Stocks, Futures Slide For Second Day As Rally Fizzles Ahead Of Jobs Data Deluge

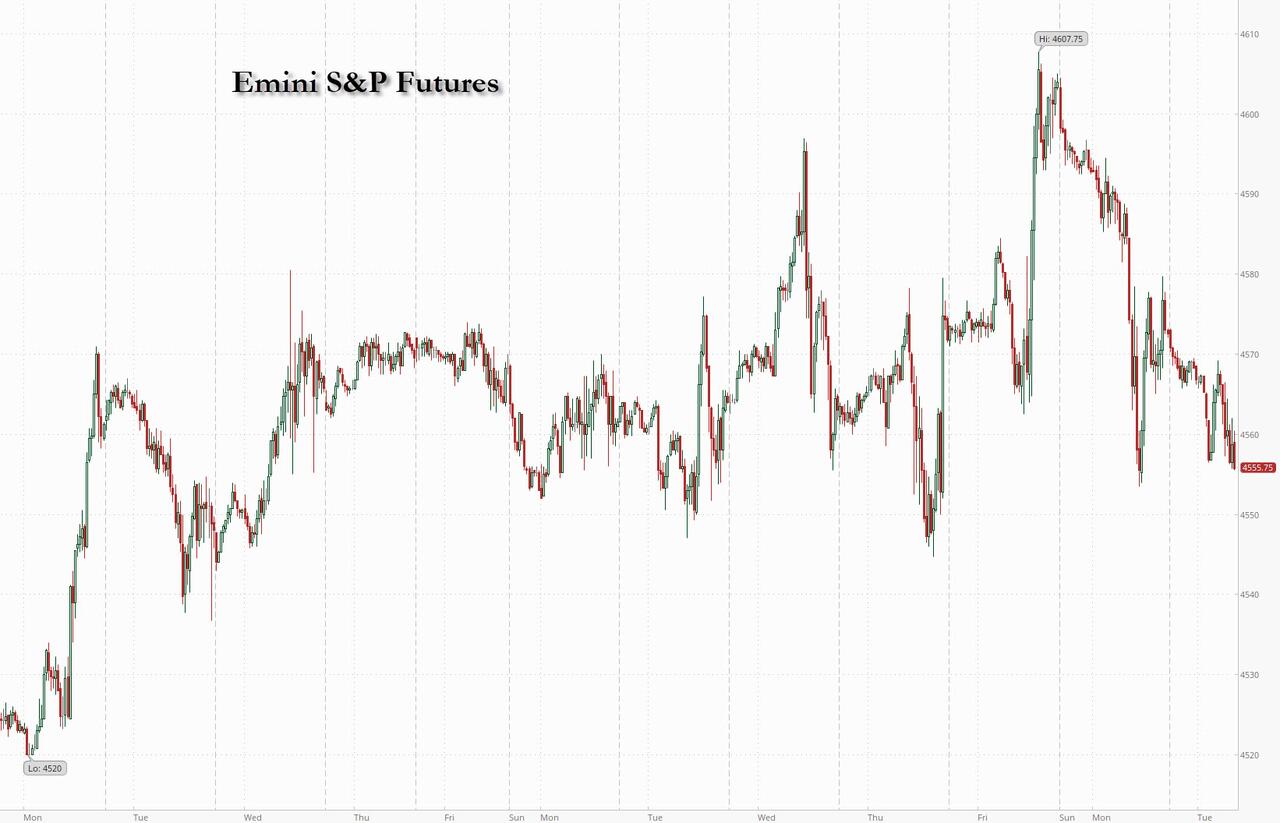

US stocks were set to extend Monday’s drop into a second day after hitting 20-month highs, as the recent rally looks increasingly stretched and traders scale back rate-cut bets while Chinese stocks tumbled to fresh five year lows after Moody’s downgraded China’s credit outlook to negative on soaring debt. As of 7:40am ET, S&P 500 futures slid 0.4%, trading at session lows, after the benchmark rose last week to its highest since March 2022 on bets the Fed would soon pivot to monetary easing; Nasdaq 100 futures dropped 0.5%. Bond yields eased as did the USD; 10Y TSY yield dropped 2bps to 4.22%. Commodities were seeing a bid within Ags and Energy while metals underperformed on China weakness despite better than expected PMIs. Bitcoin held near a 19-month high, just below the $42,000 mark.Today’s macro data focus is on JOLTS job openings and ISM Services (52.3 consensus vs. 51.8 prior).

