Europe Forced To Pay Even Higher Prices To Fill Gas Storage

By John Kemp, senior market analyst at Reuters

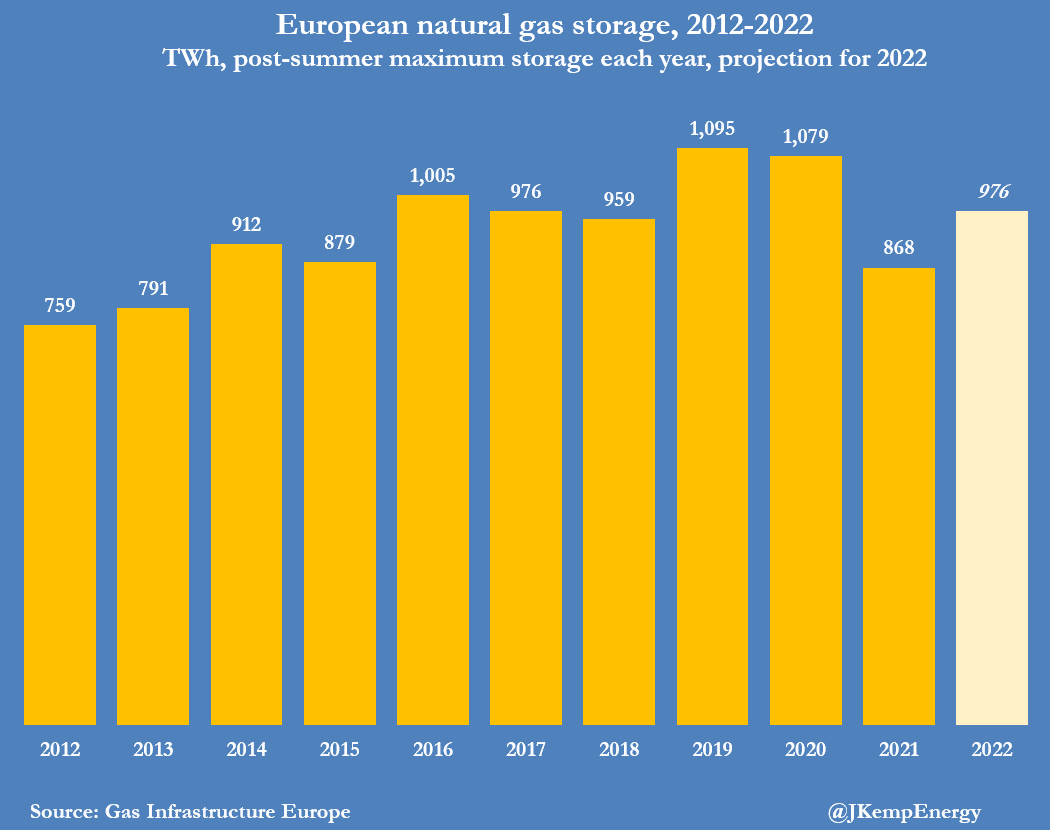

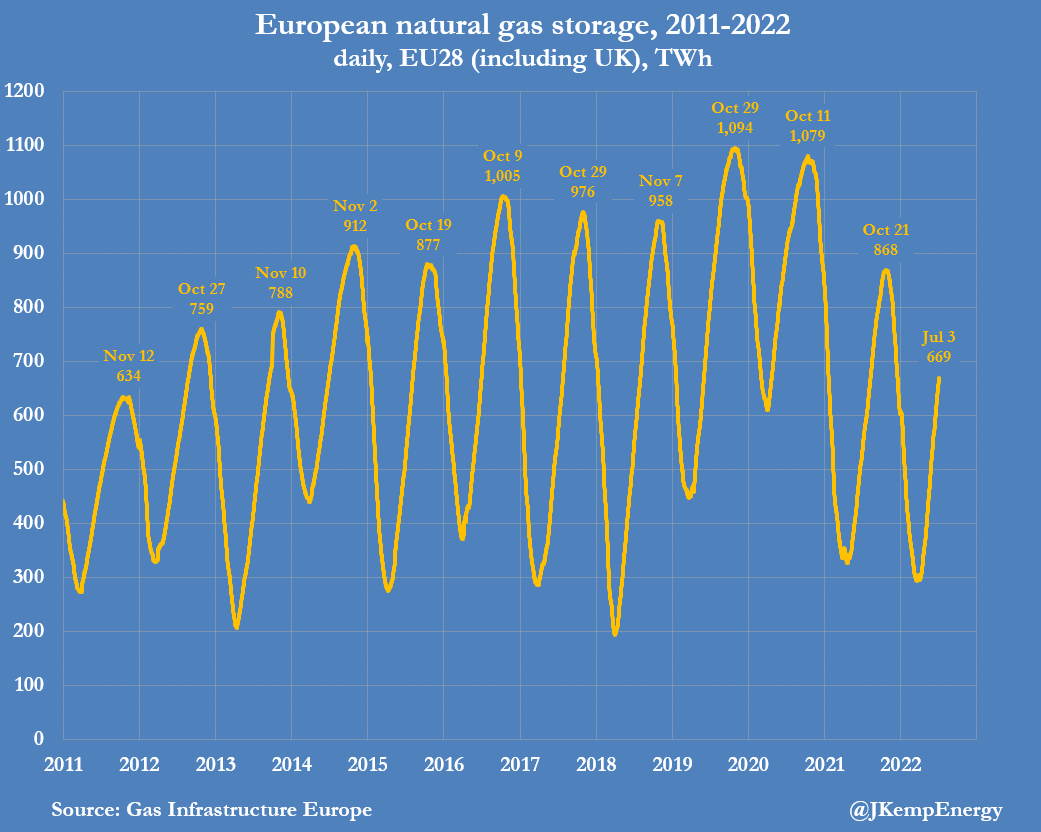

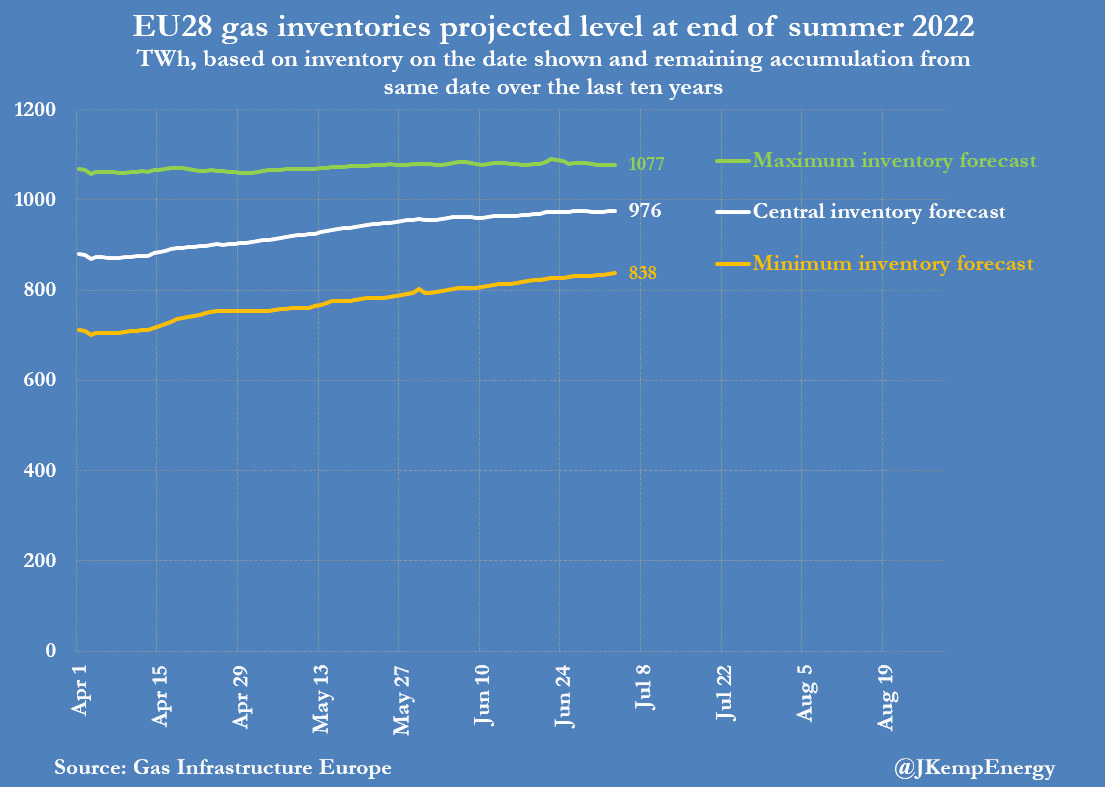

Europe’s gas inventories are on course to reach 976 terawatt-hours (TWh) by the end of the summer…

…compared with 868 TWh at the same point last year, and slightly above the 10-year seasonal average.

The region continues to buy as much liquefied natural gas (LNG) as possible to offset reduced imports from Russia and the possibility of a complete stoppage next winter but it is pushing up prices sharply.

