Key Events This Week: Payrolls, ISM, Home Prices And Fed Speakers Galore

As we head into December this week, there’s an incredibly eventful period ahead on the market calendar even outside of Omicron.

As DB’s Jim Reid notes, we have payrolls on Friday which could still have a big impact on what the Fed do at their important December 15 FOMC and especially on whether they accelerate the taper. Wednesday (Manufacturing) and Friday (Services) see the latest global PMIs which will as ever be closely watched even if people will suggest that the latest virus surge and now Omicron variant may make it backward looking.

Looking at payrolls, hiring momentum likely continued in November with nonfarm and private payroll growth of 450k, pushing the unemployment rate down to 4.4% from 4.6%. Look for strong wage growth of 0.4% mom. All eyes on the trend in the labor force part rate. November ISM surveys should point to ongoing robust activity in the broad economy, with the manufacturing index at 61.0 and services even higher at 67.5.

Elsewhere in the Euro Area, we’ll get the flash CPI estimate for November tomorrow (France and Italy on the same day with Germany today), and we’ll hear from Fed Chair Powell as he testifies (with Mrs Yellen) before congressional committees tomorrow and Wednesday.

There’s lots of other Fed speakers this week (ahead of their blackout from this coming weekend) and last week there was a definite shift towards a faster taper bias, even amongst the doves on the committee with Daly being the most important potential convert. Fed speakers this week might though have to balance the emergence of the new variant with the obvious point that without it the Fed is a fair bit behind the curve.

Importantly but lurking in the background, Friday is also the US funding deadline before another government shutdown. History would suggest a tense last minute deal but it’s tough to predict.

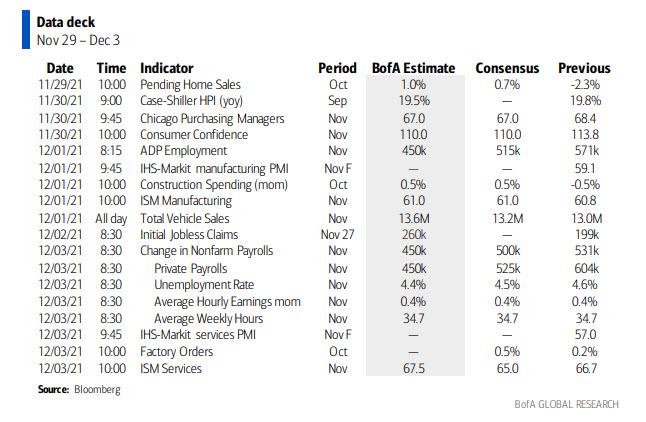

Courtesy of Deutsche Bank, here is a day-by-day calendar of events

Monday November 29

- Data: UK October mortgage approvals, Euro Area final November consumer confidence, Germany preliminary November CPI, US October pending home sales, November Dallas Fed manufacturing activity, Japan October jobless rate (23:30 UK time), preliminary October industrial production (23:50 UK time)

- Central Banks: Fed Chair Powell, Fed’s Williams, Bowman, ECB’s Villeroy, Centeno speak

Tuesday November 30

- Data: China November manufacturing PMI, non-manufacturing PMI, composite PMI, Japan October housing starts, France and Italy preliminary November CPI, Germany November unemployment change, Euro Area flash November CPI estimate, Canada Q3 GDP, US September FHFA house price index, November MNI Chicago PMI, Conference Board consumer confidence

- Central Banks: Fed Chair Powell, Vice Chair Clarida, Fed’s Williams, ECB’s Villeroy and BoE’s Mann speak

Wednesday December 1

- Data: November manufacturing PMIs from South Korea, Indonesia, China, India, Russia, Turkey, Italy, France, Germany, South Africa, Euro Area, UK, Brazil, Canada, US and Mexico, US November ADP employment change, ISM manufacturing

- Central Banks: Fed Chair Powell and BoE Governor Bailey speak, Fed releases Beige Book

- Other: OECD publishes Economic Outlook

Thursday December 2

- Data: Euro Area October PPI, unemployment rate, Italy October unemployment rate, US weekly initial jobless claims

