Is Gold Warning Us Or Running With The Markets?

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

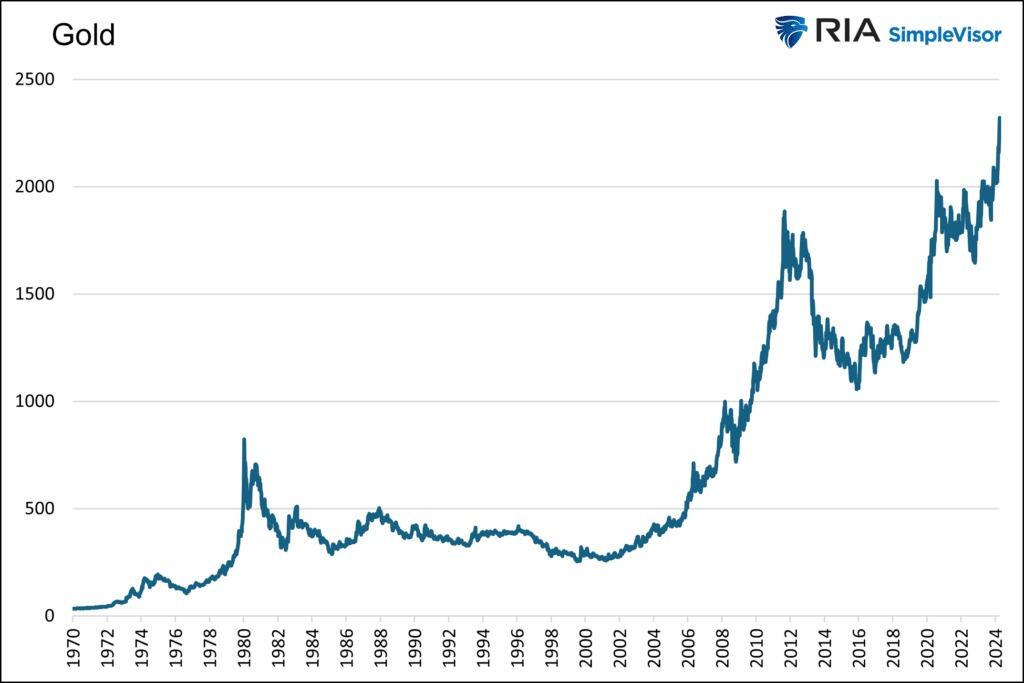

Having risen by about 40% since last October, Gold is on a moonshot. Many investment professionals consider gold prices to be a macro barometer, measuring the level of anxiety in the economy, inflation, currency, and geopolitics. Therefore, we must investigate what is and isn’t driving the price of gold higher.

The Divorce Between Gold and Real Yields

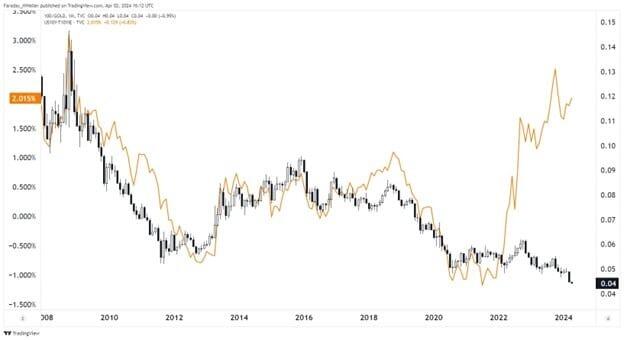

To help us figure out what may be driving the momentum in Gold, it is worth first considering that a trusty relationship that largely explained the movement in gold prices broke down about two years ago.

The graph below, courtesy of Matt Weller, shows the 15-year-old correlation between gold prices and real yields is not working. Real yields, or rates, are simply the current yield of a Treasury bond minus the rate of inflation or expected inflation.

It serves as a measure of how loose or restrictive monetary policy is. The higher the real yield, the more restrictive monetary policy is, and vice versa.

