PPI, Michigan Will Give Further Clues On Inflation’s Stickiness

Authored by Simon White, Bloomberg macro strategist,

Any hints of an inflation comeback in today’s PPI and Michigan survey data are prone to prompting a further selloff in stocks and bonds.

The net result of Thursday’s largely in-line CPI data was a drop in both stocks and bonds. Some of the yield move higher was probably no- or soft-landing driven, but the market is now more sensitive to inflation concerns, as it becomes clear just how much debt the US needs to issue.

Now that the Fed looks to be near or at the end of their hiking cycle (at least for now), CPI data is likely to be of less importance. When the Fed was using it to guide policy, it had more weight. But as a lagging indicator, the market is not going to wait for CPI to confirm that inflation is reaccelerating, and instead focus on a much broader suite of data. PPI and the University of Michigan’s inflation expectations are two such indicators.

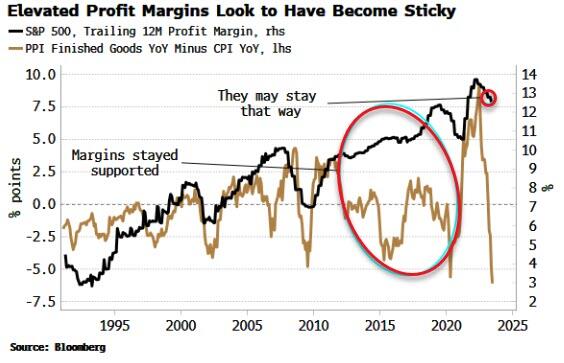

Higher profit margins was one of the key drivers of rising inflation. For inflation to come down durably, margins need to fall durably too. The Primary Services component of the PPI report is a proxy for margins across different types of firms. It shows that margins have fallen, but still remain elevated versus their pre-pandemic levels.

The chart below shows PPI vs CPI, another proxy for margins. PPI has collapsed relative to CPI, which would typically coincide with falling profit margins. But that has signally failed to happen in this cycle. Indeed, through the post-GFC period margins have continued to rise even though they were expected to mean-revert.

Sticky margins are thus one sign that inflation is becoming ingrained.

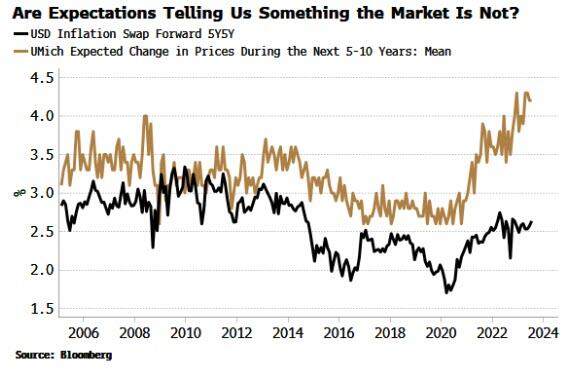

We’ll also get the University of Michigan Consumer Survey with its estimate of inflation expectations.

Longer-term (5-10 year) inflation expectations have been steadily rising since late 2020 and are now at 15-year highs. The mean has risen by more than the median, showing a rising positive skew in expectations.

The rise in inflation expectations is at odds with a more muted rise in breakevens.

We’ll only know which one was more right ex post, but breakevens have an empirically poor record of forecasting inflation, especially at turning points.

Tyler Durden

Fri, 08/11/2023 – 08:05

via ZeroHedge News https://ift.tt/e2BqxZW Tyler Durden