- Central Banks: Fed’s Quarles, Bostic, Daly and Barkin speak

Friday December 3

- Data: November services and composite PMIs from Japan, China, India, Russia, Italy, France, Germany, Euro Area, UK, Brazil and US, France October industrial production, Euro Area October retail sales, US November change in nonfarm payrolls, unemployment rate, ISM services index, October factory orders, final October durable goods orders, core capital goods orders

- Central Banks: Fed’s Bullard speaks

- Other: US deadline to avoid government shutdown (as it stands)

Finally, looking at just the US, the key economic data releases this week are the ISM manufacturing report on Wednesday, and the employment report on Friday. There are several speaking engagements from Fed officials this week, and Chair Powell will provide remarks on Monday and congressional testimony on Tuesday and Wednesday.

Monday, November 29

- 10:00 AM Pending home sales, October (GS +1.0%, consensus +0.8%, last -2.3%): We estimate that pending home sales increased 1.0% in October.

- 10:30 AM Dallas Fed manufacturing index, November (consensus 19.0, last 14.6): 03:00 PM Fed Chair Powell (FOMC voter) and New York Fed President Williams (FOMC voter) speak

- 3:00 PM: Fed Chair Jerome Powell and New York Fed President John Williams will speak at the launch of the New York Innovation Center, a partnership between the New York Fed and the Bank for International Settlements’ Innovation Hub. Prepared text is expected.

- 05:05 PM Fed Governor Bowman (FOMC voter) speaks: Fed Governor Michelle Bowman will discuss central banking and indigenous economies at a conference hosted by the Bank of Canada and the Reserve Bank of New Zealand. Prepared text and moderated Q&A are expected.

Tuesday, November 30

- 09:00 AM FHFA house price index, September (consensus +1.2%, last +1.0%)

- 09:00 AM S&P/Case-Shiller 20-city home price index, September (GS +1.1%, consensus +1.25%, last +1.17%): We estimate the S&P/Case-Shiller 20-city home price index rose by 1.1% in September, following a 1.17% increase in August.

- 09:45 AM Chicago PMI, November (GS 68.4, consensus 67.0, last 68.4): We estimate that the Chicago PMI was unchanged at an elevated level of 68.4 in November. Our forecast reflects strong manufacturing surveys and improving auto production.

- 10:00 AM Conference Board consumer confidence, November (GS 113.0, consensus 110.7, last 113.8): We estimate that the Conference Board consumer confidence index decreased by 0.8pt to 113.0 in November. Our forecast reflects mixed signals from other consumer confidence measures.

- 10:00 AM Fed Chair Powell (FOMC voter) speaks: Fed Chair Jerome Powell and Treasury Secretary Janet Yellen will appear before a Senate Banking Committee oversight hearing on the CARES Act. Prepared text and Q&A are expected.

- 10:30 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will deliver opening remarks at a New York Fed event on food insecurity. Prepared text is expected.

- 01:00 PM Fed Vice Chair Clarida (FOMC voter) and Cleveland Fed President Mester (FOMC non-voter) speak: Fed Vice Chair Richard Clarida and Cleveland Fed President Loretta Mester will discuss the Fed’s independence at an event hosted by the Cleveland Fed. Prepared text and moderated Q&A are expected.

Wednesday, December 1

- 08:15 AM ADP employment report, November (GS +500k, consensus +525k, last +571k): We expect a 500k rise in ADP payroll employment for the month of November. Our forecast assumes strong underlying job gains and reflects the mixed statistical inputs to the ADP model this month.

- 09:45 AM Markit US manufacturing PMI, November final (consensus 59.1, last 59.1)

- 10:00 AM Construction spending, October (GS +0.2%, consensus +0.4%, last -0.5%): We estimate a 0.2% increase in construction spending in October.

- 10:00 AM ISM manufacturing index, November (GS 61.4, consensus 61.1, last 60.8): We estimate that the ISM manufacturing index rose 0.6pt to 61.4 in November, reflecting improving conditions in the automotive sector, favorable seasonality, and net increases in other business surveys (GS manufacturing tracker +1.0pt to 60.9).

- 10:00 AM Fed Chair Powell (FOMC voter) speaks: Fed Chair Jerome Powell and Treasury Secretary Janet Yellen will appear before a House Financial Services Committee oversight hearing on the CARES Act. Prepared text and Q&A are expected.