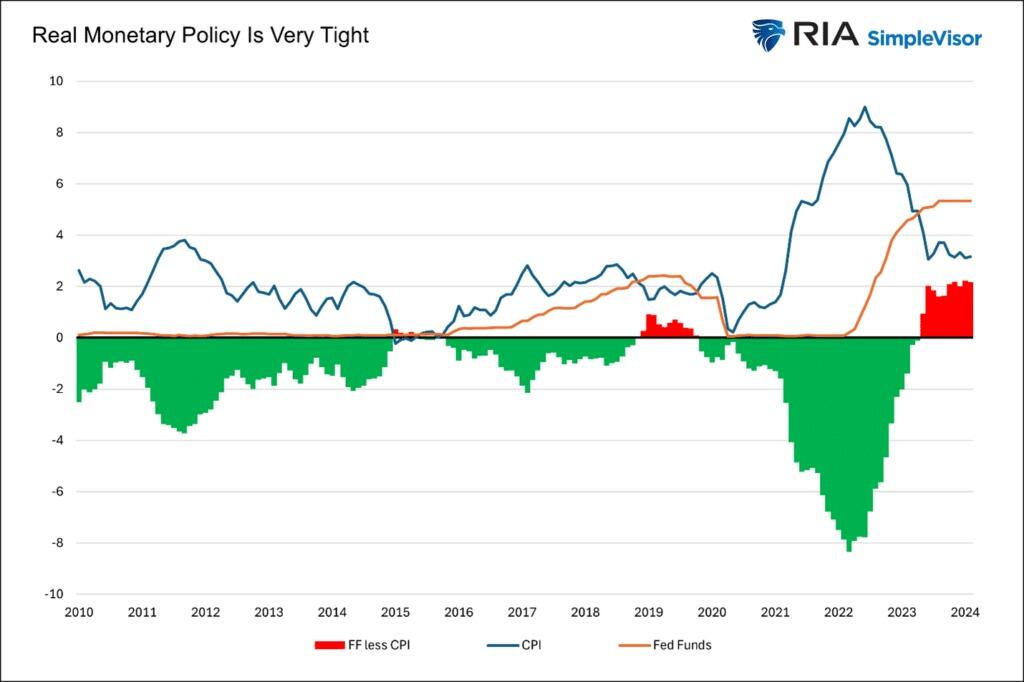

The graph below shows the current level of real yields, which is the highest in fifteen years. Accordingly, it’s fair to claim that monetary policy is very restrictive, regardless of how the Fed may have shifted its stance in recent months.

In our article The Feds Golden Footprint we discussed why the relationship between Gold and real yields exists.

The level of real interest rates is a sturdy gauge of the weight of Federal Reserve policy. If the Fed is treading lightly and not distorting markets, real rates should be positive. The more the Fed manipulates markets from their natural rates, the more negative real rates become.

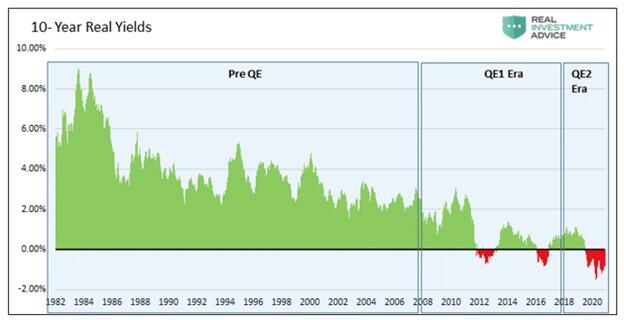

The article shared our analysis, which divided the last 40 years into three periods based on the level of real yields.

As the Fed’s monetary policy became more aggressive in 2008, the relationship between Gold and real yields grew. Before 2008, there was no statistical relationship.

Per the article:

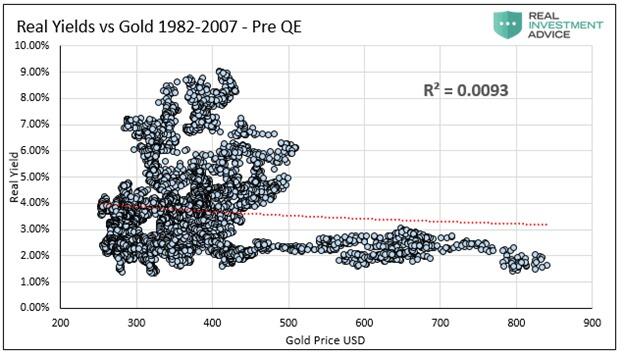

The first graph, the pre-QE period, covers 1982-2007. During this period, real yields averaged +3.73%. The R-squared of .0093 shows no correlation.

