Americans Are Getting Poorer: Price Inflation Grew Faster Than Wages Again In September

Authored by Ryan McMaken via The Mises Institute,

The federal government’s Bureau of Labor Statistics released new price inflation data today, and according to the report, September was yet another month of soaring inflation. According to the BLS, Consumer Price Index (CPI) inflation rose 8.2 percent year over year during September, before seasonal adjustment. That’s the nineteenth month in a row of inflation above the Fed’s arbitrary 2 percent inflation target, and it’s seven months in a row of price inflation above 8 percent.

Month-over-month inflation rose as well, with the CPI rising 0.2 percent from August to September. September’s month-over-month growth also shows some acceleration in monthly price inflation growth. Month-to-month growth had been approximately zero in July and August following nineteenth months of monthly growth.

September’s increase keeps price inflation near forty-year highs. June’s year-over-year increase of 9 percent was the largest CPI increase since 1981, but September’s increase percent still keeps price inflation well within the same range as the inflationary years of the early 1980s. September’s increase was the seventh-largest increase in forty years.

The ongoing price increases largely reflect price growth in food, energy, transportation, and shelter. In other words, the prices of essentials all saw big increases in August over the previous year.

For example, “food at home”—i.e., grocery bills—was up 13.0 percent in September over the previous year. Gasoline continued to be up, rising 18.2 percent year over year, while new vehicles were up 9.4 percent. Shelter registered one of the more mild increases, with a rise of “only” 6.6 percent according to the BLS.

This is bad news for the Biden administration, as this is the final price inflation report before the November elections. The administration has repeatedly attempted to downplay the relentless increases to the cost of living being inflicted on Americans after years of deficit spending, which has helped fuel inflationary monetary policy.

On Thursday, for example, the Biden attempted to claim that price inflation increase “2 percent” by slicing and dicing the numbers into an annualized rate composed of only the past three months.

In a written statement, the president insisted “Today’s report shows some progress in the fight against higher prices, even as we have more work to do … Inflation over the last three months has averaged 2%, at an annualized rate…”

In the real world, however, Americans have lost an immense amount of purchasing power. That purchasing power is lost forever unless there is sizable price deflation in coming years, and the deflation-phobic central bank is sure to intervene to make sure that doesn’t happen.

