US Treasury Rally Is Starting To Look Long In The Tooth

By Simon White, Bloomberg Markets Live reporter and strategist

The rally in Treasuries is beginning to look tired. Yields are moving in lock-step with short-term rate-cut expectations, which are looking overcooked given the loosening in financial conditions has likely helped push the timing of the next NBER recession further out.

Treasuries are becoming progressively overbought after an impressive rally of over 5% since mid-October. The rally was not unexpected as it came off oversold conditions, but the pendulum has, as usual, swung too far in the other direction, where the drop in yields is hard to square with economic expectations.

The Treasury rally has been augmented by the Federal Reserve opening the door to rate cuts next year. Longer-term yields in theory should factor in the short-term rate cycle as well as future rate cycles, and other longer-term risks such as inflation.

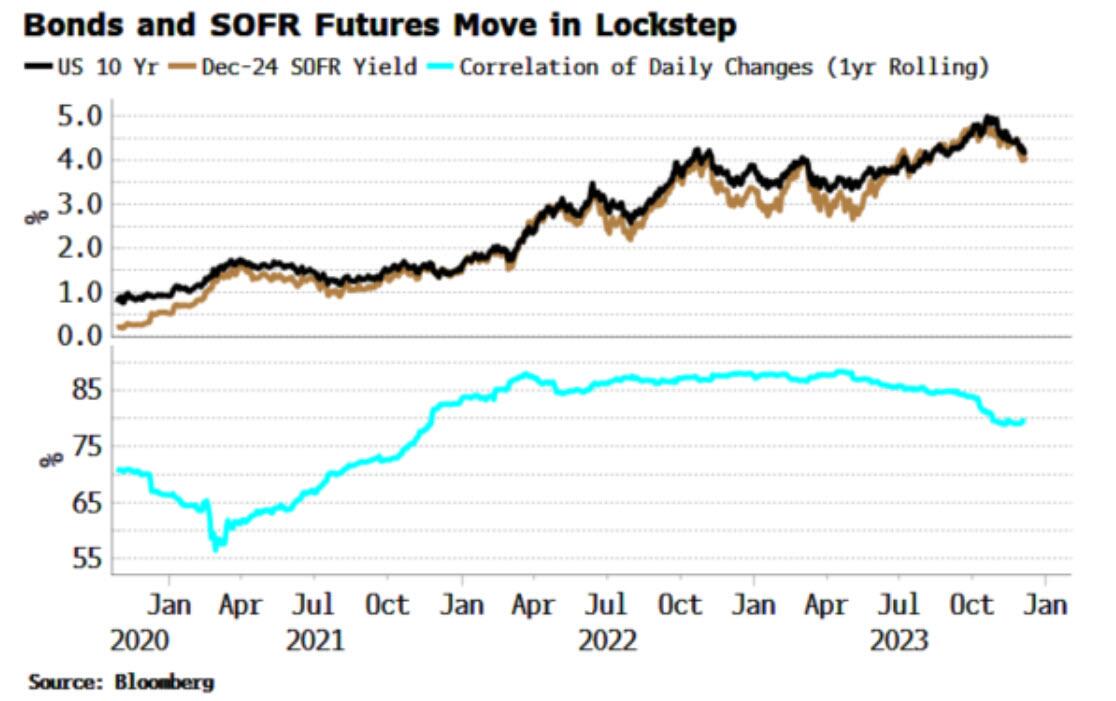

In practice, though, longer-term yields move almost in lockstep with shorter-term rates. The chart below shows the very close relationship between the December 2024 SOFR and the 10-year yield. The correlation between the two is 80% (for a correlation of daily changes, that’s high).

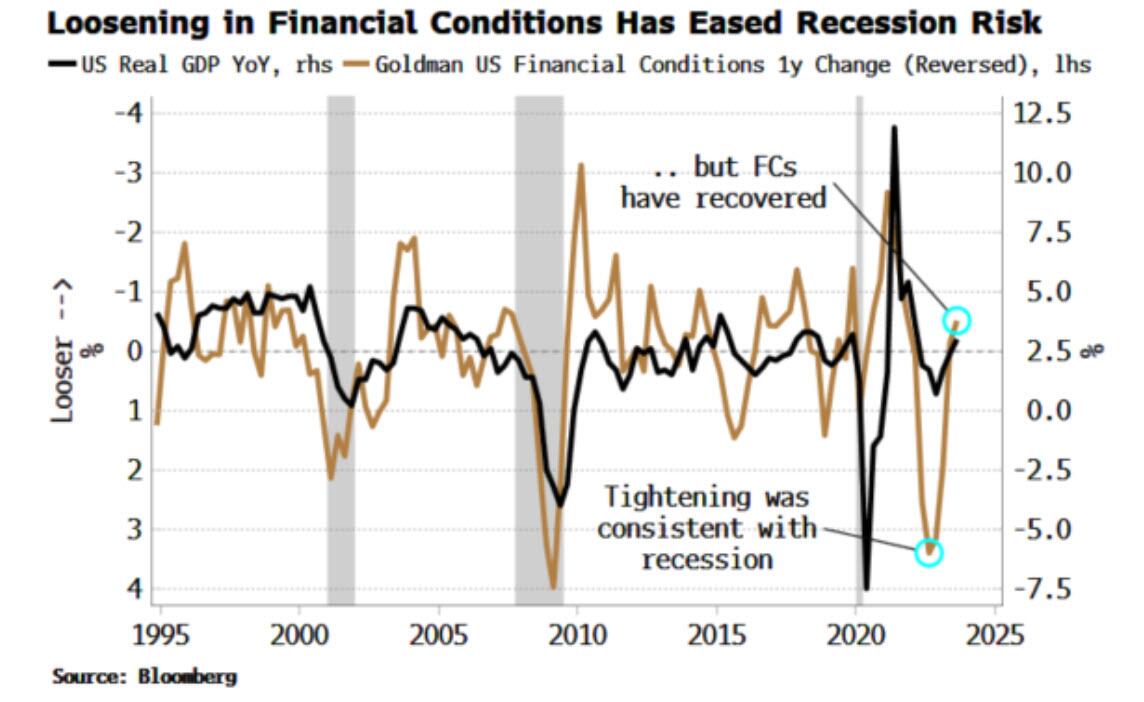

Yields have fallen with the zeal of Fed rate-cut pricing. But the “everything rally” this has undergirded has led to a sizeable loosening in financial conditions. The implied rate cut from this loosening (based on Goldman Sachs’ Financial Conditions Index) looks like it may have already helped push a NBER recession further out.

The tightening in financial conditions last year and earlier this year that was historically consistent with previous recessions has been completely reversed. This chart suggests we will need to see a re-tightening of financial conditions before a recession.

As noted on Monday, positioning in Treasuries is potentially quite long (based on JPM’s survey of active clients). Further, it would almost be unprecedented for the Fed to cut by as much as the market currently anticipates, outside of a recession. Bloomberg Intelligence rate strategists think the market may be in for a shock if the Fed sticks to its guns at next week’s meeting:

A short UST view is not exactly contrarian, but that doesn’t detract from the fact that current rate-cut expectations — and therefore yields — require more bad news, and soon, as well as a supportive Fed. Also notable was the failure of USTs to extend their rise after a weak JOLTS report on Tuesday (even though it should be treated with great skepticism).

Tyler Durden

Wed, 12/06/2023 – 10:00

via ZeroHedge News https://ift.tt/FlrXhkO Tyler Durden