A Historic Short Squeeze In Oil Has Only Begun

Last weekend, we warned readers that according to the latest data from Goldman Sachs, a massive short squeeze in energy stocks was on deck.

Goldman: Watch For A Massive Squeeze In Energy After The Biggest Shorting Frenzy In Five Years https://t.co/xNHCZkIPo0

— zerohedge (@zerohedge) September 29, 2024

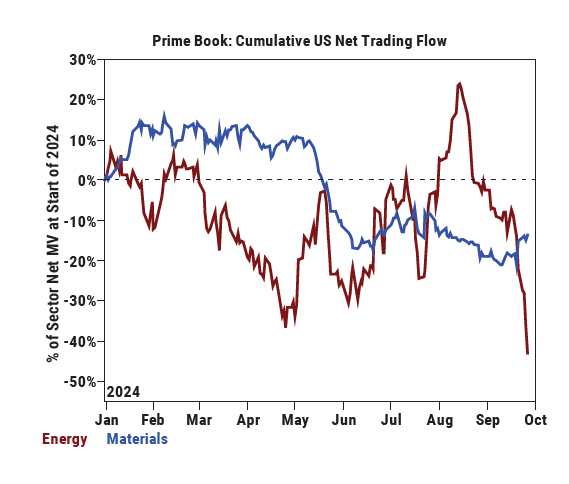

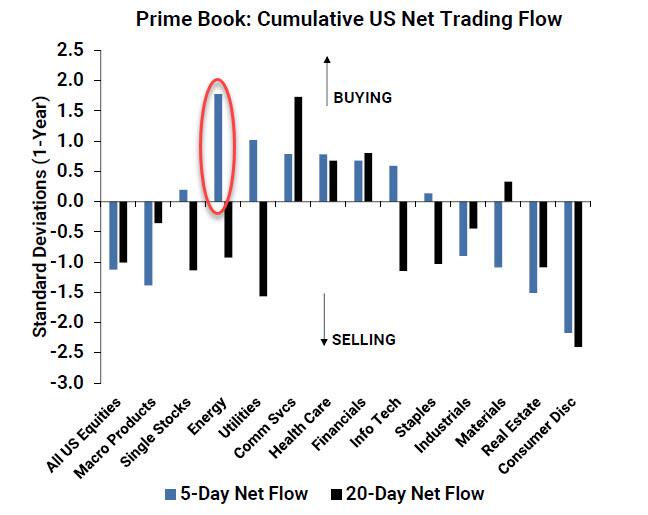

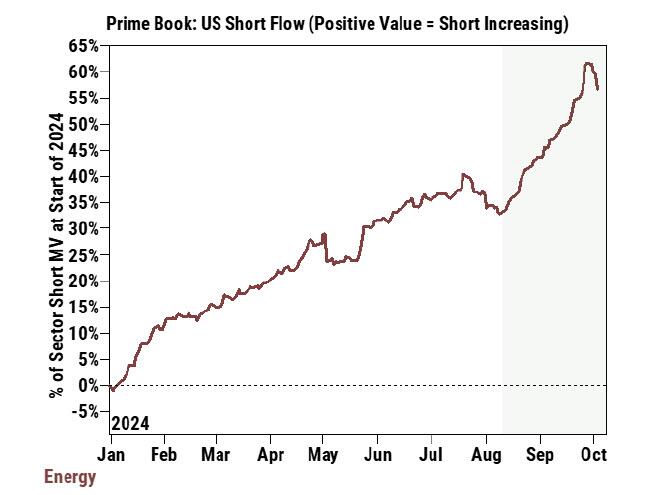

Specifically we noted that at a time when funds were the most short oil on record, the broader energy space “was the most net sold sector” on the Goldman US Prime book, “driven entirely by short sales, which outpaced long buys (6.4 to 1).”

And here, we said, was “the hint to the next mega squeeze” as the recent short selling in energy was the largest in over 5 years.