In premarket trading, Take-Two Interactive shares declined after the company’s Rockstar Games unit released the first trailer for the highly-anticipated Grand Theft Auto VI video game. With the title planned for 2025, analysts were disappointed by the lack of an exact release date. Robinhood gained after the online brokerage said November crypto notional trading volumes were about 75% above October levels. Here are some other notable premarket movers:

- Albemarle and Livent fell after Piper Sandler cut its rating on both stocks to underweight from neutral. The broker said the downgrades reflect a significant deterioration of global lithium markets.

- Gitlab jumped 16% as after the application software company reported third-quarter results that beat expectations and raised its full-year forecast.

- JOANN shares slumped 18% after the fabric and crafts retailer reported third-quarter net sales that missed estimates and a wider-than-expected adjusted loss per share.

- Nio ADRs gained 3.1% after the Chinese EV maker reported profitability that beats estimates, including better-than-expected adjusted earnings and vehicle gross margin. Revenue outlook for current quarter is well below estimates.

- Take-Two Interactive shares declined 6.1% after the company’s Rockstar Games unit released the first trailer for the highly-anticipated Grand Theft Auto VI video game, which will be released in 2025. While analysts saw the trailer as positive, they note the game being released in 2025 and the lack of an exact release date as a source of disappointment.

As November’s epic 12% rally on hopes that global central bankers were ready to shift to easy policy fizzles, investors are starting to doubt if it will extend in December especially after Goldman’s flows guru Scott Rubner warned that the rally has “Absolutely Run Out Of Gas.” As such, what had become the prevailing wisdom last month — that a “Goldilocks” scenario can be fulfilled by US central bankers in early, rapid rate cuts in 2024 — is now grounds for debate. US jobs data later in the week is seen as a key piece of the puzzle to understanding the economy and the risk that wage growth fans inflation, leading to higher borrowing costs for longer. A salvo of US job numbers are expected every day for the rest of week, including JOLTS, ADP, jobless claims, non-farm payrolls and the unemployment rate.

“Even though US PMI and JOLTs data may increase market volatility in the afternoon, the “wait and see” stance will likely continue as investors brace for the crucial US jobs data due tomorrow and Friday,” said Pierre Veyret, a technical analyst at ActivTrades. “Meanwhile, a particular focus should be maintained towards central bankers’ speeches, as traders need to check whether their dovish expectations will be confirmed.”

