Goldman’s Top 13 Charts For The Month Of August

The start of a new month means that Goldman’s flow traders need a new set of exciting ideas and trades to dangle before their clients, and that’s just what Goldman traders Scott Rubner, Matthew Fleury, Matthieu Martal , Kavita Vaja, and Jonas Bovbjerg are doing by putting together the following 13 charts that capture some of the best ideas and trade recos emerging from the world’s most powerful trading desk.

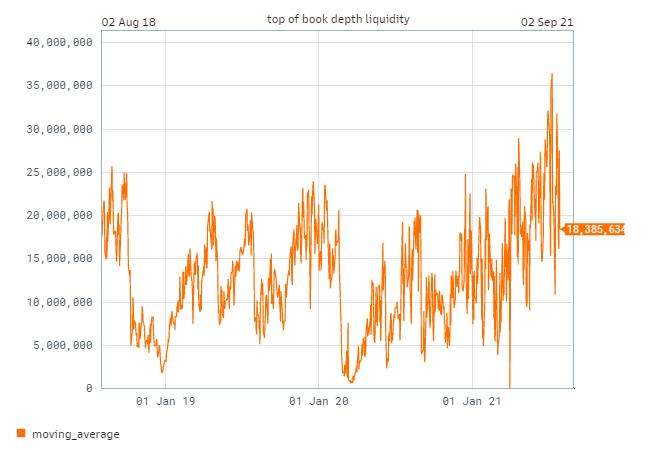

1. “If you are a stock picker watching earnings prints you are likely fully engaged this week. This week will be peak liquidity for the rest of the summer. Vacation or extended vacation schedules officially kick off next week after earnings season. As we sit right now. Liquidity is at the highs into a busy week”

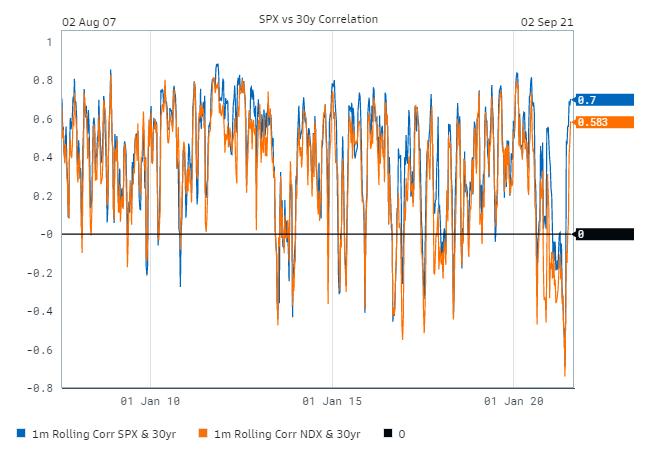

2. “I think equities would be fine with higher yields – the negative correlation of SPX & NDX with the 30yr has turned positive again. Higher yields are much less of a problem than they were earlier this year”

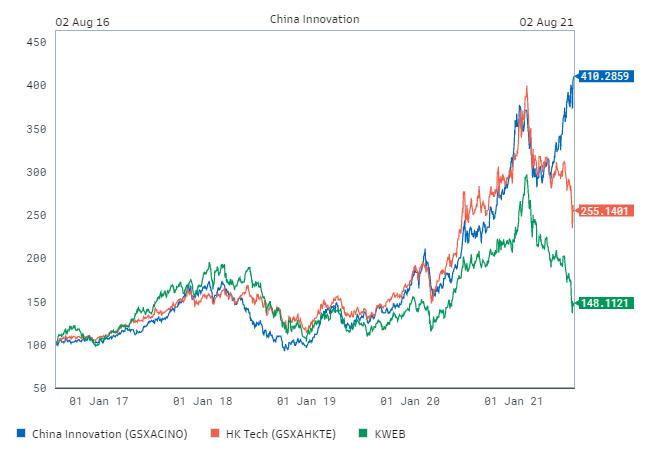

3. “China Regulation: As the regulatory pressure on China’s leading offshore internet & education firms has increased in recent weeks, tech hardware companies listed onshore have outperformed the Chinese market. With the broader Chinese economy still in a growth phase (with Chinese equities historically displaying 22% return over 15months, entirely driven by earnings re-rating), and earnings revisions outside of the internet sector higher year to date (MSCI China ex Internet EPS up +5% vs China Internet EPS down -22% YTD), this basket is designed to benefit from the expansion of China’s high tech manufacturing capabilities. For the first time in 5 years we have seen a meaningful divergence between HK and China listed Tech. ADRs have consistently underperformed.”