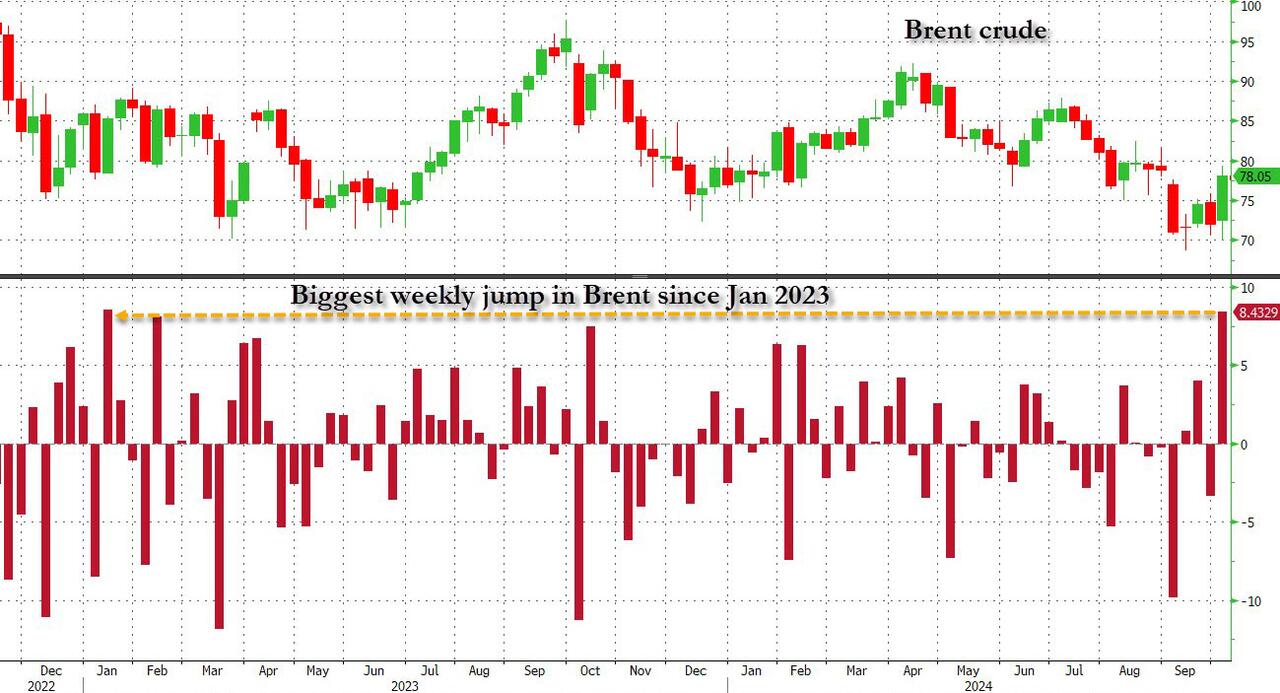

What happened next was for the history books, as Brent crude soared the most in almost two years on the back of what was a historic market imbalance with record shorts suddenly starting to run for cover…

… with the Kamala lackeys at Bloomberg going so far as to mock those who actually did the right thing and trade ahead of the inevitable squeeze as “tourists”, when in reality the only tourists here are those who expected the ridiculous plunge in oil prices to persist despite Cushing approaching tank bottoms (Bloomberg’s message is loud and clear: keep shorting oil unless you want to be branded a “tourist”, especially since a spike in oil – and gas – prices may adversely impact its favorite presidential candidate).

Unfortunately for Bloomberg, the squeeze in energy is just getting started, and not just due to fundamentals.

Crude oil soared last week as a result of the rapidly deteriorating situation in the middle east. On Tuesday, spot month WTI and Brent rallied >5% from the lows on the initial headlines from the White House that an Iranian attack was imminent. Goldman’s research desk noted on Tuesday that the jump in oil prices reflected a moderate risk premium as actual production disruptions have been limited and spare capacity remains elevated. The energy complex jumped again Thursday on news that the US was considering whether or not to support Israel’s potential retaliatory attacks against Iranian energy infrastructure.

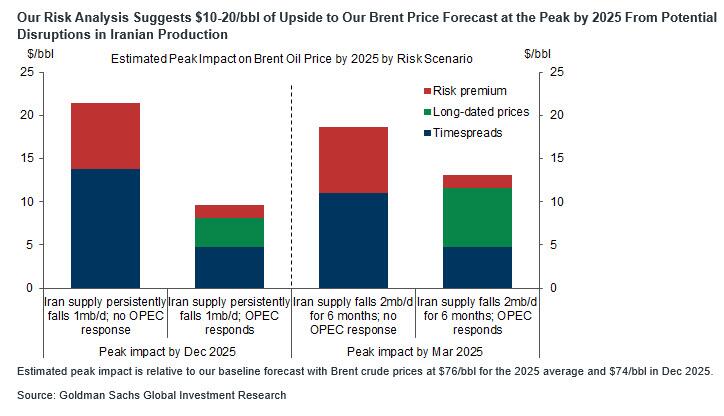

Then, over the weekend, the bank’s commodity analysts published a new report (available to pro subs) in which they tried to calculate the impact on the price of oil should Iran oil output be “limited” by Israel, to wit:

- Assuming a 2mb/d 6-month disruption to Iran supply, we estimate that Brent could temporarily rise to a peak of $90 if OPEC rapidly offsets the shortfall, and a 2025 peak in the mid $90s without an OPEC offset.

- Assuming a 1mb/d persistent disruption to Iran supply, reflecting for instance a tightening in sanctions enforcement, we estimate that Brent could reach a peak in the mid $80s if OPEC gradually offsets the shortfall, and a 2025 peak in the mid $90s without an OPEC offset.

But it’s not just fundamentals: Goldman’s Prime Brokerage wrote in its latest weekly must-read note (also available to pro subs) that “after heightened geopolitical tensions and rising crude oil price, HFs reversed course and net bought US Energy stocks for the first time in 7 weeks, driven almost entirely by short covers.”

