FOMC Minutes Preview: Hawkish But Stale

Submitted By Newsquawk

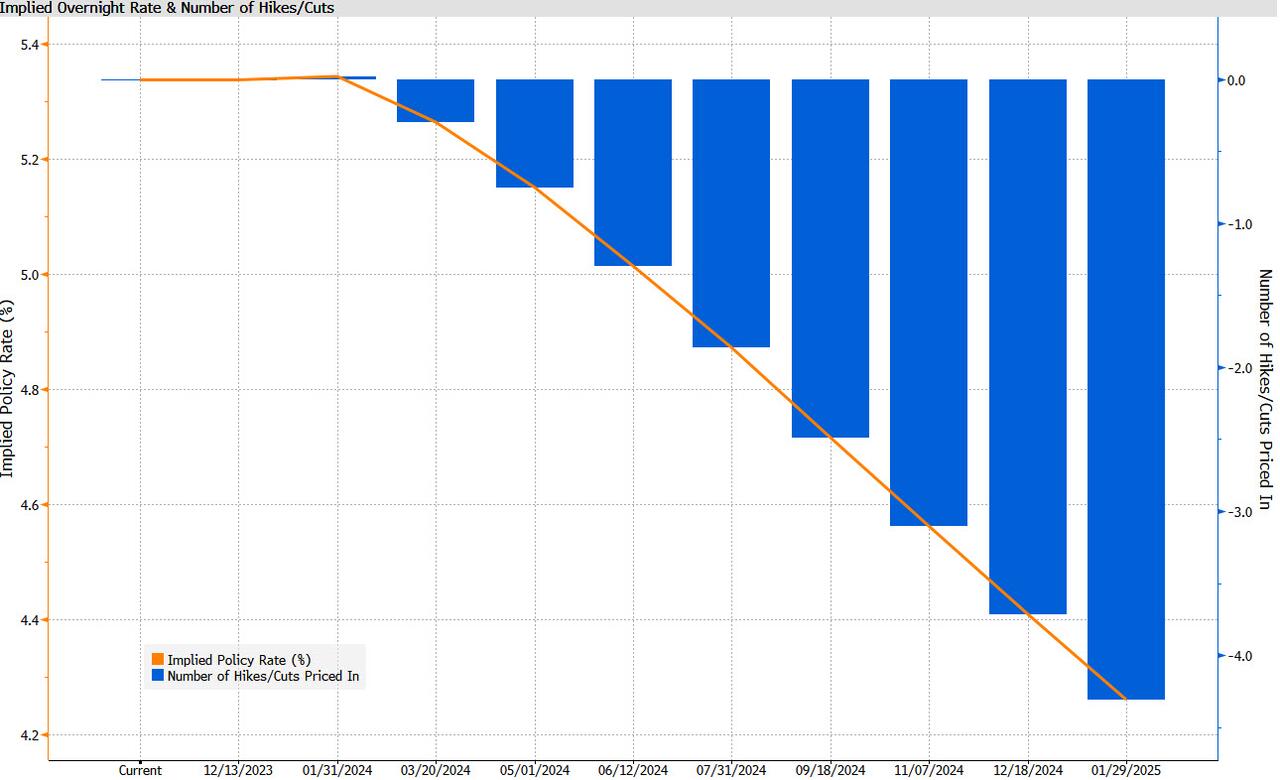

The minutes from the October 31-November 1 FOMC meeting are due at 2pm ET, and while they will likely be more hawkish than current expectations, it’s worth recalling that the Minutes will also be considered stale, given they do not incorporate the soft October nonfarm payrolls and CPI data (and other lower inflation metrics), not to mention some survey releases (such as ISMs) having seen downward surprises, resulting in traders pulling back bets on further rate hikes, and adding to bets for cuts in 2024 – nearly 100bps of easing is now priced by the end of next year with a 25% implied probability of a cut as soon as the March FOMC.

Fed Chair Powell, speaking around a week after the FOMC meeting, struck a hawkish tone, and said that although progress had been made on inflation, there was still a “long way to go”; he reiterated that officials were not confident that they have achieved a sufficiently restrictive policy stance, adding that if it became appropriate to tighten further, the FOMC would not hesitate to do so, stating that the Fed will continue to move carefully, and decide on a meeting-by-meeting basis. His remarks have been largely echoed by colleagues, and that is likely to be reflected in the minutes, but market participants are following the dovish data right now rather than hawkish official commentary.

At its November policy meeting, the FOMC left rates unchanged at 5.25-5.50%, in line with both expectations and market pricing, and its statement saw only slight changes. The central bank maintained that “additional policy firming may be appropriate” and made a slight upgrade to its description of economic growth, highlighting that economic activity had been expanding at a “strong” pace in Q3, in contrast to the “solid” pace mentioned in September. It also acknowledged that job gains had “moderated since earlier in the year” (compared to the previous “slowed in recent months” language), but it continued to emphasize the strength of jobs growth and the low unemployment rate. Further, it included a new line to address the rise in Treasury yields ahead of the meeting, stating that tighter financial and credit conditions are likely to have a negative impact on economic activity, hiring, and inflation, in contrast to the September statement, which only acknowledged tighter credit conditions.

Chair Powell’s presser remarks echoed his previous recent views and outlined the Fed’s commitment to maintaining a restrictive monetary policy. He noted that the full effects of this policy were not yet clear. He described the economy as strong, paying attention to robust growth and labor demand. Powell stressed that inflation remains high, and tight labor markets have shown some signs of wage growth easing.

In the Q&A, Powell expressed uncertainty about policy and financial conditions, hinting at potential interest rate hikes. He also suggested that the Fed is close to the end of the current rate-hike cycle and was evaluating its approach. Powell confirmed that rate cuts are not being considered, but the focus is on how long to maintain a restrictive policy.

Tyler Durden

Tue, 11/21/2023 – 11:35

via ZeroHedge News https://ift.tt/uh54Agt Tyler Durden