Hedge Funds Are Driving Price Action In The Gold Market

Looking at the data, it appears hedge funds are currently driving price action in the gold market

Please note: the COTs report was published 12/3/2021 for the period ending 11/30/2021. “Managed Money” and “Hedge Funds” are used interchangeably.

The Commitment of Traders analysis last month showed that selling had been exhausted and hedge funds were going long again. It highlighted the trouble gold faced at the $1,800 level. After the October Jobs and Inflation data, hedge funds went big into the market driving prices solidly through $1,800 before the market ran out of steam at $1,870.

The multiple attempts on $1,870 in rapid succession looked like another resistance would fall and send gold up through $1,900, especially if Brainard was nominated as Fed chair. Unfortunately, resistance held strong and a Powell nomination sent gold back through newly established support, which proved much more fragile on the way down vs the way up.

Gold is trapped below $1,800 again. A very weak jobs report provided only enough fuel to keep gold flat on the week. Will a hot inflation report next week be perceived as a “hawkish fed trade” or a “wealth preservation trade?” It all depends on managed money. The hedge funds are in complete control of this market at the moment as the data below shows.

Gold

Current Trends

Managed Money/Hedge Funds Net Longs increased slightly since last month, from 86k to 92k in November. On Nov 16, net longs peaked at 142k. This positioning accounts for the round trip gold took during November.

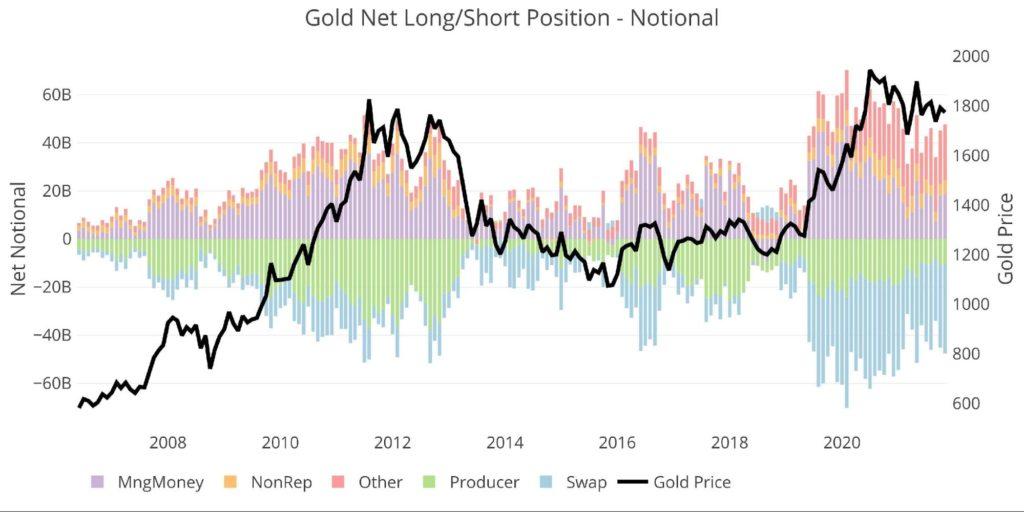

As the chart below shows, the November peak in longs did not see the same price appreciation as earlier this year. For example, in June of 2021 aggregate Net Longs were reaching 250k and the price of gold was at $1898. November saw net longs peak at 287k vs a price peak of $1853 on the same day (note: the price did reach $1879 but not on the same day as CFTC reporting).