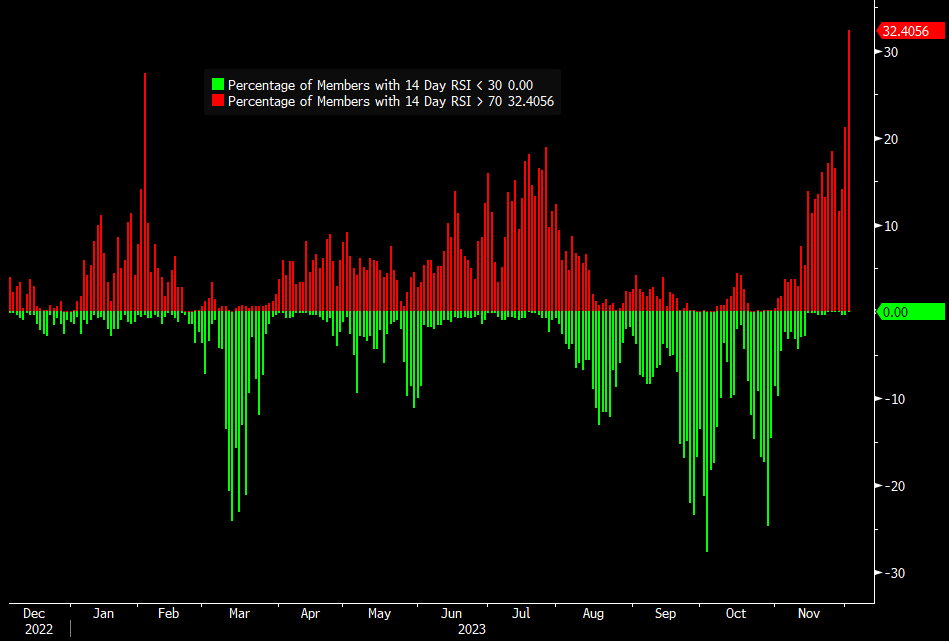

Meanwhile, market breadth on the S&P 500 now looks extremely extended with the benchmark now firmly overbought for more than two weeks, while Goldman pointing out that the proportion of index members in overbought territory reached 33%, the highest reading since June 2020.

“It’s remarkable how quickly we’ve swung from different market narratives this year,” Hugh Gimber, global market strategist for JPMorgan Asset Management in London, said in an interview on Bloomberg Television. “Now it feels like we’ve gone full circle again.”

European stocks were mixed and US equity futures are down after Moody’s downgraded China’s sovereign debt outlook to negative. Euro Stoxx 50 rises 0.3%. IBEX outperforms peers, adding 0.5%, FTSE 100 lags, dropping 0.4%, after LSE faced issues earlier. Real estate, utilities and construction are the strongest-performing sectors in Europe. German markets got a boost from comments from European Central Bank policymaker Isabel Schnabel that further interest rate hikes are unlikely. The DAX Index added 0.2%, closing in on a record high and outperforming the broader Stoxx 600. Here are the biggest movers Tuesday:

- Ericsson rises as much as 9.9%, among the top performers on the Stoxx 600, after winning a contract with AT&T that could amount to almost $14 billion over five years. Nokia, which lost out on the contract, fell as much as 10%

- SSP Group gains as much as 4.9% after the food services company boosted its 2024 revenue guidance. The guidance should be “reassuring” for the outlook of travel retail, RBC said

- Pirelli shares rise as much as 6%, the most intraday in a year, after UBS upgraded the Italian tiremaker to buy, citing earnings upside risk, deleveraging potential and an attractive valuation

- Alm Brand gains as much as 5.9% after the Danish financial services firm announced a DKK250 million share buyback program due to its “very strong solvency coverage”

- Moonpig shares advance as much as 3.5% after the onling gifting company reported first-half underlying Ebitda and adjusted earnings per share that beat estimates

- Hapag-Lloyd and Maersk decline as Barclays says the global shipping market faces “the dawn of a new annus horribilis” due to industry oversupply and muted demand

- Ashtead falls as much as 5.4% after the UK-based industrial and construction equipment rental firm reported 2Q earnings. While the results were solid, they may not reassure fully, RBC says

- Carl Zeiss Meditec drops as much as 4.9% after JPMorgan initiated coverage on the German medical optics firm with an underweight rating

- Auction Technology drops as much as 6.2% after Barclays downgraded its rating on the online auction technology provider to equal-weight, citing a more cautious view in the near term

Earlier in the session, Asian stocks tumbled and were on pace for their worst day since Nov. 20 as sharp selling in Chinese and Hong Kong shares hurt sentiment. The MSCI Asia Pacific Index slid as much as 1.1%, with Tencent, Samsung Electronics and AIA Group leading losses. Mainland China and Hong Kong stocks slumped in the wake of a move by Moody’s Investors Service to cut its outlook on the nation’s sovereign debt to negative. The MSCI China Index slid as much as 2.3% toward its lowest close since November 2022. On the mainland, the benchmark CSI 300 Index finished 1.9% lower as foreigners sold the largest amount of shares since mid-October. Sentiment was also dragged by a selloff in technology stocks across the region, tracking similar losses for US tech giants Monday. The MSCI Asia Information Technology Index fell the most since October.