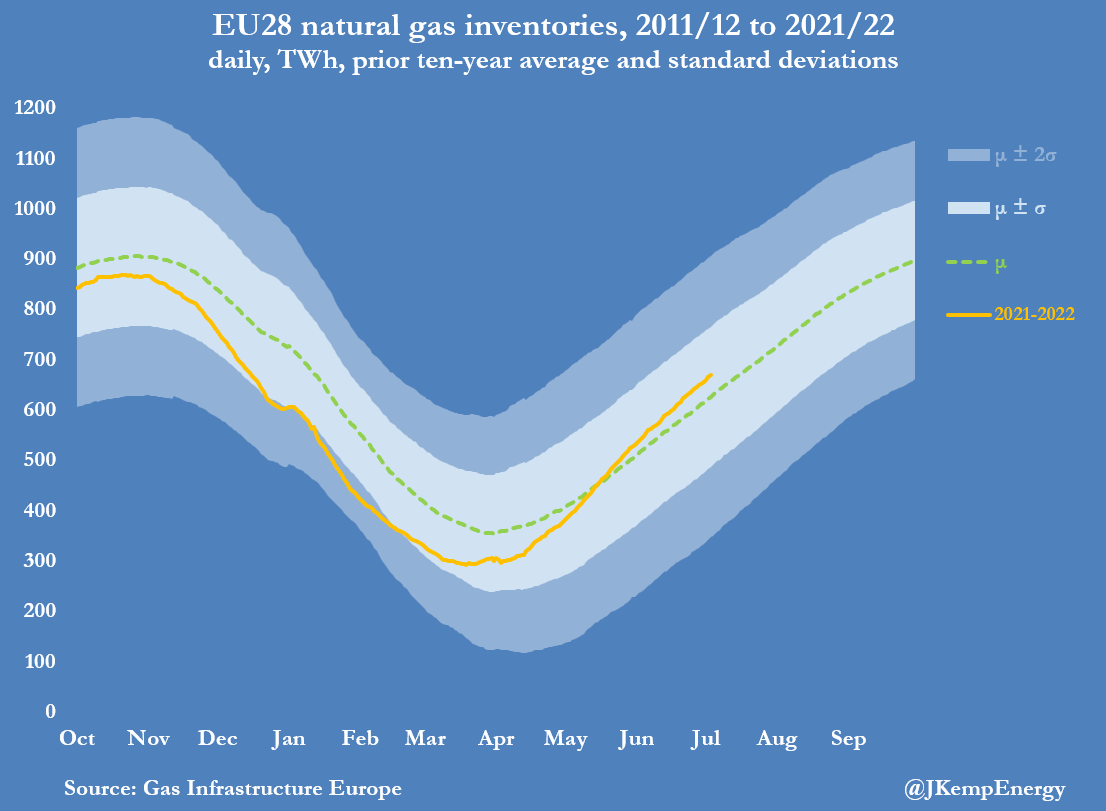

Stocks in the European Union and the United Kingdom (EU28) are on track to be 44 TWh (5%) higher than the average for the previous 10 years, based on past storage trajectories.

The probable range is from 838 TWh to 1077 TWh, and has changed little in recent weeks, as the disruption of pipeline supplies from Russia has been offset by higher prices and more LNG arrivals.