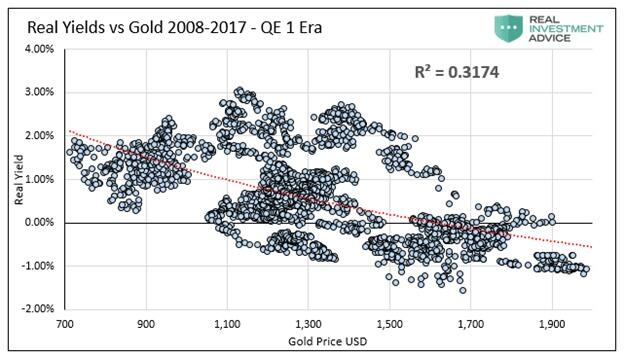

The second graph covers Financial Crisis-related QE, 2008-2017. During this period, real yields averaged +0.77%. The R-squared of .3174 shows a moderate correlation.

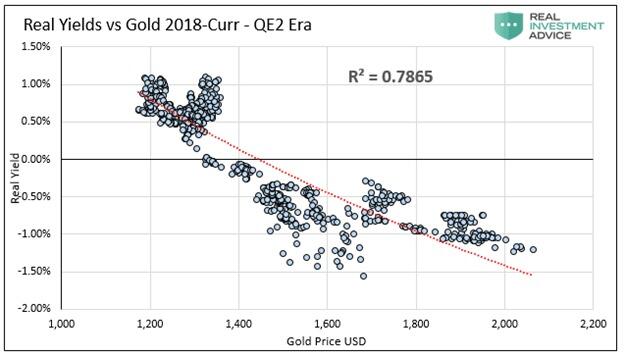

The last graph, the QE2 Era, covers the period after the Fed started reducing its balance sheet and then sharply increasing it in late 2019. During this period, real yields averaged 0.00%, with plenty of instances of negative real yields. The R-squared of .7865 shows a significant correlation.

Given our historical analysis and the current instance of high real yields, it is unsurprising that the relationship between the price of Gold and real yields has faded.

Therefore, without real yields steering the price of Gold, let’s consider a few possibilities for why it is rising so rapidly.

