Q4 GDP Unexpectedly Soars, Driven By Lack Of Destocking And An RV Spending Spree

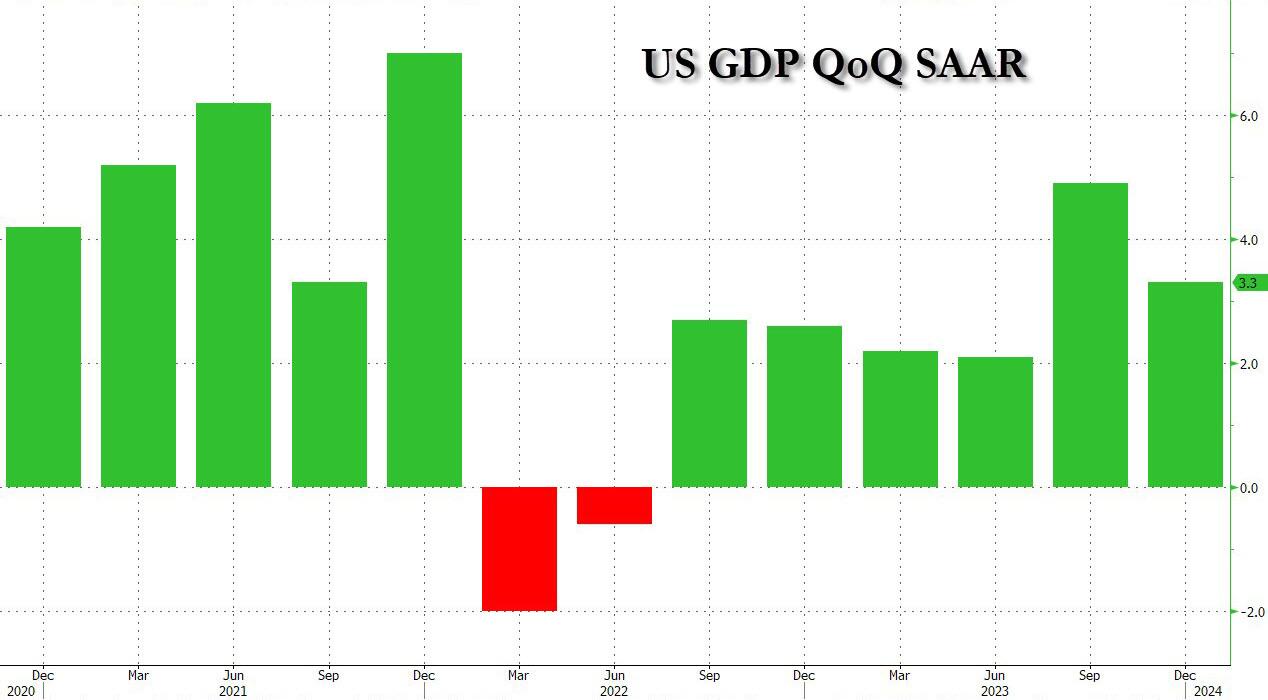

With economist and Wall Street strategists confident that in the fourth quarter US growth would slow sharply after the inventory accumulation-driven Q3 surge which saw the economy explode by 4.9% (down from a 5.2% initial print), moments ago Biden’s Bureau of Economic Analysis once again shocked everyone when it reported that in Q4, the US economy actually grew by 3.3% (3.280% to be precise)…

… which was not only above the median consensus of 2.0%, not only above the highest Wall Street estimate of 2.5%, but it was a 5-sgima beat to expectations!

So how can literally everyone on Wall Street be this wrong, and what the hell was Biden’s BEA cooking?

Well, according to the official report, “the increase in the fourth quarter primarily reflected increases in consumer spending and exports. Imports, which are a subtraction in the calculation of GDP, increased.“

Reading down the report we find the following:

