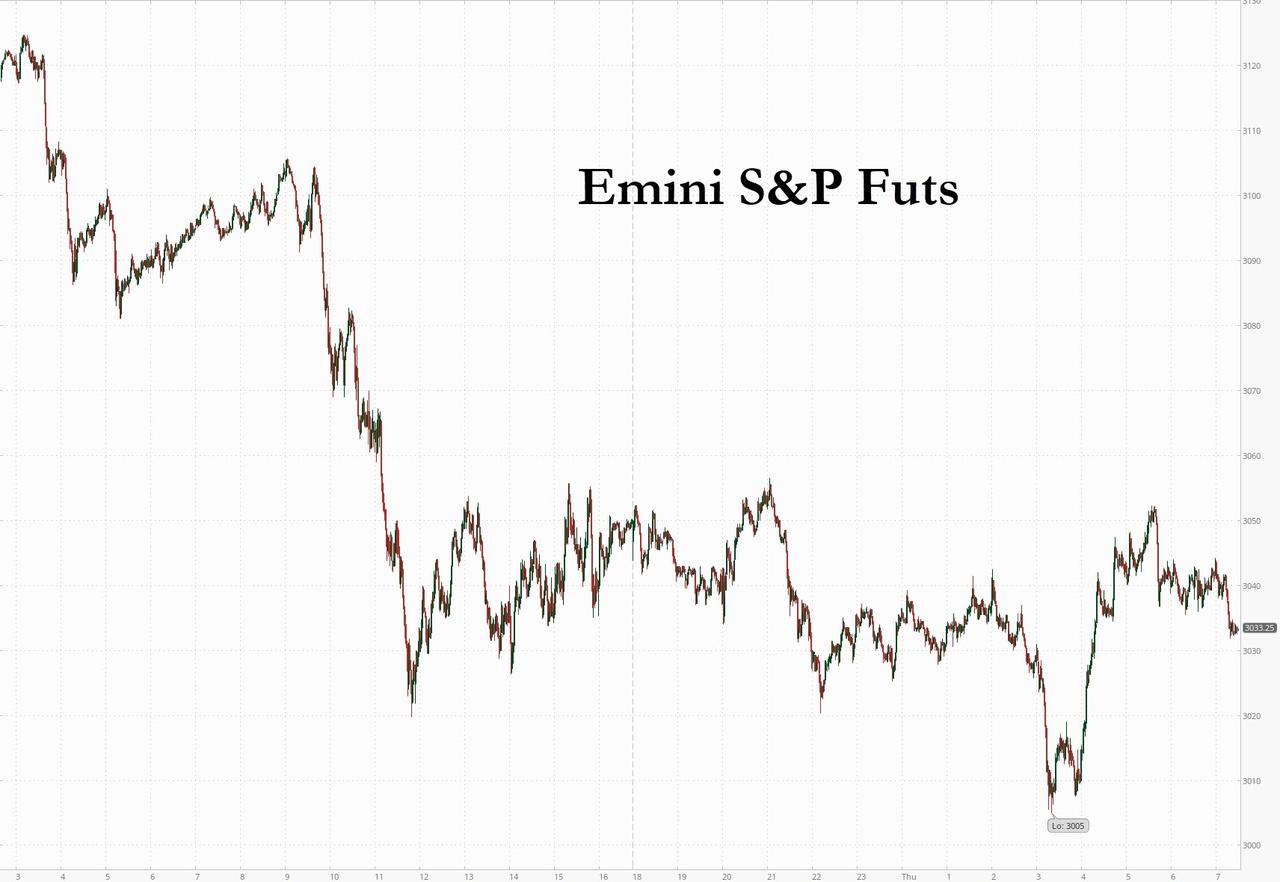

US stock futures fell for a second straight day on Thursday following Wall Street’s worst day in two weeks, as risk appetite took a hit from an alarming rise in new coronavirus cases and on expectations of elevated weekly jobless claims, although futures rebounded from a sharp drop thanks to gains in large-cap tech shares following Europe’s open which dragged down the Emini as low as 3,005 before stabilizing above 3,030. Treasury yields dropped to 0.66% while the dollar rose for a second day.