- 02:00 PM Beige Book: The Fed’s Beige Book is a summary of regional economic anecdotes from the 12 Federal Reserve districts. In this Beige Book, we look for anecdotes related to growth, the labor market, wage growth, price inflation, and supply chain disruptions.

- 5:00 PM Wards Total Vehicle Sales, November (GS 13.5m, consensus 13.35m, last 12.99m)

Thursday, December 2

- 08:30 AM Initial jobless claims, week ended November 27 (GS 240k, consensus 250k, last 199k): Continuing jobless claims, week ended November 20 (consensus 2,000k, last 2,049k): We estimate initial jobless claims increased to 240k in the week ended November 27.

- 08:30 AM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will discuss US housing costs at a virtual conference co-hosted by the Atlanta and Dallas Feds. Audience Q&A is expected.

- 11:00 AM Fed Governor Quarles (FOMC voter) speaks: Fed Governor Randal Quarles will give a speech at the American Enterprise Institute. Prepared text and Q&A are expected.

- 11:30 AM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will take part in a virtual discussion hosted by Reuters.

- 11:30 AM San Francisco Fed President Daly (FOMC voter) and Richmond Fed President Barkin (FOMC voter) speak: San Francisco Fed President Mary Daly and Richmond Fed President Thomas Barkin will speak at a virtual fireside chat at the Peterson Institute for International Economics.

Friday, December 3

- 08:30 AM Nonfarm payroll employment, November (GS +550k, consensus +535k, last +531k); Private payroll employment, November (GS +550k, consensus +525k, last +604k); Average hourly earnings (mom), November (GS +0.5%, consensus +0.4%, last +0.4%); Average hourly earnings (yoy), November (GS +5.1%, consensus +5.0%, last +4.9%); Unemployment rate, November (GS 4.5%, consensus 4.5%, last 4.6%): We estimate nonfarm payrolls rose 550k in November (mom sa). This report reflects the second full month of hiring following the expiration of federal enhanced unemployment benefits, and with labor demand remaining strong, we expect a similar pace of job growth as in October. We also expect second-derivative improvement in education categories, as we believe the 170k drop over the previous two months reflected janitors and support staff not returning for the new school year. But while dining activity continued to gradually normalize and jobless claims fell further, Big Data employment indicators were mixed in the month. We also note the possibility that labor supply constraints weighed on pre-holiday hiring in the retail industry. Finally, we believe upward revisions to prior-month nonfarm payrolls are more likely than not.

- We estimate a one-tenth drop in the unemployment rate to 4.5%, reflecting a strong household employment gain but a likely rebound in the labor force participation rate—the latter driven by expiring benefits, improving public health, and the easing of childcare constraints. We estimate a 0.5% rise in average hourly earnings (mom sa) that boosts the year-on-year rate by two tenths to 5.1%, reflecting continued wage pressures but negative calendar effects.

- 09:15 AM St. Louis Fed President Bullard (FOMC non-voter) speaks: St. Louis Fed President James Bullard will speak at an event hosted by the Missouri Bankers Association.

- 09:45 AM Markit US services PMI, November final (consensus 57.0, last 57.0)

- 10:00 AM ISM services index, November (GS 64.7, consensus 65.0, last 66.7): We estimate that the ISM services index pulled back 2 points to 64.7 in November after surging to an all-time high in October. Our services tracker fell 0.5pt to 58.6 in November.

- 10:00 AM Factory orders, October (GS +0.4%, consensus +0.5%, last +0.2%); Durable goods orders, October final (last -0.5%); Durable goods orders ex-transportation, October final (last +0.5%); Core capital goods orders, October final (last +0.6%); Core capital goods shipments, October final (last +0.3%): We estimate that factory orders increased 0.4% in October following a 0.2% increase in September. Durable goods orders declined 0.5% in the October advance report, but core capital goods orders increased 0.6%.

Source: Deutsche Bank, BofA, Goldman

Tyler Durden

Mon, 11/29/2021 – 09:55

via ZeroHedge News https://ift.tt/31bcJJR Tyler Durden