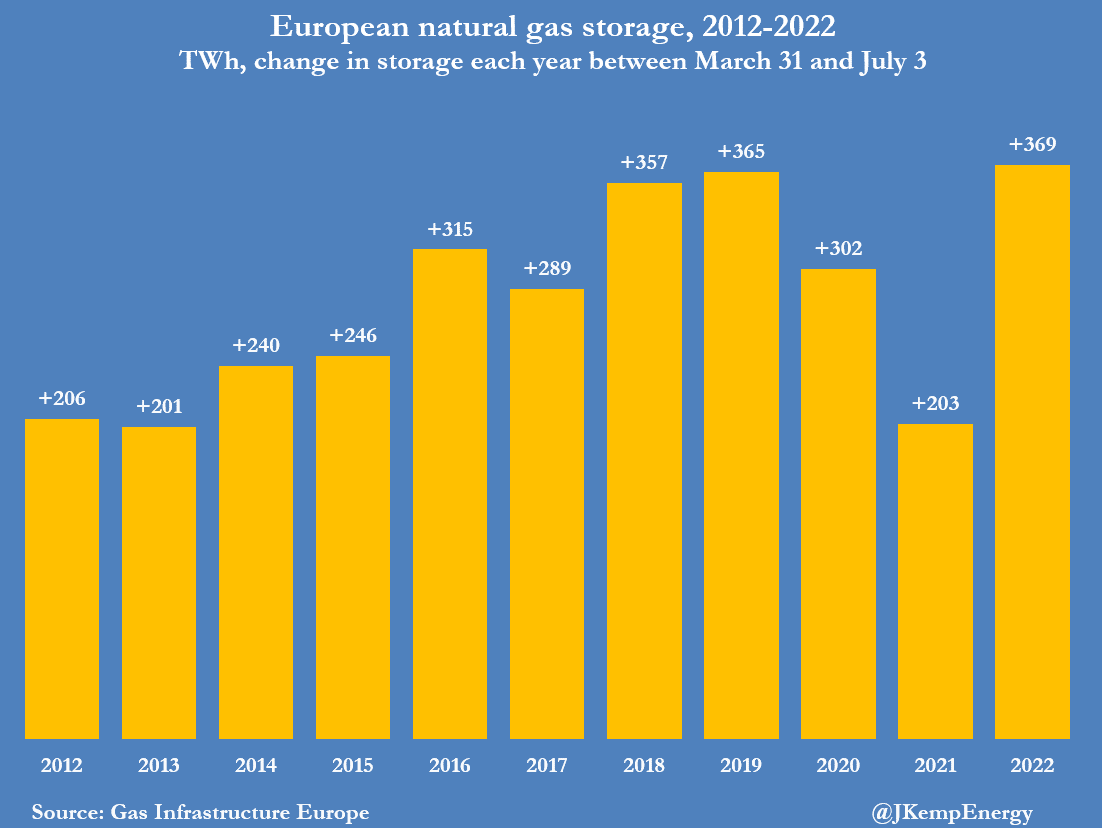

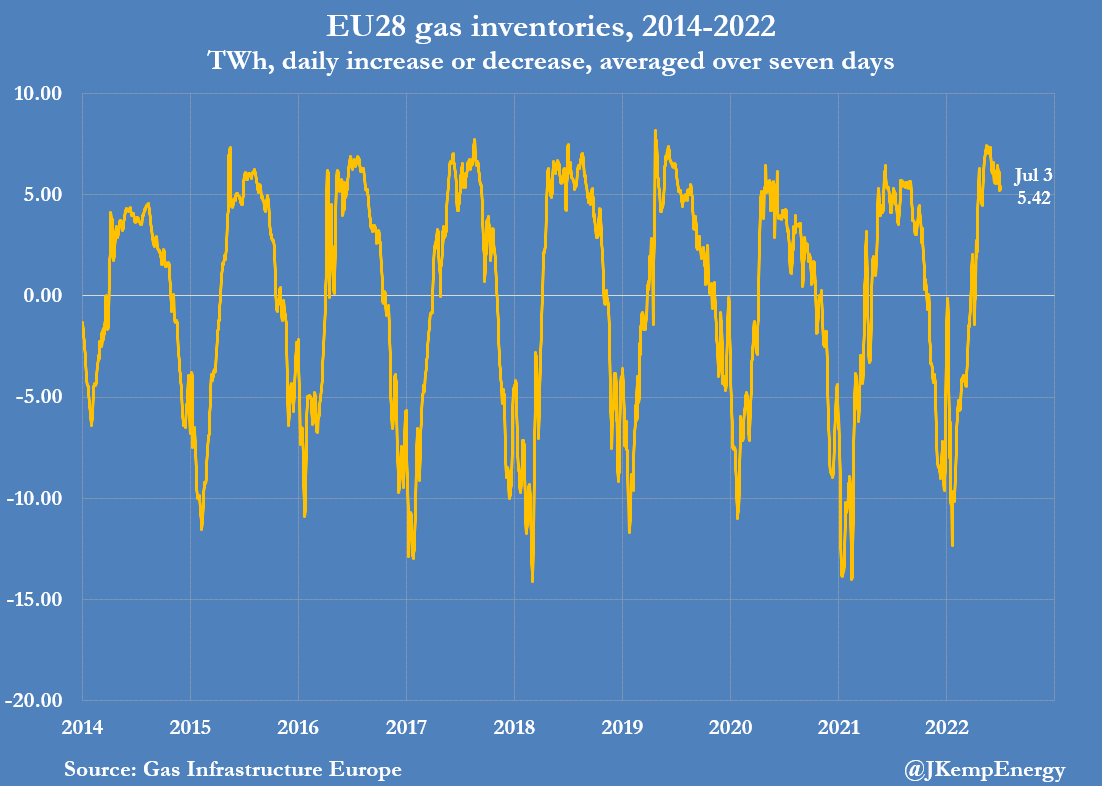

Stocks have increased by a record 369 TWh since the start of April, compared with an increase of just 203 TWh this time last year and a ten-year seasonal average of 272 TWh.