As has become the norm in recent overnight sessions, Nasdaq 100 futures erased most of an earlier decline. Walt Disney slipped 1.4% in premarket trading after it delayed the reopening of theme parks due to the health crisis. Boeing fell 2.7% as Berenberg reduced its rating to “sell”, noting the planemaker’s near-term risks are elevated due to the COVID-19 pandemic, the pace of recovery in air travel and uncertainty related to production rates.

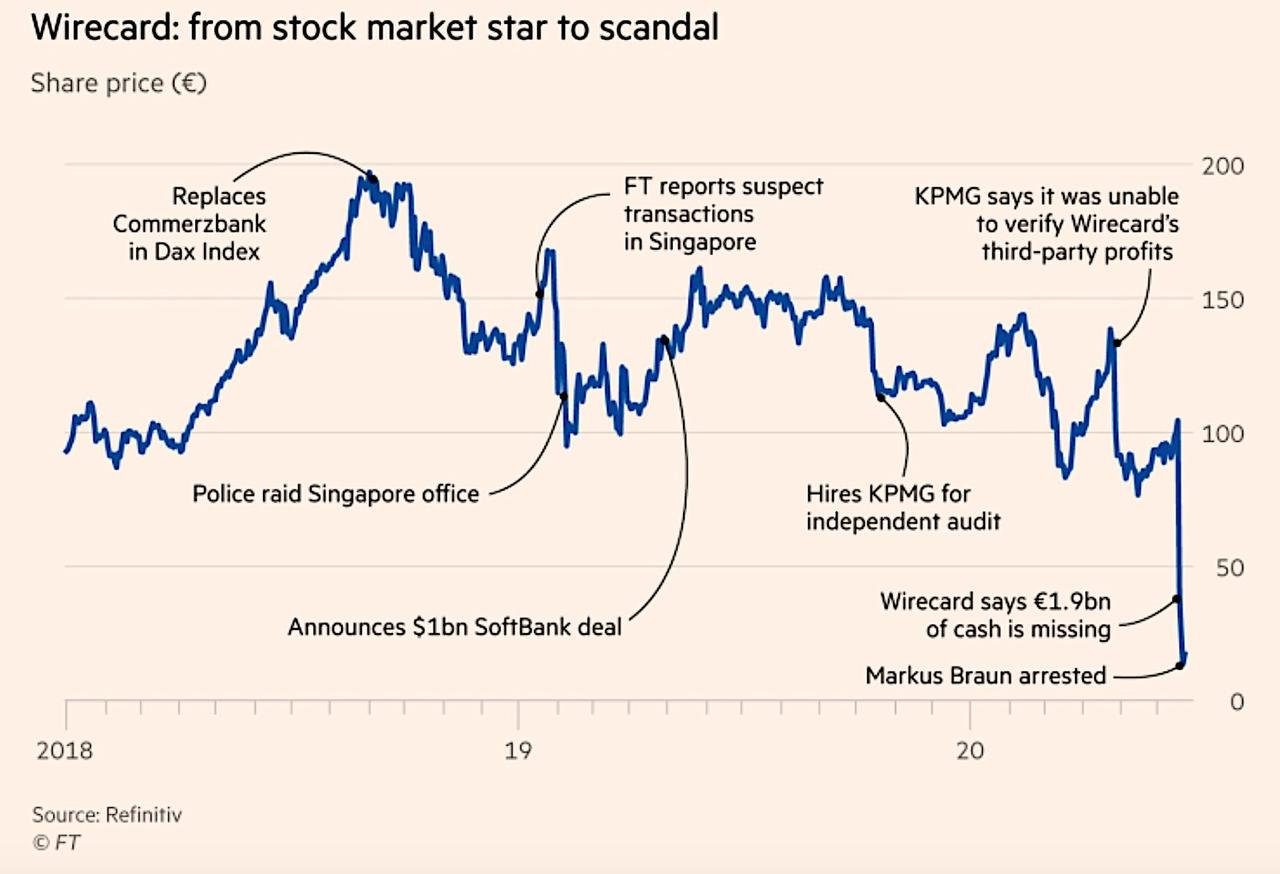

In Europe, stocks swung from a loss to a gain, with Deutsche Lufthansa rallying as its biggest shareholder backed a government rescue package. Meanwhile, the saga of German fintech Wirecard ended with the company filing for insolvency, sending its stock crashing over 80% to all time lows.

Earlier in the session, Asian stocks fell the most in almost two weeks. China and Hong Kong were shut for holidays. Local markets suffered from spillover selling after the weakness seen in global counterparts as risk appetite took a hit from several fronts including the record COVID-19 infection rates in US, half-year end rebalancing which according to JPM is as much as $170BN in selling, and a US-EU tariff threat after reports of US targeting USD 3.1BN of exports from France, Germany, Spain and UK for new tariffs.

Growing fears that lockdowns will be reimposed and economies re-opened more slowly has hurt sentiment, as investors weigh reports of new daily records for infections in Texas, Florida and California. Meanwhile, Bloomberg reports that health leaders called on the U.K. to prepare for a possible second wave, and Australia recorded its largest spike in cases since April.