Figure: 1 Net Notional Position

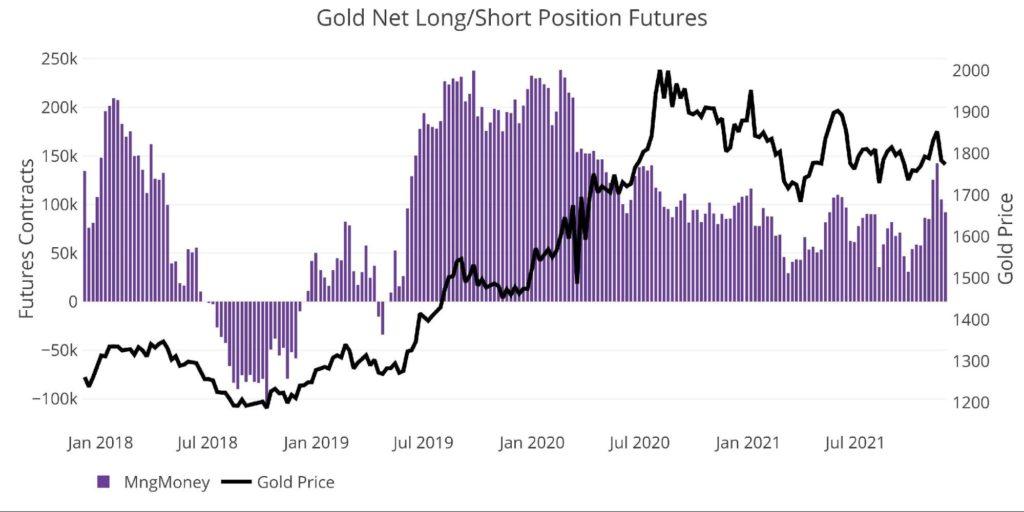

While “Other” has stayed relatively flat over the last several weeks with healthy long positions, Hedge Funds have been in and out. To see the strength of the correlation, the chart below zooms in on only Hedge Funds but extends back to Jan 2018. Hedge Funds have taken back control of the market. Their positioning is driving the price action each week. The peaks and valleys are perfectly aligned.

Figure: 2 Managed Money Net Notional Position

Putting actual numbers shows the true effect. Below lists the year and the Hedge Fund correlation vs “Other” correlation:

-

2017 .87 vs -.73

-

2018 .94 vs -.74

-

2019 .96 vs .57

-

2020 -.8 vs .64

-

2021 .82 vs -.02 (YTD)

-

2021 .85 vs -.43 (July – Nov)

The Hedge Funds lost control of the market in 2020. This is when Other actually drove the market higher. The group was helped by strong ETF flows and record delivery requests at the Comex. 2020 created a new baseline price in the metal. For example, in April 2019 Managed Money Net longs stood at 37k with a gold price of $1,303. On Sept 28, 2021, gold net longs reached 30k vs a price of $1735. At the moment $1750 is showing as strong support just as $1800 proves hard resistance.

Correlation does not prove causation, but the data makes a compelling case for Hedge Funds driving price action. Bottom line: the “weak hands” of Hedge Funds are dominating the short-term price movements of gold, but the physical demand keeps the market trending upwards.

Weak Hands at Work

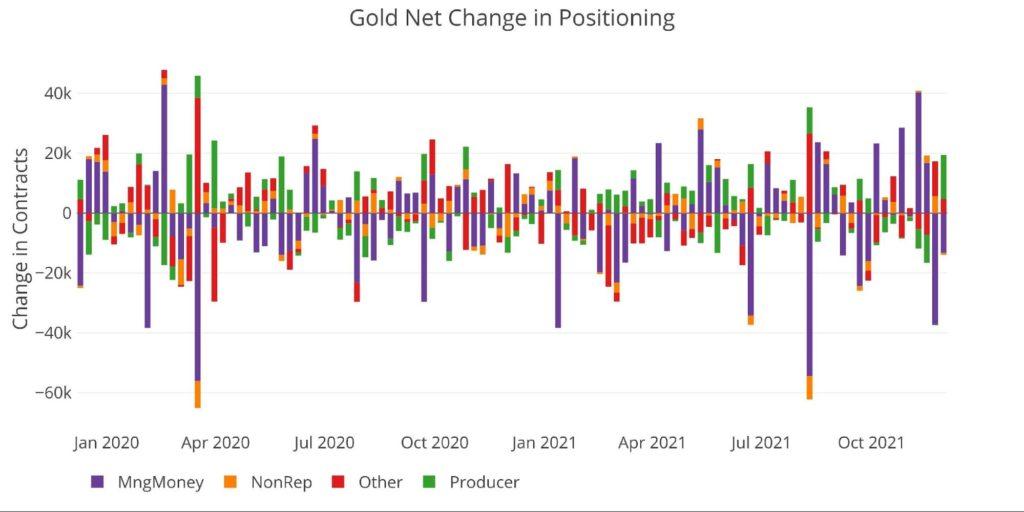

The chart below shows the week-over-week change by holder. The Hedge Funds spent 4 weeks building long positions followed by two weeks of hard selling. The traders are not in the market because of the fundamental reasons supporting the case for gold. They are jumping in and out, trading the news to make quick money in highly levered positions.

True investors should ignore this short-term movement and recognize the power of physical metal as insurance against government ineptitude.

