Is This Market Breaking From The Bottom Up?

By Peter Tchir of Academy Securities

Revisiting Maslow, “Safe” Assets and Bubbles

It has become impossible not to just watch the rise in treasury yields, but to question what the heck is going on! The march to higher yields has been relentless. On some days there seems an “obvious” reason. Some piece of data that fits the narrative for higher yields. But on many days, there is little to no explanation, and certainly not one that would “justify” the magnitude of the moves.

Getting things wrong in markets sucks and is costly. But, often, we can understand what we did wrong. I bet on lower yields because I thought XYZ and would, but the opposite of XYZ happened, so I got it wrong. It is much more difficult to explain what has pushed the 10-year treasury towards 5%. If it was just me, I’d crawl back into my cave and lick my wounds, but this seems to be an almost universal discussion point. Even those who have had the right call on yields, seem somewhat perplexed as to why it is happening. For those who are interested we list several things such as Fed probability, energy prices, JOLTs data, etc. that don’t seem to be enough to push yields as high as they’ve gotten. i

As a contrarian, the number of times I’ve heard “paradigm shift” or the more colloquial “broken” has risen dramatically, so maybe, just maybe yields can go lower from here.

That is my view, but it does seem like a good opportunity to revisit a few long running themes.

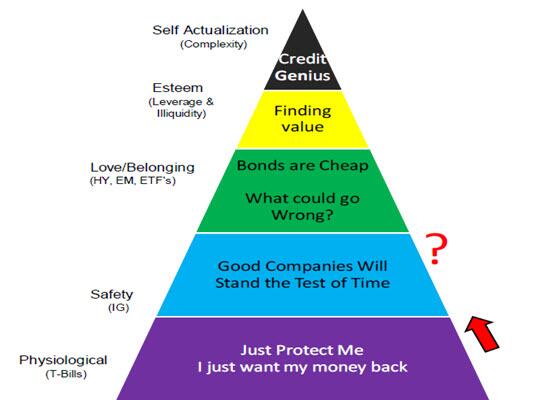

Maslow’s Hierarchy of a Credit Bubble

Do we need to rethink Maslow’s Hierarchy of a Credit Bubble?

Using Maslow’s Hierarchy of needs has been an effective way of thinking about credit bubbles since well before the Great Financial Crisis. We move up or down the “needs”. As times improve we move up the pyramid, taking on more and more exotic risk. During the years of ZIRP, when the chase for yield was profound, we got darn close to “Credit Genius” status again, but the leverage and risk appetite wasn’t quite what was pre- GFC.

Normally, on the way down, we see asset classes “break” as investors “retreat” or consolidate to the next safest investment.

Is this market breaking from the bottom up?

Are problems in the treasury market eroding the levels above them? That is incredibly counter-intuitive, but could it be happening?

While I doubt it, two prior T-Reports are jumping up and down, screaming at the top of their lungs, that we should not ignore what is going on!

-

Back in May 2020, we published Credit Cards & American Ingenuity. We highlighted a conversation we had with Meredith Whitney post GFC. In retrospect, the American Consumer “broke” the pecking order of debt. Credit monitors had a specific pecking order that was the “normal” course of defaults for American consumers:

-

1. Default on Store Branded Credit Cards.

-

2. Default on Major Credit Cards.

-

3. Default on Auto Loans.

-

4. Default on Mortgages.

-

-

Quite quickly the average consumer figured out that they could default on their mortgage and face none of the usual consequences (foreclosure, eviction), but they needed their most basic credit cards to purchase the items they needed ever day.

-

Has something gone on in our system where investors are more concerned about Treasuries than other forms of debt? It seems highly unlikely, but order of priority has failed to be a good indicator in the past, which seems “crazy” related to treasuries, and yet….

-

In August of this year, we wrote about U.S. Government Credit and argued that while U.S. Treasuries don’t trade based on ratings, the actions in D.C. that spurred the ratings action at the time, all “justified” it. That from a credit standpoint, “our” behavior has deteriorated and wouldn’t be ignored in a “normal” credit.

-

While “far-fetched” and maybe even whimsical, we broached the subject of a “sovereign ceiling” for U.S. corporate issuers in our Mid-Year Review. Could a company (or companies) with strong corporate governance and a strong global presence trade tighter than the U.S. government? It still seems more like a conversation for emerging market countries, with weak sovereign leadership, but strong, typically asset based, corporations, but maybe it isn’t as silly as it sounds?

If one thing resonates for me on why yields are grinding higher, it is a lack of faith in the government’s willingness to control and even pay debt.

Bubbles Only Happen in “Safe” Assets

Discussing the sovereign ceiling seems like the perfect segue to dragging out another theory that has served us well – bubbles only happen in safe assets.

Back in March 2020 we posted Credit and Financial Bubbles. We once again paired the discussion of Maslow’s Hierarchy of a Credit Bubble with the “Safe Asset” concept, since they do go so well together (in a you put you peanut butter in my chocolate, you put your chocolate in my peanut butter, kind of way).

The premise that “safe assets” are where bubble risks reside is quite simple:

Two Conditions Required for a Financial Bubble or Crisis

-

The banks need to be heavily exposed to the asset. Banks are the lynchpin of the financial system, so for anything to create a bubble, it needs to hit the banks. And to hit the banks, they need to own a lot of it.

-

The asset has to be owned on a highly leveraged basis. Leverage is what creates forced sellers. It probably sounds trite, but you have to have a margin account to get a margin call. Forced sellers are the key and that is directly tied to owning an asset on a leveraged basis.

My view is that you need a ‘safe’ asset, that banks own a lot of, and that both banks and other investors own with significant amounts of leverage. Does any asset fit these criteria better than treasuries?

In the original report, we lay out how every recent financial bubble in the U.S. (going back to the 1980’s) can be tied to so-called “safe” assets, or at least assets that were thought to be safe before they cracked?

Somehow, CRE seemed to be the “safe” asset that was high on my watch list, but I have to wonder about Treasuries and all we have to do is go back to earlier this year and look what was a big reason behind at least one of the bank failures.

Seems crazy, but…

Bottom Line

The move in rates is overdone. Rates will move lower from here.That will help risk assets.

The talk of “broken” is overdone.

The “natural” order of treasuries as the “safest” asset may now be up for discussion and something we will have to deal with over time.

At Academy, we argued that freezing Russia’s dollar reserves was a bad decision, with far-reaching consequences. We think that is playing out as more and more trade occurs in the Yuan. Similarly, this current bout of weakness in treasuries will likely end, sooner than later, hopefully starting today, but I’m not sure the treasury market will be looked at the same again.

That is particularly true as we seem set to endure more antics out of D.C. on budgets and debt in the coming months and years, that will be increasingly difficult to dismiss.

Tyler Durden

Wed, 10/04/2023 – 13:45

via ZeroHedge News https://ift.tt/9QJZSTd Tyler Durden