“The market really got the shivers over the prospect of a big increase in Covid and maybe starting to see places that were opening up have to close up,” Wells Fargo PM Margie Patel said on Bloomberg TV. “We’ve had such a great run from the end of March it’s only inevitable that we should get at least a little step back.”

Besides the pandemic, data due at 8:30 a.m. ET is expected to show about 1.32 million Americans signed up for unemployment benefits in the latest week. Although that figure is down from 1.5 million in the prior week, the pace of declines has slowed as weak demand forces U.S. employers to lay off workers.

In rates, Treasuries were higher led by long end, trimming yields in 20- to 30-year sector lower by nearly 2bp. Price action echoed the wider bull-flattening for the German curve, while gilts outperformed, sending U.K. five-year yields to a record low of minus 0.047% and the curve flattened, after some investors were caught out from bets on a steeper curve following last week’s Bank of England meeting. At the same time, 3M USD Libor rose by over 2bp, a headwind for front-end eurodollar futures. Today the Treasury auction cycle concludes with $41b 7-year note sale at 1pm ET; WI 7- year yield at ~0.51% is ~4bp richer than last month’s result and below April’s record low 0.525%.

In FX, the dollar traded mixed versus Group-of-10 peers after Antipodean and Scandinavian currencies swung from losses to gains as sentiment improved. The kiwi dollar led G-10 gains and outperformed its peer in Australia, where sentiment was hit by a surge in virus cases and job cuts at the national airline.

In commodities, West Texas crude oil fell below $38 a barrel, while gold pared an earlier gain.

Economic data include initial jobless claims, durable goods orders and the third print of first-quarter GDP. Nike is set to report earnings.