“The accumulation of news over last few weeks would be raising questions on China’s economy into 2024,” said Xin-Yao Ng, an investment director for Asian equities at abrdn. “Macro data has been soft. The big concern over the property slump remains as sales volume are still very weak.”

- Hang Seng and Shanghai Comp retreated which saw the latter breach the psychological 3,000 level to the downside amid lingering frictions after China criticised the US for seeing it as a threat following calls by Commerce Secretary Raimondo for more funds to back chip curbs, while encouraging Caixin Services PMI data which printed a 3-month high at 51.5 (exp. 50.7) only provided a brief tailwind.

- Nikkei 225 continued to weaken and slipped below the 33,000 level despite softer-than-expected Tokyo inflation data.

- ASX 200 was led lower by the commodity-related industries with underperformance in gold miners after the precious metal faded the recent surge, while sentiment was also not helped by weak data and after the unsurprising RBA rate decision in which the central bank kept rates unchanged and reiterated its forward guidance.

In FX, the Bloomberg dollar spot index was steady. JPY and GBP were the strongest performers in G-10 FX, AUD and NZD underperformed.

- EUR/USD pared a loss of 0.3% to trade flat at 1.0839, after the ECB’s Schnabel said that the moderation in inflation has made another rate hike unlikely; euro-area bonds rallied

- AUD/USD sank as much as 0.8% to 0.6569, a one-week low, after the Reserve Bank left its policy rate unchanged and said inflation is continuing to slow

- USD/CNH and USD/CNY steadied following Moody’s cut to its Chinese debt outlook to negative

In rates, treasuries held small gains amid steeper rally in bunds after ECB’s Schnabel said she sees further rate hikes as unlikely, citing a “remarkable” fall in inflation, according to Reuters. US yields are richer by 1bp-2bp across the curve with spreads flatter but still within 1bp of Monday close; 10-year yields around 4.23% with bunds and gilts outperforming by 3bp in the sector as core European rates drive gains. German bonds rose, with the front end outperforming comparable USTs and gilts, and money markets up their ECB easing bets after ECB’s Isabel Schnabel said that further interest rate hikes are unlikely. Peripheral spreads tighten to Germany. Dollar IG issuance slate includes JPMorgan 3Y and IADB 3Y; seven names priced almost $9b Monday and at least one stood down. Treasury coupon issuance is on hiatus until next week’s 3-, 10- and 30-year sales. US session includes ISM services index and JOLTS job openings data.

In commodities, oil steadied after three days of losses. Saudi Arabia said recent cuts by OPEC+ would be honored in full and could be extended. Most base metals trade in the red. Spot gold falls roughly $3 to trade near $2,027/oz.

Bitcoin held near a 19-month high, just below the $42,000 mark.

To the day ahead now, and data releases from the US include the ISM services index for November, and the JOLTS job openings for October. Elsewhere, there’s the global services and composite PMIs for November and Euro Area PPI for October. From central banks, we’ll get the ECB’s Consumer Expectations Survey for October.

Market Snapshot

- S&P 500 futures down 0.2% to 4,566.50

- STOXX Europe 600 up 0.1% to 466.33

- MXAP down 1.0% to 159.84

- MXAPJ down 1.1% to 497.42

- Nikkei down 1.4% to 32,775.82

- Topix down 0.8% to 2,342.69

- Hang Seng Index down 1.9% to 16,327.86

- Shanghai Composite down 1.7% to 2,972.30

- Sensex up 0.6% to 69,290.91

- Australia S&P/ASX 200 down 0.9% to 7,061.55

- Kospi down 0.8% to 2,494.28

- German 10Y yield little changed at 2.30%

- Euro little changed at $1.0840

- Brent Futures up 1.1% to $78.85/bbl

- Gold spot up 0.1% to $2,030.89

- U.S. Dollar Index down 0.10% to 103.60

Top Overnight News

- Moody’s lowered China’s credit outlook to negative from stable while retaining a long-term rating of A1 on the nation’s sovereign bonds, according to a statement. China’s usage of fiscal stimulus to support local governments and its spiraling property downturn is posing risks to the nation’s economy, the grader said. BBG