Fiscal Imbalance

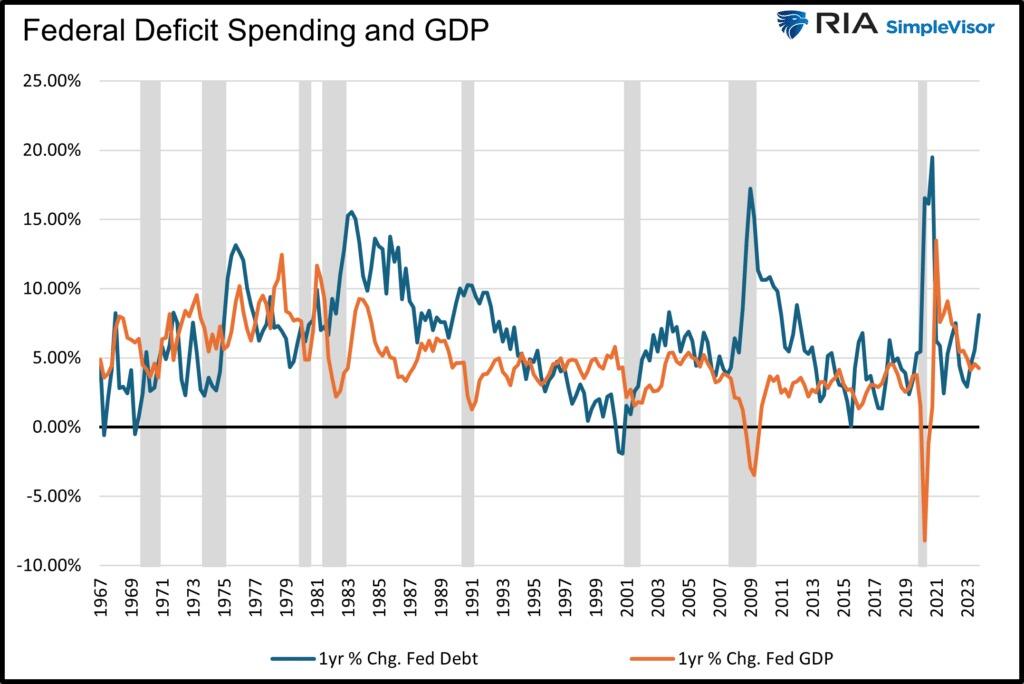

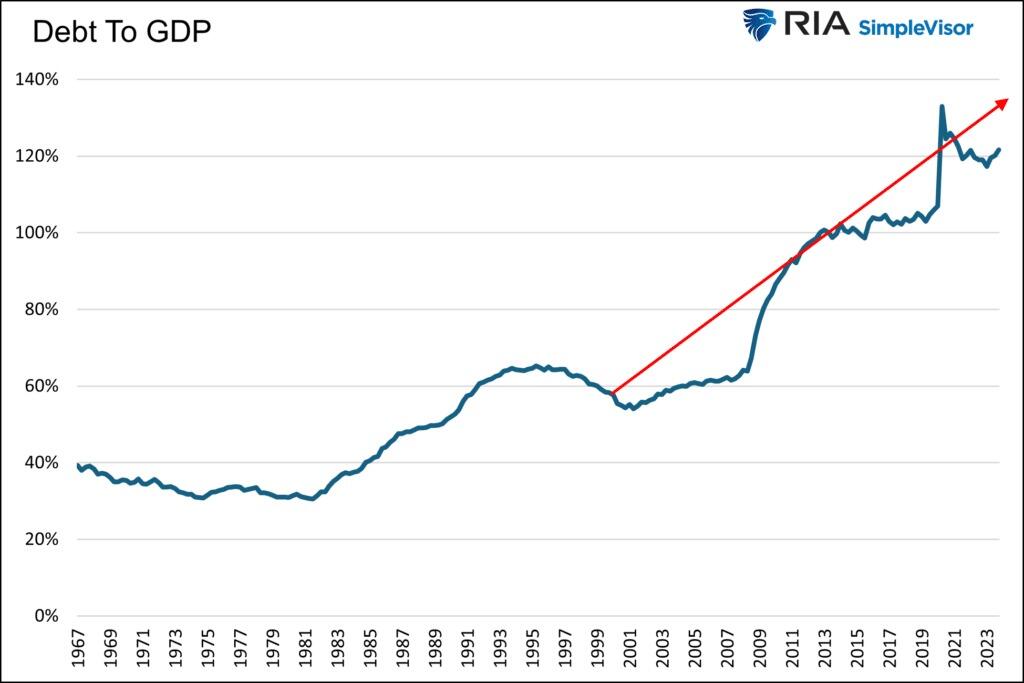

The Federal government is running large deficits. As shown below, the annual percentage increase in federal debt is over 8%. Such significant deficit spending occurs as economic growth is running above its natural growth rate and pre-pandemic levels. Typically, deficits tend to be lower during periods of economic growth and bigger during recessions or economic slowdowns.

The recent increase in debt growth is significant, but not much more so than other non-recessionary peaks in the last ten years. Additionally, it is well below the debt increases associated with recessions. A $2+ trillion-dollar deficit sounds daunting, but the economy has grown by 33% or $7 trillion since 2020 and doubled in size since 2009. The graph below, showing the debt-to-GDP ratio, helps put more context on the rate at which the government borrows.

The upward trending debt to GDP ratio is not sustainable. However, the current ratio and slope of the recent trend align with the trend going back 20 years and even longer.

We have written many articles on the problem of debt growing faster than GDP and the economic damage it is doing and will do. However, when putting current deficits into proper context with the pace of economic activity, the recent growth is not glaringly different from other experiences of the last 20 years.

As such, we find it hard to believe that debt is responsible for the recent run-up in Gold.

Geopolitical

Geopolitical problems, especially regarding Ukraine and Israel, are indeed problematic.

Russia could deploy nuclear weapons or expand the war to other neighboring countries. An invasion of a NATO country would all but force involvement from the U.S. and European powers.

The Israeli-Hamas conflict appears to be a proxy war with Iran. While the theater of war is primarily in Gaza and, to a lesser degree, surrounding countries, the possibility of more direct involvement between Israel and Iran is problematic. Direct Iranian actions against Israel would likely be met with military force from the U.S. and other NATO powers.