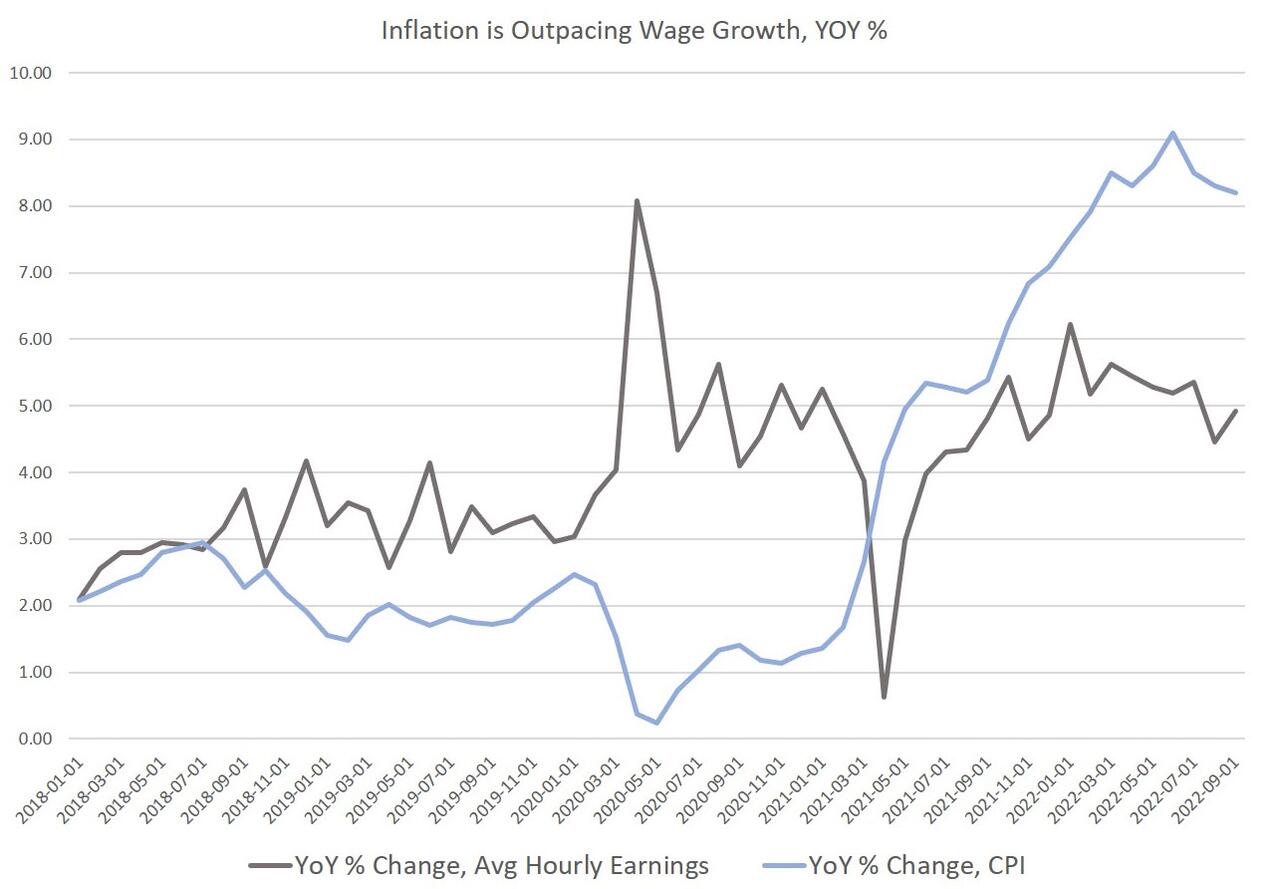

In terms of real earnings, this has been devastating for many wage earners. According to the BLS, average hourly earnings in September came in at $32.40. That’s an increase of 4.92 percent, year over year. This might be good news were it not for the fact that price inflation was up 8.2 percent during the same period.

So, the gap between wage growth and price inflation in September was –3.3. This means September was the eighteenth month in a row during which price inflation has outpaced earnings.

This is bad news for the administration, and it’s also bad news for the Federal Reserve. The persistent price inflation is a repeated reminder of just how far behind the curve the Fed is, and how reckless the Fed was in essentially printing nearly $5 trillion between February 2020 and April 2022. Over the past two years, the Fed repeatedly assured the public that creating vast amounts of new money would be no problem and that price inflation would never be anything more than “transitory.”

Once that narrative was disproven, the Fed then began to admit late in 2021 that CPI inflation was not transitory but that the Fed would not allow it to become “entrenched.” Price inflation did indeed become entrenched, but the Fed waited more than six months, from the fall of 2021 to spring 2022, to actually begin raising the target federal funds rate. The Fed’s lack of real action can further be seen in the fact that the Fed’s portfolio—which grew by $8 trillion with newly created money from 2008 to early 2022—has dropped by only 2.3 percent this year. That may be enough to spook markets, but it’s hardly enough to promote any sort of return to real prices in asset markets or normality in monetary policy.

There are only painful options for bringing price inflation under control at this point, and that’s all thanks to the Fed’s creation of countless bubbles and malinvestments over the past decade. The Fed has created a bubble economy that’s desperately addicted to quantitative easing, ultra-low interest rates and other forms of easy money. So, putting the brakes on new money creation, even without any real effort at quantitative tightening, will lead to soaring defaults, and attempts to save on expenses by laying off workers.

The only “good” news here—considering the options—is that this will lead to falling prices as unpaid debts evaporate thus shrinking the money supply. Demand destruction will also occur and people lose their jobs and higher interest rates mean less spending. We’re already starting to see some evidence of this. According to the Case-Shiller index, home price growth if finally slowing. Meanwhile, job opening as fallen to a fourteen-month low, savings rate have fallen to a post-2008 low, and disposable income growth has collapsed.

That will slow price inflation, but not without also bringing a lot of pain to ordinary people trying to make a living.

Tyler Durden

Fri, 10/14/2022 – 14:40

via ZeroHedge News https://ift.tt/HJmQDBg Tyler Durden