It Seems Like Silly Season Is Here For Markets, But Things Are Likely To Get Even Sillier

By Peter Tchir of Academy Securities

It’s 4:20. Do You Know Where Your Yields Are?

It isn’t quite as haunting as “It’s 10pm. Do You Know Where Your Children Are?” but it’s a pretty important question for market participants!

For most of Friday morning, it looked like we were going to be able to discuss the 10-year closing the week at 4.3% (in line with our target) and where we started to get nervous that lower yields would weigh on risk assets. By the end of the day, the 10-year finished at 4.2% and stocks seemed to love it!

One of our clients pointed out that municipal bonds had one of their best years ever, in November! The beginning of December hasn’t been too shabby for them either.

Corporate bond spreads did well, especially considering the violent move lower in all-in yields. While supply should pick up, CDX IG could break into the 50s and the Bloomberg Corporate OAS could dip into double digits (given potential supply, all-in yields, etc. I think that CDX has a better chance than actual bond spreads).

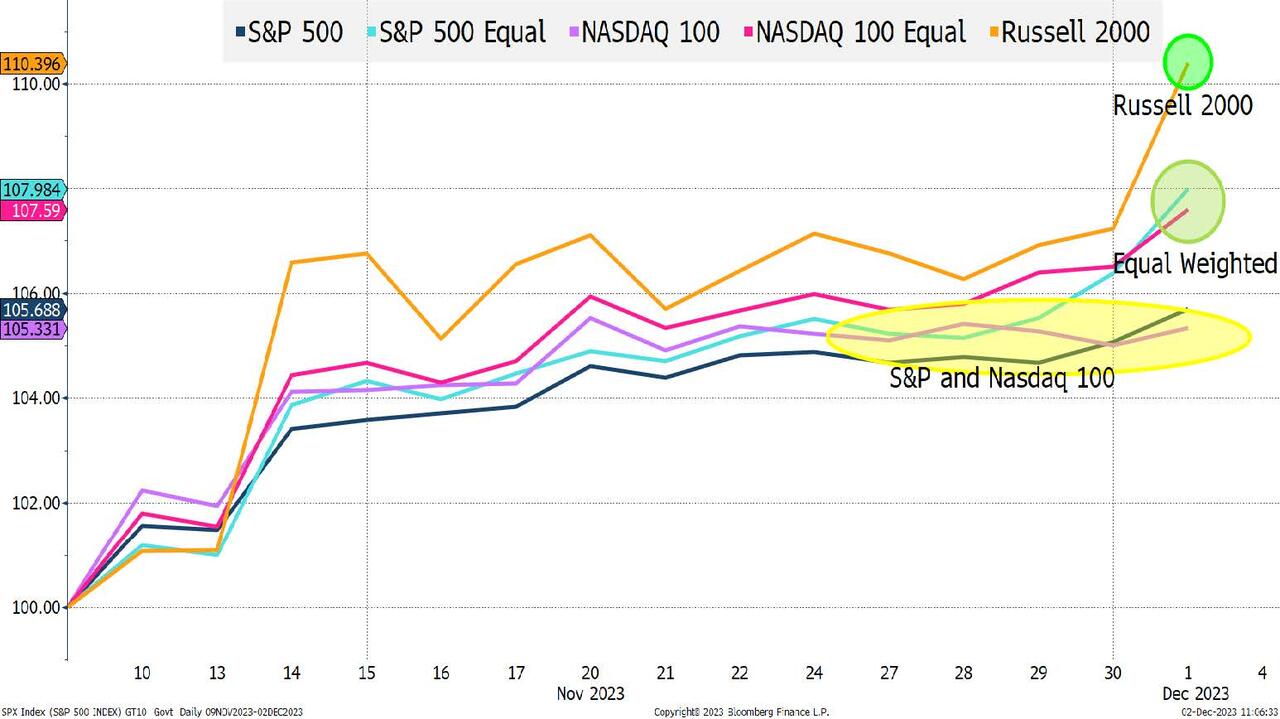

But one of the big stories remains the outperformance of the indices (and sectors) that were left behind.

On Bloomberg TV on Monday (1 hour 49 minute mark) we got to discuss several topics, but most importantly:

- The market leadership had already changed. We’ve been arguing for a few weeks that despite all the “Magnificent 7” chatter, leadership had already shifted. The market performance post-NVDA earnings solidified that view. See Rally on Garth! and Didn’t Learn Much.