- China’s Caixin services PMI for Nov comes in ahead of plan at 51.5, up from 50.4 in Oct and above the Street’s 50.5 expectation. RTRS

- Japan’s Tokyo CPI undershoots the Street in Nov, w/the core (ex-food/energy) number coming in at +3.6% (down from +3.8% in Oct and below the Street’s +3.7% forecast). BBG

- South Korea’s CPI undershoots the Street in Nov, with the core number coming in at +3% (down from +3.2% and below the Street’s +3.1% forecast). BBG

- The ECB can take further interest rate hikes off the table given a “remarkable” fall in inflation and policymakers should not guide for rates to remain steady through mid-2024, ECB board member Isabel Schnabel told Reuters. RTRS

- Qatar Holding, a subsidiary of the Qatar Investment Authority that helped bail out Barclays during the global financial crisis, launched the sale on Monday of almost 362mn shares of Barclays, worth about £510mn. The QIA is Barclays’ second-biggest shareholder, according to Bloomberg data, and the stock sale is expected to reduce its stake from 5.3% to 2.9%. FT

- The head of Airbus has said the group “might need some support” from European governments for a new, multibillion-dollar commercial aircraft program as it gears up for a successor to its best-selling A320 family of jets. FT

- Israeli forces closed in on the city of Khan Younis in the Gaza Strip on Tuesday, engaging in close combat with Hamas fighters in what could be the decisive battle of the two-month-old war, while residents fled from the fighting amid a worsening humanitarian plight. WSJ

- CVS Health will overhaul how drugs are paid for, adopting a “cost plus” model whereby it will charge a simple markup and a flat fee on top of what it pays for pharmaceuticals. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined following the mostly negative lead from Wall St where the major indices were choppy and ultimately weighed amid a rebound in yields ahead of key data releases. ASX 200 was led lower by the commodity-related industries with underperformance in gold miners after the precious metal faded the recent surge, while sentiment was also not helped by weak data and after the unsurprising RBA rate decision in which the central bank kept rates unchanged and reiterated its forward guidance. Nikkei 225 continued to weaken and slipped below the 33,000 level despite softer-than-expected Tokyo inflation data. Hang Seng and Shanghai Comp retreated which saw the latter breach the psychological 3,000 level to the downside amid lingering frictions after China criticised the US for seeing it as a threat following calls by Commerce Secretary Raimondo for more funds to back chip curbs, while encouraging Caixin Services PMI data which printed a 3-month high at 51.5 (exp. 50.7) only provided a brief tailwind.

Top Asian News

- RBA kept the Cash Rate Target unchanged at 4.35%, as expected, while it reiterated its forward guidance that whether further tightening is required to ensure inflation returns to the target in a reasonable timeframe will depend upon data and evolving assessment of risks. RBA also repeated that the Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome, as well as noted there are still significant uncertainties around the outlook and that the limited information received on the domestic economy since the November meeting has been broadly in line with expectations.

- Moody’s affirms China’s A1 rating; changes outlook to Negative from Stable. Reflects risks relating to persistently lower medium-term economic growth and ongoing downsizing of the property sector.

- Chinese Finance Ministry says Chinese economy will maintain its rebound and positive trend; we expect the Q4 economy to keep the positive trend

- Foxconn (2317 TW) November Sales +17.95% Y/Y (October -4.56% Y/Y); outlook for Q4 should be better than the original guidance for “significant growth”; revenue performance in the first two months of Q4 has been slightly higher than expected

European equities, Eurostoxx50 +0.3%, are mixed, with the FTSE100, -0.2%, once again the relative underperformer, largely hampered by ongoing losses in Basic Resources which is the worst performing sector. European sectors are mixed with a slight positive tilt; Real Estate outperforms following broker upgrades at British Land, +1.3%, and Land Securities, +0.8%. US equity futures are trading on the backfoot, continuing the losses seen in the prior days’ session as the year’s final few key events/releases begin with JOLTS.