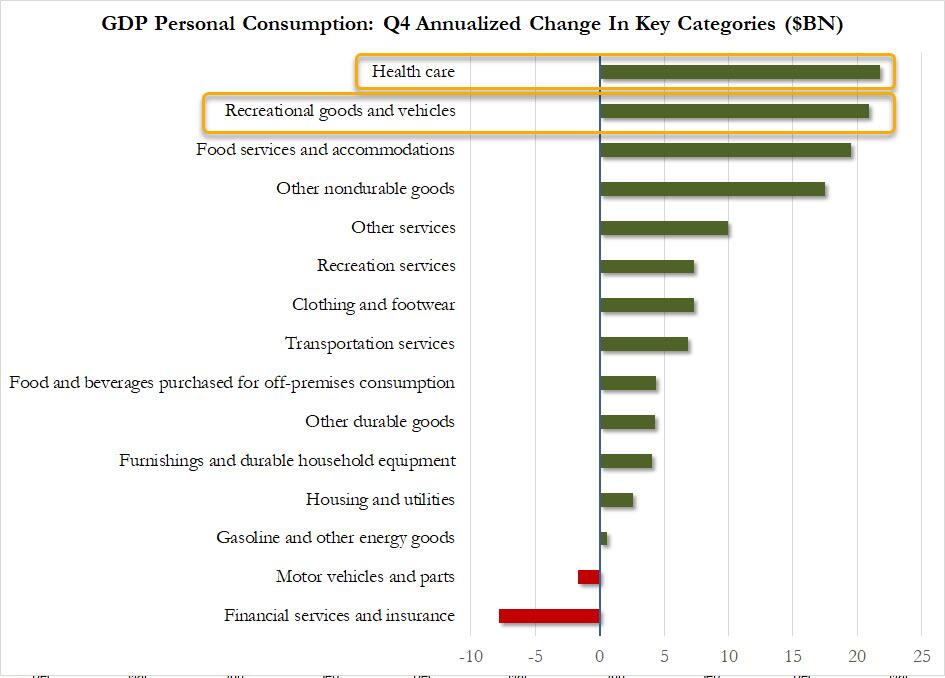

The increase in consumer spending reflected increases in both services and goods. Within services, the leading contributors were food services and accommodations as well as health care. Within goods, the leading contributors to the increase were other nondurable goods (led by pharmaceutical products) as well as recreational goods and vehicles.

Keep that last in mind for a minute, we’ll revisit it shortly: Finally, “the increase in exports reflected increases in both goods (led by petroleum) and services (led by financial services).”

That said, Q4 GDP was below Q3, and according to the BEA, the “deceleration in GDP in the fourth quarter primarily reflected slowdowns in inventory investment, federal government spending, housing investment, and consumer

spending. Imports decelerated.”

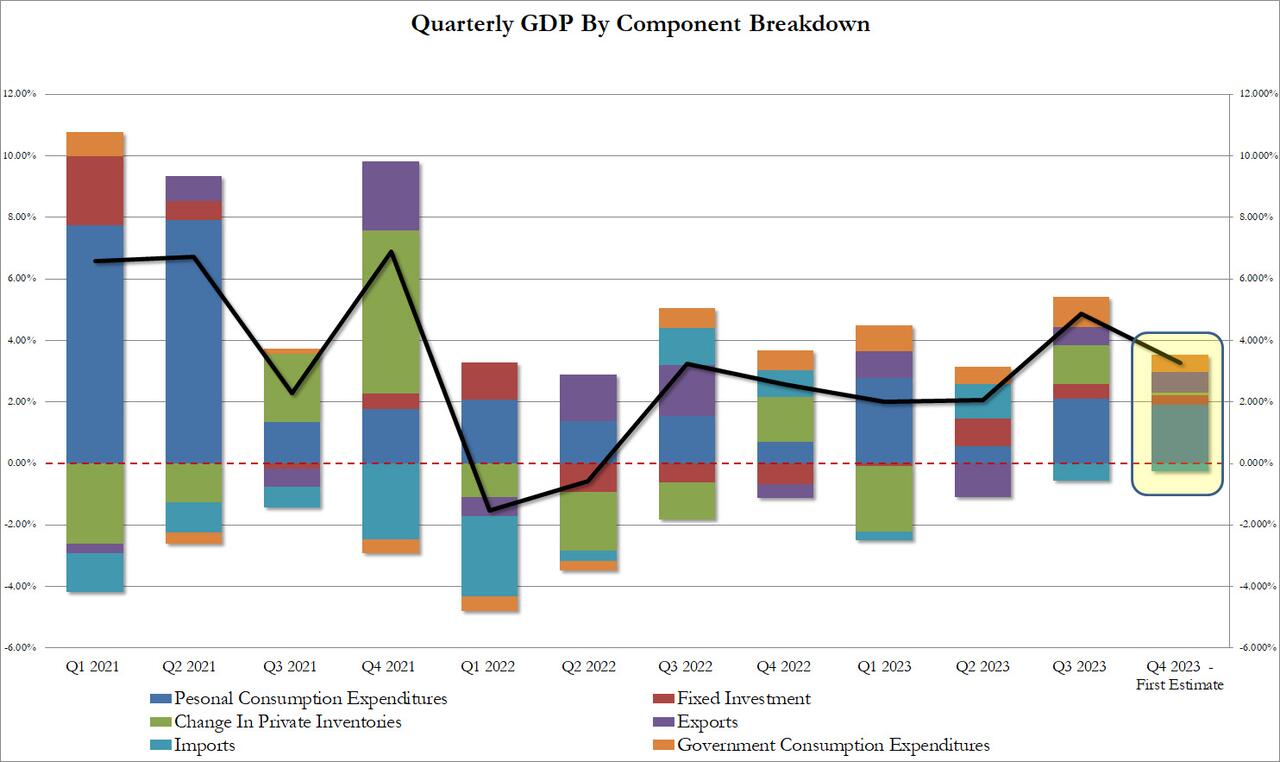

A more granular analysis reveals the following details:

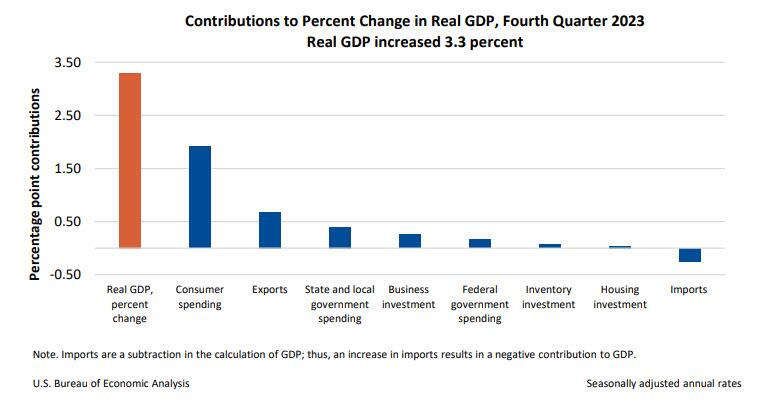

- Personal consumption contributed 1.91%, more than half of the 3.280%. On an annualized basis, this amounted to a 2.8% increase, better than the 2.5% expected, but down from 3.1% last quarter.

- Fixed Investment also dipped, adding 0.31% to the bottom line number, down from 0.46% in Q3

- The change in private inventories was flat, contribuing 0.07% of the bottom line number, and denying expectations of a decline due to Q4 destocking after last quarter’s 1.27% inventory change surge.

- Also in the unexpected column was the contribution from net exports, which added 0.43% to the bottom line number, up from 0.03% last quarter, as exports supposedly surged despite the sharp jump in the dollar in Q4.

- Finally, government contributed another 0.56% of the bottom line number, which while down from 0.99% in Q3, has continued a bizarre series where government remains one of the largest GDP contributors.

And visually:

Turning to the all important consumption, we can’t help but smile when noticing that the BEA is again resorting to such favorite GDP-boosting gimmicks of the old Obama administration as spending on healthcare and… RVs! The two contributed to roughly half the growth in consumer spending in the fourth quarter.

Hilarious RV spending spree aside (although in Biden’s economy nobody can afford a house so it does make sense), some of the beat was also a function of a lower-than-expected deflator, which also impacted the unexpected positive contribution from exports which, again, made no sense in light of the much stronger dollar.

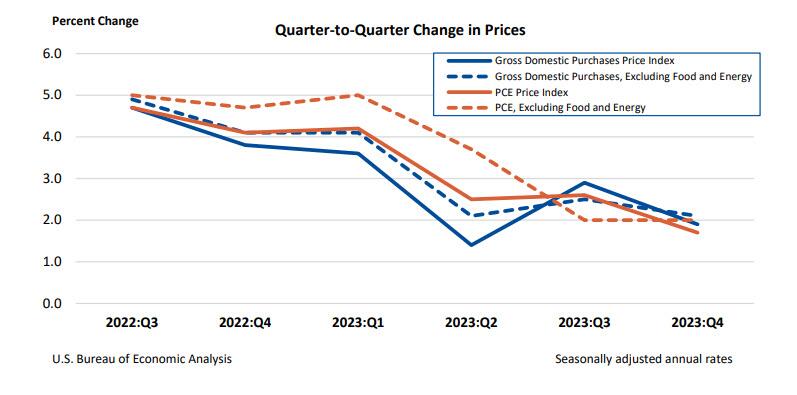

Turning to the inflation components, core PCE inflation was in line, which is what matters for the Fed, however this number was stale and we will get a more accurate, monthly not quarterly, print tomorrow. Specifically, Personal consumption expenditures (PCE) prices increased 1.7% in the fourth quarter after increasing 2.6% in the third quarter. Excluding food and energy, the PCE “core” price index increased 2.0%, the same increase as in the third quarter, and in line with estimates.

Finally, real disposable personal income (DPI) – personal income adjusted for taxes and inflation -increased 2.5% in the fourth quarter after increasing 0.3% in the third quarter. Current-dollar DPI increased 4.2% in the fourth quarter, following an increase of 2.9% in the third quarter. The increase in the fourth quarter reflected increases in compensation, personal income receipts on assets, and proprietors’ income that were partly offset by a decrease in personal current transfer receipts.

One can also argue that much of the spending came from the continued drain of savings, and one would be right: personal savings as a percentage of DPI was 4.0% in the fourth quarter, compared with 4.2% in the third quarter. This number will keep dropping.

Overall, as Bloomberg concludes, one can argue that the GDP figure was fairly neutral for markets, as private domestic demand was largely in line with forecasts, as was core inflation.

Tyler Durden

Thu, 01/25/2024 – 09:21

via ZeroHedge News https://ift.tt/npijloU Tyler Durden