Not to minimize the two geopolitical events and other less critical ones, but the U.S. and Europe have been in various wars in the Mideast and Afghanistan for most of the last 20 years. Is today’s global geopolitical situation much more frightening than in years past?

As we started writing this on April 4, 2023, a rumor circulated that Iran might be planning missile attacks against Israel. The S&P 500 fell by over 1% rapidly, and Gold promptly gave up $25. If geopolitical concerns are responsible for the recent gains, shouldn’t increasing tensions in the Middle East further add to Gold’s value?

Gold Predicts Inflation, Or Does It?

Some argue that Gold prices are warning that the lower inflation trends of the last 30 years are reversing.

If Gold is such a good predictor of prices, why did the price go nowhere when the Fed and government were raining money on the economy and supply lines were shut down? That period represents the most significant inflationary setup in over 40 years.

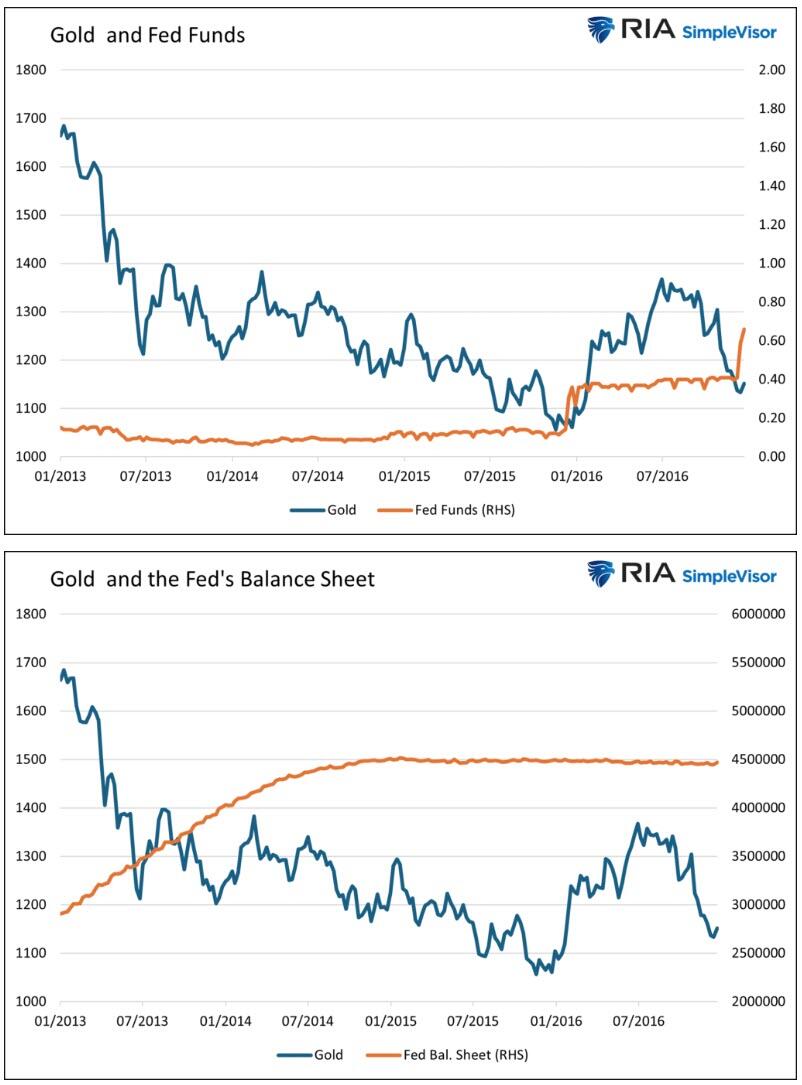

Dovish Fed In High Inflationary Environment

Since late last year, the Fed has flipped from an uber-hawkish tone to a more dovish one. Despite easy financial conditions (LINK), high and sticky inflation, and above-average growth, the Fed seems intent on cutting rates multiple times this year. Many would argue that a more prudent Fed would keep its hawkish tone and possibly raise the specter of increasing rates further.