- While 4.3% seemed like a bold call when the yield was at 5%, it was easy to see why equities would do well if that occurred. It is less clear why stocks should continue to do well as Treasuries head lower on fears of an economic slowdown. Having said that, the Nasdaq 100 is actually lower today than where it closed on November 22nd! The chart above is really important!

A Special Shout-Out to Small and Regional Banks!

Small and regional banks have done very well in the past few weeks. The reason for the “shout-out” is that the indices do not do justice to their strength. Most of the regional banks that I track are trading near or above their highest levels since March. The KBW index does not do justice to this performance, as it is still below the levels seen in July/August. My belief, and I haven’t fully verified it, is that the index is suffering from the fact that some very large holdings that contributed to the fall (Silicon Valley Bank, First Republic Bank) are not around to participate in the upswing. So, as much as I love indices (as a macro person), I think that the full picture behind the scenes is even better!

If It Wasn’t December…

Well, I’ve been waiting to drag Beavis and Butt-Head into the mix. It is one of the few things that I can think of that is more juvenile than Wayne’s World, but here we are.

- Beavis: Heh heh, heh.

- Butt-Head: Heh heh, you really going to short the market in December?

- Beavis: Heh heh, yeah!

- Butt-Head: Beavis, you’re stupid!

- Beavis: Heh heh, yeah!

I don’t think that is an actual scene, but it is the image that is playing in my head.

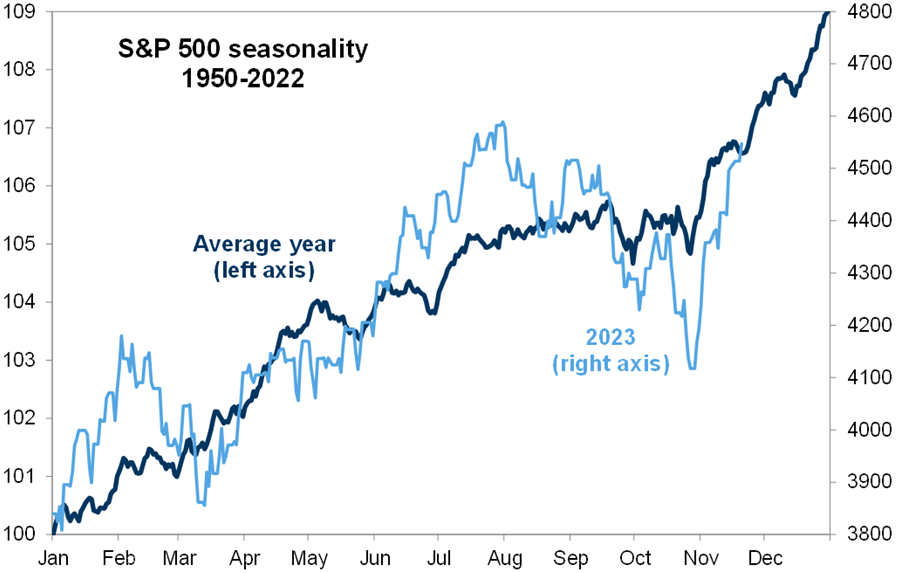

I hate the fact that “seasonality” seems to be a major factor driving markets. In an era of AI, it seems bizarre that something as “trite” as the Santa rally can be real, but it is tough to fight!

Though, as a warning, August traditionally is a “trend” month (it follows the trend leading into August) and this year August was a reversal month!

Could we get another “head-fake” on seasonality?

Yes, but could that turn into something as simple as the “market weighted indices” and “megacaps” continuing to be weak relative to the laggards? That does seem to be a potential “pain” trade for a lot of quant/algo driven funds.

Treasury Yields Are Lower for Many Reasons

More specifically, Treasury yields are lower for many of the wrong reasons.

- Fast money was too short at higher yields (good reason).

- People got too scared about supply too quickly (good reason), but supply and the deficit are not being fixed or addressed (bad reason).

- Signs that the economy is weakening, and the job market is cooling off (bad reason).

While some of the reduction in yields is for “good” reasons, I’m getting nervous about the upcoming economic data. We get job reports this week, which I expect to disappoint considering already mediocre expectations. Holiday sales (Black Friday and Cyber Monday) started strong, but how much was due to what seemed like aggressive discounting and how much just pulled shopping forward remains to be seen (that is the story that I expect).