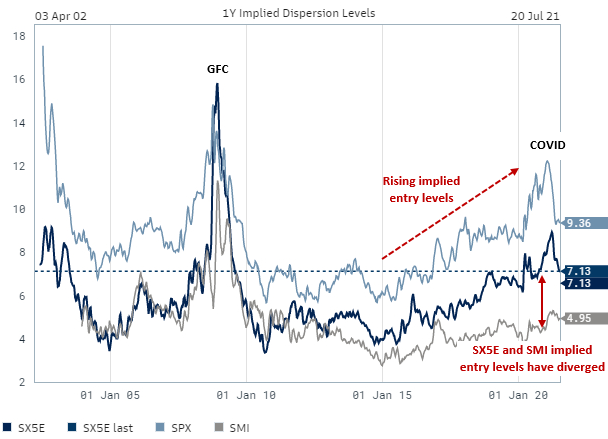

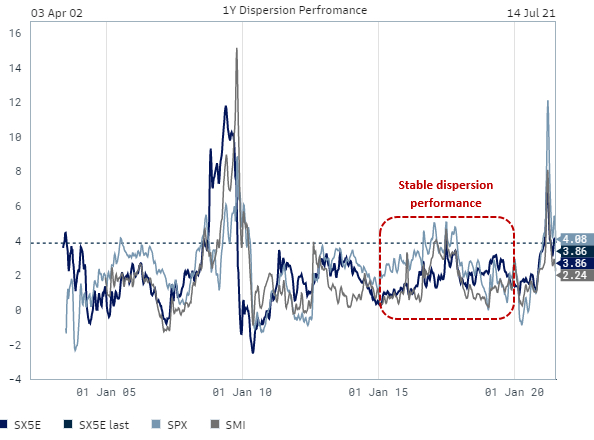

4. Implied dispersion levels have structurally reset higher over the past 5Y in Europe & US.

5. Dispersion performance has been stable due to rising realized levels over the same period

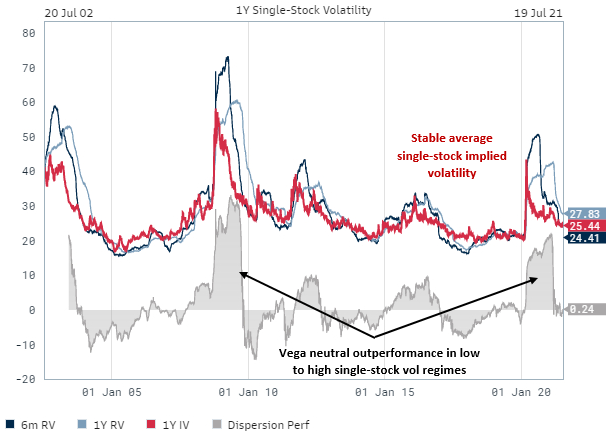

6. SX5E 1Y Vega neutral dispersion offered defensives properties in GFC & COVID due to realized volatility spikes.

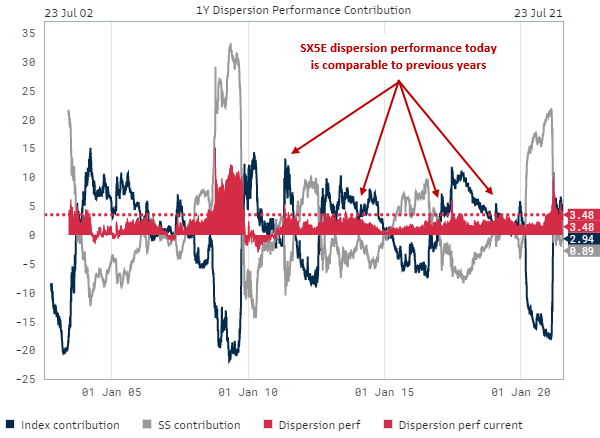

7. Index implied volatility has reset sharply lower pre- and post-COVID, which has contributed to rising implied entry levels for dispersion. However, the compression of index realized volatility since the US elections has maintained stable dispersion performance from the index leg. SX5E 1Y Dispersion performance has been stable due to contribution from both index and single-stock legs.