Market Snapshot

- S&P 500 futures down 0.4% to 3,036.75

- STOXX Europe 600 up 0.1% to 357.59

- MXAP down 1.1% to 158.82

- MXAPJ down 0.8% to 515.49

- Nikkei down 1.2% to 22,259.79

- Topix down 1.2% to 1,561.85

- Hang Seng Index down 0.5% to 24,781.58

- Shanghai Composite up 0.3% to 2,979.55

- Sensex up 0.2% to 34,933.13

- Australia S&P/ASX 200 down 2.5% to 5,817.68

- Kospi down 2.3% to 2,112.37

- German 10Y yield fell 1.4 bps to -0.454%

- Euro down 0.1% to $1.1238

- Brent Futures down 0.8% to $39.98/bbl

- Italian 10Y yield rose 1.1 bps to 1.14%

- Spanish 10Y yield unchanged at 0.468%

- Brent Futures down 0.8% to $39.98/bbl

- Gold spot up 0.2% to $1,765.37

- U.S. Dollar Index up 0.1% to 97.28

Top Overnight News from Bloomberg

- The U.S. economic recovery is showing incipient signs of weakening in some states where coronavirus cases are mounting. The ebbing is evident in such high-frequency data as OpenTable restaurant reservations and follows a big bounce in activity as businesses reopened from lockdowns meant to check the spread of Covid-19

- Germany’s coronavirus infection rate fell to the lowest in almost three weeks, easing concerns that local outbreaks would prompt a resurgence of the pandemic

- Germany’s constitutional court rejected a separate challenge against the European Central Bank’s 2015 Expanded Asset Purchase Program as inadmissible

- The European Central Bank will set up a precautionary facility to provide euros to central banks outside the currency area to help ease any liquidity stress as a result of the coronavirus pandemic

Asian stocks suffered from spillover selling after the weakness seen in global counterparts as risk appetite took a hit from several fronts including the record COVID-19 infection rates in US, half-year end rebalancing and a US-EU tariff threat after reports of US targeting USD 3.1bln of exports from France, Germany, Spain and UK for new tariffs. ASX 200 (-2.5%) was led lower by underperformance in the energy sector due to lower oil prices and with hefty losses seen in travel stocks after Qantas announced several cost-cutting measures. Nikkei 225 (-1.2%) was pressured by the ill-effects of the predominantly firmer domestic currency and KOSPI (-2.3%) traded downbeat following South Korea’s announcement of a capital gains tax on stock trading from 2023, while trade for the region was also hindered by key holiday closures with mainland China, Hong Kong and Taiwan all closed for the Dragon Boat Festival. Finally, 10yr JGBs were flat as prices failed to take advantage of the risk averse tone, advances in T-notes and with the latest update showing the BoJ’s share of the JGB market increased to 44.2% as of end-March vs 43.7% Q/Q, with participants kept sidelined amid the 20yr auction in which nearly all metrics pointed to a weaker result.

Top Asian News

- Philippines Surprises With Half-Point Rate Cut to Boost Economy

- NTT Buys NEC Stake in Bid for Slice of Global 5G Gear Market

- In Asia, Brands Built on Racist Stereotypes Face Scrutiny

- Pandemic Gives Singapore Air Chance to Grab Emirates India Share

Price action for European stocks has been relatively choppy thus far with downside initially emanating from the soft leads presented by the US and APAC sessions as the COVID-19 case count in certain areas of the US continues to deteriorate. Stocks in Europe were presented some reprieve as the session progressed with not much in the way of standout fundamentals behind the move. Some have attributed part of the move to the ECB announcing a new Eurosystem repo facility to provide euro liquidity to non-euro area central banks, however, stocks were already gaining ahead of this announcement. Note, it is plausible that equities could struggle for direction in the first half of the session until COVID-19 case count data from the US is released mid-afternoon; something which has been a key source of price action over the past few days. From a sectoral standpoint, it is a relatively mixed picture thus far with some cyclical areas such as Autos and banks faring slightly better than peers, whilst the travel & leisure sector is a noteworthy underperformer. Despite stellar gains for Deutsche Lufthansa (+16.5%) following reports that shareholder Thiele (15.5% stake holder) said he will vote for the rescue package in today’s EGM, travel names have taken greater direction from easyJet (-5.6%) after the Co.’s latest earnings update in which the Co. also announced it is to launch a GBP 450mln rights issue. Wirecard (-79%) remain in focus with shares opening lower in the wake of the recent scandal with the latest chapter in the saga seeing the Co. announce it has applied for insolvency proceedings – shares were halted at EUR 10.74 ahead of the announcement before slumping to EUR 2.50 upon resumption. On a more positive footing, albeit of best levels, Bayer (+1.4%) shares have been supported since the get-go after news the Co. will pay up to USD 10.9bln to settle a string of cancer claims linked to the Roundup weedkiller case. Finally, Royal Mail (-8.2%) shares are also seen lower this morning after post a decline in profits to GBP 180mln in the year to March 2020 which has subsequently forced the Co. to lower its headcount by 2,000.