Top European News

- ECB’s Schnabel says current level of restriction is sufficient, has increased confidence that 2% target will be met in 2025; must not declare victory prematurely; further hikes “rather unlikely” after November inflation data. Must be more cautious with rate cuts than markets pricing; further hikes “rather unlikely” after November inflation data. Inflation developments are encouraging, fall in core prices is remarkable

- YouGov/Citi survey showed the British public’s expectation for inflation in 5yr-10yr’s time rose to 3.5% from a prior 3.3% view in September.

- German Ifo: Retailers Expect Little Help from Christmas Sales; Business Situation -8.8 (prev. -13.5).

- Kantar UK Supermarket update (Nov): grocery price inflation 9.71% in the four weeks to Nov 26th; UK grocery sales +6.3% Y/Y.

- ECB Survey of Consumer Expectations (October 2023): median consumer inflation expectations for the next 12 months and for three years ahead remained unchanged.

- The London Stock Exchange (LSEG LN) is currently investigating an issue impacting its trading/information system. We are now resuming trading on impacted instruments. Instruments will go into auction at 09:55GMT with uncrossing beginning at 10:15GMT. All live orders remain on the system. LSE: Impacted securities are now in regular trading.

FX

- DXY extended on the upper end of its overnight range towards 103.84 ahead of the European equity cash open and now resides within the middle of today’s range of 103.84-53.

- EUR/USD is trading around flat having bounced off lows on revisions higher to Services & Composite PMI data.

- The Japanese Yen is the G10 outperformer at the time of writing amid a combination of a pullback in US yields coupled with the broader risk aversion overnight.

- AUD, NZD, CAD are all softer to varying degrees amid the initial broader risk tone, but the Aussie is the marked G10 laggard in the aftermath of the RBA policy decision which lacked hawkish undertones.

- PBoC set USD/CNY mid-point at 7.1127 vs exp. 7.1476 (prev. 7.1011).

- China’s major state-owned banks were seen acquiring dollars via onshore swaps and selling them in the spot FX market, while it was also reported that the RBI was likely selling dollars near the 83.38-83.39 rupee level, according to sources and traders cited by Reuters.

Fixed Income

- ECB’s Schnabel (Hawk) says that further hikes are now “rather unlikely” following the November inflation data.

- Commentary which drove Bunds to a 134.17 peak; though, upward revisions to PMIs have prompted a pullback, but one that is limited by the reports internal commentary.

- Similar action has been seen in Gilts which perhaps derived initial support from the latest YouGov findings as well.

- Finally, USTs are directionally in-fitting but with magnitudes more contained at the mid-point of 110.10 to 110.18 parameters ahead of JOLTS & PMIs/ISM.

- UK sells GBP 1.5bln 0.75% 2033 I/L Gilt: b/c 2.68x (prev. 2.94x) and real yield 0.724% (prev. 0.831%)

- Germany to sell EUR 3.66bln vs exp. EUR 4.5bln 3.10% 2025 Schatz: b/c 2.48x (prev. 1.7x), average yield 2.64% (prev. 3.06%), retention 18.67% (prev. 17.82%)

Commodities

- WTI and Brent, +0.7%, front-month futures are on firmer footings after choppy trade on Monday amid continued fallout from OPEC+ in the backdrop of cooling economic data and volatile Middle East tensions.

- Metals are mixed with precious metals moving horizontally as the DXY trades flat intraday spot gold and spot silver taking a breather following yesterday’s hefty losses.

- Libya’s NOC Chair says current production is 1.3mln BPD (vs 1.218mln on 6th Nov), planning a bidding round for offshore/onshore blocks for end-2024. In the early stage to identify blocks. Says seeing a lot of interest for upcoming bid round from US, European and Asian firms. On track to increase production capacity to 2mln BPD in the next three-five years. Says hopefully oil production will increase by 100k BPD by end-2024.