As a result, inventories are 44 TWh (7% or 0.31 standard deviations) above the average for the time of year, having been 129 TWh (23% or 1.37 standard deviations) below average at the end of January.

In recent weeks, the rate of inventory accumulation has slowed to 5 TWh per day, from more than 7 TWh per day in late May.

Until early June, storage had been filling at an unsustainable rate so some deceleration was expected by the end of June or the beginning of July.

Inventory accumulation normally slows at this time of year and the current rate is still slightly above the seasonal average for 2012-2021.

But the reduction in pipeline supplies from Russia has accelerated the adjustment and put explosive upward pressure on prices by forcing European buyers to purchase extra LNG cargoes to make up the shortfall.

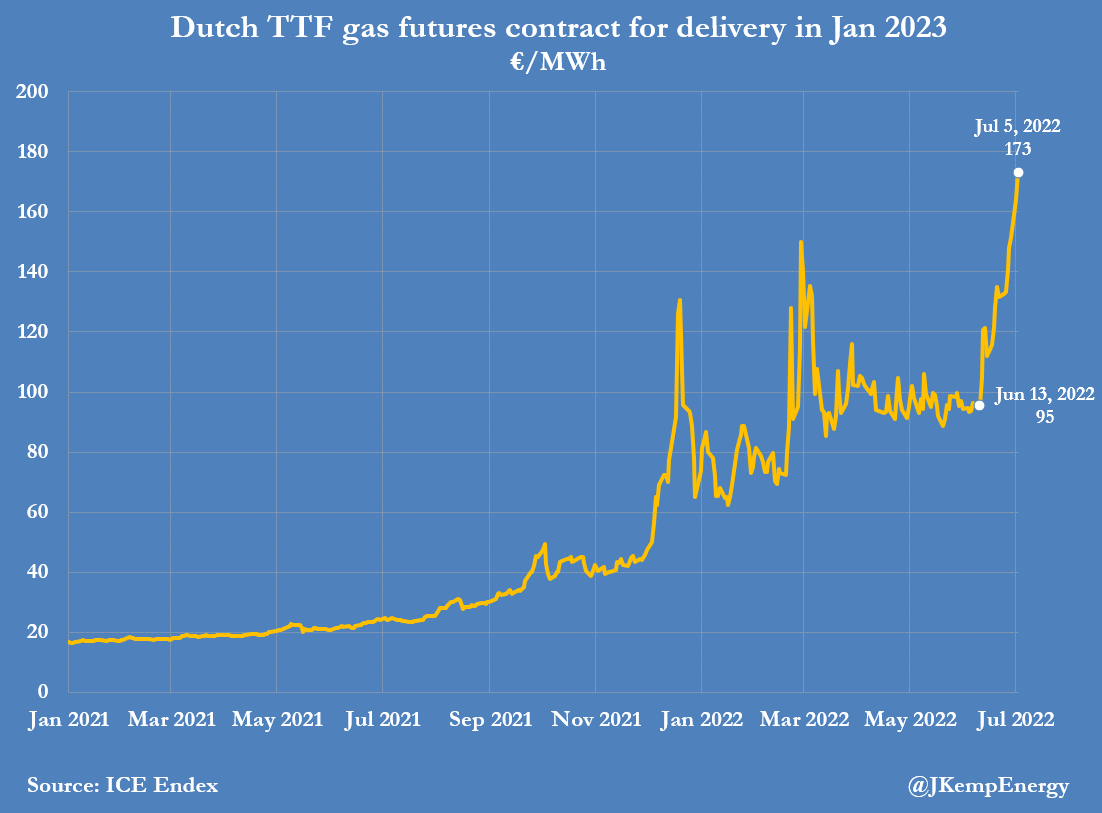

Futures prices for deliveries in Northwest Europe in January 2023, in the depths of next winter, have climbed to a record €173 per megawatt-hour (MWh) from €95 in the middle of June.

Soaring prices are signalling the need for conservation by businesses and households and maximum fuel-switching to coal, biomass and hydro by electricity generators to build stocks even faster.

Futures for deliveries in Northwest Europe in January 2023 are also trading at a record premium of €35 per MWh compared with deliveries for the same date in Northeast Asia.

Europe’s buyers are attempting to divert the maximum volume of LNG to improve their own supply situation, in the process squeezing utilities in South and East Asia, worsening shortages at the other end of Eurasia, and pushing up prices for everyone.

Tyler Durden

Wed, 07/06/2022 – 07:35

via ZeroHedge News https://ift.tt/1KauvRQ Tyler Durden