Top European News

- Top Lufthansa Investor Backs $10 Billion Bailout Before Key Vote

- Some of U.K.’s Largest Retailers Withheld Quarterly Rent: Times

- Royal Mail Cuts Management Jobs as Virus Hits Demand

- Swedish Scientist Who Doubted Face Masks Reconsiders Their Use

In FX, the DXY Index holds onto yesterday’s gains above 97.000 but trades in a relatively tight 97.160-404 intraday band thus far as safe-haven demand keeps the broader Dollar propped up amid rising COVID cases across the US and other economies such as Germany, Japan, Australia and China heading into the half-year, quarter and month-end, while participants remain on the lookout for a follow-up to US tariff threat on the EU and UK. Looking ahead, the data-docket sees an abundance in Tier 1 data in the form of Durable Goods, Q1 GDP (F) and Initial Jobless Claims, albeit focus will likely remain on COVID-19 case counts State-side and abroad.

- EUR, GBP – The Single-currency has trimmed losses against the Buck, but more so on USD-dynamics with little reaction seen to the improvement in Gfk consumer sentiment. Meanwhile, reports early-doors noted that the German Constitutional Court has rejected a separate case in regard to the ECB’s asset purchase programme, but details remain vague at the time of writing. This followed reports overnight that the ECB has agreed to provide the Bundesbank with documents on proportionality, as expected. Next up, the ECB’s accounts from the June meeting could provide some meat on the bone over the decision-making process on the PEPP ramp up to 1.35tln from 750bln. EUR/USD meanders around 1.1250 having had printed a current band at 1.225-60 with option expiries seeing a sizeable EUR 1.6bln at strike 1.1200, EUR 805mln at 1.1260 and almost EUR 1bln at 1.1300. Meanwhile, Cable continues to grind higher above its 50 DMA (1.2417), and resides around 1.2450 (ahead of its 10 and 21 DMAs both at 1.2488-89) with little by way of fresh fundamentals ahead of remarks from BoE’s Haldane – who voted against the BoE’s QE ramp up last week. Thus, EUR/GBP trickles lower towards the 0.9000 mark, with short-term support seen around the 0.9014-18 ahead (lows over the last three trading sessions).

- AUD, NZD, CAD – All firmer against the USD, albeit to different degrees with the Kiwi the marked outperformer as it consolidates from its post-RBNZ losses despite a relatively lacklustre May trade balance release overnight. NZD/USD however, remains sub-0.6450 with its 10 DMA at around the psychological level. AUD/USD moves in tandem with the Dollar as price action remains contained within a 30-pip range (0.6848-84), whilst upside technicals see the 100 WMA situated at 0.6909. The Loonie fails to reap the same benefits as its high-beta peers as gains remain somewhat hampered from a sovereign downgrade at Fitch (AA+ from AAA-; outlook Stable). USD/CAD holds onto a 1.3600 handle but resides around session lows (1.3620) amid an attempted recovery in the energy markets.

- JPY – Safe havens trade choppy within tight ranges as the pairs track sentiment and price action in stocks. USD/JPY keeps its 107.00 handle having had dipped below the figure overnight, with its 50 DMA at 107.39.