- Russia’s Kremlin, when asked if Russian President Putin will discuss coordinated actions on oil market, says such discussions are held in OPEC+ format but the issue is always on the agenda; Kremlin confirms Putin will visit Saudi and UAE on Wednesday. Russian President Putin is to discuss oil market issues in the UAE and Saudi Arabia, according to Tass

- Brazilian miner Vale expects iron ore market to remain tight in the coming years, says China cannot control the price of iron ore and there is no supply coming

- China’s NDRC will cut retail gasoline and diesel prices by CNY 55/ton and CNY 50/ton, respectively, commending Dec 6th; NDRC sees weaker oil prices in the short term

Geopolitics

- Israel is reportedly mulling a plan to flood Gaza tunnels with seawater, according to WSJ.

- Israel’s army said its fighter jets attacked Hezbollah positions, infrastructure and military in response to a recent shooting, according to AJA Breaking via social media platform X.

- Investors with prior knowledge of the October 7th attack on Israel by Hamas made at least tens of millions of pounds shorting Israeli stocks, according to The Telegraph.

- US National Security Advisor Sullivan said attacks on vessels in the Red Sea are a threat to international peace and stability, while they have every reason to believe these attacks were fully enabled by Iran. Sullivan also said the US is engaging with allies on the next steps after the Red Sea attacks and weapons used by the Houthis in the attacks are being supplied by Iran.

- White House warned that a failure to approve additional aid for Ukraine would ‘kneecap’ Kyiv, according to FT.

US Event Calendar

- 09:45: Nov. S&P Global US Services PMI, est. 50.8, prior 50.8

- 10:00: Oct. JOLTs Job Openings, est. 9.3m, prior 9.55m

- 10:00: Nov. ISM Services Index, est. 52.3, prior 51.8

- Nov. ISM Services New Orders, est. 54.9, prior 55.5

- Nov. ISM Services Employment, est. 51.4, prior 50.2

- Nov. ISM Services Prices Paid, est. 58.0, prior 58.6

DB’s Jim Reid concludes the overnight wrap

Markets have lost a little of their recent poise over the last 24 hours, with the S&P 500 (-0.54%) coming off its YTD high from Friday, just as yields on 2yr Treasury yields (+9.6bps) moved back up to 4.64%. There hasn’t been a specific catalyst for the softness, but the astonishing rally in November and long positioning has led to some scepticism about how much further it’s able to run, at least until we get some more data that’s soft-landing friendly. After all, even though markets are fully pricing in a Fed rate cut by the May meeting in just 5 months’ time, this isn’t the first time this year that rate cut speculation has built up. In fact, at the height of the SVB turmoil in March, futures were fully pricing in a rate cut by the July meeting, which was just 4 months away. So it’ll be fascinating to see the extent to which the FOMC’s dot plot next week validates or pushes back on current market pricing, which is now looking for 124bps of cuts in 2024 .

When it comes to the Fed’s next meeting, today kicks off a run of important data releases that will help shape the 2024 outlook. That includes the ISM services index, which will be in particular focus after the manufacturing number underwhelmed on Friday. Indeed, the Atlanta Fed’s GDPNow forecast for Q4 stands at just 1.2%, which if realised would be the weakest quarterly growth since Q2 2022. Alongside that, we’ll get the JOLTS report for October, which have shown job openings actually ticking back up over the last couple of months, suggesting that the labour market was still pretty tight. For instance, there were still 1.5 job vacancies per unemployed individual in September, which is still clearly above its pre-pandemic level around 1.2. We’ll see if that’s changed today.

Ahead of those releases, the S&P 500 (-0.54%) was unable to sustain its recent gains, suffering its worst start to a week since February. To be fair, it’s worth noting that the decline was fairly concentrated among big tech stocks, with the equal-weighted S&P 500 up a marginal +0.03%. And the small cap Russell 2000 index (+1.04%) actually rose for the fourth session in a row. But even so, it wasn’t much consolation for those segments that did lose ground, with both the NASDAQ (-0.84%) and the Magnificent 7 (-1.61%) seeing a notable underperformance .