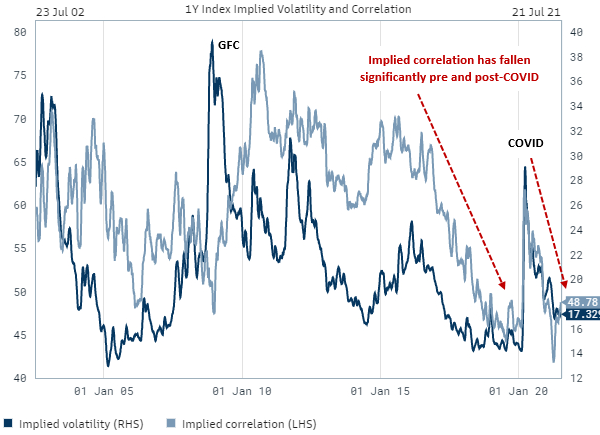

8. The fall in index implied volatility in recent years can be partly explained by the sharp fall in index implied correlation levels as well as falling demand for upside call options in European equities. Market-implied average single-stock correlation shows that whilst index implied volatility has fallen since 2015 and again post-COVID, driving the implied dispersion entry level higher, this has coincided with a sharp fall in implied correlation levels over the same period. Therefore, dispersion strategies which sell expensive implied correlation have continued to perform well despite higher implied dispersion entry levels. SX5E 1Y implied correlation has fallen more than index implied volatility levels.

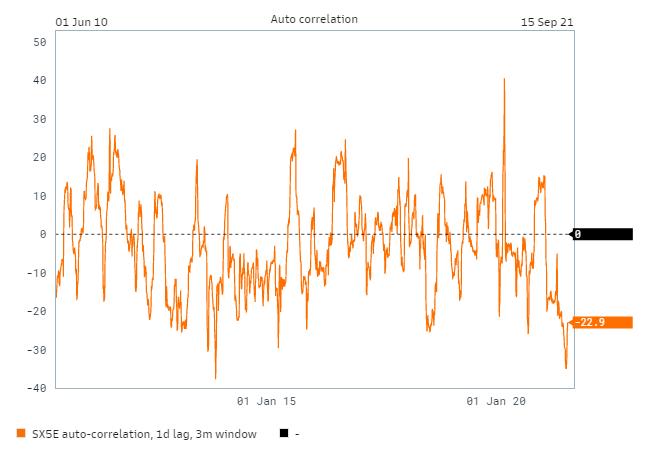

9. Correlation of returns on t vs t-1 is deeply negative in SX5E

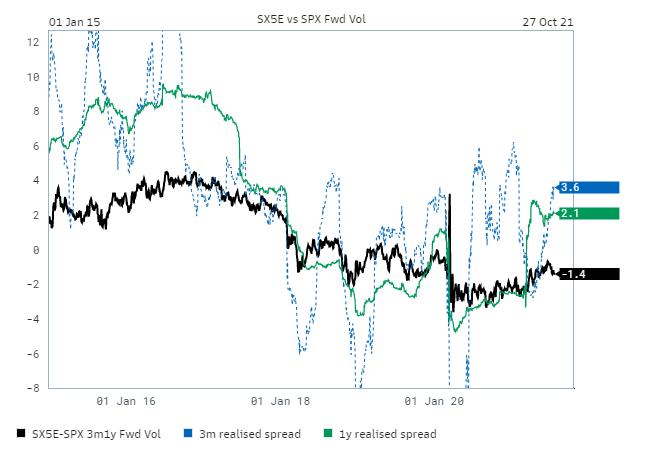

10. Despite the spread trading off the lower values during the post-Mar20 period, it remains at historical lows (18th percentile vs. past 5y). The recent pick up in realized spread should support the forward vol level as we roll into the spot spread. Term-structure roll is favorable due to the steepness of the SPX term structure (~0.5v positive carry over the next 3m, everything else remaining equal). The spot spread gets delivered in December at extreme lows, >3v below current 6m realized.