In fixed Income, core bonds initially began the European session somewhat softer, after a comparatively uneventful overnight session where they were subject to a grinding bid as sentiment remained subdued following yesterday’s stock pullback. Interestingly, even given the strong risk-off trade seen yesterday the UST yield curve only saw modest bull-flattening, with similar price action being seen currently and as such expanding on yesterday’s action; for instance, today’s UST 10yr yield low stands at 0.6630% just below yesterday’s 0.6760% floor. On this, desks have highlighted that US steepeners are, given additional pressures from supply and inflation, seen to be outperforming their European peers ahead; with some option premium measures having surpassed pre-COVID levels – potentially explaining some of the recent magnitude discrepancies. European hours have seen pronounced choppiness across the debt complex, as well as markets more broadly, with initial bond upside derived around the EU equity cash open and just before, but seemingly unrelated to, reports the GCC have rejected a separate case regarding ECB QE; note, details on this headline are still very vague and on the subject attention is on today’s ECB minutes. Nonetheless, at the time Bunds sharply retreated and BTPs saw a firm bid; albeit, both moves were within session ranges failing to test the sessions low/high of 176.09 and 143.80 respectively and ultimately pared back. Since then, while debt has been subject to periods of choppiness as sentiment in general struggles to find direction, we are overall marginally firmer on the day for core counterparts but seemingly capped by the session’s ranges. In terms of focus for the session ahead, we do have the aforementioned ECB minutes alongside a number of central bank speakers and US data – but focus will likely remain on the COVID-19 count and particularly updates from the key US states of Florida, NY and Texas.

In commodities, choppy trade in the crude complex as price action is predominently dicatated by market sentiment in which the downbeat APAC session saw WTI and Brent August contracts relinquish the USD 38/bbl and USD 40/bbl level respectively. However, amid an improvement in broader sentiment as European trade is underway, the benchmarks have rebounded off lows of USD 37.13/bbl and USD 39.50/bbl respectively, with the latter reclaiming USD 40/bbl to the upside. News-flow has been light for the complex but price action is likely to be influenced by COVID-19 developments ahead of Tier 1 US data. Elsewhere, spot gold remains relatively steady around USD 1765/oz within today’s range despite the whipsaws seen cross-market, with initiall impetus derived as European players entered the markets to a softer APAC session. Copper trades with modest gains as the red metal retraced earlier downside amid a recovery in stocks, but price action remains contained within recent ranges.

US Event Calendar

- 8:30am: GDP Annualized QoQ, est. -5.0%, prior -5.0%; Core PCE QoQ, est. 1.6%, prior 1.6%

- 8:30am: Personal Consumption, est. -6.8%, prior -6.8%

- 8:30am: Advance Goods Trade Balance, est. $68.1b deficit, prior $69.7b deficit

- 8:30am: Retail Inventories MoM, est. -2.8%, prior -3.6%; Wholesale Inventories MoM, est. 0.4%, prior 0.3%

- 8:30am: Durable Goods Orders, est. 10.45%, prior -17.7%; Durables Ex Transportation, est. 2.1%, prior -7.7%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 1.0%, prior -6.1%; Cap Goods Ship Nondef Ex Air, est. -1.0%, prior -5.7%

- 8:30am: Initial Jobless Claims, est. 1.32m, prior 1.51m; Continuing Claims, est. 20m, prior 20.5m

- 11am: Kansas City Fed Manf. Activity, est. -3, prior -19

DB’s Jim Reid concludes the overnight wrap

I’ve got the rest of the day off today as the golf course I’m a member of opposite my house is hosting a charity pro-am. So I’ll be playing with a touring pro and they’ll be competing for a healthy prize. So the big question on everyone’s lips at the golf club last night as I went to the range to try to limit my embarrassment today was who they’ll be playing with. Yes the pros were all wondering which of them will be playing with the author of the EMR. Lucky them. Sky Sports News have their cameras here at Worplesdon all day so there’s the outside chance you’ll see my dodgy swing on the bulletins. Without much live sport at the moment they have a lot of airtime to fill. I’ll have mixed feelings if Liverpool win the league tonight for the first time in 30 years and it bumps my pro-am appearance off the sports news.