Meanwhile on the rates side, there was a fairly sharp bounceback in Treasury yields following last week’s declines. The 10yr yield rose +5.8bps to 4.21%, though it rallied in the latter part of the US session having been up as much as +10bps intra-day. There were larger moves at the front-end as the 2yr yield (+9.6bps) saw its biggest daily increase in four weeks, moving back up to 4.63%. That came as investors took out some of the cuts priced in for 2024, with the total amount falling by -10.2bps to 124bps. And in turn, with investors expecting slightly fewer rate cuts, real yields also bounced back, with the 10yr real yield (+7.2bps) moving back above 2% again .

That advance in real yields put a pause to the gold rally over recent days. At the open, gold prices did manage to hit an all-time intraday high of $2135/oz, but by the close they were down a full -2.23% to $2026/oz. So a 5.56pp range on the day, which is a huge intra-day swing for Gold. Although we hit fresh all-time highs during the session, it’s worth noting that this is still only a nominal high point, since if you adjust for inflation then prices were higher in the early 1980s, in 2011, and even at the recent peak in 2020. Elsewhere in the commodities space, Brent Crude oil prices (-1.08%) were down again to $78.03/bbl, building on their run of 6 consecutive weekly declines .

Over in Europe, the market moves were much less aggressive yesterday, with the STOXX 600 only falling -0.09%. Similarly for sovereign bonds, yields on 10yr bunds (-0.8bps) actually fell back to a 5-month low of 2.35%, and others including 10yr OATs (+0.2bps) and BTPs (+2.5bps) only saw a modest increase. Gilts were the main exception to that pattern, with the 10yr yield up +5.5bps, as the 10yr real yield (+9.6bps) even hit a one-month high.

Asian equity markets are slipping this morning with the Hang Seng (-1.76%) emerging as the biggest underperformer followed by the Nikkei (-1.15%), the CSI (-0.80%), the Shanghai Composite (-0.69%) and the KOSPI (-0.38%). S&P 500 (-0.21%) and NASDAQ 100 (-0.24%) futures are edging lower.

Early morning data showed that Tokyo’s inflation rate rose by +2.6% y/y in November (v/s +3.0% expected), its slowest rise since July 2022 and compared with a downwardly revised increase of +3.2% in the previous month. Core CPI rose +2.3% in November (v/s +2.4% expected) from a year earlier down from a +2.7% gain in October thus clouding the BOJ’s exit path a touch. The BOJ next meet on Dec. 18-19 with our view that they will remove YCC in January. Elsewhere, China’s Caixin services PMI for November advanced to a three-month high of 51.5 (v/s 50.5 expected and 50.4 in October), thus diverging from the nation’s official PMI data that showed a contraction .

In monetary policy action, the Reserve Bank of Australia (RBA) decided to keep its official cash rate (OCR) unchanged at a 12-year high of 4.35% as consensus expected at its final board meeting of 2023. With the RBA’s statement viewed as being on the dovish side, the Aussie currency has come under renewed selling pressure, dropping -0.54% to trade at 0.6584 versus the dollar .

Looking back at yesterday’s data, October factory orders were the one notable release in the US. These saw a -3.6% monthly decline (vs -3.0% exp) and with September revised down to +2.3% from +2.8%. The less volatile non-defense capital goods series was revised down to -0.2% from 0.0% in the advance reading. So adding to a sense of weakening US growth momentum in Q4.

To the day ahead now, and data releases from the US include the ISM services index for November, and the JOLTS job openings for October. Elsewhere, there’s the global services and composite PMIs for November and Euro Area PPI for October. From central banks, we’ll get the ECB’s Consumer Expectations Survey for October.

Tyler Durden

Tue, 12/05/2023 – 08:16

via ZeroHedge News https://ift.tt/gdyr3uv Tyler Durden