Figure: 3 Silver 50/200 DMA

Still, for investors frustrated by the price movement, looking at the Hedge Fund trading provides a clear explanation. The table below has detailed positioning information. A few things to highlight:

-

The Managed Money Net Long monthly increase was driven primarily by shorts

-

Shorts have moved lower from 55k to 45k

-

Longs fell over the month from 141k to 137k

-

-

Other the past week, the move was primarily long liquidation from 152k to 137k

-

“Other”, which still represents the biggest Net Longs, was also driven by shorts closing

-

Longs were flat over the month at 172k

-

Shorts decreased from 44k to 39k, all of which came in the most recent week

-

It looks like there is “dry powder” on both sides of the equation. The monthly move was driven by shorts closing, but the weekly move was driven by longs closing.

Figure: 4 Gold Summary Table

Historical Perspective

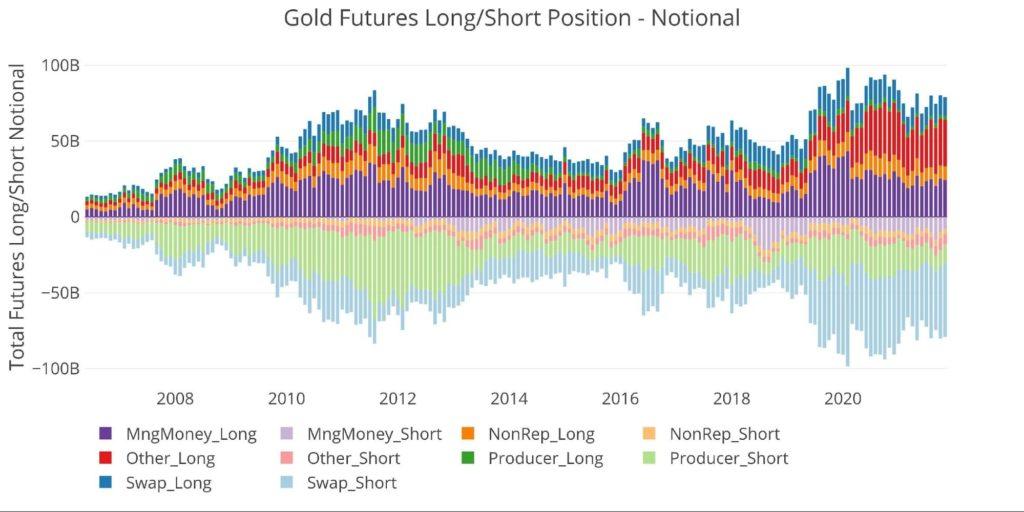

Looking over the full history of the COTs data by month produces the chart below (please note values are in dollar/notional amounts, not contracts). The chart shows the last run-up in price in 2011, followed by the slow fall into 2015 until the new bull market started in 2016. The response to the Trump election (gold sold off hard) can be seen clearly in the sharp drop-off in late 2016.

This chart also shows how big the “Other” category has become on the long side. In 2011, Other Long had $8.6B in gross long vs $30.6B in the most recent period.

Figure: 5 Gross Open Interest

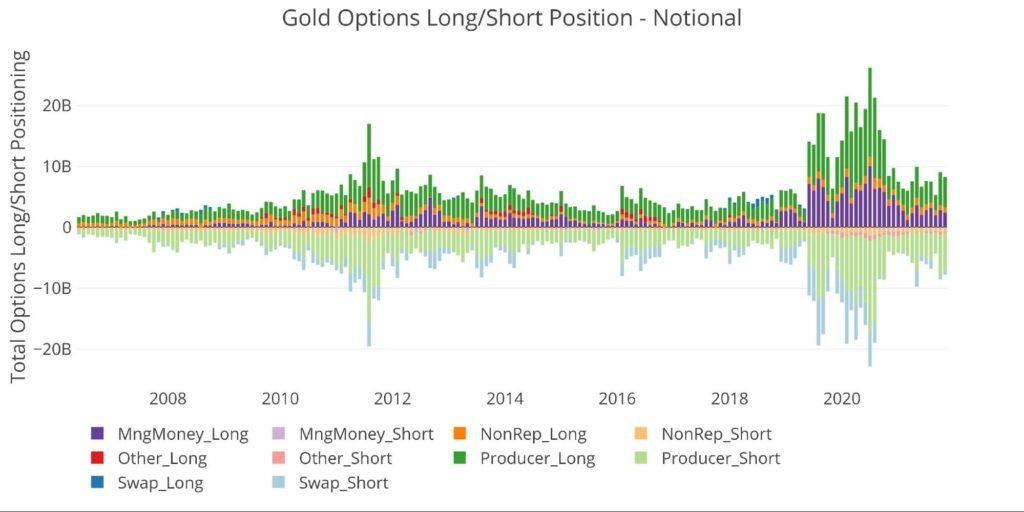

The CFTC also provides Options data. This has mainly been dominated by Producers, but recently Managed Money has played a larger role within the market. The current period shows a similar trend with Managed Money Longs decreasing from $2.8B to $2.4B during November.