The business channels have had no such problems filling air time over the last few months and they will again have plenty to discuss today. A plethora of bad news about the virus led to a major sell-off in risk assets yesterday as volatility returned to financial markets once again. It wasn’t a single bad headline that led to the plunge, but a drip-feed of negative stories that all combined to show increasing signs of a deteriorating situation on the virus, most obviously in the US. In terms of the news there, Florida (the 3rd most populous US state) saw its number of Covid-19 cases rise by 5.3% yesterday, some way above the previous 7-day average of 3.7%, and the number of hospitalisations rose by 256 in the state, the largest increase in a month. California also saw a record jump in cases, with over 8800 new ones yesterday. This equated to a 4.8% rise – notably above the 2.5% average daily rise over the last week. Covid-19 ICU cases have risen 18% in the last 2 weeks according to the state, but the rate of fatalities has thankfully not picked up in recent days. This could be still to come, but perhaps it is a sign that hospitals have gotten better at treating the virus now that we are further into the pandemic and maybe that the average age of new cases has fallen. In the pdf today (click “view report”) we show graphs of 7 day rolling cases against 7 day rolling fatalities with a lag of 7 days for the 4 troubled US states and also the US overall, alongside NY and Germany. These last three are included to show the correlation earlier in this pandemic and how it might be changing. We say might because the graphs show we’re at a critical point where fatalities should be going up. However there is evidence from the US overall and the four states that this isn’t happening to the same degree it did in other parts of the world in March and early April. An important few days ahead then. Note that the pdf also includes the usual case and fatality tables.

Meanwhile, in what represents a notable reversal from earlier in the pandemic, the three states of New York, New Jersey and Connecticut are going to order visitors coming from virus hotspots to quarantine for 14 days. Texas was one of the states that originally ordered those restrictions on Northeastern states. And yet yesterday the 2nd most populous state in the US had news come through from Houston that intensive-care units were currently at 97% capacity and are likely to exceed tomorrow. With the state as a whole right up to its limit of ICU beds, Texas Medical Center is currently projecting that they will access their surge capacity starting this week. They are also likely to surpass that capacity (887 surge ICU beds) in about two weeks if current virus trends continue. The rise in Texan cases yesterday was followed by headlines that Apple was moving to close seven stores in the Houston area, with 18 stores now closed nationwide following their reopening. Overall the US saw cases rise by 1.6%, above the 1.3% average daily rise over the last week, while the number of new cases per week is now approaching the highs of the pandemic. See our US economists piece last night (link here) that suggests states with faster case growth are now underperforming economically based on measures of small business activity, restaurant bookings and consumer spending particularly in the southern states already mentioned.

Looking at the market reaction, these revived concerns about the virus saw equity markets lose substantial ground yesterday, a move that more than erased Tuesday’s gains. Looking at the major indices, the S&P 500 was down -2.59% (-3.17% at the intra-day lows), with energy stocks leading the decline on the back of plunging oil prices. It was the worst daily performance for the index since June 11th (-5.89%) and the second worst since May 1st (-2.81%). Elsewhere the NASDAQ snapped a run of 8 successive gains to fall by -2.19%, down from its fresh record the previous day. Over in Europe the picture was somewhat worse with all the major indices closing at their lows of the day and missing the small bounce that US assets saw late in their session. The STOXX 600 was down -2.78% as energy similarly led the declines with the DAX (-3.43%), CAC 40 (-2.92%) and the FTSE 100 (-3.11%) also falling back. The selloff in Europe and the US was incredibly broad with only about 3.5% of stocks in each of the S&P 500 and STOXX 600 up on the day.

While the moves haven’t been quite as severe, Asian markets are lower this morning too with the Nikkei (-1.23%), Kospi (-1.82%) and ASX (-1.62%) all down. Markets in Hong Kong and China are closed for a holiday. In FX, the US dollar index is up another +0.18% building up on yesterday’s gains. Yields on 10y USTs are down a further -1bp overnight to 0.670% while futures on the S&P 500 are down -0.52%.