As a result, the US Energy long/short ratio increased +5% – the largest weekly increase in nearly 5 months – to 1.36, which is in the 69th percentile vs. the past year and 14th percentile vs. the past five years.”

That said, the short overhang in energy remains staggering, and hints at a far more brutal unwind once the upward momentum persists for another week, and not only in energy stocks where the short flow on Goldman’s Prime Broekrage is just shy of record highs…

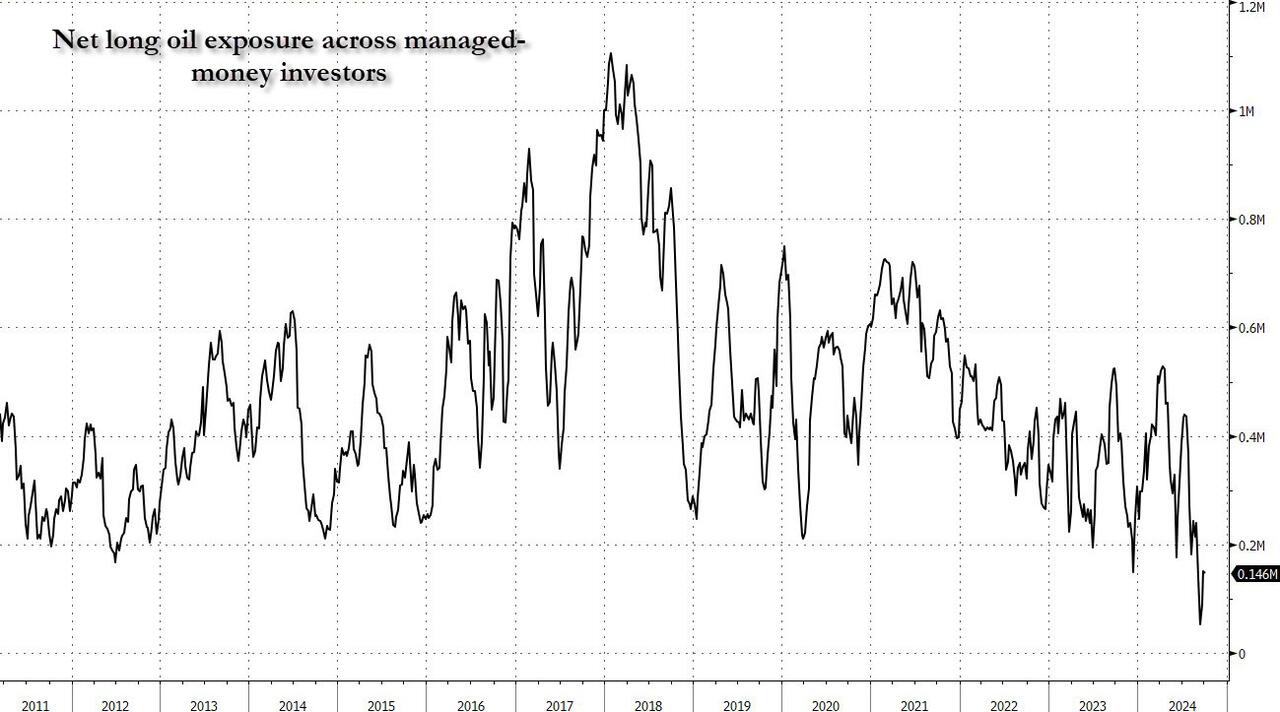

… but also in the oil patch, because after oil short interest hit a record two weeks ago as traders turned the most bearish on oil they have ever been, the amount of short covering was virtually non existent, and net managed-money (i.e., hedge fund) exposure across the 4 main oil contracts (Nymex and ICE WTI, Nymex and ICE Brent), is barely above its record lows!

Putting it all together, Goldman Energy specialist Ryan Novak writes that “energy led to the upside on the week after we exited the prior week with aggressive PB selling/short selling that flipped this week, managed money positioning remains short – at all-time lows and tensions across the Middle East escalating with Israel beginning its ground invasion. E&Ps led on the week +7%. All eyes on any incremental news regarding any attack on Iranian energy infrastructure which would pose further upside risk to the commodity and equities.”

Bottom line: with record shorts now painfully squeezed as upward momentum has been ignited across the energy sector, and the risk of a flashing red headline that Israel has leveled Kharg Island looming, unwind of what until a week ago was a record short position in oil and energy stocks is just getting started. And that’s without Israel even doing anything. Should Israel however take the plunge and either take out Iran’s oil infrastructure or, worse, target its nuclear industry, then the coming explosion in oil will make the Volkswagen short squeeze of 2008 seem like quaint amateur hour.

More in the full notes available to pro subscribers here and here.

Tyler Durden

Sun, 10/06/2024 – 22:45

via ZeroHedge News https://ift.tt/vD9ipL8 Tyler Durden