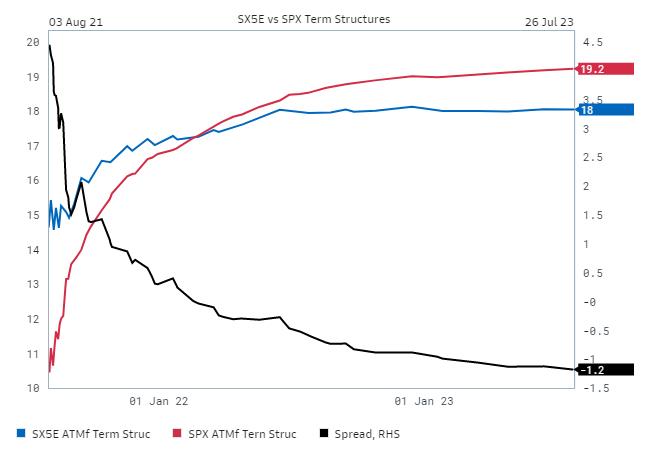

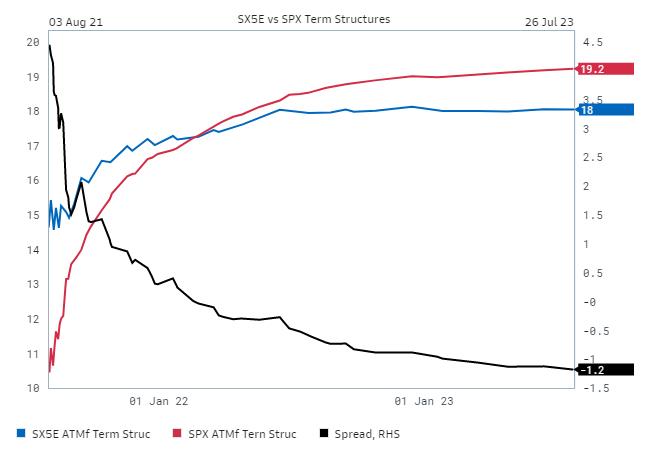

11. Significant roll-up in the SX5E-SPX spread

12. Realized correlation between broader market vs. Momentum vs. EU Cyclicals/Defensives

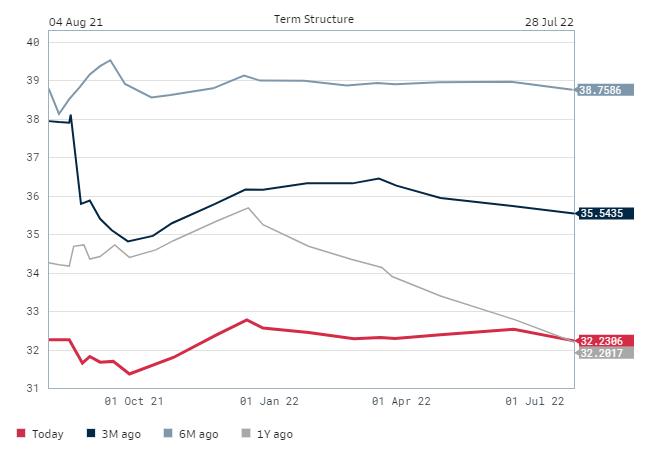

13. VOW3 term structure has materially flattened over the past year (red vs. grey), driven by a combination of call overwriting in the front-end and more recently, long-dated upside options buyers. Implied volatility has also recently reset lower across the curve (red vs. navy) and the skew is flat/call skew is inverted. Therefore, consider owning long-dated upside call spreads which offer a high max. payout ratio (chart 4, navy) where you sell a call 3v higher (grey) than where you buy a call.

Tyler Durden

Wed, 08/04/2021 – 21:40

via ZeroHedge News https://ift.tt/2WXpmWz Tyler Durden