Figure: 6 Options Positions

Finally, looking at historical net positioning shows the correlation of Managed Money positioning with price. The peaks and valleys in price are mirrored in the open interest. The correlation did strongly diverge last year after the March 2020 sell-off. Hedge Funds continued reducing net long positions even while the price rose dramatically. This was probably due to strong ETF buying which won’t show up in the futures.

Note: The correlation will look stronger because price is half of the Notional value equation

Figure: 7 Net Notional Position

Silver

Current Trends

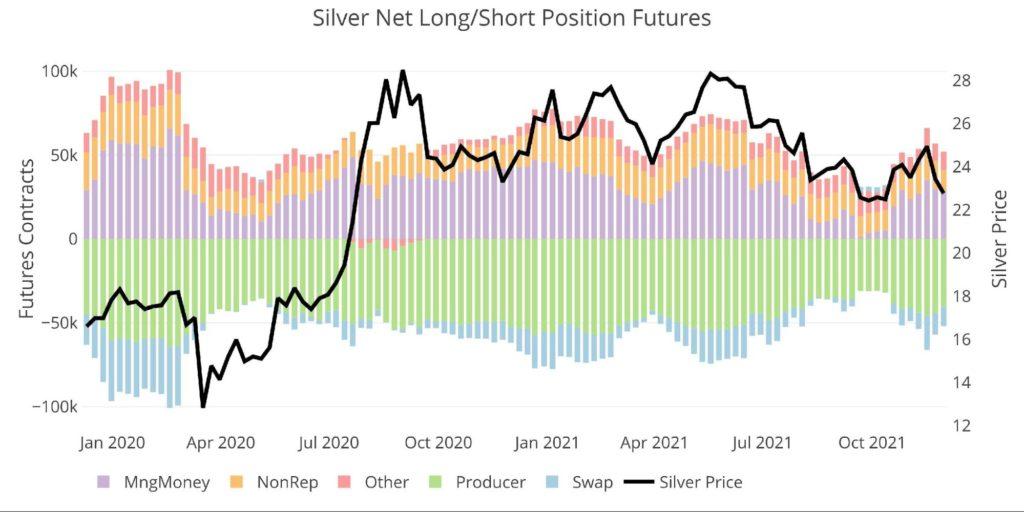

The most recent move in silver was actually driven by Non-Reportables rather than Managed Money. While Hedge Funds were responsible for the drubbing silver took in September, their current net longs stayed relatively stable compared to Non-Reportables.

Figure: 8 Net Notional Position

This can be seen more clearly in the weekly chart. While Hedge Funds did liquidate the last two weeks, they only unwound some of their recent positions. Non-Reportables unwound their entire new position and then some.