Can Risk Assets Keep Rallying on Lower Treasury Yields?

Let’s not dismiss the possibility that yields could stabilize or even drift higher while stocks continue their upward pattern, led by the laggards (that is in the running for my base case).

Can risk assets keep rallying if the economy is slowing enough to drive bond yields lower? Normally, I would say no, but here are three reasons why we could see that occur for a bit longer.

- No one wants to say that the consumer is done consuming. Whether it’s wage growth, inflation, jobs, credit card debt, interest payments, the end of student loan moratoriums, etc., it doesn’t matter. There has been no “rational” reason for a dramatic slowdown in consumer spending. Analysts will NOT want to talk aggressively about consumption slowing until it is already obvious because it has been a call that has been wrong over and over again. So, if the consumer is slowing (my base case), the evidence will be fought for longer than normal.

- Few want to say that the recession is here or near. Much like the “death of consumption,” calling for a recession has been dangerous this year. However, there is some chatter about it again, as we’ve discussed and continue to believe. But analysts are facing “The Economist who Cried Recession” syndrome, which doesn’t make for great year-end discussions (whether with clients, or those paying your bonus), so recession fears will be downplayed. This means that markets can ignore signs more than they would have at this time last year.

- Pain. Pain will always play a role, and it often seems to play an outsized role in December. If this current relative value trade continues, it will continue for a couple of main reasons:

- Quant/Algo driven funds will continue to close out positions as stops are triggered.

- Managers who had thoughtfully positioned their portfolios to tell a great year-end story (how they were massively long the winners and underweight the losers) start to decide that story doesn’t sound as compelling as it did just a month or two ago and start rebalancing their portfolios so their year-end statements can capture this narrative.

- Seasonality. Okay, I said three reasons, but I can barely consider seasonality as a reason (though, it cannot be ignored). So, call it reason 3.5 (I’d insert a shoulder shrug emoji here if I knew how to do it).

While risk as a whole may stall, the relative outperformance trade should continue to work.

Bottom Line

Neutral to bearish on rates. Maybe the grind to lower yields continues. However, the market now seems long and has discounted supply (corporate and Treasury), thereby it is poised for a bit of a fade. Could we hit 4% before 4.5%? Sure, but I like 4.35% by the middle of next week ahead of the jobs data.

Neutral to mildly bullish on credit. Unlike rates, I think that the market still has some shorts positioned against it, and that some of the money allocated to distressed might have to “redefine” distressed so that they can enter the market. However, the “easy” money in credit is over. So on credit, maybe be long the “wings” barbelling your portfolio with some very high quality names (A+ and above) and some stressed names (B- and below) skewed to the leveraged loan side of things.

Slightly bullish on equities, but very bullish on the laggards! Our target for the S&P 500 got bumped to 4,650 from 4,600 (a good thing, as we are there), but I cannot justify raising it further with everything going on. On the other hand, I could see the Russell 2000 popping another 5% to 8% in the coming weeks (that would take it to a 12% to 15% return on the year, which doesn’t seem unreasonable given where the other indices are). On the sector side of things, biotech, regional banks, and even “disruptive” tech seem appealing for a trade.

A wildcard that I think could occur (and would really let the “everything” rally continue robustly) would be some sort of a “deal” with China. It could be something as simple as a path to lower tariffs (many of the economists who seem to advise Biden were originally very negative on tariffs), a clarification on what tech is allowed or not (I assume that there is some strong lobbying going on here), or using our advantage in food production to generate something interesting. We should probably expect “promises” more than anything tangible from China (i.e., I think that it will be a one-sided “deal”), but it should be “deflationary” and “growth-oriented” at the same time and something that markets should love!

A second wildcard is that the potential for escalation in the Middle East has increased as Israel has renewed its attacks on Hamas. While escalation is not our current base case, it is a threat that wasn’t as much of a threat last week.

The final wildcard is AI, but that seems like a late Q1, or even Q2 type of event (see Didn’t Learn).

It seems like the “silly” season is here, but things are likely to get sillier! However, I suspect that we will have an opportunity to short these markets before year-end, just not yet (except for maybe Treasuries, which can be shorted already).

Tyler Durden

Sun, 12/03/2023 – 13:00

via ZeroHedge News https://ift.tt/loQrNJ5 Tyler Durden