In overnight news, the Pentagon has put up a list of 20 Chinese companies that it says are owned or controlled by China’s military, opening them up to potential additional US sanctions. The list includes Huawei Technologies Co. and Hangzhou Hikvision Digital Technology Co. amongst others.

In terms of those other moves yesterday, oil lost ground as mentioned earlier with Brent crude down -5.44% to $40.31/bbl. Unsurprisingly, oil-producing currencies underperformed in response, as both the Norwegian krone (-1.53% vs. USD) and the Russian ruble (-1.03%) weakened. The US dollar had a fairly strong performance however, up +0.52% in its best day in over a week. Over in fixed income, sovereign bond markets see-sawed as they oscillated between gains and losses through the session. By the close, core bond yields had moved lower, with those on 10yr Treasuries and bunds down -3.3bps and -3.2bps respectively. BTPs underperformed however, coming off their nearly 3-month lows with a +1.1bps increase.

Staying with Europe, this week our Economist team published a report titled ‘Bank credit, economic growth and the COVID shock: an adjusted perspective’ . Watch a new video with Mark Wall, Chief Economist, EMEA (link here to the video and report) where he explains that the focus of the note is on bank credit in the euro area – on its surprising, and misleading, strength during the COVID shock and where it is likely to go next.

Keeping on the economic theme, the mood was dampened further yesterday by updated forecasts from the IMF, who downgraded their outlook for the global economy compared with their April forecasts. They now see the world economy undergoing a -4.9% contraction this year (vs. -3.0% previously), before growing by +5.4% in 2021 (vs. +5.8% previously). The downgrades were seen in both advanced as well as emerging market and developing economies, while their projections for the volume of global trade sees a decline of -11.9% this year.

In other news, with just over 4 months to go now until the US election, a New York Times/Siena College poll out yesterday gave Joe Biden a 50%-36% advantage over President Trump. This is but the latest in a pattern evident for some weeks now of a widening lead for Biden. FiveThirtyEight’s polling average now puts him +9.3% ahead of Trump. This has been reflected on the betting and prediction markets too, with Biden now the favourite there as well. It’s also worth noting that Trump’s approval rating at this point in his term is below that of his 3 immediate predecessors who went on to win re-election.

Staying on politics, and yesterday we had a statement from the Elysee that President Macron and Chancellor Merkel would be meeting on Monday, with the EU budget and the recovery fund on the agenda. Remember that this comes ahead of another EU leader’s summit on the 17-18th July, where the 27 leaders will meet in person in Brussels to hold further discussions on the recovery fund. That said, there’s still substantial differences between the different member states on this, particularly with the so-called Frugal Four, and any final agreement will require unanimity between the member states. On a side note however, Euro Area inflation expectations rose to their highest level since early March yesterday, with five-year forward five-year inflation swaps closing above 1.10% for the first time since then.

Looking at yesterday’s data releases, the main highlight was the Ifo business climate indicator from Germany, which rose to 86.2 in June (vs. 85.0 expected), up from a revised 79.7 in May. Nevertheless, this is still some way from the 95.9 reading in February before the economic impact of the pandemic hit. Otherwise, the FHFA US house price index rose by +0.2% in April (vs. +0.3% expected).

To the day ahead now, and data releases include the weekly initial jobless claims data from the US, as well as the third reading of Q1 GDP. In addition, there’ll be the preliminary data on durable goods orders and wholesale inventories for May. From central banks, the ECB will be releasing the account of their June monetary policy meeting, and speakers include the ECB’s Schnabel, Mersch and Knot, the Fed’s Bostic and Kaplan, along with the BoE’s Haldane. There’ll also be monetary policy decisions from central banks in Turkey and Mexico.

via ZeroHedge News https://ift.tt/2YwdhFT Tyler Durden