Figure: 9 Net Change in Positioning

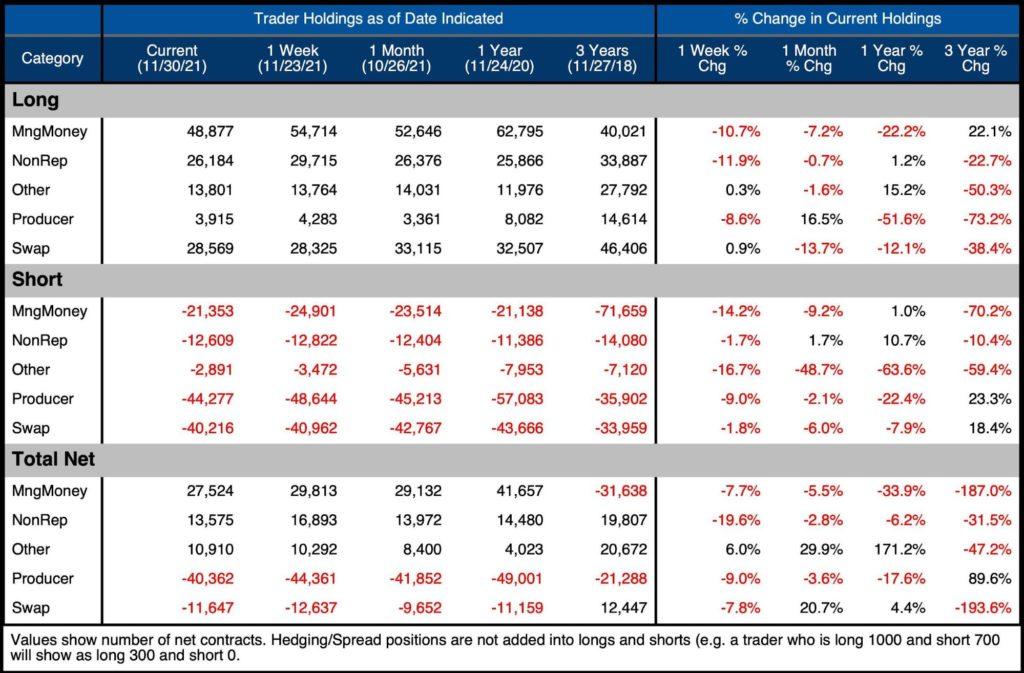

The table below shows a series of snapshots in time. This data does NOT include options or hedging positions. Important data points to note:

-

Within Managed Money, the monthly change was a modest 1600 decrease and was even positive last week

-

Longs drove most of the move, going from 52k to 54k last week and down to 48k this week

-

-

As of last week, NonRep had increased net longs by 3k contracts, 4x the movement of Hedge Funds

-

Longs went from 13.9k to 16.9k and down to 13.5k

-

Figure: 10 Silver Summary Table

Historical Perspective

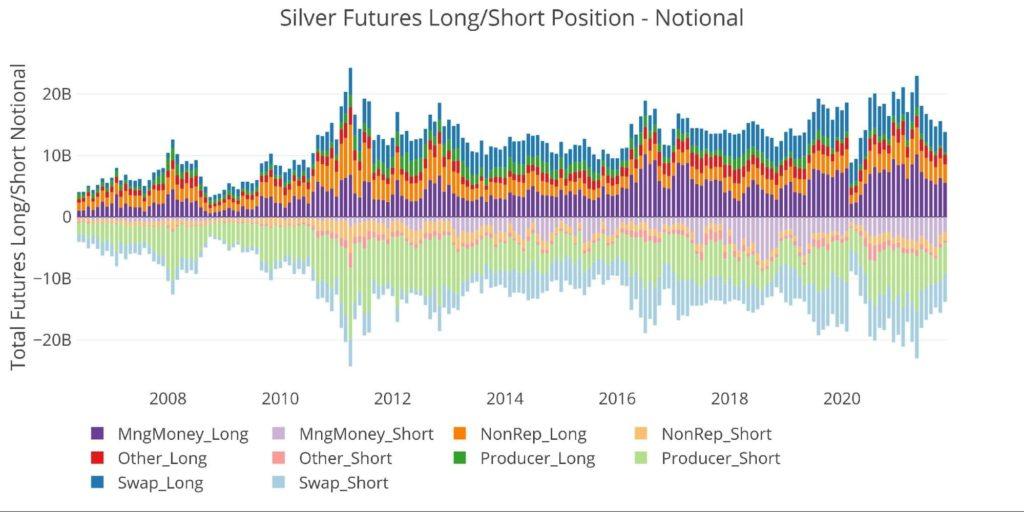

Looking over the full history of the COTs data by month produces the chart below. The chart shows the last run-up in price in 2011, followed by the slow fall into 2015. The price collapse in silver in 2020 is clearly visible in this chart. As can be seen, gross longs are still well above the 2020 lows.

