Europe’s Super-Stock Envy Feeds Mag Seven Monikers

By Michael Msika, Bloomberg Markets Live reporter and strategist

The US has the Magnificent 7 tech giants charming investors and driving up valuations. Europe — depending on which strategist you ask — has the Seven Wonders, the Super 7 or the GRANOLAS.

The Mag 7 imitators highlight Europe’s unfulfilled ambitions for its own supergroup of stocks. The continent’s companies are hobbled by relatively lower earnings, sluggish economic growth and this cycle’s heavy preference for US big tech — all curbing the Stoxx Europe 600’s returns to about half of those on the S&P 500 in 2024. Nevertheless, Europe has some strong arguments.

“These monikers are a great way to remind investors that there’s attractive stocks in Europe too, and at cheaper valuations than in the US,” says Citigroup strategist Beata Manthey. As a consequence of the zero-rates era when US growth stocks were “the natural place to flock to,” Europe now has solid, yet “underestimated” companies, she says.

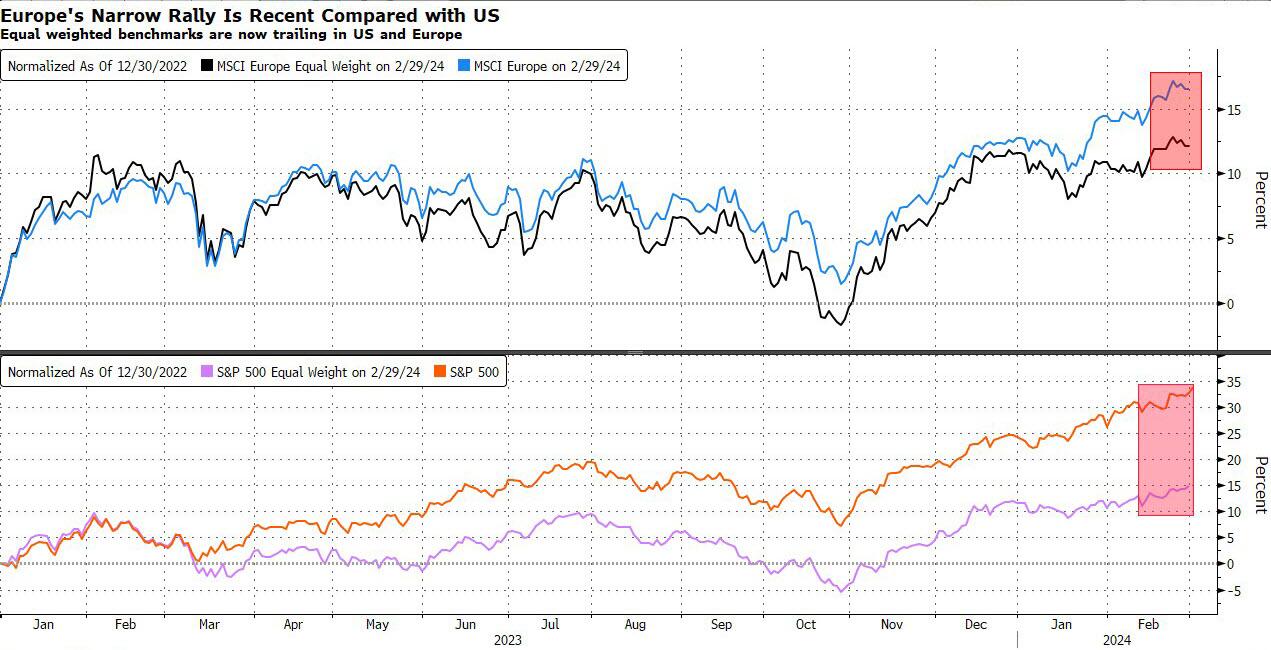

The strategist adds that in contrast to the US, it’s unusual for Europe to showcase a narrowing market — where growth is concentrated in a select number of stocks. This could be good news, however, as historically stocks tend to rise in the 12 months following narrowing episodes, albeit with higher volatility.

The US has the Magnificent 7 tech giants charming investors and driving up valuations. Europe — depending on which strategist you ask — has the Seven Wonders, the Super 7 or the GRANOLAS. The Mag 7 imitators highlight Europe’s unfulfilled ambitions for its own supergroup of stocks. Beata Manthey, Citigroup Global Markets Global Equity strategist discusses with Francine Laqua on Bloomberg Pulse.

As the market rally could stay narrow, Manthey has identified European megacaps who could be the continent’s own Magnificent 7. Her “Super 7” includes Novo Nordisk, ASML, LVMH, SAP, Schneider, Richemont, and Ferrari. These stocks are cheaper than the Mag 7, offer similarly attractive margins and have underperformed the Mag 7 by 70% since the start of 2023, “leaving room for catch-up,” she says.

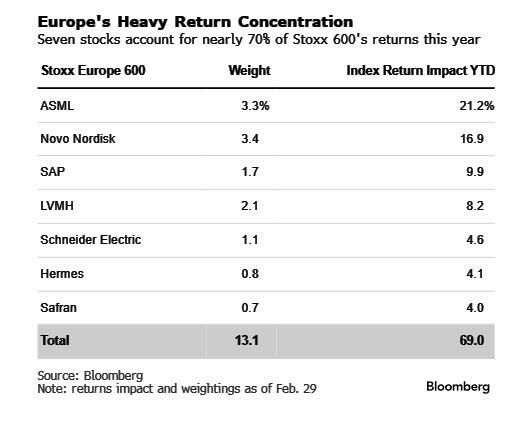

As shown in the chart above, seven stocks have accounted for nearly 70% of the Stoxx 600’s 3.3% rally this year. Across the pond, the Magnificent 7 account for 23% of the S&P 500’s market cap and 50% of returns year to date. The US group is up 14% YTD, more than twice the return of the benchmark.

In Europe, the list of would-be super-stocks varies from one strategist to another, with some core large caps always present. Societe Generale strategists, led by Roland Kaloyan, have coined the “Seven Wonders of Europe,” including Novo Nordisk, ASML, LVMH, SAP, Siemens, Schneider and Hermes. It touts the “earnings champions” as global players with limited domestic exposure, which are more diversified than the Mag 7.

SocGen strategists say the rising weight of megacaps is becoming an issue at the country level, as big stocks approach funds’ limits. “Few investors are comfortable with dedicating more than 10% of their funds to a single stock, if they are even allowed to, a threshold recently reached by ASML in the Euro Stoxx 50,” they say.

Europe’s 10 largest caps now account for over 20% of the Stoxx 600, getting close to the peak of 22% reached during the tech bubble in 2000. While large caps have carried the benchmark’s performance, European equities continued to suffer outflows, shedding $8 billions this year, while US peers gained $13 billion in inflows, EPFR Global data show.

But let’s give to Caesar what belongs to Caesar: Goldman Sachs strategists created a megacap acronym for Europe back in 2020, during the first lockdown. GSK, Roche, ASML, Nestle, Novartis, Novo Nordisk, L’Oreal, LVMH, Astrazeneca, SAP and Sanofi have since been the “GRANOLAS.” The group has performed like the Mag 7 since the start of 2022, with half their volatility, and are 30% cheaper.

“The GRANOLAS exhibit qualities that we expect to predominate in this cycle: strong earnings growth, low volatility, high and stable margins, and strong balance sheets,” say strategists including Guillaume Jaisson, who remain overweight the group. “They also stand to benefit from the structural shift toward passive investment and the lack of liquidity in the European equity market.”

Tyler Durden

Sat, 03/02/2024 – 09:20

via ZeroHedge News https://ift.tt/D2tdNeU Tyler Durden