‘Alice In Wonderland’ Stock Market Gain Expectations Now Up To 17.5% Annually

Authored by Mike Shedlock via MishTalk.com,

Investors appear to be growing more and more optimistic about how their portfolios will perform in the years to come. Disappointment is bound to follow…

The image (plus my comment about a bone) and the lead comment are from the WSK article When a 59% Annual Return Just Isn’t Enough

Let’s compare investor expectations in the WSJ to John Hussman’s latest expectations starting with some snips from the Journal.

In a recent survey of 750 U.S. individual investors, Natixis Investment Managers found these people expect to earn 17.3% this year, after inflation.

That might not sound like pie in the sky. The S&P 500 returned 18.4% last year, counting dividends, and is up 15.9% so far in 2021. Recent past returns always mold future expectations.

Over the long run, however, the people in the Natixis survey anticipate earning an average of 17.5% annually, after inflation—even higher than for this year. That’s up from the 10.9% long-term return they expected in 2019, the previous round of the survey.

It’s also more than twice the return on U.S. stocks since 1926, which has averaged 7.1% annually after inflation.

I asked Wharton Research Data Services, which analyzes business and investing information, to rank all U.S. stocks and exchange-traded funds over the last 10 years.

WRDS counted 3,790 stocks and ETFs that traded continuously over the 10 years that ended May 31, 2021. Only 14% earned total returns that exceeded 17.5% annually. Fully 22% earned negative returns.

In short, investors were more likely to lose money than to compound it by at least 17.5% a year.

It’s the Starting Point Stupid!

Author Jason Zweig hits the right idea with his final assessment at the end of the article:

From today’s levels of interest rates and stock prices, I’d be thrilled if stocks returned at least 4% annually over the next decade or two after inflation. I’d also be surprised.

Alice’s Adventures in Equilibrium

With that, let’s take a look at John P. Hussman’s latest assessment in Alice’s Adventures in Equilibrium.

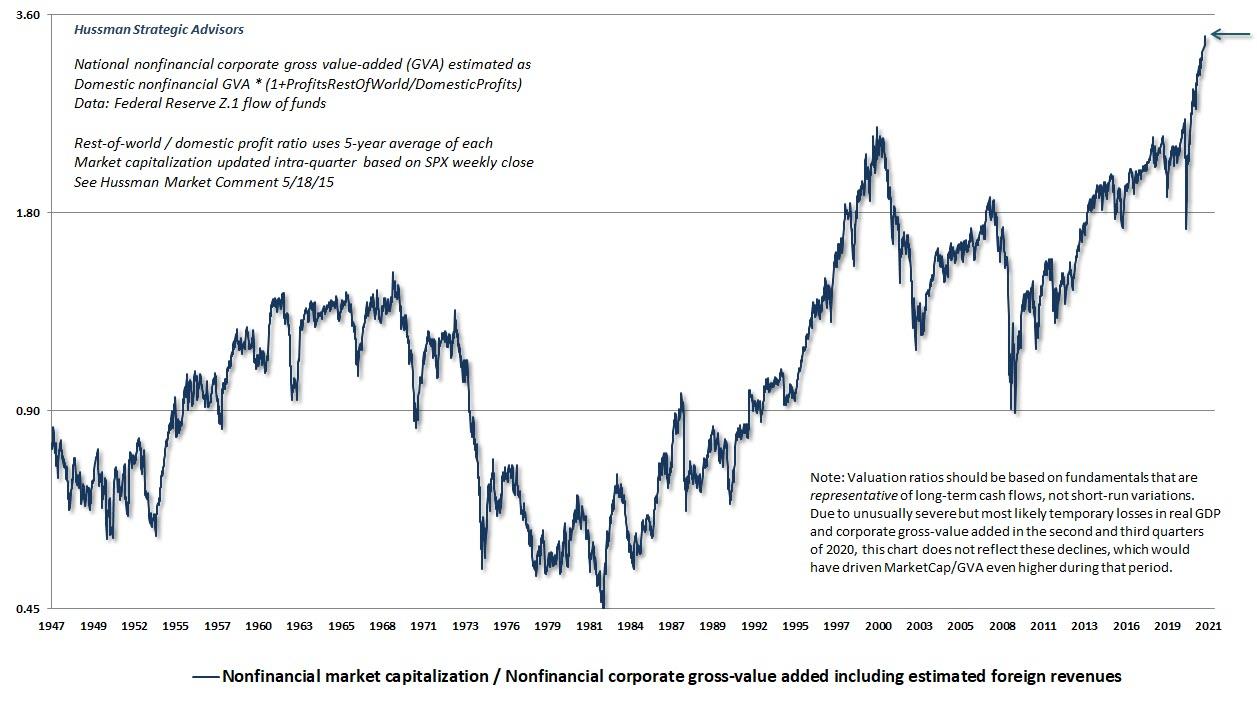

The chart below shows the ratio of nonfinancial market capitalization to corporate gross value-added, including estimated foreign revenues. This is the valuation measure that we find best-correlated with actual subsequent market returns across a century of market cycles, as well as in recent decades.

Nonfinancial Market Capitalization

Presently, we estimate clearly negative average annual total returns for the S&P 500 over the coming 12-year period. The scatter below reflects two of our most reliable valuation measures: nonfinancial market capitalization to corporate gross value-added (including estimated foreign revenues) in data since 1950. I’ve extended the chart back to 1928 by setting valuations in proportion to our margin-adjusted P/E (MAPE) in data prior to 1950. The valuation of the U.S. stock market on June 11, 2021 was easily the highest level in history. [Mish Comment: It’s even higher now.]

Expected 12-Year Annualized Returns

It’s important to recognize that while valuations are extremely informative about prospective market returns on a 10-12 year horizon, and potential market losses over the completion of any market cycle, valuations are not reliable short-term measures. If elevated valuations were enough to drive the market lower, we could never observe the sort of extremes that emerged in 1929, 2000 and today. Over shorter horizons, we have to attend to whether investors are inclined toward speculation or risk-aversion, and we find that this psychology is best gauged by the uniformity or divergence of market internals across thousands of individual stocks, industries, sectors, and security-types, including debt securities of varying creditworthiness.

Widest Difference of Opinion in History

-

People in the Natixis survey anticipate earning an average of 17.5% annually, after inflation.

-

Hussman expects deeply negative returns for a full 12 years, about -5% annually if I interpret the arrow on his chart correctly.

Expectations Gap

I believe this is the widest long-term expectations gap in history but I cannot prove it.

Regardless, it is immense.

Not only do investors fail to take current conditions into consideration, they have extrapolated them the wrong way far into the future.

It’s important to note that is how we got here in the first place.

* * *

Like these reports? I hope so, and if you do, please Subscribe to MishTalk Email Alerts.

Tyler Durden

Mon, 07/05/2021 – 06:00

via ZeroHedge News https://ift.tt/3ADv3bF Tyler Durden