Figure: 11 Gross Open Interest

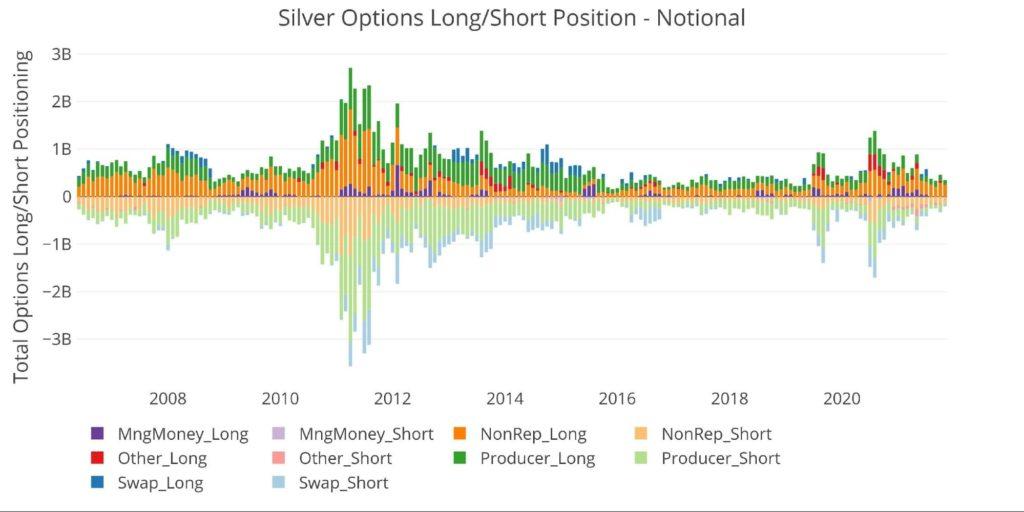

The CFTC also provides Options data. This has mainly been dominated by Non-Reportables, exceeding even Producers. Options have fallen off significantly from the spike last July and is still well below the peak in 2011.

Figure: 12 Options Positions

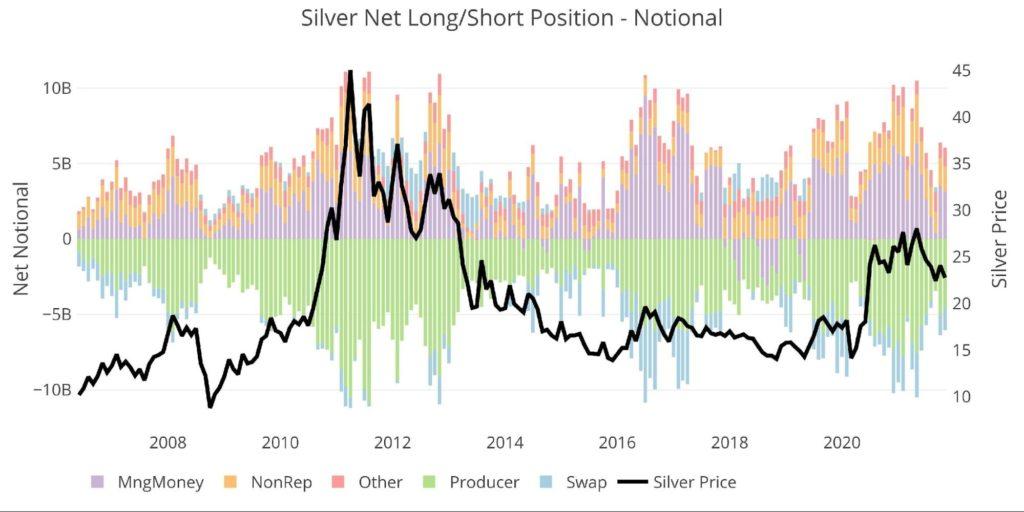

Finally, looking at historical Net positioning shows the correlation of positioning with price. Similar to gold, the peaks and valleys in price are mirrored in the open interest. Again, the latest pop did not generate the price increase that would have been expected given the magnitude of the move.

Figure: 13 Net Notional Position

Conclusion: How Will Hedge Funds Respond to the Fed?

Hedge Funds certainly trade using technical analysis, which is why Fib targets and round numbers (e.g. $1,800) prove to be such difficult resistance points. Over time, the physical market has pushed prices up, but the short-term move is dominated by hot money. How long until Hedge Funds call the Fed’s bluff? More importantly, how long until there isn’t any physical to back the paper contracts because it’s been delivered and then removed from the vault?

Astute investors should keep the long-term picture in mind. The short-term gyrations can be immensely frustrating, but gold and silver are not Bitcoin. They are not vehicles to get rich quick because that would disqualify them as safe-havens. Remember, what goes up quickly, can come down quickly. Stay the course, trust the fundamentals, use the CFTC analysis to explain the short-term price movements, and understand the protection provided by physical precious metals.

Tyler Durden

Sun, 12/05/2021 – 11:30

via ZeroHedge News https://ift.tt/3lEil6i Tyler Durden