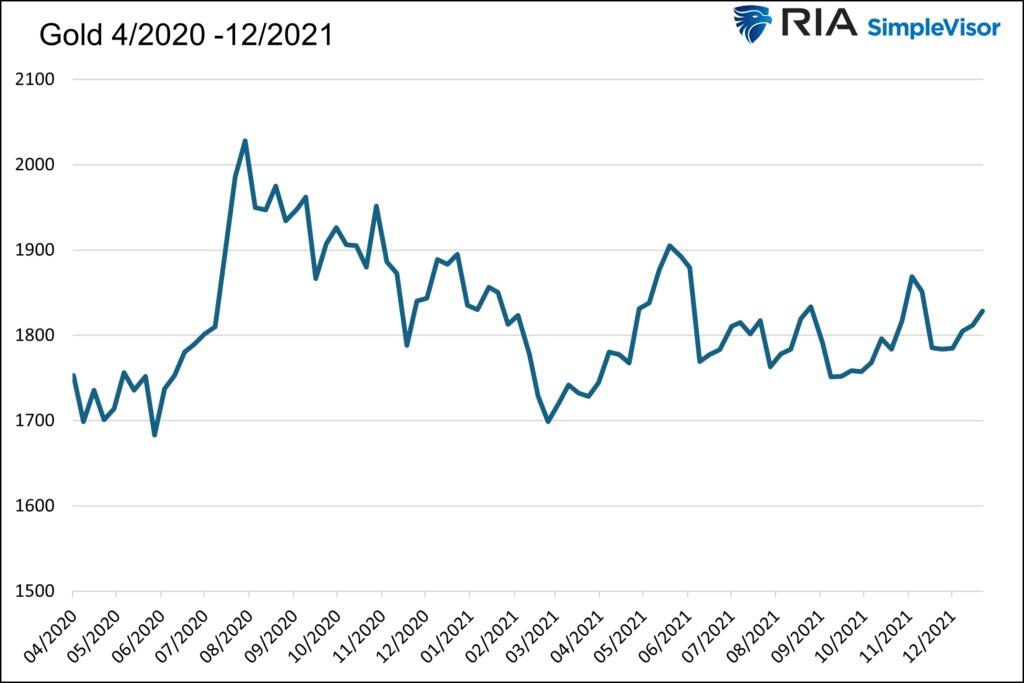

As we showed earlier, monetary policy, while seemingly becoming easier, is still at its tightest levels in over 15 years. Compare monetary policy today to that in 2013 and 2014. The economy was growing then, yet the Fed had rates pinned near zero percent and was doing QE. As we share below, Gold languished during that period, despite complete monetary policy carelessness.

Crypto – AI Mania

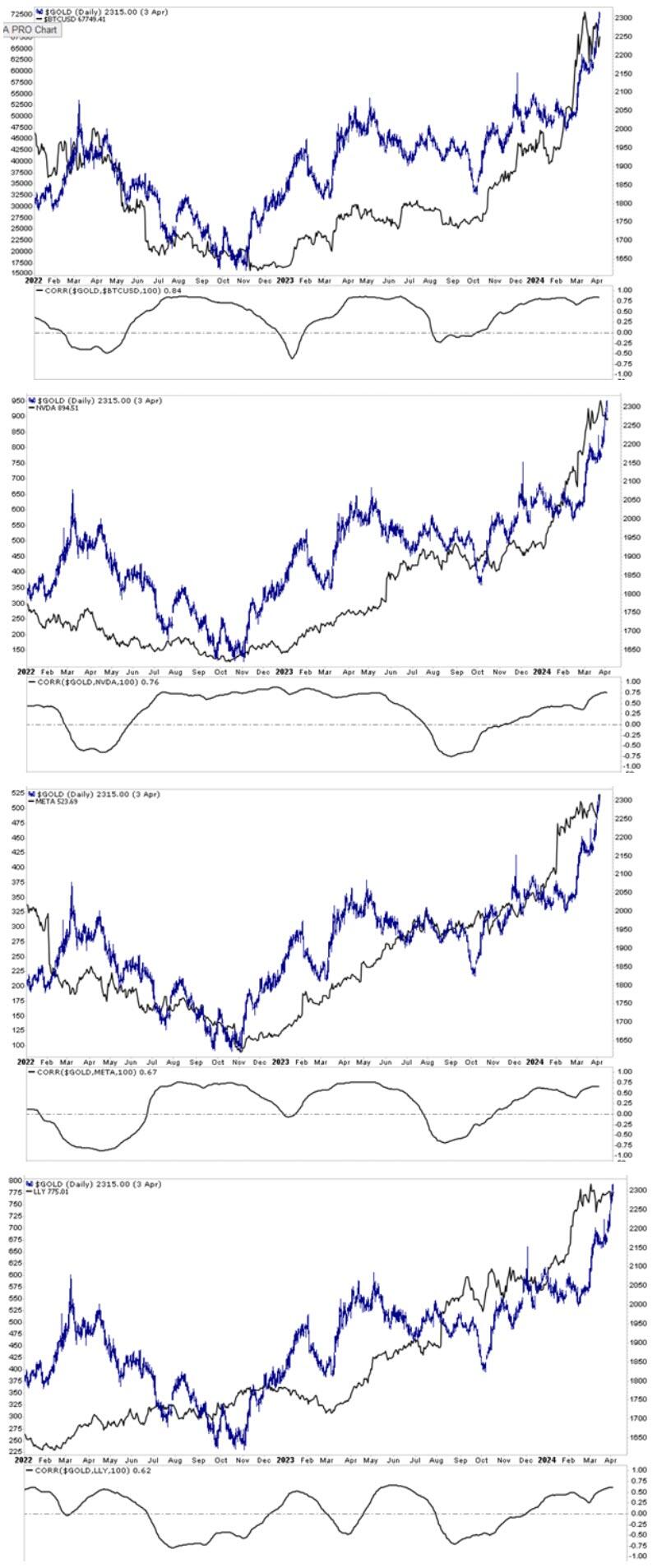

Having discussed a few of the standard responses pundits are spewing regarding Gold’s ascent, we share one that may not be as popular with gold holders.

Gold is a speculative asset. Accordingly, it can rise and fall, and at times violently, based solely on the whims of traders and speculators.

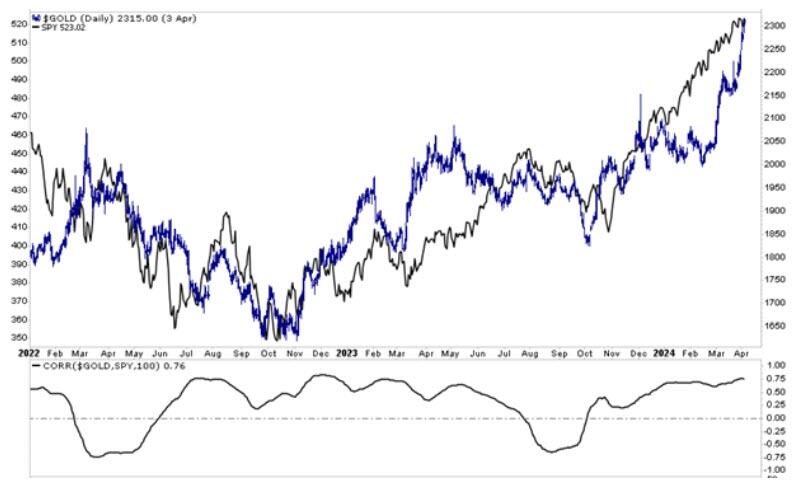

Might the current surge in Gold be less a function of the issues we raise above and more about the speculative mania flowing through many markets? Consider the five graphs below. The graphs show a solid visible and statistical correlation over the last two years between Gold and Bitcoin, Nvidia, Meta, Eli Lily, and the S&P 500.

Summary

The previous few sections share some typical rationales to justify higher gold prices. While they sound like legitimate reasons for Gold to soar, when taken into context, they are not that different from other periods in the last twenty years when Gold was flat or trending lower in price.

The price of Gold can provide valuable insights at times. But other times, Gold can give false signals warped by irrational market behaviors. We think Gold is getting caught up in a speculative bubble, and its price is not presenting us with a warning of fiscal, monetary, or geopolitical crisis.

Gold is likely to have a more reliable and sustainable run higher when the Fed returns to its careless ways with real yields near 0% or even negative, and QE is again in operation.

Tyler Durden

Wed, 04/10/2024 – 12:25

via ZeroHedge News https://ift.tt/XauW3mo Tyler Durden